Great thanks for your valuable work! I would say that more time should be spent on finding correct level of steel prices since that is single biggest driver. Additionaly, steel companies get compared on EV/EBITDA basis as EPS is not a correct metric over the complete cycle. Raw material security puts a floor to earnings and hence bankrutcy is not an outcome here like Tata Steel’s India ops even when steel prices collapse.

Steel Industry Analysis

WHY CHINA SNEEZES AND EVERY BODY GETS FLUE….?

I have tried to keep my analysis as simple as possible. (But it is quite lengthy)

As per the reports, the total steel production of the world in 2016 was 1630 MT out which production in China was 808 MT (Approx 50%). Steel consumption of the World in 2016 was 1515 Mt and consumption of China was 681 Mt (45%).

As on 1996 the Steel production of the world was 751 MT whereas of China was 101 MT (13.45%).

So in the last around 20 years the Steel production of the world has increased by 879 MT and that of China has increased by 707 MT i.e out of 879 MT increase in Steel production of world China alone has contributed 707 MT i.e around 80%.

Where does India Stand : Current Production of India is around 100MT i.e where China was in 1996.

Now why there is a buzz around Steel Industry…?? Answer…. China

In today’s time the reason for everything whether going up or down is one and only one i.e CHINA.

China is now forced to cut its production due to following main reasons :

- China has built excess capacity for Steel Production of 808 MT. China itself is the biggest Consumer of its own Steel and is also flooding the world with Cheap Steel. Now the Chinese economy is on slow down and other countries of the world have also restricted the import of Chinese Steel (through anti dumping, Minimum Import Price, Minimum Quality criterion etc). So now with the slow down of Chinese Economy and Import restriction by various question the question is what the Chinese will do of this 808 MT???.

Production capacity of 808 MT is a huge amount by any means and now the consumption of 808 MT is now causing a huge problem for China. For the sake of comparison, US and other European countries were developed countries in 2000 with very good infrastructure and at that time the total world production of Steel was only 850 MT. T

The point here is that the world including China had gradually developed steel production capacity till 2000 and hence its consumption was never a problem. Now in the last 15 to 20 years the production capacities increased by china is out of proportion. The moderately growing World Economy is not having such a huge apetite for Steel and hence till the time China was growing around 10% the steel capacities were a boon, however as the the Chinese economy is also slowing it is now turning out to be a curse.

Besides this the health of Chinese steel industries is also not very good because they were use to selling Steels at Cheap rates at Break even profit and at times also in loss. One interesting fact is that for production of steel China imports around 80% Iron Ore which is the major raw material for producing steel.

The Chinese Steel Companies are highly leveraged and most of them are also hidden Non Performing Assets in the books of their Bank. Thanks Chinese Central Bank did not had any one like RaghuRam Rajan. The Chinese financial sector will also be greatly impacted once the health of steel sector deteriorates further.

-

The level of pollution in China has reached to such an alarming situation that now they do not have any choice but to Shut down their polluting steel factories to reduce the alarming level of pollution.

As per Reuters “Official figures from China show it has cut 110 MT of legal steel capacity and 120 MT of illegal capacity since the start of last year, but the cuts are only now starting to translate into lower production. -

Now the most important thing: My analysis is that production and dumping of cheap steel by China had a huge (really very huge) environmental cost to China. We will have to understand that why is the cost of production so low in China and high in developed countries like US and Europe.

It is not that China is highly efficient in producing things at a cheap cost. Some of the the reason for lower cost of manufacturing in China as per my understanding are as under :

a). One of the major input cost is man power. The labor laws in developed countries is much more regulated and healthy which increase their cost of production. Due to high population man power resources are abundant and also available at very cheap rates and are therefore prone to expolitations.(We are all aware of labor exploitation in developing countries including India)

b) Environment and quality norms are very stringent in western countries where as China ranks amongst the poorest countries in this parameter. But how does this affects the cost of production???

i. Quality of raw material affects the level of pollution. For example burning of benefited or washed coal will have less pollution rather than raw coal. But coal beneficiation has some cost which increases the cost of coal. Same is it for other raw material, if you treat them as per norms before use, it will have less polluting impact but all this will increase the cost.

ii. The air and gases coming out of the chimney are required to be treated as per norms to reduce pollutants but again there is a cost attached to it.

iii. The water being discharged from factory needs to be treated before discharge and there is a cost included in the treatment of waste water.

iv. Mining which is being done should be as per environment clearance norms. etc etc

If a country does not follow above norms then definitely the cost of production will be very low and they will be very competitive with the world but the catch is that they are not calculating the expense which they are debiting to their environment.

We will have to understand and should not to take the problem of pollution in China as a passing by event. This is having a very- very serious impact and has caused irreparable damage to their environment. China has now realized this thing and now they are forced to cut down the production. As already mentioned that the Chinese were mad to an extent that they were selling steel at break even prices and even some time at loss to retain their market share. Had they calculated the cost that they are incurring on Environmental they would have never entered into a loss making proposition.

So the summary is that China Steel Industry is under a major problem due to following main reasons

a) Pollution.

b) Excess capacity developed in short span.

c) Slowing economy

d) World imposing restriction on Chinese Steel.And the opportunities for Indian Steel industry are :

a) India’s steel production is at the levels where China was in 1996 and we are expecting a very strong economy growth going ahead(more or less like China) were steel demand will outpace steel production.

b) Steel prices today are less then what they use to be in 2008. And with shutting down of Steel Plants by China (already around 150 MT) the excess capacity will be trimmed down which will help in strengthen steel prices and hence margin of steel companies.

c) China has understood the cost of cheap steel which has deteriorated their environment and hence now they are focusing on quality steel which will further help in strengthening of Steel Prices.

d) The Indian government is also committed towards Indian Steel Industry and will curb and cheap and low quality steel.

e) We will have more cost advantages then China as we have availability of Iron ore in our country.

Conclusion : With the Indian economy growing in a big way and commitment of China towards capacity reduction and production of quality steel, the opportunity for Indian Steel industry in domestic as well as in International markets is really very large and this has just started.

India’s steel industry is having a great opportunity (as we are the second cheapest after China) and is having very strong chance of repeating success story of China, however we should be cautious that while we repeat the success we do not repeat the mistakes done by China.

Datas collected from website of World Steel Association

15 Likes

Thanks Value2017 . It was so much of details.

Thansk for the insight . Just one Q , aas you mentioned that china consumption had drastically reduced but Production capacity of 808 MT is huge and cant these be exported to other countries and if so why it would be still favourable of indian companies

Or

Out of 808 MT already approx 230(110+120) is cut and rest is getting consumed internally within china?

and is the cost of manufacturing in INDIA is stil cheaper than rest of teh world and how much of capacity can be manufactured by the Indian companies and at what cost . I will also try to find the answer but if you have it handy please share…

Dear Sunil

Chinese consumption has not reduced drastically but definitely due to slow down in its economy it is coming down gradually. Regarding exporting of excess capacity to other countries I have already advised that

a) Due to alarmingly high level of pollution, Chinese government is forcing to cut down their Steel production and as per their data they have cut down production of around 150 MT. So the fall in consumption will be matched to some extent by Shut down.

b) The countries(including India) are imposing restriction on importing Cheap Chinese Steel by way of anti dumping, MIP , Quality Check etc

c) As already advised cost of production depends on many factors, however Indian steel Industry is definitely competitive in all parameters. In the quest of producing cheap steel the chinese have cause an irreparable damage to their environment, which they are now realising. I mean, what is the point in exporting cheap steel at break even profit and after causing lot of damage to your environment. The price at which Chinese were selling steel was not sustainable because of which lots of Indian Steel companies are on the verge of bankruptcy.

The Chinese have now realized that had they debited environment cost in their Cost of Production , they would have never sold Steel at such a loss proposition.

Chinese will have to match their production capacity with their consumption (+10% for exports) and for the remaining production capacity they will have to swallow the bitter pill and shut them down.

We in India are projected to have a situation were demand will outpace production and and we will do very well in domestic and if Chinese intervention is not much, then in exports also.

Board decided against issuance of convertible warrants. The price set for the warrants was 137.25 in Nov 2017. Maybe due to recent price run-up, the promoters have decided against it. Since promoters would have actually gained in case they had converted those warrants (due to the difference between conversion price and current price), I believe this is a friendly move from perspective of minority shareholders?

Reason for issuance of convertible warrants was to improve working capital and pay back debt. So I’m guessing company is not facing any problem in that regard and equity does not have to be diluted.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/9e65e04f-1c17-42ba-95b2-89302df67812.pdf

3 Likes

Yes , Its a great news that the company has prevent equity dilution @ 137.25 which is substantially lower then the current market price.

The only caveat here is that the promoters were the major subscribers of the warrant.

Anyone aware about the online link in which we can track about the final clearance for iron ore mines? It is important to track this development since next leg of margin growth going to come from this only and company were always mentioning in their annual report about earliest start of mining operation in the alloted mines from last 5 years. However now only in their presentation they had start giving timelines like April 2018 for Sirkaguttu mines and April 2019 for Kawardha mine.

Though past has been riddled with some or other controversy for this counter however, with raw material backward integration (coal linkage and mining leases) along with cycling uptick is making this interesting. Top it up with PVC demerger. One way to play on this counter could be to ride through demerger till capacity expansion on PVC segment which has good tailwinds.

I think the story part has been covered well in this thread (though part of that is still management version of the story). Some effort on valuation part:

My calculation is indicating:

-

Top line: ~3000 Cr. for FY’18 (9 months reported numbers + 60% YoY growth projection by management for Q4) .

-

Net Profit: ~426 Cr for FY’18 (9 months reported numbers + 25% EBIDTA projection for Q4 by management - (35 Cr. depreciation, 21 Cr. interest expenses and 0 Tax))

-

Net Profit Margin = 19%

-

Asset Turn = total sales 3000 Cr./Total assets 3556 Crs (as on Q3’18). = 0.85

-

Leverage = 3556 Crs./ networth 2338 Crs (as on Q3) = 1.48

-

ROE = 19* 0.85* 1.48 = 24%

Competitive valuation landscape:

- Considering the cyclic nature of industry, think it will help to look at it more from an EV valuation perspective instead of PE.

- More so since Prakash may possibly have higher depreciation etc. considering the recently commenced 5th kiln. Also, no tax in lieu of MAT provisioning.

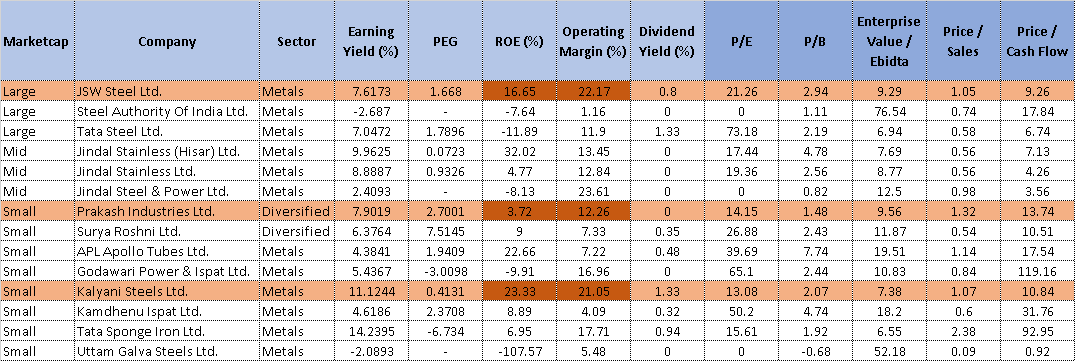

- Out of the given industry players I am inclined to look at Prakash valuation against JSW steel and Kalyani since margins and ROE are mostly in line for each of them. (image is suggesting margins at 12% for Prakash however we know that this is going to be in the range of 19% - 23%, same is the case with ROE) for FY’18.

- What is striking here is that on three distinct valuation parameters namely EV/EBIDTA, Price/Sales, Price/Cash flow Prakash is already valued higher as compared to JSW and Kalyani. Though on PE and PB it may have to catch up a bit with rest two.

So, if other valuations methods are anything to go by, how much of juice is left in Prakash? BAU business is mostly valued at par with best in class peers even if we go by numbers entirely from management projection only.

As market is more forward looking mechanism, I think this will get some edge for:

a: expected capacity addition of 0.2 Mn Tons of sponge Iron by Q3,19.

b: 100% coal linkage is a huge plus and projected to have ~100 Cr. saving per year.

c. Most importantly, for the yet to be demerged PVC business. This business has good tailwinds and peers has historically commanded good valuations. 20% capacity addition is coming on stream in next 2 months and 2x capacity by next 18 months.

PVC Business valuation:

- Basis PBIT of 33 Crs, the EPS comes out to be Rs.18 for FY17.

- PE has been in the range of 30 - 60 for most of the significant players for PVC business.

- Astral of the world quoting at 66 PE and EPC Industires at 82 PE !!! (not denying that we are seeing the untamed bull in action).

- managements indirect reference point is ~1000 Cr MCAP post demerger.

- Feel free to assign a tape price for PVC business for yourself (as and when getting listed) however at current EPS of 18 and with expectation of 2x capacity expansion this looks steal.

Risk factor:

- Guilty as charged, I realize that this story is too much hinging on what management has painted for us. Finding little difficult to cross verify (still work in progress).

- End of the day significant ~88% part of the business is in a cyclic industry.

- Time and again management has been into news for all not-so-good reasons.

Discloser:

- Invested

2 For now slotted in the most riskier part of the portfolio with force capped upper limit of allocation.

Thanks,

Tarun

11 Likes

I had analysed the issue of cancellation of allotment of Convertible warrant and I am of the opinion that this step is extremely positive step and also a step towards good corporate governance. I would appreciate the management on taking such a step and had they not taken this step it would had caused a loss (notional) of around Rs 103 Crs** to existing shareholders = (250-137)x9107500*

*assuming any fresh issuance of warrants will be at least at around Rs 250

**another way of looking at it is that profit of Rs 103 Cr for share holders is loss (notional) to promoters.

Senior forum members view are welcomed @ayushmit

Thanks for the write up! All your calculations will become redundant without taking proper steel prices. I would say that EBIDTA per ton is a very important metric. Brokers are expecting FY19 EBITDA/t of 10000/t for Tata Steel and I would use that benchmark since they are also an integrated player. During bull phase of 2006-08 EBITDA/t peaked at $200/t so I would use Rs 10k/t in an uncycle for an integrated player. Prakash will have 1.2mt in medium term so they could potentially generate 1200cr - 1500cr EBITDA. Now the multiple EV/EBITDA during an upturn could be 6-7.5x but I would assign higher multiple if the debt is very low which is the case here. Let’s take 8x in bull case and 5.5x in bear case. My sixth sense is that steel companies in this cycle won’t stop before 10x EV/EBITDA. They say that expansions could come from internal resources so I would assume they could have 500cr-600cr debt in 18 months.

Base/bear case - 1200x5.5 = 6600cr (EV) -600 (debt) = 6000cr market cap vs. current mcap of 3700 indicating 50-60% upside.

Bull case - 1500x8= 12000 - 600 = 11400 market cap vs. 3700cr currenty indicating 200% upside.

I have not assigned any value to PVC div. currently and its demerger could be used for factor of safety. A very important thing to keep in mind that new steel plants will be starved of new debt going forward given expenrience of the indian banking system. Setting up an integrated steel plant is becoming a very challenging task.

disc - these are just indicative figures not a recco by any means.

4 Likes

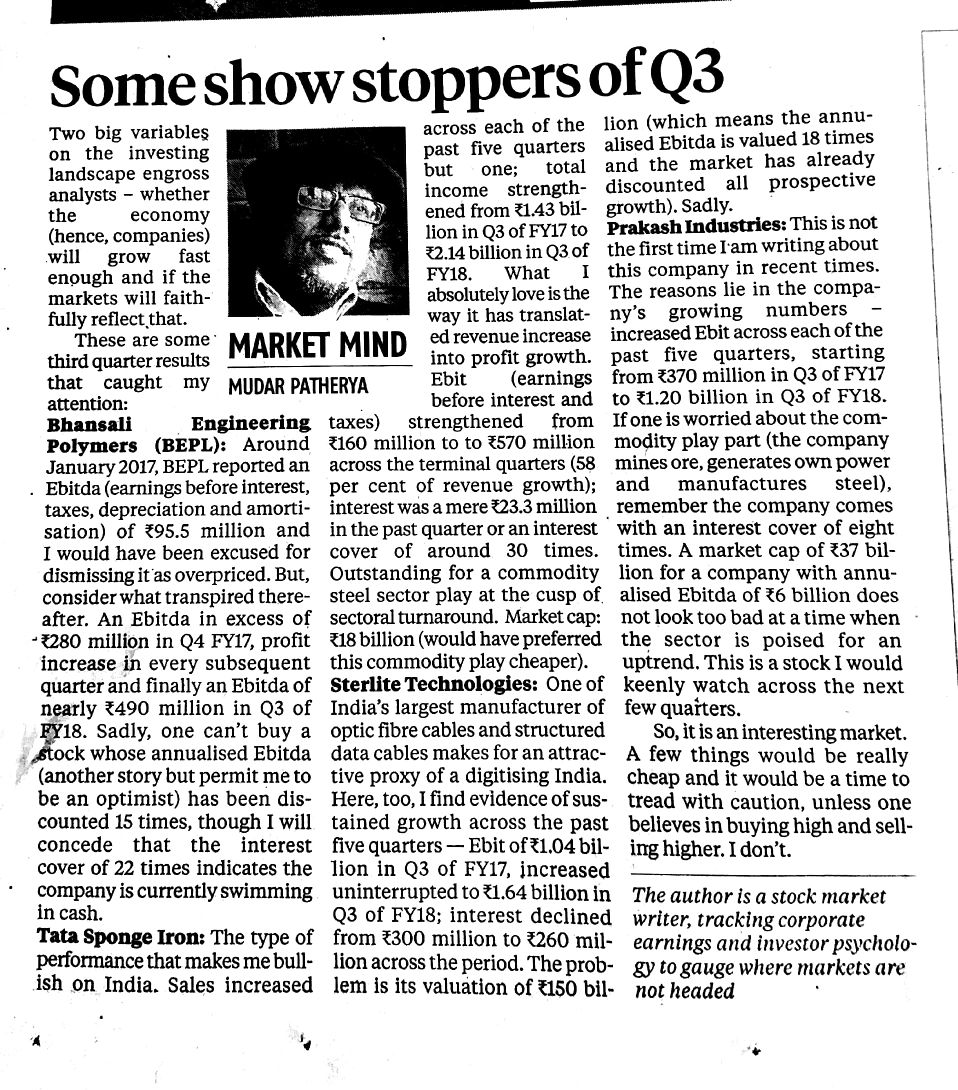

Its good that analysts like Mudur Patherya are keenly watching and tracking Prakash Industires.

One food for thought

While doing valuation for Prakash Industries, the valuation of steel division has been done at a price comfortably above current market price. We are not considering valuation of PVC division and taking it as a factor of safety. But there is a third division also in Prakash Industries which is Power Division having capacity of around 235 MW.

I had gone through the annual report of JSW steel and have found that JSW Steel have listed their power business under separate company i.e JSW Energy. It means JSW Steel is a purely a steel company who is purchasing its power from JSW Energy, whereas in Prakash Industries the power consumed is generated in house by 235MW capacity.

Now I am struggling to find out whether in our valuation of Steel Division whether we have factored the power division completely.

Installing thermal power plant entails cost of around Rs 4.5 Cr per MW so for 235 MW around Rs 1050 Cr.

I hope other members may throw some light on it.

3 Likes

As read in a forum and endorse too

Company is reducing the debt with its CFO(Cash flow from operation) , which is very good thing one company can do… debt will come down every quarter…QIP, would speed up the debt reduction…The stock has multiple triggers unlike other peers…

- Continued growth fronext quarter and 40% in thenext financial year.

- Reduction if debt which will reduce the interest pay out which will improve PAT margin.

3)Expansion going on in phased manner, next capacity expansion in Sept 2018 would start contributing to the revenue. No debt will be taken for any

expansion which is good strategy. internal accruals n QIP money would be used.

4) De merger will unlock values in a great way .

5) Company Iron ore mine will start production from April 2018, this will fur the reduce the input material cost which will in turn improve the margin. another mine start production next year which will again help with the expansion.

6) Company has secured the coal linkage agreement with Coal India for 5 years at fixed rate, which is 20 to 30% less than the market price now.so coal price increases will not affect our company. this will make sure margin will not get impacted.

7) Captive power capacity will make sure no impact of hike in power tariffs.

8) End to end Integrated

plant facilities give it a sustainable , secured , optimized operations which would help big players like Prakash in this steel up cycle. small

players who does not have integrated facilities, they will not be able to do well due to various reasons. So, this should outperform its peers in a

big way in the steel up cycle…next 2 years are full of triggers, which will give the stock strength, apart from very good quarterly results expected…l

1 Like

Promoters release Pledged shares

http://www.bseindia.com/corporates/ann.aspx?scrip=506022&dur=A&expandable=0

1 Like

The companies annual interest cost is around Rs 80 Cr .With the QIP and cash accrual , the company has projected to reduce the debt to Rs 300 Cr and by 31/03/2019 a debt free company. This will have a positive impact0on its earning and will increase the EPS of the company by around Rs 5. With the increase in EPS by Rs 5 and and PE of 10, the company will see further improvement in its valuation going forward.

Why do you suggest a PE of only 10, for a high growth and high visibility stock like Prakash pl.

Value lies in beeholder eyes.

Current capacity of 1 million ton. Assuming the incremental capacity comes by April’18 at 1.2 million ton. Peak of 2008 saw finished steel prices touching to the extent of Rs 40,000 in certain regions. But this was just a blip and these prices were never sustainable for long. Hence we cannot assign any value at these price level. But again it is individual call how you want to justify you holding and fair value. Current finished steel price is around Rs 22,000 per ton. Applying average price of Rs 30,000 per ton. Steel business EV would be Rs 3,240 cr at 90% utilization and 1.2 million ton capacity.

Adding to this the PVC value for 55,000. Finolex current market cap is around Rs 8,100 for 280,000 tons which translates into Rs 290,000 per ton equity value. At 30% discount to this value, the equity value of PVC pipe business of Prakash would be around Rs 1,100 cr.

Power is 100% captive consumption, hence will add no value except savings in cost which is already getting accounted under EV calculation.

Current consolidated debt is around Rs 770 crores (even after payout of Rs 160 cr during 9MFY18).

Overall equity value based on the above translate to Rs 3,580 cr vs. current market cap of Rs 3,585 cr. Add Rs 100 cr to make it Rs 3,700 cr

To me it does not add any further significant value from here on in comparison to risk that is poses like softening of steel prices (valuation done at Rs 30,000 per ton - current price is far lower), weakness in broader markets and inability of firm to reduce its debt considerably. Finolex is far superior relative to Prakash and hence the discount to valuation may be even higher (assumed at 30%)

New capacity addition is 18 months away and who knows how the cycle will play out when the new capacity comes on-stream.

By any stretch of imagination, the current valuation seems to discounting all the positive news and to my sense it is discounting far more positives than negative surprises. Let us keep a close watch and keep our eyes and ears open.

8 Likes

https://dir.indiamart.com/impcat/kamdhenu-tmt-bars.html

I do not agree that current finished steel prices are far lower then Rs 30000/-.

In fact as per above link the basic finished steel product like TMT is at around 35000/- to 38000/-. Basic raw material like Sponge iron is traing at Rs 20000/-

One may may make inquiry in their near by steel shop to get the actual rate. I made a personal inquiry and found that all rates for TMT are fairly above Rs 36000/-. Other forum members can also post their local rates.

Please correct me if I there is something missing in my understanding.

@yudiagg : I had conservatively estimated my valuations at PE of 10 even for a growing company to have sufficient margin of safety.

My belief is that my valuations should first give me comfort at current valuations and then at projected valuation, so that I do not get panicked even when there is down fall of 40 to 50%, and on the contrary it should boost my confidence to allocate more money during the fall.

1 Like

I believe u r talking about the retail prices. To give another perspective, the Tata Corus deal was done at USD 700 a ton and people were justifying even USD 1100 a ton for an integrated capacity. But strategic acquisition can take the valuation to a considerable distorted level. So I am not using it as a reference point.

Even if you add 50% premium to Rs 30,000 a ton value or Rs 45,000, still the risk-reward does not favor in this case as per my understanding. Unless we see some significant correction it offers more risk than reward.

With winter behind some capacity of China will come back into the market. Also some capacity will come on-stream by meeting with new environmental laws of Chinese Government. Besides, China has been the largest consumer of metals in 2017 and with Chinese economy slowing down as per recent IMF forecast for 2018 and 2019, we may see some intermediate correction in prices which subsequently will set off by supply deficit at a later stage on global scale.

1 Like