I joined ValuePickr about two years back and I can’t thank you all enough for creating this wonderful community for investors to brainstorm and share their views in the most constructive manner and the senior members to enlighten with their wisdom.

Before sharing my portfolio and the brief write-up about the stocks I hold, let me give a brief profile of me.

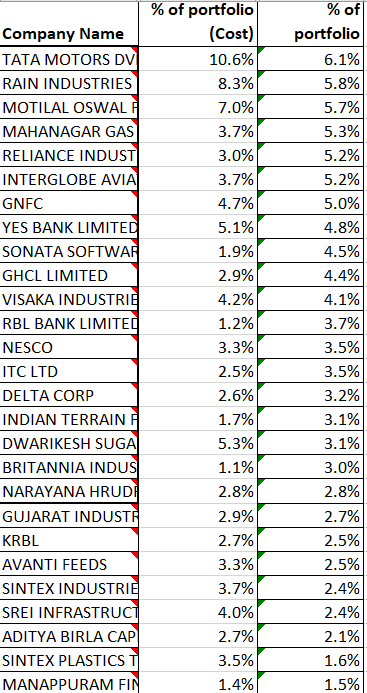

I am 27 year old and was always interested in stocks as a kid. I started investing when I started working in 2013, with zero capital, by investing my savings gradually into stocks. I had accumulated over 100 stock and after reading value investors and other books, I realized i needed to reduce the no. of stocks in my portfolio. In Sept-Dec 2017, worked on my portfolio and consolidated my holdings. I have made a CAGR return of ~10% till date, which is below par and hope to achieve a ~15% return from this portfolio. I believe in the portfolio size of 20-25 stocks. I am from a finance background and work in the capital markets. I request fellow members to share their views on my portfolio.

Some of the stocks on my watchlist are Minda Industries, Godrej Properties, Arvind SmartSpaces, Max Financial Services and NOCIL

1 Like

Hi @jajushobhit

It would be nice if you could post your investment thesis as well. Regarding the real estate stocks in your watchlist - this business is going through some tough times and after RERA - developers have a major cash crunch issue. Some premium developers have been forced to exit the space completely and some have gone bankrupt. Its exceedingly difficult to be a developer and earn a decent return on capital - so I would suggest you relook at them. Rest except Mahanagar I don’t track so no view on the same. Mahanagar Gas is a good co and valuations are also moderate. I would suggest that you have a greater allocation.

Broadly, i think your portfolio consists of some stocks which you may have purchased because their cheapness so thesis has to be doubly sound.

Best

Bheeshma

4 Likes

I do not know about all of the stocks in depth but since you asked on portfolio level I will try and answer.

Weights of 3% and below have almost nil effect on your portfolio returns.

Unless you have plans of increasing weights I would suggest cutting out all the positions under 3% and buying into the positions at 3% or your higher conviction ideas.

I would suggest trimming this out. I know experts suggest and take tracking positions but let us come to reality and know our limitations. We are not experts. You can take a tracking position even with 0.1% of the portfolio.

Coming to the stocks I would stay away from the cyclicals.

Do not buy expensive or pay a premium unless you are getting something in return. I will refrain from taking the high quality names but I would never pay a premium valuation for a company unless they are of that class. So that is something to consider.

Sintex I think you need to check the promoter and books.

Stay away from the cyclicals, trim the portfolio and pay a premium only when justified.

1 Like

You and I have similar thinking patterns. It consists of Good stocks. In addition do have a look at ICICI Lombard and VST industries.

1 Like

I think you would do well with a bit more concentrated portfolio. I can sense that given the amount of research you have done, separating high conviction ideas from low conviction ideas should be your next step. The portfolio allocation thread offers a very good metric to help decipher the same.

2 Likes

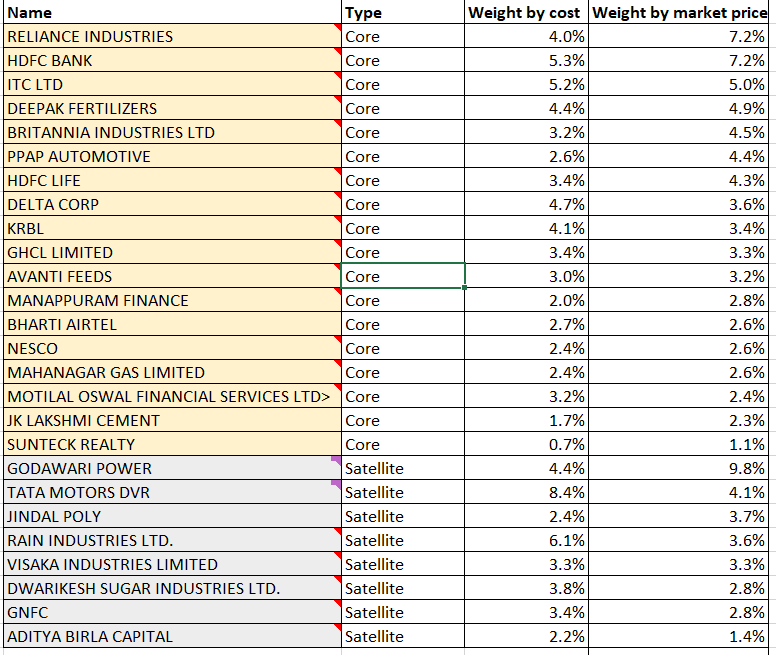

I spent the last two years on improving the quality of stocks I hold. The approach towards a core and satellite portfolio helped me in understanding the reason why I am invested in a stock. Special thanks to @bheeshma for making me revisit my thesis on " cheap stocks" which made it easier for me to eliminate some of them. I will appreciate your views on the portfolio. Thanks in advance

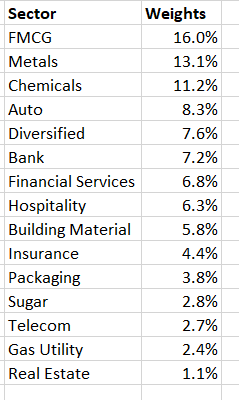

Core Portfolio is ~70% by market price, would like to take it to ~80%. Obvious sectors missing in the portfolio are Pharma and IT. Sector wise break up is as follows:

Hi @jajushobhit

Clearly, your core portfolio consists of solid names with an established market position so the way forward is to have a view on their intrinsic valuation. The most easiest way to have a handle on valuation is to write the 200dema against the cos name. Ofc, it’s not scientific but since your core consists of names that a dominate the industry they are in and are well followed by analysts, it provides a good idea about the valuation status. I don’t know much about your satellite cos. Have recently started reading up on godawari power and have been invested in Cosmo which is in the same industry as Jindal poly. Packaging film cos are having a good run due to good gross spreads.

2 Likes