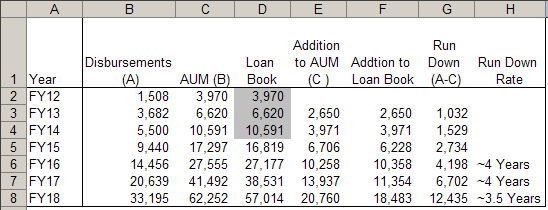

Does PNB disclose its prepayment rate? It appears to be high based on disbursements and growth in AUM and loan book.

Source: PNBHF Company Presentations

PNB’s portfolio rundown for FY18 was 12,435 Cr which is approximately equal to its AUM as of H1FY15. Thus PNB’s rundown rate is approximately 3.5 years compared to LICHFL’s 9 years and Canfin’s 6-7 years. This means there are lot of prepayments because average maturity of a loan must be about 15 years. A higher prepayments means PNBHF loans have high interest rates and people are switching over to cheaper loans. If high interest loans are prepaid, only low interest loans will remain on the book and this will affect spreads in a rising rate environment. LICHFL is already facing this even though its prepayment rate is lower.

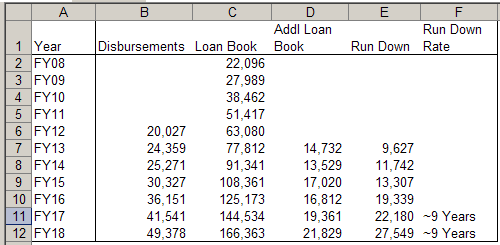

Same calculation for LICHFL is below

Source: LICHFL Company Presentations

LIC’s rundown period of 9 years means approximately 11% of the beginning portfolio runs off in a year. This is also mentioned in the presentation.

Source: LICHFL Company Presentation for FY18

@Yogesh_s T here is so much to learn from you the way you weave out real stories in the form of insights out of numbers . I think you ve hit upon a very important point and why let me tell with my personal experience .

In 2014, when Bangalore real estate dried, many developers came up with double your money scheme in exclusive partnership with NBFCs. This led to 100% loan approval for developers at retail house loan rates and passing all the risks as onus of retail junta who got lured by double money scheme. Under the arrangement, builder was supposed to pay interest till property gets ready n buyer if not interested could return n get double money of equity. The whole assumption was real estate market will revive in 3 years . NBFCs for opportunity to show stupendous disbursal . Fast forward 3 years down the line and situation is -

Builders r in tremendous pressure n ve asked buyer to forget double money scheme

Builder not even paying interest n buyer to save his credit rating is paying

Those buyers who leveraged n not able to pay are defaulting

Those who ve accepted the fact that it was a trap n now holding house are shifting to SBI as NBFC exclusivity period ended n they r finding SBIs at cheaper rate of lending

This is my personal experience of 1 project with 1300 units where I purchased for living purpose but m aware of many guys purchasing more than 1 unit under double money scheme n some defaulting as chain of mails circulated in buyer group . The project is related to Mantri n NBFC is PNBHFL. I did not highlight on this forum because I was never aware if PNBHFL exposure to such projects was significant or very less but the way you dissected this data and what’s happening on ground made lot of sense. I remember there were many builders with such schemes during 2014-15 .

May be one can check in concall share of such projects in disbursal loan book n take a call if is too small to ignore or needs some serious thought. Personally, my exclusive loan tenure has ended up n m also looking to shift to SBI as I find PNBHFL rates costly

Infact one of the companies whom they acquired called Andromeda was the 3rd party during 2014 which was managing whole show between Mantri, PNBHFL n customers .

Disc : The intent of post is not to create panic but just to highlight the possibilities of may be scenario why @Yogesh_s is getting those numbers out of his analysis . Please do your own research n due diligence. This could be a small part of PNBHFL overall exposure or could be bigger. I do not know. Not invested n not interested

@suru27 Can you please put some light How PNB Housing’s prepayment closure is co-related with your experience in Bangalore? Your experience could be result to rise in NPA but though pnbhfl is increasing its AUM 50% rate but GNPA quiet stable. Prepayment happen for every NBFCs that does not mean it is fishy

@Yogesh_s You will get your answer in Today’s concall. It was well explained by management with proper data.

The whole reason of staying with pnbhfl is because they were the exclusive partnership under the scheme n no other or bank was providing loan under this scheme . Others were providing simple construction linked loan. So, once 3 year construction period gets over , you either move out with double money (which did not happen ) or you start paying full EMI ( because developer defaulting on promised interest payment ) which means it is as good as any common housing loan where 100 percent disbursement has occured. So, if there r better interest rates available in market why one should stay with PNBHFL n not a SBI (if project is SBI approved ). Also, please note I m trying to correlate between what’s visible in those numbers and what I am seeing on ground in one of projects based on personal experience and I am not claiming this is the big picture. Will iterate again I am not sure if this is a small part of problem or big problem. You may google on pnbhfl mantri webcity money back scheme ,special on real estate related portals.

As I have said above , I am not sure how big or how small is PNBHFL exposure to such accounts and hence I will refrain to make any comments on above. It’s up to one to dig facts . I have just highlighted what is happening in one of the projects.

Never felt the need to update but when saw the numbers at bigger level highlighting prepayment and smaller loan tenures , felt worth sharing it.

If retail junta keeps paying free interest on time as it’s their rating which will be screwed , it will add more profit , if they default , I am not sure if there would be some kind of arrangement between these 3 parties , you can deep dive on ground .

Also as I was not interested in double money , when builder could not make free interest payments after 24 months of successful payment and approx 12 months pending, I settled with builder with a bigger unit and started my direct EMI payments (not the interest which builder was supposed to pay ) but there are guys who are not willing to settle (may be their sole intent was investment and now when builder defaulting on interest , they are stuck) and some defaulting (as per mail circulation ). Again , I would repeat I am not sure how small or big the issue is. Please do your own due diligence .

Hope this helps .

I never mentioned it’s fishy or not as I am not aware of scale of issue n hence I ve emphasized to check the scale of exposure to take a call on extent of issue

If you ask my opinion, I think builder n lender r safeguarded legally n it’s the burden of retail investor who took such risks for greed of doubling money.

Request to you and all the fellow boarders please go through the latest concall . All the doubts/concerns related to dubious Builders Lending, compression in Spreads,LAP portfolio ,Parent issue is well answered by Gupta-ji with proper data. Now ball is on our court whether we will believe Sanjay Gupta’s data or not . To ride on any growth story we need to give benefit of doubt to management and here I considered I will do it so by giving the same to Sanjay Gupta and Team. I am also like other boarders who hate PNB brand but invested in this business solely due to Sanjay Gupta and Caryle.

@suru27 Thanks for sharing your experience. It shows that PNBHF is aggressive in marketing loans in order to grow at astronomical rates. This is common in PE backed firms who are trying to achieve an escape velocity. There is nothing wrong in being aggressive as long as it is not unethical or illegal.

PNBHF’s loans are not sticky and entire portfolio is running off in less than 4 years. This is well below peers who can hold on to the loan for 6-8 years or longer. I did a similar analysis on DHFL and it has a runoff rate of 6.5 years. Runoff rate is also declining although by a small amount. Peers have seen a gradual increase in runnoff rate. This is the downside of being aggressive and may even be an indication of mis-selling.

I am not sounding any alarm bells here just sharing my observations from the numbers I gathered from company presentations and inviting counter views from investors in the company.

@Yogesh_s - Not tracking PNB Housing closely, though will loan asset sell-downs effect this run-down calculation? For instance IBHF is an aggressive seller of loans, which they do to conserve capital and improve ROEs. PNB Finance might be doing the same thing which effectively brings AUM down.

By the way, what is the exact difference between AUM and Loan book?

@Yogesh_s There is a book called “the unreal estate” by one of industry CEOs which highlights how real estate financing has changed over a period of time where one’s exit was others entry point (it would be worthy to validate by crunching data of claim that bankers stoped lending to real estate in 2011 due to risk issues and that’s where NBFCsgot aggressive,I think I ve read some research reports validating 6 % bank credit growth this sector against high double digit NBFC. I am talking of construction finance not home loans but I think double money schemes r situations when lines between both get blurred n I find myself confused where to place such loans ). Worth reading if one is invested in real estate sector in any form. I am invested in this sector through both developer n financing companies hence just try to keep my caution factor alive as I see some merit in bears finding fault in those investments. For example, Ambit came with a bearish report on this sector including PEL n i have good allocation in PEL. Though what I saw on-ground , kind of agreed on report but I think ultimately it depends on how companies handle it if hard time arrive, also how they manage their own portfolio as nothing comes without risk n most important how much of conservatism we investors have put in valuations considering past growth and future expectations . Last month few articles were published on how NBFCs are helping developers to get sales done and how new lending products r emerging (to overcome current crisis basically in my opinion ), I think, they are continuation of same where Ambit left it with a bearish call, companies are using their business acumen to fight that bearish outlook in best possible manner.

By the way, coming to PNBHFL, on service front , I think experience with PNBHFL was very smooth whenever in last 3 years I had interaction like for transfer of unit n loan etc.

My calculation of runoff rate for PNBHFL is based on AUM and not loan book. Look at the screenshot in my earlier post. Runoff rate based on loan book will be even lower.

Sell-down activity at PNBHFL is still low. PNBHFL earns only a servicing fee and not spread income on these sold-down loans so it may not be as ROE accretive as it is for IBHFL or HDFC. Sell-down activity will only free up the capital which can enable company to grow faster. A silver lining is that unlike IBHFL, it does not provide credit enhancement to buyers of sold down loans.

I have not done a comparison of the run-off rates of different real estate NBFCs. It is possible that 4 years may not be very low for the kind of portfolio PNBHFL has (50% home loans). Home loans have average door to door tenures of ~20 years and average run-offs of 7-8 years. LAP, Construction Finance have much smaller door to door tenures and hence run-off much quicker. Reliance Home Finance has ~50% home loans and its run-off rate is also ~25% (4 years). Till the previous year, the run-off rate was much higher for Reliance Home Finance (lower average tenure of the loans). The management is comfortable with 25% run-off rate and expects it to remain at similar levels.

PNB H share prices are unable to move beyond 1400 despite very good set of numbers. Now a Carlyle stake sale would further dampen the market prices.Lot of lessons learnt.

Never buy stocks in large quantity during sector bullishness-Last year HFCs were on fire

Do not blindly follow famous investors- You know whom I am referring

PSU name tag and the scandal of PNB is a drag

When overall market is weak - good performance does not matter.Wait is invariably longer and so opportunity costs are higher

In the Indian context very few stocks are real compounders where you can invest reasonably large quantities-all the rest need to be very watchful or prone to sudden weakness -no reasons known

A stock doesn’t move for a year and investors have 10 learnings, compounding needs patience and that is a rare trait in investors… and we all know compounding is not a linear line

Question we should be bothered about is: has it shown any deterioration in performance… answer is no…it is faster growing HFC with improving ROEs… Who could have predicted all these events 1 year in advance… well if you see the picture 3 years forward… you are probably looking at 12PE 3 years ahead and may be 2.2x book… Can it stay there?

Now one can look at 3 years forward picture for other NBFCs and take his call… if scared one can just diversify, as there is a sector tailwind, into likes of: Edelweiss, Piramal, Bandhan, Bajaj Finance etc(just examples of strong growth and able management NBFCs)…

On following key investors, the story remains true for investors and all humans… heads(favourable event)=“its me”, tails(unfavourable event)=“luck/govt interference/global markets etc etc” … having said that if you like someone - follow his complete portfolio along with %allocation, not 1 stock.

. I think you ve hit upon a very important point and why let me tell with my personal experience .

. I think you ve hit upon a very important point and why let me tell with my personal experience .