Thanks, good going for the quartz segment but we should not miss marked weakness in granite. Emkay had come out with management visit note where they seem to give outlook for sales growth @15-20% for both granite and quartz. They intend to invest in creating additional capacity for quartz by the end of FY18.

Sumit, could you plz send the link to the Emkay report?

Granite in absolute terms compared to Sept didnt decrease. i had a look at it.

I spoke to the investor relations couple week back, they say how Brazil currency is hurting Indian granite exporters. I think going forward, Granite growth will be marginally incremental. Quartz is where the most growth should come from.

Sorry, difficult to share the report but would share the main points later. This was just a mgmt interaction note without any research/analysis as such.

Thanks to google, found it in one minute ![]()

http://www.emkayglobal.com/Uploads/EmkayResearch/Pokarna%20Ltd.%20Visit%20Note_271115.pdf

Quartz imports to US went further up. Granite declined marginally from India. Directionally I think trend will continue, quartz will continue to expand and eat share of Granite.

Last 2-3 months Quartz from India to US growing even month on month. Can someone crack this puzzle if there is any other Quartz exporter to US from India than Pokarna?

I dont know why Pokarna has corrected so much, every time I search for alternate, I decide to stick with it. High ROE, higher 20% growth, huge size of opportunity, 1st mover advantage, minimal capex needed to expand. What could be the reason to fall more than 40% from its high when the fundamentals look so good, what am I missing? This one is testing my patience…

Does anyone know anybody in this Industry??

Waiting for the Q3 results…

Thanks-Mahesh

2 Likes

Mahesh

i hold pokarna - I did some detailed research

- quartz exports from india are going up for sure

- pokarna is seeing no slow down on that front

- pokarna’s key competitor caeser stone is seeing a big slow down as there have been allegations of fraud in their numbers

- there’s a rumour that forced margin selling of a HNI has resulted in a pummelling of stock price - of course, I can’t verify it

Let’s see how q3 pans out - if quartz looks alright, I intend to add more. of course, i have concerns on governance (on a SEBI indicted person on the board), lack of visibility on RM sourcing (as they do not own the mines themselves) and sustainability of margins.

High debt too is a cause for concern if operating leverage turns the other way.

1 Like

Hi varadharajan, were you able to get the reason why they burn so much money on apparel business? They are taking losses to the tune of 13 cr this Yr.

No but I think its some sort of indulgence fro the MD’s progeny - not good for a minority sharholder for sure

Yeah that is sad! I added more today. Now my average price is closer to 1000. I know I bought it very expensive but I fell in love with the product when I saw it in USA. I bought it just after coming back and sadly at that time it was around 1400. My game was that company might start building a brand in Engineered Stone in India and by next 5-7 years I might have a 50% compounder. As many people pointed out, I wasn’t able to find any company using Bretton stone tech to make this crystal so I thought this is the Gem I was looking for a long time. Now I just have a hope that promoter might get their act together and use this opportunity to create wealth for himself and his shareholders.

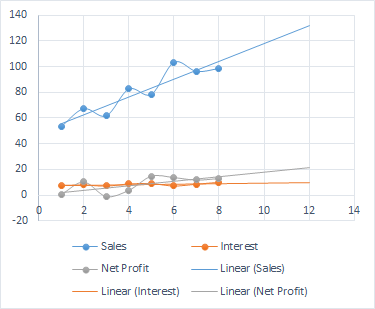

Just playing with numbers. The D/E ratio is very high. Too much loan or what ? The quarterly sales is growing faster than net profit as interest is rising faster. Is this the reason of stock price fall, that investors are finding net profits forecast subdued in coming 1 year +…

While quartz seems like a great product with immense scope and growth, I can’t see how the company will capitalise on the same given 80% capacity utilisation, and inability to do more debt funded CAPEX given high leverage. The last time company set up a line for quartz, it went into cdr.

As we pointed out above, Abhishek the moment company stops their garment business, it will be able to free up 30cr of working capital and will save 15-20 cr annually. All I have is a hope that promoter will someday understand that appreciation of market cap of his company also makes him rich. If that doesn’t happens then yeah they might have to go to cdr is things turn sour after further expansion.

Any further details on the results and how various products have performed in the foreign territories.

Appreciate anyones inputs on the same.

Good set of numbers by Pokarna. Net profit has gone up to 20.81 cr from 13.04 QoQ and sales are flat. Proportion of quartz has increased as expected and their Finance cost has come down from 10cr to 8.5 cr QoQ which is a good sign. Again apparel segment has been a drag. @varadharajanr if by any means you can contact the management and get the facts clearer then we could be sitting on a gold mine. Investment of 200cr(in quartz) is giving a yearly profit of more than 50 cr after all the interest expenses. Plus could you think of a possible reason why there capital employed in granites have gone up given the fact that sale of Granite in US is falling down?

It is trading at 7x FY16 EPS of close to 100+. Don’t know if market is building bankruptcy or corp. governance event!

Sumit it is a corp. governance issue but there are not clear cut indicators. Things like investing and losing money in cloth business (with interest) when their main business is doing fantastically, paying themselves first before the lenders, no investor con calls and increasing capital allocation where the demand is slowing down are a few concerns. The only reason I am invested here is that I like the product they make and the feel of the product is fantastic. Also 5 % stake by Ashish Kacholia gives me a little comfort with an assumption that he might convince the management to be more investor friendly.

Well, you know capital employed is Fixed assets + working cap so I suspect they have inventory accumulation/new machinery in the granite division which is ok since it will allow them to sell more in the coming quarter. Look, even redeeming own debt is ok to an extent since it was @14% interest while bank loan is less than 13%. The only big trigger for re-rating could be dividends or announcement reg. closure of apparel biz. I am hopeful they won’t blow it away.

The granite sales are falling because Quartz sales are rising in US (you can check the stone update page), so it doesn’t make sense to invest more capital in granite, also margins in Engineered stone are far more than Granite. I was hoping that they will go for further expansion in Quartz as they are already running near full capacities(their MD said that in some interview). They can even start marketing the product in India and we don’t have any shortage of Millionaires here. Also If you see their sales in Granite have more less remained stable with their apparel business burning money. One possible explanation as you said could be inventory build up but inventory build up of 14 cr with stable sales doesn’t look good given the fact that they already have so much debt in their Balance Sheet and expanding granite instead of Engineered stone would look stupid. I know I am a bit harsh but I am trying to understand the reasoning of all the above things.

Results are OK. Earnings are not disappointing. I am giving up on correlating Quartz imports to US vs Pokarna’s Quartz sales. Never matched until now.

Quartz grew. Impressive was the PBIT of Quartz segment. Nearly 50% of revenue and nearly 3 fold increase YoY. This is what I have been hoping. I will try and find out how are they preparing for the continued Quartz slabs demand. Granite is disappointing, when I last spoke to them, they told me how Brazilian currency has affected their Granite business (Brazilian Real has depreciated about 30% compared to about 9% Indian rupee vs USD in last 1 year). They also said proximity of Brazil to US helps Brazil companies.

I think Daltile’s quartz slab the ONEQuartz is all from Quantra. In next few weeks I will try and find out how is Daltile doing with its Quartz surface business. Housing market in US is doing great.

Instead of speculating and counting on public information, I would like to know if some can volunteer to meet the management in Hyderabad, I can try scheduling. Weird thing is (I have often felt strange) they dont respond to emails. They answer questions over phone.

Can we try to work on scheduling a meeting with management? can anybody help putting it together?

Thanks-Mahesh

1 Like

Today’s delivery of 67% and 71k shares is heartening. I averaged it around 700 more and my total Cost price now stands at 1100. Hoping to relieve some capital from this investment soon and maintain the capital I originally wanted to be in the stock.

Also it was encouraging to see a presentation and their statement about increasing value added products in Quartz. However still my doubt remains as we discussed above.

Mahesh I live in Bangalore so it is not possible for me to go to Hyderabad and ask the questions.

Thanks

Kanv