Ayush,

The idea behind my query was to know your sell strategy because it looked perfect in this case. Definitely not interested in your personal or for that matter anyone’s trades. That’s why I didn’t tag you in my query so you could choose to avoid it altogether, unfortunately it became a popular query here and you answered it and thanks for that. You say you did some partial profit booking. So on what criteria/trigger point you do partial profit booking in micro caps. Because it looks like great strategy atleast in this case. Once again pls ignore this query if you feel it is personal. My query is mostly broad one, on how to make profit in small cap and more importantly how to retain it. I know you were one of early ones to spot this stock, and many of VPers jumped into it much much later, that’s the only reason posing this question to you. Thanks.

Hi @Yogesh_s ,

I’m not sure about the details just now but from what I had checked earlier, I don’t think there is cap on bringing back money from Vietnam. I think cos can pay-back by way of dividends. Cpl of examples that come to my mind are KCP (they are already getting dividends from their sugar operations in Vietnam) and CCL products. Taking a clue from the success of these cos in Vietnam and seeing that it has become a production hub for textile cos, I have been hoping for success for Premco.

@srinii_mm - As I was invested from much lower levels…I would have sold small qtys (5-10-15%) on sharp upswings. But overall it doesn’t makes great impact.

Regards,

Ayush

Ayush, Thanks for the response. Anyways I have sold out of this at 12% loss. So couldn’t come up with insightful queries. I was really hesitant to invest in this at first. But found your blog and your arguments so finally invested in it, Held for 2 yrs and sold at 12% loss. The moment I started finding better ideas, sucked up the pain and I just threw this one away and went away. Not everyone can coattail and make profit isn’t it ?

Please correct me if I am wrong, but one of the hallmarks of good companies is that they respond to and treat small and minority share investors well. Having attended a few AGMs and also having written to managements requesting information, I have found that companies which respond well and promptly are the ones who are eventually the best performers in my portfolio. I would like to also mention that in one particular packaging company that failed to respond to any queries I sent to the emails, I sold out the entire holding and am glad that I did. This was despite the fact that a very famous investor in India had a substantial stake in the company and had mentioned about it appreciatively in of his interviews. After my sale was complete, the stock crashed and reports of governance issues cropped up in websites like Moneylife about it. Not sure if I can mention the name of that company in this forum as I am relatively new here. But again, this is my personal opinion, and I would welcome views from other participants about small/minority investor relations with respect to the quality of management.

Poor performance from Premco continue even during Q3FY18.

Standalone for Last 5 quarter

| Rs Crore | 31-12-2017 | 30-09-2017 | 30-06-2017 | 31-03-2017 | 31-12-2016 |

|---|---|---|---|---|---|

| Standalone | |||||

| Income | 11.70 | 13.03 | 20.12 | 15.50 | 14.31 |

| RM Cost | 4.89 | 6.33 | 11.49 | 5.32 | 5.93 |

| Employee | 2.27 | 2.25 | 2.17 | 1.96 | 2.10 |

| Other expense | 2.93 | 2.93 | 3.33 | 3.88 | 3.56 |

| EBITDA | 1.61 | 1.52 | 3.13 | 4.34 | 2.72 |

| EBITDA % | 13.8% | 11.7% | 15.6% | 28.0% | 19.0% |

| Depreciation | 0.60 | 0.72 | 0.46 | 0.59 | 0.59 |

| Interest | 0.14 | 0.20 | 0.38 | 0.32 | 0.36 |

| Other income | 0.41 | 1.51 | 0.95 | -0.34 | 0.90 |

| 0.34 | |||||

| PBT | 1.28 | 2.12 | 3.24 | 3.10 | 2.68 |

| Tax | 0.40 | 0.50 | 0.71 | 1.14 | 0.81 |

| PAT | 0.88 | 1.61 | 2.53 | 1.96 | 1.87 |

Consolidate for last 5 quarters

| Rs Crore | 31-12-2017 | 30-09-2017 | 30-06-2017 | 31-03-2017 | 31-12-2016 |

|---|---|---|---|---|---|

| Income | 18.96 | 16.67 | 22.05 | 16.31 | 16.31 |

| RM Cost | 9.80 | 7.52 | 10.90 | 4.43 | 4.43 |

| Employee | 3.45 | 3.72 | 3.22 | 3.11 | 3.11 |

| Other expense | 3.85 | 3.36 | 4.36 | 4.54 | 4.54 |

| EBITDA | 1.86 | 2.07 | 3.57 | 4.23 | 4.23 |

| EBITDA % | 9.8% | 12.4% | 16.2% | 26.0% | 26.0% |

| Depreciation | 0.81 | 0.93 | 0.66 | 0.77 | 0.77 |

| Interest | 0.17 | 0.25 | 0.43 | 0.58 | 0.58 |

| Other income | 0.18 | 1.31 | 0.81 | -0.45 | -0.45 |

| PBT | 1.06 | 2.20 | 3.29 | 2.43 | 2.43 |

| Tax | 0.40 | 0.50 | 0.71 | 1.14 | 1.14 |

| PAT | 0.67 | 1.70 | 2.58 | 1.29 | 1.29 |

| Minority interest | -0.04 | 0.06 | 0.01 | -0.10 | -0.10 |

| Net profit after MI | 0.70 | 1.64 | 2.57 | 1.39 | 1.39 |

Vietnam (Derived from Consolidated less Standalone)

| Vietnam Operations | |||||

|---|---|---|---|---|---|

| Income | 7.26 | 3.64 | 1.93 | 0.80 | 0.80 |

| RM Cost | 4.91 | 1.19 | -0.59 | -0.89 | -0.89 |

| Employee | 1.18 | 1.48 | 1.05 | 1.15 | 1.15 |

| Other expense | 0.92 | 0.43 | 1.03 | 0.65 | 0.65 |

| EBITDA | 0.25 | 0.55 | 0.44 | -0.11 | -0.11 |

| Depreciation | 0.20 | 0.21 | 0.20 | 0.18 | 0.18 |

| Interest | 0.03 | 0.05 | 0.05 | 0.26 | 0.26 |

| Other income | -0.23 | -0.20 | -0.14 | -0.11 | -0.11 |

| PBT | -0.21 | 0.08 | 0.05 | -0.66 | -0.66 |

| Tax | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| PAT | -0.21 | 0.08 | 0.05 | -0.66 | -0.66 |

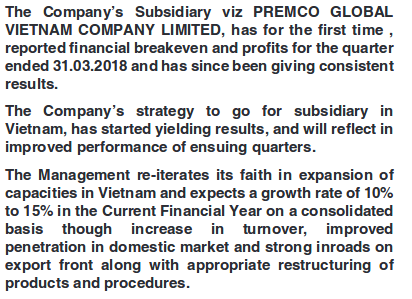

The company performance has been consistently deteriorating over last 4 quarters. In standlone operation, EBITDA margin improvement over Q2FY18 is the only silver lining in the financial. Vietnam operation also improving top line with recording highest ever quarterly sales of Rs 7.26 Cr. However, margin coninue to remain concern in Vietnam operation which turn negative in Q3FY18 after achieveing breakeven during Q2FY18. Vietnam employee cost also decline in Q3FY18 vis Q2FY18 despite growth in topline needs explanation.

In notes to accounts, the company did indicated reduction in duty drawback as one reason for deteriorated margin. However, there are many moving parts which currently appears to showing headwinds to the short term future of the company.

Disclosure: I have reduced my exposure by nearly 50% after Q2FY18. My view may be biased due to my investment. Investors shall do its own due diligence before making any decision.

The track record on Roe has been quite consistent over the last 10 years :

https://www.screener.in/company/530331/

Hoping that this is a temporary blip.

Disc :invested

Ayush bhai, would love to hear your pointers on how do we track such companies who barely make a news on the internet and we have to solely depend on the quarterly results and annual reports. How do we gauge whether this is a temporary blip ( as all good business will have a rough patch for a while ) or something serious is going on within the company?

Disc : Invested. Confused on whether this is the bottom of margins or not

@eyesice - i myself don’t know  . By being patient one gets rewarded in few stories while punished in some other. I have been interested in this one due to the high gross margins they have had and that they had already invested money in expansion but the execution has been terrible. Hoping that they will come back on track in sometime.

. By being patient one gets rewarded in few stories while punished in some other. I have been interested in this one due to the high gross margins they have had and that they had already invested money in expansion but the execution has been terrible. Hoping that they will come back on track in sometime.

When the entire focus was on TPP, we have so many schemes in India that have been impacted because of GST. Govt provides a lot of incentives to textile companies to promote exports - ROSL (Remission Of State Levies), MEIS (Merchandise Exports from India Scheme), duty drawback, interest subvention etc. Textile companies enjoyed a drawback rate of around 7%. Post-GST, it has been reduced to 2%.

There was no clarity on ROSL rates. Just before Gujarat elections, govt announced an increase in MEIS rate from 2% to 4% and also announced Post-GST rates for ROSL. And it’s effective till Jun 30th. There is no assurance of this continuing in the future. This clearly shows that GST was a hastily implemented plan without proper thought process behind so many things. So many small companies are struggling because of this.

According to WTO, once a country reaches export competitiveness, they go through a phase out period during which all export subsidies should be phased out gradually. USA has been continuously asking India to get away with such schemes. Whereas, on the other hand, exports have slowed down in last three years and textile associations have been requesting to provide incentives that were provided earlier. It seems all these companies have been lethargic. They always rely on subsidy to run the show. It tells us about the difficulties in this industry (as it always operates on low ROCE. Buffet has extensively mentioned this in his letters) and also about companies that are not open to operate more efficiently than they are now.

A company has a true competitive advantage when it has the ability to pass on it’s cost to end customers. If it is dependent on the Govt’s incentives to retain margins, then it becomes another commodity player. When the company mentions this as a primary reason in its notes section, then it is something to worry about. Because in the long run, these subsides may not be available. At the same time, if the difference in incentives is so high (above 5%), then Indian companies will obviously lose it to other countries like Vietnam, Bangladesh etc. Entire textile export from India will have a structural disadvantage. We have to wait and see if the company can improve its margins without any help from Govt schemes.

Scaling up from 10 Cr to 100 Cr, 100 Cr to 1000 Cr, 1000 Cr to 10000 Cr. All these require different skill sets. Initially, a company can skip a few processes. But when you scale up, implementing processes and following them diligently will play a vital role in growing big. Hopefully, management will learn from its mistakes.

Disc: Continue to hold

Sir, Could you share the names of companies which respond promptly?

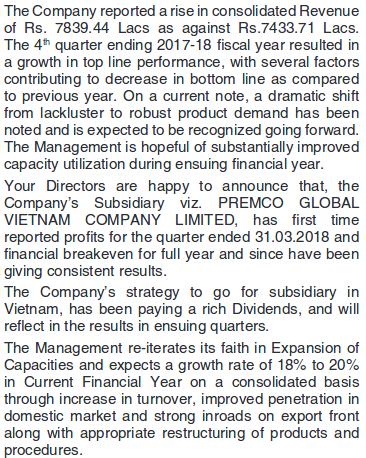

In the same report, the management has further added that in the last portion of the quarter gone by, the demand seems to have gone from “lackluster to robust product demand, which will be recognized in the near term.”

“PGL is optimistic on it’s future outlook on both domestic & international fronts”

@drravindra_2005 : The 27 cr turnover mentioned here, do we know how much more is the scope for the turnover to improve further (given the vietnam plant underwent expansion) ?

Sir, sorry for the delay, I had been unable to focus on markets of late due to various reasons. To answer your question, the three companies I had that responded very promptly were ttk prestige, titan, and madras cement. The companies that responded the worst to small investors were bilcare and champagne indage, got frustrated and exited those two latter stocks and am thankful that I did.

Management sounds positive and results are good after lot of bad quarters…things coming on track…

@ayushmit

Sir can you tell me the difference of standalone and consolidated revenues …what exactly it is?

Because the subsidiary revenues are shown as 10 crores in audit report , then what exactly revenue difference 21.38 - 18.28 i.e. 3.10 crores comes from?

Difference is due to additional revenues from the plant they had set up in Vietnam

But that has been mentioned in audit report attached as 10 crores…it’s not 3 crores…

Can it be safely assumed that Premco will benefit from the Vietnam plant but the growth won’t be similar to when the TPP was in place?

Notes from AR 2018

Link to AR: http://www.premcoglobal.com/reports/ANNUAL%20REPORT/ANNUAL%20REPORT%202017-2018.pdf.

Page 8:

Vietnam business will grow in coming quarters.

Dividend:

Final Dividend of Rs.3.00 per share for the financial year 2017-2018 on fully paid shares of 10/- each. (same as last FY)

Business focus : No changes in core business

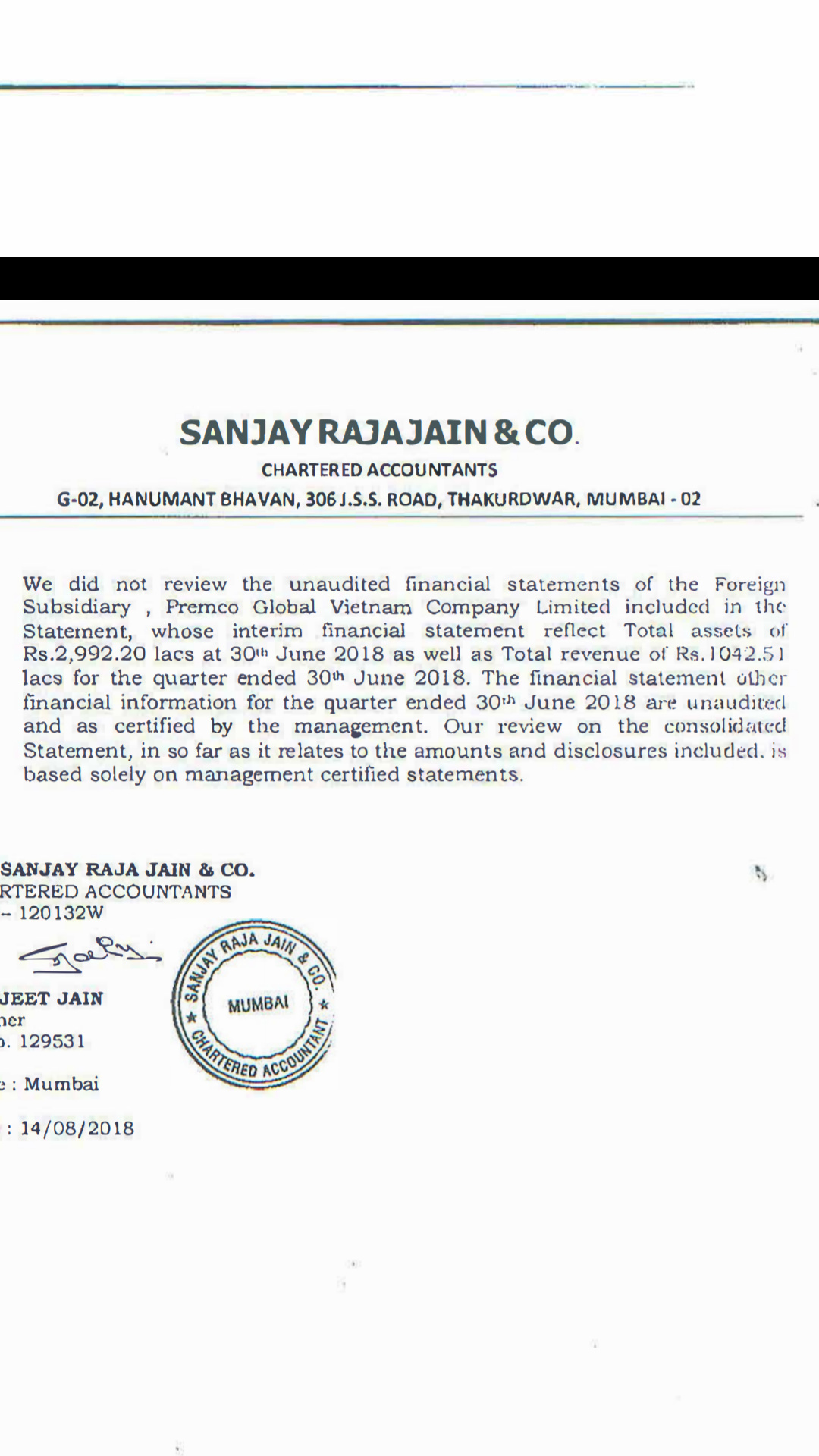

Auditor: M/s. Sanjay Raja Jain& Co., Chartered Accountants,

Single susidiary: Premco Global Vietnam Company Limited in which it holds 85%. No Joint Ventures/Associate Companies.

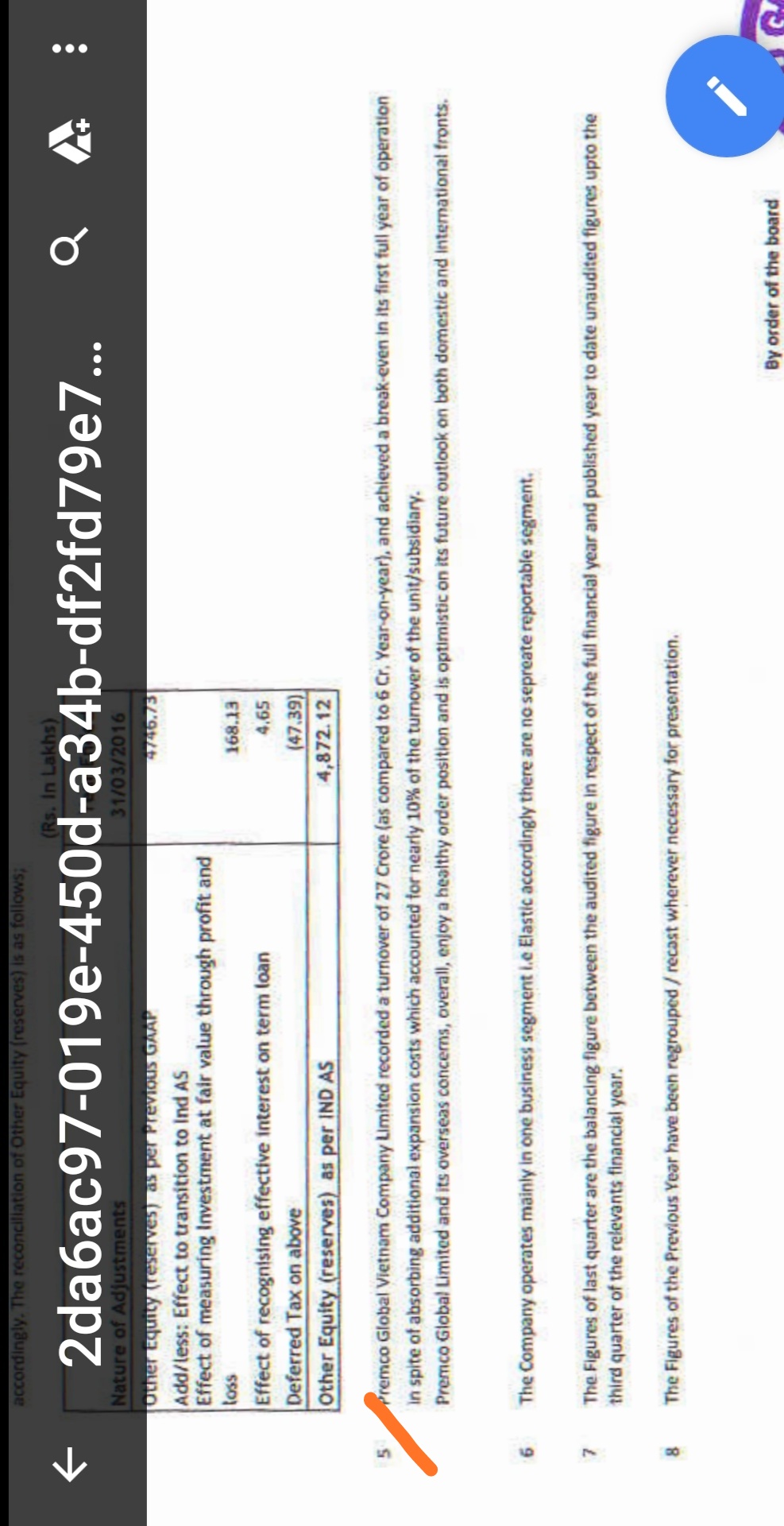

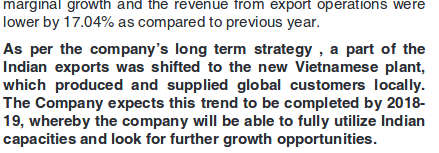

Why Lower revenue for standalone ?

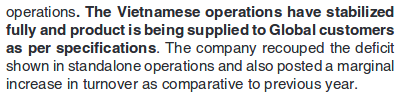

It is due to exports shifting to new Vietnam plant.

More on Vietnam

HR

I am new to AR reviews and focused mostly on mangament discussion and analysis

I feel the business would improve from now on going by the AR.

Inviting comments from seniors.

Disc: Invested. 5% of PF holding from higher levels and holding at loss. Added some recently after AR review.