That was a sharp upmove.

Any news ./ was it operators ?

The company has released a investor presentation to the BSE. Not sure how valuable it is though. We seem to know most of that already:

And no mention on winding down the apparel business.

Benefits of operating and financial leverage in full flow. It seems apparel biz is to keep his daughter busy. Will be interesting how it funds the next leg of quartz growth. If it waits for cash flows, risks stagnation at some point of time or high leverage again if it doesn’t.

I think it is written in the presentation that they are working on increasing the slab size which should actually increase the productivity. I think a year of consolidation with cash flows like this will be enough to fund future growth, plus it is a growing sector so maximum risk can be stagnation (but not evident from the numbers) and even then they will be able to pay off the debt. As mentioned above the only concern I have is of corporate governance rest we are sitting on a gold mine literally!

Also they mentioned in bold letters that they are still the only producer of quartz using Bretton Stone Tech in India

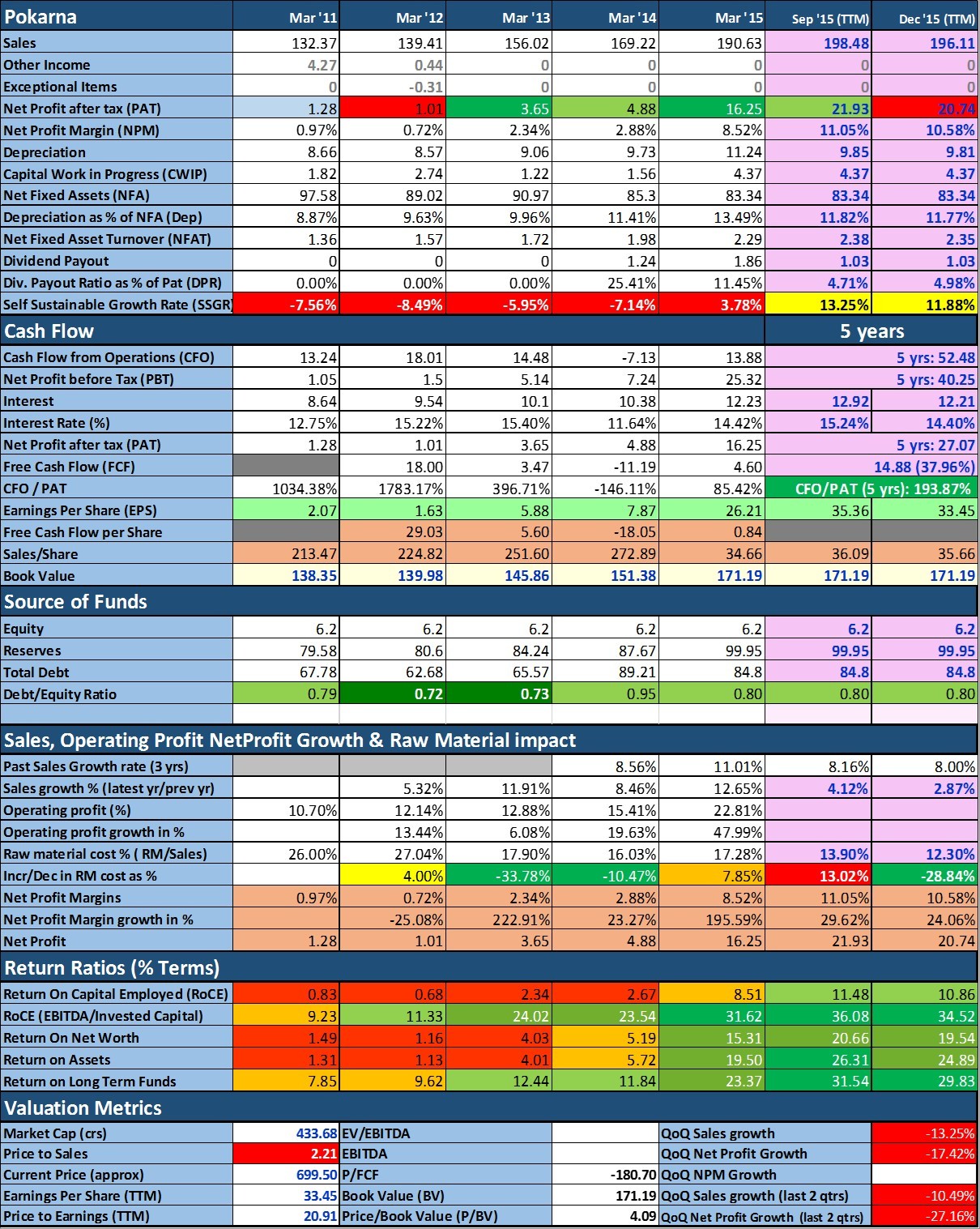

Can someone please explain to me why the pe ratio shown is 21 in moneycontrol and 8 in screener? I understand that screener uses TTM net profit to calculate the ratio. Even if you use the FY15 net profit, shouldn’t the pe ratio be around 14. So why does in moneycontrol it shows as 21?

Thanks!

No answer from my side buddy. But it is something that MC can answer. Do not get into all this… calculate your own PE or have ways to verify which is correct one. That said on PE terms company is cheap… move on

1 Like

The difference must be consolidated v/s standalone.

2 Likes

In Money control the PE is incorrect.Its not calculated in consolidated basis. The PE is nearly 8 and TTM EPS is nearly 93. you can find out the EPS for the last 4 quarters , add it and then divide the current price by it. You will get the correct PE.Look at the Growth the company has given in the recent quarters. its stellar, Management guidance for Fy16 of 400 cr against of 232cr in the FY15 with increased OPM tells the Story. The valuations are quiet cheap because this is not a pure commodity business. Engineered Stone in the growth engine for this company which has got Koesher certification which is a much need for selling Quartz slabs in US markets,

2 Likes

Moneycontrol displays both “standalone” and “consolidated” figures. But by default they show standalone figures. Click on the “consolidated” TAB for consolidated data.

1 Like

If one is seriously studying a company for investment then it makes a lot of sense to go by the authentic data presented by the company in the annual reports and results put up on bse or nse.

Even if one uses screener or MC as a starting point then also it makes sense to double check from above authentic sources.

If that is done then these kind of questions would not arise.

8 Likes

Thank you everyone for the feedback. Yes, I was looking at the standalone results from MC. Appreciate your advice Hitesh Bhai!

For Self Sustainable Growth rate see: Calculate Self Sustainable Growth Rate (SSGR) of a company - Dr Vijay Malik

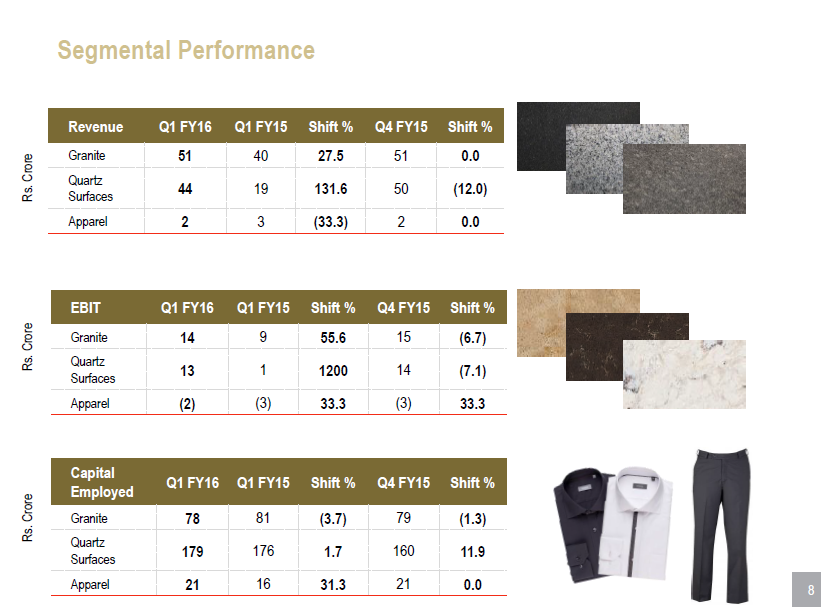

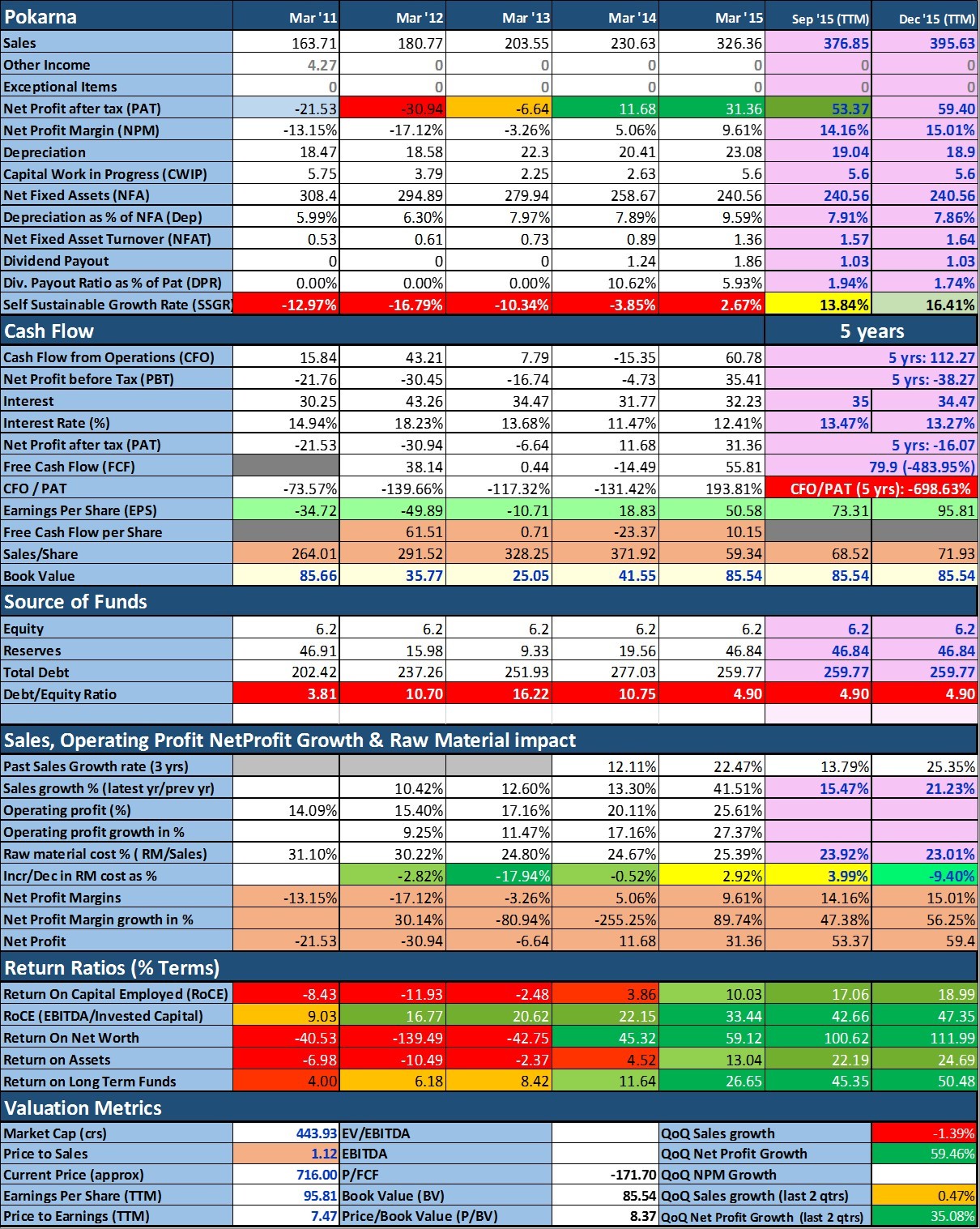

Maven there is no point in looking at standalone sales. You have to look at the consolidated sales where quantra’s profits are also added.

Quantra is under their Quartz division PESL (Pokarna Engineered Stone Limited) which is driving a major growth for Pokarna.

Below slide is copied from Pokarna’s 2016 Q1 Presentation.

Disclosure: 10% of my PF. Planning to accumulate more.

Does anyone know what is current capacity utilization for Quartz plant what are expansion plans?

@maven26 Thanks for sharing this…I have seen you do this for other companies as well. Really helps…Appreciate it

I have been looking at this company and the growth in its quartz segment is surely very impressive. However , I have a few questions and will be thankful if any of the board members can help me find answers to them

- Granite exports to US have been decreasing consistently since the past few months. Any particular reason for that?

- How significant is the Breton technology? If it is so vital then why is it that Chinese quartz has higher demand? I dont know of any player in China with that technology? Does it depend on the application of the product?

- As per https://www.zauba.com/exportanalysis-quartz+slab/hs-code-6815-report.html , the highest importer of quartz is UK. Pokarna has been supplying 70% of its products to US which means that it is not the only supplier like the boarders thought initially - which again brings me to this question- how important is the Breton technology since it is the “exclusive licensee” as per the company?

- What is the price differential of quartz import from india or china vs quartz procured from US itself. If it is an abundant resource then why do companies need to import it from foreign countries?

- What has led to to the sudden jump in EBIT margin of quartz to 49%(from 36%) even though the sales increased by just 10% QoQ in Q3FY16?

1 Like

More questions

- How is the brand name ‘Quantra’ significant if they cant even sell it in that name? Daltile is selling Pokarnas products under the brand name ‘One Quartz’.

- When a company undergoes CDR, the lenders in most cases place covenants on capacity expansion. As per the MRA, the company under certain terms and conditions may owe 23cr to the lenders (haircut that banks took on their loans) until 2021. How will they allow capacity expansion in such circumstances?

- How is the company selling its products? Caeserstone sells it directly to fabricators. What about Pokarna? Daltile is a fabricator so I am assuming they sell in the same manner too? Do they have dealers in the supply chain that in turn sell it to other fabricators?

- What are the gross margins in the quartz segment? Caeserstone was earning 45% until 2014( now reduced to 38% due to supply related issues) . Even then Spruce capital raised question marks on it. The report claims that 45% gross margins are ‘outrageously higher’ than it global peers? Even on a consolidated basis doesnt 72% gross seem a bit too high?