The Breton technology will remain exclusive for Pokarna till 2020. The risk of partnering is not that high as it needs huge capex to set up even a single line and I feel this provides good comfort for Pokarna

1 Like

Breton tech setup takes almost 1.5-2 years if done efficiently. Pokarna has exclusive rights till 2020, so even if there are some other tie ups post that, they will come online around 2021-2022. So, still a lot of runway for Pokarna’s additional capacity coming online.

2 Likes

Pokarna Results

QoQ Sales -2.6% & YoY -4.5% (Standalone r disappointing)

QoQ PAT222 % & YOY 36 %

Inventory 10%

Debtors -15%

Debt -3%

Interest -10%

We should see the consolidated numbers since Quartz surfaces is their major product line:

A decent set of numbers IMO. I am just wondering why they haven’t showed any capital WIP.

Disclosure invested at lower levels

Results look ok, considering the season (winter and snow) the last quarter nos looks pretty good to me, may be quatz did highest ever in this quarter. US housing starts have been increasing, lot of talk about increased construction activity should propel its growth in the coming quarters if they tap. So is the talk in India too.

Therefore, I guess it has better days ahead and predictibilty of the growth is not bad in this case.

On top of all this, in last 1 year the management is a lot transormed , if I can put it that way,

they restructured the debt and paid some of it, started doing more and more investor meets, decided to double the quartz capacity, got listed on NSE, have decided to split and create more liquidity, have agreed to dispose the apparel business. Developed new clients and markets (Ikea India).

So many significant developments and market has recognized that.

If we extrapolate the last quarter , its avialable at 10 times the cash profit which I think very cheaply valued considering the predictibility and the visibility of the growth in the business.

4 Likes

Conference call announced. Is this the first time management is doing conference call? http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/378dd8db-75cd-43c7-91ed-1e82e8f58ac1.pdf

No they have done it before. Go to researchbytes to listen one. Last time they said that they may dispose off garments divisions and now they have finally decided.

Company Presentation - http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/ed42b99a-8e56-4d50-9653-9563c379082a.pdf

Did anybody attend the concall? if someone did, could you plz update the details?

Ikea to open in Navi Mumbai by Jan '19 http://www.thehindubusinessline.com/companies/ikea-starts-work-on-navi-mumbai-store-to-open-in-jan19/article9706858.ece?utm_source=RSS_Feed&utm_medium=RSS&utm_campaign=RSS_Syndication

1 Like

I am just looking into this company and so was looking at their competitors. Found some reports negative on Caesarstone.

Link to one of the bearish views on Caesarstone - this is when their stock price was materially higher atleast from Aug 2015). Some of the views are of course specific to Caesarstone but some are generic.

- Quality of quartz vs granite; has anecdotal complaints but volume growth of quartz counters this trend unless the distribution channel has incentives to sell engineered stone. Other reviews online claim that issues are mainly due to installation.

- Raw material cost increase: Does Pokarna cover their entire needs from their own quarries? Could not spot the answer to this in the AR

Also, on a separate note it seems that this is now a fairly generic product with all using Breton technology; so if Pokarna sells at a lower price it still is a matter of spending enough on marketing to get it sold to the end consumer. Looking for caesarstone reviews gets quite a few; but for quantra couldnt find anything except a person asking for opinions since there were no reviews:

Any view on the channel and how this purchase decision gets made? The end consumer is unlikely to be familiar and might be strongly influenced by the contractor/architect/etc.

3 Likes

My notes from the concall -

-

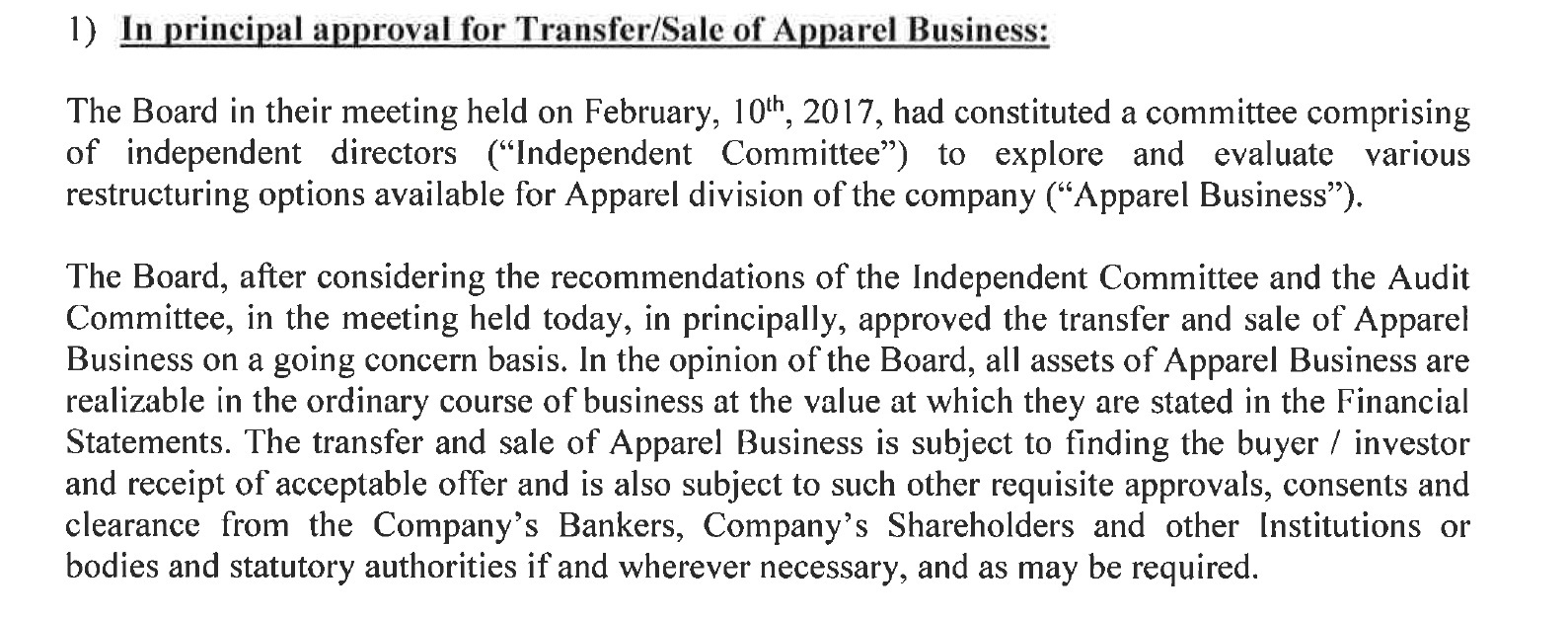

Apparel business performance remained muted. It was decided it would be sold provided they find suitable offer/buyer. A committee has been formed to take care of the matter. This is been done to remain focused on the core stone business.

-

Multiple headwinds like competitive intensity, lower realizations, excess supply impacted granite business. Prices barely met the production costs. We want profitable growth, do not run after topline…so took backseat and didn’t chase lower margin granite business, even if it meant lower revenue. Focusing on cut to size segment where realizations are better by 15-20% than slabs business. Pricing pressure will remain as Brazilian companies are flooding US market with their product. New color with little competition will have higher realization. Brazil is blessed with much more granite colors than India, but Indian colors that are in demand (costing is much cheaper) and we will have our share going forward. Even here, value addition is important to get better pricing. US market (where it is mostly used as Kitchen counter tops), granite is being replaced with Quartz. They probably believe granite’s negative scenario is at the bottom, and won’t go below this.

-

Valuing/analyzing granite business is difficult as what is good today might not be good tomorrow. Price varies based on colour, size etc. But what is in demand today might not be in demand tomorrow. So, everything is a variable of time. Along with, product varies from quarry to quarry and even in the same quarry, while costs remain the same. So margins differ and it is difficult to give guidance in this business. Currently they are doing 22% EBIT (24% last year). On the question whether it will not go below 20%, they were positive, but again repeated that with natural stones, anything can happen.

-

Giving actual % utilization in granite is not possible. Enough capacity is available to meet any aggressive plans going forward in granite business. They are focusing on granite mining side and have recently started a new granite mine. Capacity utilization has to come from all three verticals - right from slab, cut to size, and mining business.

-

Quartz delivering sturdy performance backed by strong demand scenario. Improved product portfolio has helped maintaining momentum. Plans to increase capacity and partnership with Ikea should further consolidate their position along with increasing the reach and visibility. Ikea would be like any other client. We would be looking for newer tie-ups in India and abroad going forward. No dependence on Ikea. Ikea helped Caeserstone dominance once they tied up exclusively in 2013. Pokarna panning to launch Quartz in India on their own through kitchen and bath stores, builders, architects, and will be doing aggressive marketing and proper education on how different the quartz is and also the difference between manufacturers. 5 years from now, fair to assume that 25% of the quartz business will be from India.

-

In Quartz business, focus is on getting higher realizations rather than making more slabs. What matters is per sq. mt realization. So, utilization level is a function of value addition. If you are doing more value addition, utilization levels would decrease, but at the end of the day, it would compensate with higher realizations. Pokarna’s margins are best in the industry despite RM cost headwinds. Polyester and crude prices have increased in last 1 year.

-

In Quartz business, current run rate is 58 cr, peak they can attain is 60 cr… as they have inventory.

-

Debt cost will be reduced by 300 bps. Lead bank has confirmed, waiting for other banks to follow.

-

New capacity should be online by q2 FY19 i.e. by Sep-Oct 2018. They are projecting 60% capacity utilization during first year of operation. So close to 100 cr topline addition (first 2 qtrs). Peak will be 250 cr for full financial year of operation of new line. Margins might be better from this new line, as they are trying lots of different very difficult first of its kind things with this highly updated new line. They have sufficient visibility to utilize production from new line. They will try to maintain at least the current margins (45-50%).

-

Competition is already there in Quartz, and more players are coming in. Their biggest advantage is Breton tech. where we are exclusive participants. Other new entrants will be working with Chinese machines where the end product is not as good. Pokarna’s market reach is good, established customer network, and have best technology around.

-

Ikea business will fuel growth from next year. They are planning to open their first store in first qtr of FY 19. Currently the relationship is only for India for this product, but things can change going forward.

-

Receivable days have reduced significantly from 73 to 64. Inventory days have increased from 82 to 94. Small variations would be there depending on various factors such as shipping lines, customers holding dispatches for a few days.

-

Upcoming qtr might be soft owing to shutdown (15 days) of quarts business for maintenance. Looking for 10-12% growth in quartz topline until new line comes online. SO whatever comes in is going to be bonus!

-

On the question of them not being cautious as they are planning to take 250 cr debt when they have just come out of CDR, Mr. Jain was dismissive. He said they would like to fuel this growth through debt as it is cheaper than raising money through equity. Cost of these new funds will be around 5-6%. It would be LIBOR + x, so a natural hedge.

-

Breton exclusivity – Breton does not like to work with new players. Even they want to maintain exclusivity of their priced technology with the current players. Mutual understanding is that every 3-4 years existing players will go for capex, and will continue with their exclusivity. They had exclusivity for 10 years, and now with the expansion coming in, exclusivity will be there probably. There is no revenue sharing. Upfront costs are there. They keep getting know-how from Breton during the course of the agreement.

-

Land acquisition for the capex is almost finalized. Breton would be sending new line in Aug, by the time it reaches Pokarna in Hyderabad, would be September.

-

Margins will be impacted owing to RM and currency changes. Cannot do anything about it.

-

Capex of 34 cr was done in FY2017 in granite business and 5 cr in Quartz business.

-

Will try to focus on US but will explore newer unrepresented geographies like Australia and Africa in future, if need be. They have very good network in UK now, good market in Palestine, and few other places as well.

-

Working capital requirement for the two businesses (granite and quartz)…quartz is more predictable. With granite, problem is that if the quarried stone is not good, they might have to buy it from the market, which means additional time and cost…and things like that.

-

Regarding mines, quality is important. No one can assess quantity with accuracy. They have quartz mines which they haven’t exploited yet. They are just quarrying in granite segment at the moment. Their entire quartz business is based on third party mines. On the question of Quartz RM being in short supply, they were honest – Said, every good RM is usually in short supply. At the moment they don’t have any issues, but things can change. So, they have kept their own mines in tact.

-

Tax rate to be 25%.

-

GST impact?

18 Likes

Thank you Mridul for the Conf call summary

Is Breton technology exclusivity for a certain region or how else is the exclusivity divided up?

Exclusivity is for country…pokarna is the exclusive breton partner for India.

Thanks a lot for the update Mridul.

A quick back of the envelope calculation on expected steady state PAT when the company ramps up fully:

FY17 PAT: 70 Cr

Adding back Interest + tax of 52Cr, EBIT = 132Cr (incl. other income of 10Cr)

Current EBIT from quartz: 95 Cr

Best case scenario:

Incremental quartz EBIT after 1.3x growth and full capacity : 95 x 1.3 = 123Cr

Interest = 6% x 325 Cr = 20Cr

EBT = 103Cr

PAT = 72 Cr

Incremental PAT from sale of apparel = 2Cr

Total Incremental PAT = 75Cr, implying 109% upside to PAT

The timing is the issue here. As per concall notes this is achievable by FY20, which is about 3 years from now.

At CMP, the share is available at 13x FY17 EPS and 7x FY20e EPS as per my calculations above.

Discl invested at lower levels.

guess it is fairly valued then. Capacity expansion is one off. Such businesses are not secular scalable businesses and usually are given a pe of 10 or so