While PPAP has corrected a lot recently, it’s promoters have purchased a lot of shares in multiple transactions.

Can somebody confirm how much shares the promoters purchased?

Shares worth 3.84 lacs purchased by promoters again.

% of change in Remuneration for Director is 65% … is this something to worry about is it related to hike ? because in same company no one get hike of 65%

Is it % increase or total remunration in lakhs? Please verify sometime heading is not correct:grinning:

total remunration is 236 lakh so it is percentage only i guess

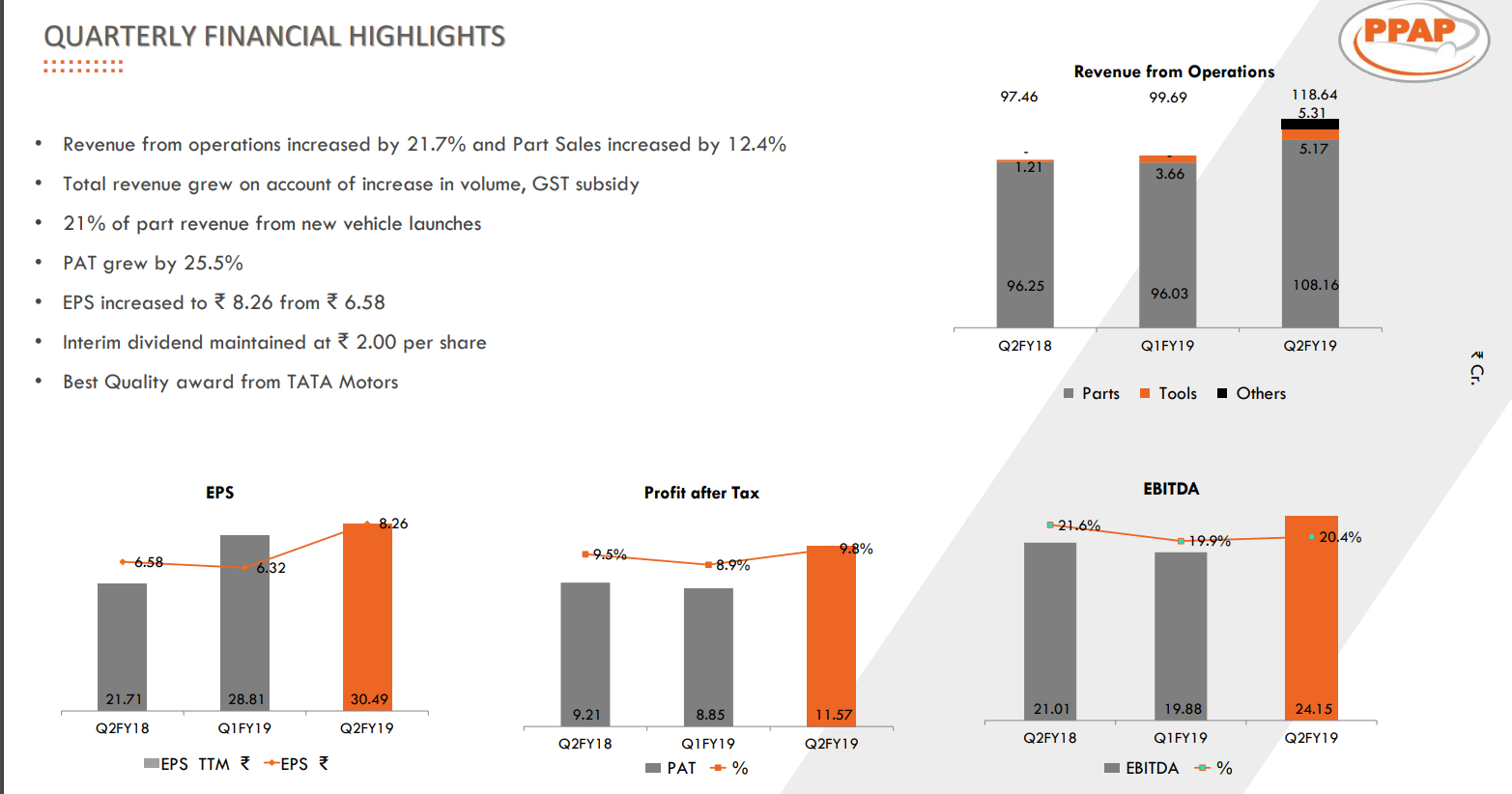

:PPAP AUTO delivers good set of quarterly results.

Net Sales at Rs 118.64 crore in September 2018 up 21.73% from Rs. 97.46 crore in September 2017.

Quarterly Net Profit at Rs. 11.57 crore in September 2018 up 25.57% from Rs. 9.21 crore in September 2017.

EBITDA stands at Rs. 24.39 crore in September 2018 up 12.19% from Rs. 21.74 crore in September 2017.

PPAP Automotive EPS has increased to Rs. 8.26 in September 2018 from Rs. 6.58 in September 2017.

Financial Performance : Q2FY19

Revenues up 21.7% to Rs. 118.6 crore;

PAT at Rs. 11.6 crore up by 25.5%

PPAP Investor Presentation_Q2FY19

Following are some of my thoughts on business post Q2 results. I have not jotted down details with fine tooth comb from conf call or presentation, this is just how I see things.

Disclosure

I have sold shares of the company in last 90 days and brought down allocation to ~2.5% from earlier 5%. This is not a buy or sell recommendation. Investors are advised to do their own due diligence.

Turbulent Times in Auto Industry

The automotive industry is going through turbulent times due to - increase in prices of petrol/diesel, rupee depreciation & commodity price hikes leading to escalation in RM costs. Things are further exacerbated by change in insurance regulation - where third party liability insurance of three years is required to be brought upfront resulting in higher purchase costs. The industry might find it difficult to grow in double digits if one were to go through commentary of Maruti Suzuki or track the volume numbers from SIAM.

In this context of lower growth visibility, I decided to take some money off the table. When I bought PPAP 3 years ago, this was a story of improving OPM from 9-10% to current 20% with lower finance & RM costs resulting in good growth in EPS. Currently I feel company might be at peak margins (although not at peak valuations). On longer term basis, I remain optimistic on passenger vehicle market in India & on the future prospects of the company. Ability to maintain OPM at 18%+ rate and any capex announcement remain two important moniterables for my view.

Q2FY19 & HY19 Results

The investor PPT captures the results & different components of in fairly great detail. Following are some observations →

- The topline growth looks higher for Q1FY19 due to GST refunds of ~5Cr from Rajasthan government in Q2FY19. This was refund from beginning of GST till current quarter. Going forward company expects to get ~1Cr refund every quarter.

- Part sales grew at an growth rate of 12.4% - which is much higher than end industry growth rate. This is primarily helped by strong sales of Maruti Suzuki Swift, Honda Amaze & Toyoa Yaris. Honda Amaze sold 50000 cars in shortest time in the history of Honda cars and PPAP has higher per car contribution for Honda cars as it supplies both sealing and injection molded products.

- If one adjusts for GST refunds & factor in the fact that these are peak margins, the results looks pretty average/expected with growth of 10-20%.

- The material costs have gone up from ~48% few quarters ago to anywhere between 50-53% in last 2/3 quarters. The forex costs get automatically passed on to customers but other costs get passed with a lag of one quarter or sometimes do not even get passed on. The RM cost passing depends on model/part/customer etc.

Why I remain Bullish on company on longer term basis -

- The company is absolute leader in automotive sealing systems part in India with company supplying parts to 70% of PV sold in India.

- The employee cost of the company is ~15% for last 2/3 years. My inference from this is that - the company is really adding value to their customers and probably also has invested in manpower to come up with new products.

- Hyundai remains a biggest optionality for the company. Currently company supplies parts on for Hyundai Eon and they will start supplying parts for another model starting from Q3FY19. Hyundai is second largest PV maker in India and getting Hyundai should result in very good growth.

- On injection molding side, the company supplies parts to Honda and is trying to sell these parts to other customers. The competition is higher on this side but so is potential. In my mind, if a company can pass the quality criteria of Honda, it can pretty much pass the quality criteria of any PV maker in India.

- If Indian PV market is t grow at 8-12%, Maruti Suzuki will probably lead the way. Growth in Maruti volumes along with potential to get more wallet share is provided by PPAP. e.g. For newer Swift model, company will supply more parts compared to older Swift model.

- The company is developing good relationship with TATA as evident from recent conf call and is also engaged with several newer Chinese new car makers.

- The Rubber JV of the company provides the primary sealing systems and the numbers will probably improve going forward.

Risks

- I still do not see PPAP as a strong business with some competitive advantage. It still remains an average business and hence it must be bought as an undervalued story in my opinion. The end market size of automotive sealing systems is small (e.g. PPAP sells only 1200Rs. worth of secondary sealing parts for Swift) and hence not a lot of competition might come in this part of the business. This is not true for injection molding side of the business though.

Competition - Automotive Sealing Systems => Cooper Standard, Anand Nishikawa

Competition - Injection Molding Systems => Motherson Sumi, Krishna Maruti, Machino Plastics - The company has no pricing power & ability to pass on 100% cost pressures is limited

- Very high growth rates will materialize only from market share gain which is not an easy task. The end industry will grow at most 10-15%.

10 Likes

Press release

Q4FY19 results moderate considering the downtrend in PV sales.

The Company derived 98% of sales from the Passenger Vehicle segment of the Indian Automotive Industry.

1 Like

PPAP has got 1 year of order pipeline with MG Hector model.

Good that they are adding new customers.

being a near debt free, high margins business with future assured products even in EV era, its a good buy at current 230 cr mcap.

Getting business from Hyundai’s new models is key. Mgmt said they are trying for Hyundai business.

2 Likes

PPAP provides sealing products for 100% of Honda models. In Injection Molding,

its market share is still very small as Honda is the only major customer. With Honda turning soft on Indian market, does this make things difficult for PPAP?

3 Likes

By foreseeing the view of Electrical Vehicles, PPAP Established Subsidary PPAP Automotive Technology limited for electrical vehical components.

Q3FY20 Investors presentation ,contribution of MSIL reduced in overalll sale and adding new cusomers.

Help in inviting views from the folks tracking this company closely - I see the company as fairly undervalued now, and anticipating a turnaround in the PV sales in the near to medium future, consider auto ancillaries would be a good play. I see the company has got low ROCE during the periods (probably owing to low PV sales, issues with its main customer Maruti strike in the Manesar in 2012, hike in raw material prices, etc. and general correlation with the PV sales) post which it has grown profits at a decent pace.

Promoter buying through an open market. Shareholding increased from 64.5% to 64.77%.

Debts and working capital both are under control.

did anyone know the reason behind the resign of Mr. Anurag Saxena, CFO of PPAP, is that a personal reason or anything?

why the company is not conducting con calls for 2 quarters?

While am also worried with the recent fall, I’d wait till this quarter’s results rather than second guessing. Holding tight onto a rather significant position I hold. The company has been there for decades and withstood the test of time.