India needs lot of houses in years to come…everyone needs one rather many…that’s how people are attached to physical assets…talk about equities to my dad…or any elderly…they give me some random faces and asks me to buy plot or flat… and last…recessions doesn’t come calling…and as many say… and as india is consumption economy…any recessions will be short lived IMHO…forecasters will forecast on very much everything…to macros crude interest rates…what trump will do tomm…but we need to stick to good business in thick and thin…as long as they perform…

1 Like

Current scenerio and dunamics are not favourable for housing and all ancillaries, i have some properties where rates arw stagnant for last 2 years, its a very vulnarabke area and lot of skills required to access exact business model, DHFL was darling of markets was not looking fairly valued even at 670 level , MOSL came with 750 targets and other brokerage 850, even 1000, look at it rightnow. Crashed 400 rupee in one day. Buying a house and making profit from housing stock are too different. All Banks, NBFC have housing arms, growth in sale of flats is negative, real per capita income is too low to create a huge demand for 25-35 lakh houses. Job growth is negative. There is zero safety of margin in pure housing company even at current levels. Cycle is not complete yet, you will see huge defaults from builders in coming months, that will create a recession in basic economy, government is sensing same, wait and watch.

2 Likes

There’s no valuation model as such.

My approach is to invest in those businesses which are easier to understand (pharma companies are an exception).Usually I just look at the company’s performance, size of opportunity, competitor landscape ,regulatory issues etc.If a company performance happens to be consistent , opportunity seems to be never ending and competitors are either absent or are unable to catch-up , tend to put that stock in my portfolio (examples :Godrej ,Oberoi in RE , Saregama in music space ,Tata Elxsi,Sonata in IT ,CRISIL )

Many a times there’s competition, regulatory issues in certain sectors, there I tend to go with market leaders with a strong management history , But most of these stocks happen to be overly priced , hence try to buy those during the periods of fear when people tend to act irrational (Gruh, ICICI Sec,Maruti,Harita HDFC AMC are the examples)

There’re few stocks where either capacity expansion or lot of tailwinds (example Deepak Nitrite , although I believe that it may go down a bit from here as PE is very high )

3 Likes

Agree. Keeping an hawk eye is important. My approach is to take partial profits in cyclical stocks time to time.

While everyone has right to have their own views , but as per my view we need to be careful about writing off a sector . Whenever we talk about a sector , let’s separate euphoria from long term story.In real estate, euphoria is over in last 6/7 years. Gone are the days where every Tom,Dick & Harry would book several houses to sell for instant profits and some other Tom,Dick or Harry would everyday announce new projects. Due to structural change in the sector (RERA ,GST, credit squeeze,few builders going bust ,demonetization) , some of the players are doing badly and so called investor class has burnt their fingers . But it does not mean that demand from end-users is going to die.

Every Indian dreams to have a home , there are so many marriages happening every year, families getting nuclear, urbanization etc are the factors that housing would keep doing well ( yes euphoria may not be there) .Apart from that most of Indians have few options to invest their surplus money , many dont understand equities, gold as an asset class has its own limitation ,so real estate happens to be the only place where a rich businessman, a rich farmer , a corrupt government employee tend to park their money for long term.

Yes we need to be selective about the scripts we select in this sector. Have given my logic of selecting Godrej and Oberoi in one of the messages .

Very good question. Yes I do average up . One fundamental factor is if we understand a company well and have high conviction , there should not be any apprehension in averaging up (provided one has liquidity or one wants to shift from low conviction stock to high conviction script)

Here are few scenarios l :

a) Company keeps giving excellent & consistent results , it walks the talk but market does not realize it and keeps undervaluing it (in today’s market, I find Oberoi and Saregama in that bucket although I’m skeptical with overall market direction ,hence would wait for broader market correction to add more )

b) In a bull market, when everyone becomes irrational and there’s a tendency for price to grow faster, I tend to average up if the PE levels are lower than the greed -levels of market -participants.

c) If there’s a structural change in the sector or a certain sector starts becoming the leader of the bull market ( averaged up lot of NBFC stocks in 2017 bull market but exited later on as sector got overheated )

d) In case of capacity expansion and available market opportunity (chemicals sector )

e) Favorable regulatory changes or certain sectoral tailwinds

My approach is to invest in those businesses which are easier to understand (pharma companies are an exception).Usually I just look at the company’s performance, size of opportunity, competitor landscape ,regulatory issues etc.If a company performance happens to be consistent , opportunity seems to be never ending and competitors are either absent or are unable to catch-up , tend to put that stock in my portfolio (examples :Godrej ,Oberoi in RE , Saregama in music space ,Tata Elxsi,Sonata in IT ,CRISIL )

Many a times there’s competition, regulatory issues in certain sectors, there I tend to go with market leaders with a strong management history , But most of these stocks happen to be overly priced , hence try to buy those during the periods of fear when people tend to act irrational (Gruh, ICICI Sec,Maruti,Harita HDFC AMC are the examples)

There’re few stocks where either capacity expansion or lot of tailwinds (example Deepak Nitrite , although I believe that it may go down a bit from here as PE is very high )

[/quote]

Dear Radhe shyam agarwal…

I was also with the same mindset of you earlier. I was aggressively investing based on different themes, methods, formulas, calculations and estimations. But I did it for learning not for earning.

The primary important thing in stock market is safety. You have allotted major portion of your portfolio to realty and pharma. May be your estimation of growth may come true. We must and should concentrate on the word “if not”. If in case your estimations go wrong, you will again quit market after 5-10 years (Because there is no other option). Instead, spread your portfolio among quality companies. There is no restriction to limit our portfolio to 8-10 or 20 companies. This is for multibagger returns. But not for safety. Our goal is to “EARN HIGH INTEREST WITH LOWEST POSSIBLE RISK”. But not multibagger returns with highest risk. (You already know what is the risk…every thing we have may get wiped out if any thing goes wrong).

Even if we are correct in the estimation of company growth, frauds in corporate governance may completely damage the share. we have many examples in the recent years.

A small advice from me. It is better to spread your risk among quality companies including emerging good companies.

Thanks for the sincere comments . I’ve been investing in the market for last 30 years (am 60 + as informed above in one of the message) . Out of my total disposable income ,I only have 40% exposure in equity ( had exited in 2017 December, started investing again in August 2018 and above portfolio is just 20% what I’ve kept aside for the equities) , so it is clear that I don’t put all my eggs in one basket.

And from equity , I want make out the maximum returns as compared to other asset classes. I’ve learnt over the years that you don’t earn much if you don’t concentrate , Diversification is other name of lack-of-conviction or lack-of-knowledge. That’s why I normally don’t have more than 15 stocks in my portfolio (again that number is high , I would rather like to have 5 or 6 ) .

Things can go wrong? Yes they can. I feel if out 10 stocks, if 6 perform well ,the risk is covered.

2 Likes

Please do read this good article. It is in today’s Mint. This underlines my philosophy of being choosy in the sector and investing in Godrej property. It has an asset light model, a good brand name , good management history and few more things ( full explanation is in one of the above messages)

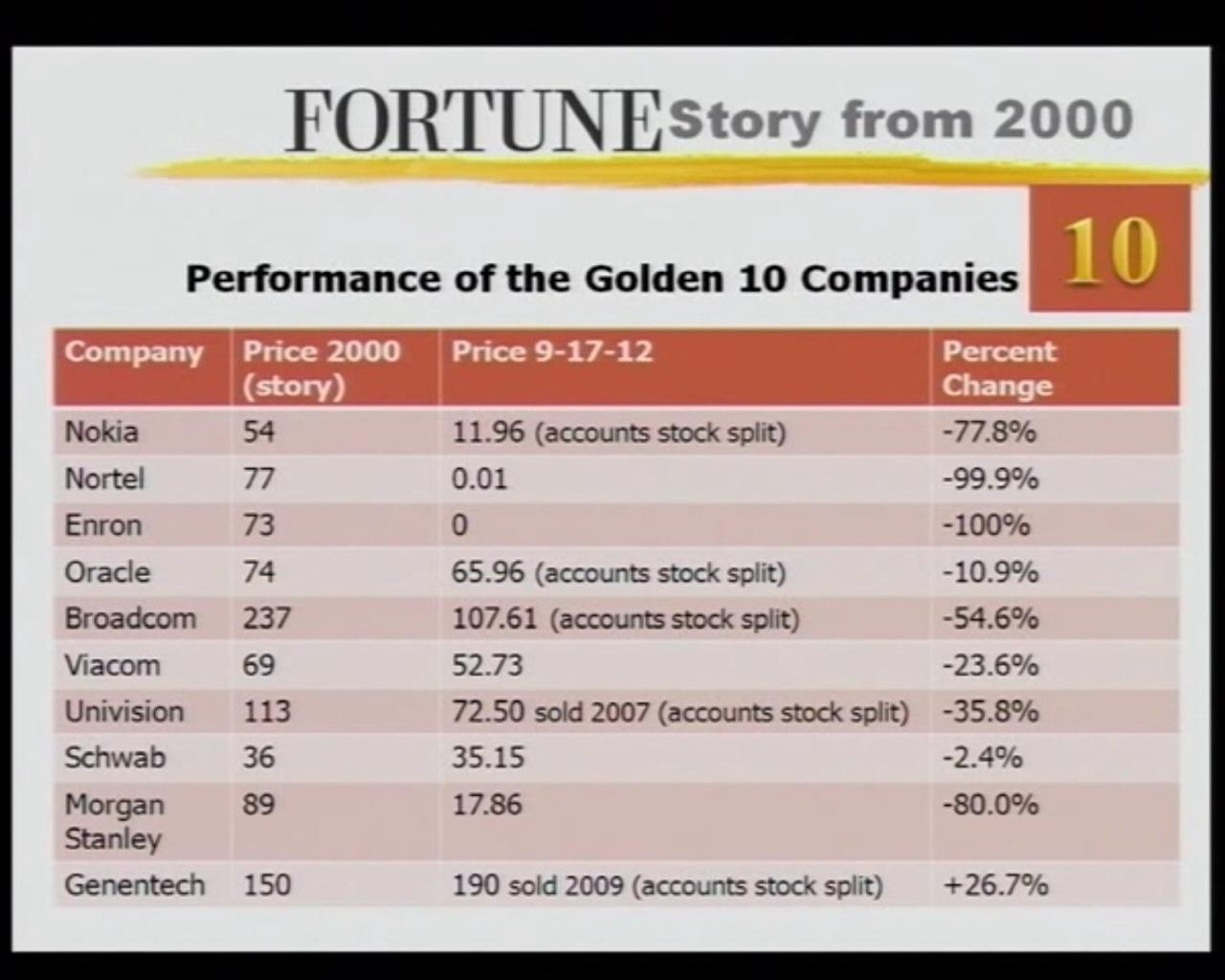

Here is something which supports yours and mine view …keeping a hawk eye. Buy-it-forget-it only works in the hindsight ![]()

![]()

In 2000, Fortune magazine came up with a ‘Buy-and-Forget’ portfolio - stocks that would last the decade. This is what the returns were like in 2012 after accounting for splits.

I feel that the price paid by you while creating the portfolio are excellent. Since you have bought the stocks during the panic in October, the margin of safety is good. With your experience and conviction, I am sure your portfolio should do fine. Good stocks picked during panic times helps in keeping the portfolio green in short, medium and long term.

1 Like

If one will analyse the past performances of sectors , Pharma , Financials , Consumer businesses have created huge wealth as well as protected capital and will do so for next many years.

Eg: Dabur , ITC , HDFC , Kotak , Abbott , Nestle , Britannia , Lupin , Sun , Bajaj Finance , Asian Paints , Pidilite , Havells , Page etc . Very few have gone wrong in this sector.

Lots of Tech companies have come and gone and have destroyed huge wealth except very few who have successfully adopted themselves…

Most of the scams have happened in this sector.

Lots of RE and Construction companies are closed and destroyed huge capital.

Eg. Unitech , DLF , JP , lanco , GMR which were favorites of market at their times. Only L&T has remained alive…

In the events of Crisis , everyone becomes Irrational and start painting everyone with same Brush… Approach towards individual Companies should be discreet. One should find great companies and should look at the opportunity size.

In good times , not every company is good and in bad times , not every company is bad.

Companies which have experienced 2008 financial crisis and 2013 liquidity crisis , Companies with sound Fundamentals will navigate through tough times and will grow and create good assets and wealth.

For India to grow at 7% of GDP , NBFCs , Financials are the backbone. They remains the most important and crucial credit source. Increase in consumption and continuous demand should be a factor too

For a Capital Goods company whose products lasts for long , they will find it hard to increase the volumes after a point.

For consumer businesses where the end products are needed regularly , they find it very easy to grow.

Size of opportunity is a very important factor.

Small Fish in a Big Pond will create huge wealth

Big Fish in a Big Pond will create wealth as well as protect Wealth

Small Fish in Small Pond will create a limited wealth

Big Fish in Small Pond will find extremely tough to grow and will destroy the capital over the time.

4 Likes

I will agree thT wealth creation will require sizable investment in your top 4-5 high conviction bets. My 60% of portfolio is concentrated in top 5 bets, than comes 5 stocks with 25-30 % allocation and 10-15 % is reserved for new entrants, i foind that managing more than 20 stocks is very hugh effort, had maximum 17 at a time and started trimming due to heavy monitoring requirement. Rightnow hold 11 stocks. Mostly prefer midcaps as mulribagger returns comes from unknown companies, thats how i have earned in last 4 years.

Below are my high conviction bets

- Force Motors

- LT Foods

- Apex Frozen Foods

- Kiri induatries

5 Trident

6 Yes Bank

7 Phillips Carben

8 Ceat

Of the list of these eight companies could you spare a few lines to explain the rationale behind Force motors being your top bet.

So more of a fundamental analysis person, you are and at the same time had sold off everything looking at the valuations, hence you are aware of valuations too. Nice analysis, thank you very much Radhey Shyam ji.

And what do you think of Ashiana, of the management and their business model?

Huge Debt + Very Capital Intensive Business. Requires high level of inventory. KRBL might be a better bet as it is a Market leader with much sound fundamentals. Disc: I don’t like the sector.

Seasonality issues as well as risks of Diseases. Opportunity size is big and better to bet with Market Leader with strongest balance sheet. I will go here with Avanti. Disc: I bought Avanti recently.

Commodity Business. Very limited size of opportunity due to very low entry barrier and presence of other leaders. Continuous equity dilution.

Poor Return Ratios , Highly capital Intensive Business , Negative Free Cash Generator

Lot of other good private Banks are available. Buy Quality , not cheap.

Another commodity business. Poor Return Ratios . Requires timely entry and exit. Can not come into long term list of stocks.

Disc: I hold none of the above stocks.

2 Likes

Force motors operates in 5 verticals

- Tempo Traveller, tractors, trax, Gurkha, recently launced 33/42 seater minichassis bus

- Working on electric traveller launch by 2020

- Sole partner for BMW and Mercedec in India

- Sole partner for rolls royce AG for india, nepal and bangladesh

5 started defence production recently

Main USP for force motors is engine and power train manufatoring for mercedes and BMW. Current selling is 30000 annual, expected selling is 200000 in 5-7 years as UHNI population will triple to 1.2 million in 2025. Even this can be held for 10 years horizon. Force is only company where both BMW and mercedes have tie up in a country. Zero equity dilution in last 5 years. Zero debt. Low equity. This will be a mega multibagger.

1 Like

Excellent take on the stocks. I was about to respond on similar lines. As far as CEAT is concerned, do analyse GOODYEAR , one would find it a better investment candidate.

1 Like

I will prefer Balkrishna Industries and MRF. Moreover i am investing in Tyre Rubber Companies like OCCL and NOCIL. They look very good for a 3 Year period as huge expansions is coming in Tyre Sector. The Q2 Concalls and Presentation of both these companies are very exciting.

Disc: I hold Nocil , OCCL and Balkrishna !

3 Likes