I have received multiple questions on my current portfolio in my earlier thread : BULL in BEAR Market - #20 by kb_snn

This thread is in response to that . For regulatory reasons kindly read the following

I AM NOT SEBI AUTHORISED FINANCIAL ADVISOR NOR I INTEND TO BE ONE .

NO ONE IS EXPERT IN MARKET AND MARKET TEACHES US NEW LESSON EVERY YEAR

PL DON"T IMITATE THIS PORTFOLIO IN PART OR FULL . THIS CAN BE DANGEROUS IF READER DOES NOT UNDERSTAND WHY I BOUGHT IT AND WHEN I WILL SELL IT IN PART OR FULL… PLUS MY RISK PROFILE MAY NOT BE SAME AS YOURS .

ANY PORTFOLIO OR STOCK DISCUSSION SHOULD BE USED AS CASE OF LEARNING AND NOT AS RECOMMENDATION

Watch This Video before I get into details on how I construct my portfolio

I *************************************************************************************** I

STEP 1 : ASSET ALLOCATION FOR YEAR 2018

Primary Objective : Long term survival and compounding

Like every year this year too I have put across a guideline for my portfolio equity / debt asset allocation . My equity portfolio is primarily large cap so I am using NIFTY as benchmark of market mood / behaviour

| Equity % | 30% | 50% | 60% | 65% | 70% | 75% | 80% | 85% | 90% |

|---|---|---|---|---|---|---|---|---|---|

| NIFTY LEVEL | 15030 | 14529 | 13527 | 12525 | 11022 | 10020 | 8993 | 8094 | 6745 |

What above table means if NIFTY is @ 15000 my equity % in overall portfolio will fall to 30% and if nifty is @ 6800 equity allocation will increase to 90% .

Currently since NIFTY is around 11000 -10000 , my equity allocation is 73% …

Now comes the question why this range … This range is based on past NIFTY behaviour over 25 years.

Can NIFTY go beyond this range in this year – Sure it can but the probabilities are low .

What will I do if NIFTY goes beyond this range ,

Say < 6800 – Under No circumstance pure fixed income will fall below 10% of my portfolio . This MOS in for any black swan period like 1929 - 1948 when market equity market remained undervalued for nearly 20 years … Since such period are often deflationary - I assume fixed income can cover my annual expenses even if companies discontinued dividends …

Similarly if Nifty > 16000 in 2018 - I will retain my equity position at 30% and not reduce it …

I *************************************************************************************************** I

STEP 2 : Portfolio Construct :

Primary AIM : Portfolio Gr > Inflation + 8% -10%

1***************************************************************************************************1

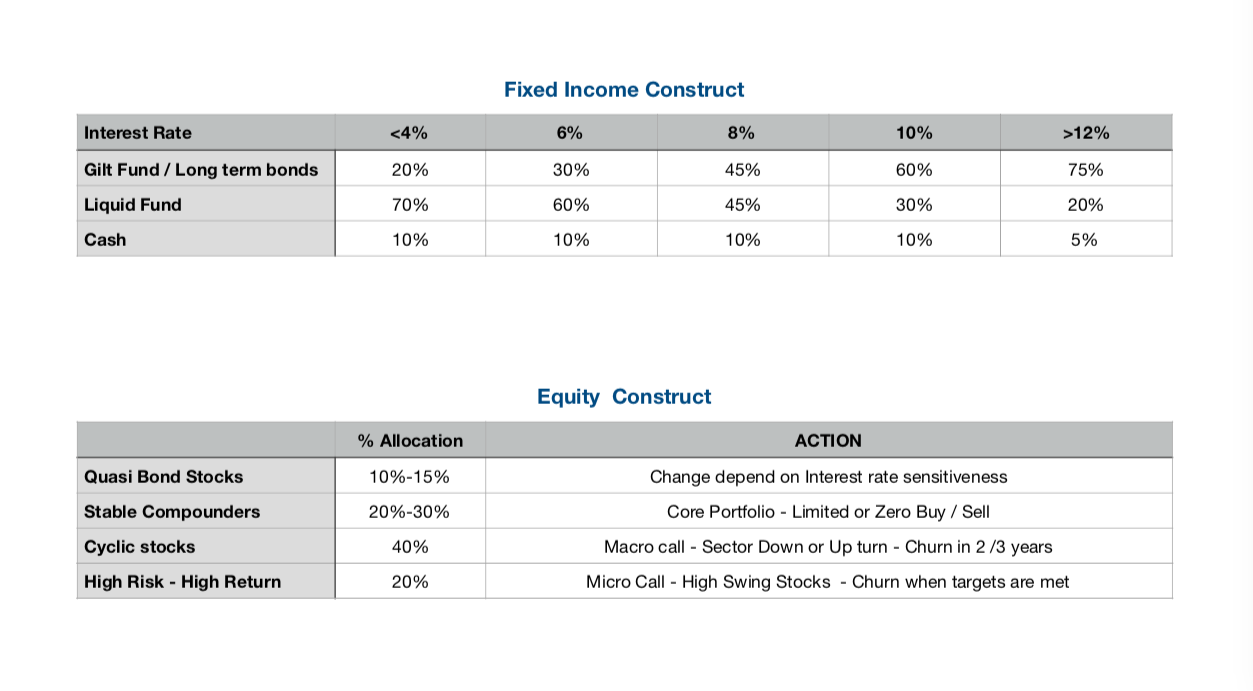

Current Fixed Income Components

LONG TERM BONDs

- Gilt Fund ( currently it is Kotak Gilt Fund )

- Perpetual Bond ( Tata Power )

- Tax saving bonds ( Multiple companies and with differing maturity profiles )

Since last year I have reduced Gilt fund % and moved into liquid funds . This year most of money is moving into Quasi bonds … More on that later , My Plan is in coming year I want to reduce Gilt funds to zero and shift to attractive Corporate Long term Bonds when available …

LIQUID FUNDS

HDFC Liquid Fund ( Feeder to Long term bonds depending upon interest rate )

ICICI Liquid Fund & Kotak Liquid Fund ( As alternative to cash for re-investment in Equity )

1**********************************************************************************************************************1