@kanavgarg123 FCF is obviously going to be negative with rising debt.

bhai that will depend upon the repayment terms. For Example Currently Pokarna has a FCF of 80+ cr per year after paying interest cost and taxes. Now with the increment of capacity by 130%, their FCF should double at the least. Their LT debt is 171 cr. which is just 2* fcf. After capacity expansion, their debt would be 420 cr but their FCF will rise up to 160 cr. With this much cash, they can easily pay off their debt. The FCF i am taking about is CFO - Interest Cost - Tax. I hope that clarifies.

Kanv

@kanavgarg123 If you use a generally used terms like FCF, it will be assumed to have the text-book definition (which is Equity buyback+ Debt repayment + dividend + interest repayment). What you mean is post interest operating cash flow. This will double earliest in FY2020 (as capacity starts production in FY19) and ramp up will take time. But this assumes full capacity utilisation. So while it will have cashflow to repay debt by then but it will once again hit the growth hurdle as it will be operating at full capacity and another large capex will be on horizon….if growth is to continue….

Correct and that is why I clarified after realizing my mistake. I took that assumption because

- Pokarna is the cheapest producer of Quartz and their brand recall is good as mentioned by someone in the group after talking to dealers

- Tie up with Ikea will absorb the capacity as their requirements are far far higher than the production capacity of pokarna.’

- We are yet to factor in the India demand. Engineered stone is of superior quality. Ikea stores locally should bring Quartz into the eyes of India public and that should increase the demand substantially.

Some amount of debt is required for the businesses to run. Post interest and tax operating cash flow with a little debt should be able to finance the third expansion hence we won’t run into the debt spiral.

Lastly, small cap businesses contain inherent risk of capex going wrong. I see higher rewards in this business as the valuations are comfortable. If the capex go wrong then yeah, the company may die but the reward look sufficiently high to me to take the risk.

Is Italian marble same as Quartz/ Engineered stone?

Disclosure: Exited a few months back

Flattish to poor results by Pokarna

However Notes to accounts have an interesting development. It appears that management might actually be getting serious about selling apparels division.

Sachit

2 Likes

Market is hammering Pokarna today, but I really dont understand Why? Result is flat but not very bad for such steep correction in a day. And management is thinking about selling/disposing off the loss making apparel business, if that happens it’s a huge positive for the company and EPS will be around 150 to 200 soon, and an 15 PE makes the price to 2250 to 3000 - at least double from current level. But market does not recognizing that. Is there anything I am missing here?

Even I was wondering the same thing. However, we can see this as a reversal of a recent rally. I expect Pokarna to post flattish results until Q4’18. The new Quartz capacity will kick in Dec 2017 and IKEA will start absorbing capacity from then on. So another 4 quarters of flat results. Further, with addition of debt I wouldn’t be surprised if the company posts some losses too. However, we an expect the company to repay its debt of 230 Cr in less than 2 years from then. So after Q4’20 we should see a clear picture of earnings improvement.

It’s a long story

Discl: Invested

Hi,

Sharing my notes of Q3Fy17 Concall.

- Better profitability was a result of:

- Consistent performance of quartz

- Better cost control

- Lower interest exp.

- Granite:

- Challenging environment prevalent at present.

- Realization remain under pressure owing to excessive supply.

- We are focusing on cut to size business more, where realizations are better.

- We get help/benefit from having captive quarries.

- Our focus is towards profitability and sustainability of business.

- We are hopeful to be recognized for what our services are worth in the long-term.

- Quartz:

- Continues to perform consistently.

- Our efforts to develop new and improved product has helped us develop good relations with clients.

- We are confident of our effort in growing this segment and improving brand visibility will help us grow business sizably in coming years.

- Apparel:

- Performance remain muted.

- We have set up a committee to decide the fate of this business.

- Continue to participate in international exhibitions.

- CAPEX in quartz segment

- 130% capacity increase.

- At an expense of 325 Cr

- Expected to be completed by jun 2018

- Bank loan of 250 Cr in foreign currency terms @ 7.5%

- We have right to use exclusive breton technology status till Mar 2020.

- New facility will be most advanced technology.

- Machine will be supplied by end of aug. post that we will start erection process. Following qtr will be used for dry runs.

- 195-200Cr will be for machine part.

- Partnership with IKEA. They will gradually ramp-up their business in India.

- Pain in granite segment will continue for some time. However, we are positive for our strategy to play out in the long-run.

- Slowdown is for 2 reasons:

- Change in the thickness that was supplied in the market.

- Maintenance which was carried out during the Qtr affected production.

- Several players from Brazil, China and India are trying to dump granite in US market.

- Our focus in granite is more on the quarrying side of it.

- There are couple of domestic players in the US market under quartz. America doesn’t have granite quarries and quartz RM so Trump’s policy should not be disruptive. At present we don’t have any import charges or restrictions.

- Capex Process:

- We have bank sanctions in place.

- Signed purchase agreement with breton.

- Shortlisted land and requested govt for approval.

- Break-even will be @50-60% utilization.

- Peak 80-85% utilization in 3 years time.

- Interest burden is mainly due to Indian currency loan. We have already requested our bankers to convert it to foreign currency loan.

- Int. Cost 24 cr in 9 Months (PY 9months 47Cr)

- Foreign currency loan will be available at 7.5% vs. the current rate of 13.9% on indian currency loan.

- Looking to convert 70Cr

- In quartz major RM is quartz and resin.

- Resin prices are dictated by global oil prices.

- Margins have come down because of resin prices going up.

- Quartz is a more technical product than granite. Over the years we have developed a ready network for upcoming facility. So, it will be a better experience than we had in the past while setting up quartz for first time.

- On annual level we will be able to maintain EBITDA level what we had in PY.

- New quarry is operational and the colour has been well accepted by customers. We need 1-2 more qtr to get full fledged productivity. This quarry will play an imp role in future turnover of the company.

- Granite side improvement investment are already made and it is an ongoing process. Not looking at any major investment in granite side.

- We entered UK market in Q3 and have one of the important position there in terms of customer. Traction in other european market is decent and we are not very aggressive in entering there as that is 12mm market majorly, while we are more into 20mm. (UK is a 20 mm market).

- Sale is not just on the basis of cost it also involves service level. Pokarna offers relatively better service level in terms of lead time to our customers.

- We still have scope to improve our capacity at the current quartz plant.

- Granite has both domestic(40%) and export (60%) sale.

- Demonetization not much of a effect as we are not in retail. These orders are not instant in term of payment and installation.

- 2 types of shutdown:

- Maintenance

- Upgrading from time to time provided by breton to improve quality and efficiency.

Regards,

Yogansh Jeswani

Disclosure: Invested (I have tried to cover major points and it is possible that I might have missed some detail. Please consider the same and do your own due-diligence)

11 Likes

thanks for these notes yogansh

i think a lot of hair around pokarna has gotten cleared in teh last 60-80 days.

-

the company has stated its intent of adding capacity which can double its quartz turnover. Given the operating leverage, this can potentially do about 220-250 eps in about 3 years’ time.

-

the mgmt has realized the drain from teh apparel business and they have shown their intent to act on it. if they do, this will remove another drag

-

granite continues to be under stress and reversion to mean is sometime away. but the business is managed for cash flows and margins and not for growth - that’s a positive sign. if this reverts to mean in 2 years time, this will add to the EPS - that’s an optionality.

given teh robust housing market in the USA, dollar staying strong, the demand environment for quartz is quite robust if the managemeent executes well (they are adding lots of sales people to sell quartz in europe/USA), this can re-rate over a 3-5 year time frame.

ashish kacholia increasing his stake is a positive sign too. other triggers could be appointment of professional COO/CEO and better quality board members. For a 20-25 % eps grower, 8.5 ttm pe is quite cheap imho.

Adjusted cash flow yield - viz., OCF - interest payments is about Rs. 70-75 Cr. and that’s a 10% yield on today’s mcap - which basically discoutns all future growth and accretion from divestment of the apparel biz. Given teh huge operating leverage in quartz, margins could go up after an initial j-curve from the new capacity. lets see how this plays out.

discl: i hold from 700 levels and added at around 1050-1100 recently again.

11 Likes

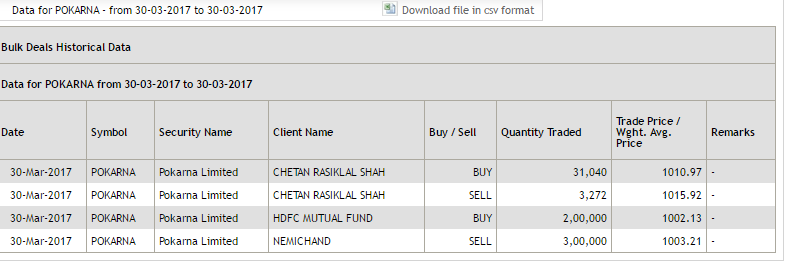

I see Hdfc MF buying 2 lakh shares ( that’s roughly 3% of equity) but do we know who nemichand is ( is he part of promoter group and why did he sell such a large qty?)

Currently Pokarna is only covered (as per me) by HDFC and Equity master and hence when it becomes well known and gets in B2C space thru IKEA in India or otherwise ,upside in future should be huge -surprisingly Ashish Kacholia has high stake(8.2%) in this

1 Like

The above report is from one of the largest research company -they are talking global trends and mentions world wide only 4 companies and Pokarna as one of them

As per Freedonia, the global countertop industry is expected to be around US$95 billion. The market is currently dominated by the extensive use of granite and solid surfaces. However, in last four to five years, the demand for the engineered stone (Quartz) has outpaced the surface/countertop industry. Over 1999 to 2016, global engineered quartz has grown by ~18% CAGR.

quartz is 15% of USD 95 billion -that is the share of prize for Pokarna ! the global market leader (Caeserstone) operating margin is 25% and Pokarna 45%+!!(even though Caeserstone charges almost double the price that Pokarna charges).One of the reason is the raw material advantage …It will always help Pokarna to command better margins than its global counterparts and will help it gain market share if it wants to pursue competitive pricing. Over last 7 years Pokarna’s Quartz business grew at a CAGR of 60+%, whereas Caeserstone’s top line grew by 18%.

5 Likes

http://www.pokarna.com/wp-content/uploads/2014/04/Shareholding_Pattern_Q4_2016-17.pdf

As per the latest shareholding, ashish kacholia has increased the stake from 7.1% in dec’16 to 7.5% in Mar’17

Seems there is a disconnect. As per latest shareholding on BSE website for Quarter ending March 2017, Ashish Kacholia’s name does not appear. Either of the report is faulty.

http://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=532486&qtrid=93.00

I dont see HDFC securities also in the list, I saw a new shareholder PCS securities with 300k shares.