HFCs aggressive loan book growth in past without proper underwriting could spike NPA in future once loan book near to ripe!!

Please post the source before making a statement like this or else stop speculating

1 Like

i see lots of posts on equity dilution…the only dilution they did was when then came up with ipo ( which was necessary else we will not be discussing the stock)…apart from that there is no equity dilution…ROE will improve in coming quarters as they utilise their capital…which is matter of time…pnb stake sale doesnt dilute the equity…

Disc: I am invested

3 Likes

Share capital increased every year from 2012 from 30Cr to 165Crs for PNB Housing Finance as per screener which was what I meant by. IPO is not necessarily the only way for equity dilution. It could have been additional equity raising from existing shareholders.

1 Like

@SlownSteady, yes you are right that PNB HFC diluted the equity past years. The reason behind that Opex to ATA, CIR was very high then (Due to rapid branch Expansion etc )which came down significantly now so the consumption of capital will be much lesser. Securitization will be also used to reduce capital consumption as per management commentary. risk weightage of housing is also reduced. Don’t think management need capital fusion in near future. Management also confirmed the same in past con calls.

6 Likes

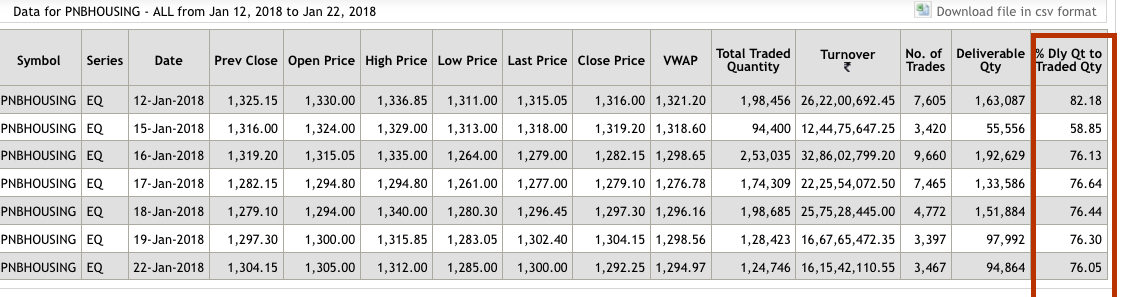

Astonished at the consistently high delivery percentage, and isn’t it strange to see 76% for 5 sessions in a row? ![]()

what do you infer from this?just trying to understand as I am new to studying this aspect of delivery

IMO 70% plus is considered high. That its 76% for 5 straight sessions is amusing

is it positive or negative for the stock?Stock is down by more than 20% from its high.

Yes, Its generally considered positive.

Many mutual funds are increasing their holdings in these.

But there were some news in last few days that NPAs could rise for Housing Finance Companies. So, trade cautiously.

I feel it is a boggy raised by vested interested parties to garner stocks. Read Edelweiss report saying - total loss of money in a retail house loan is less than 4%. Loan is given at half the value of house, no family wants to loose his home, hence most of the NPAs are temporary in nature. Even if someone defaults, money is easily recovered by selling the house. RERA bad effects were temporary & are declining, now the good effects of RERA will start. See the good results of Gruh & DHFL. Today Canfin, PNB Hsg & IBHsg results may reconfirm it.

2 Likes

Loss of money is in LAP segment and loans extended to builders not in individual housing loan.With interest rates coming down and PSU banks also joining the competitions, margins may come under pressure.My take is RERA positive impact in all segment will kick in & disbursement are likely to increase with lower margins.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/96d4dd59-7962-4942-9f58-48587666a2c8.pdf

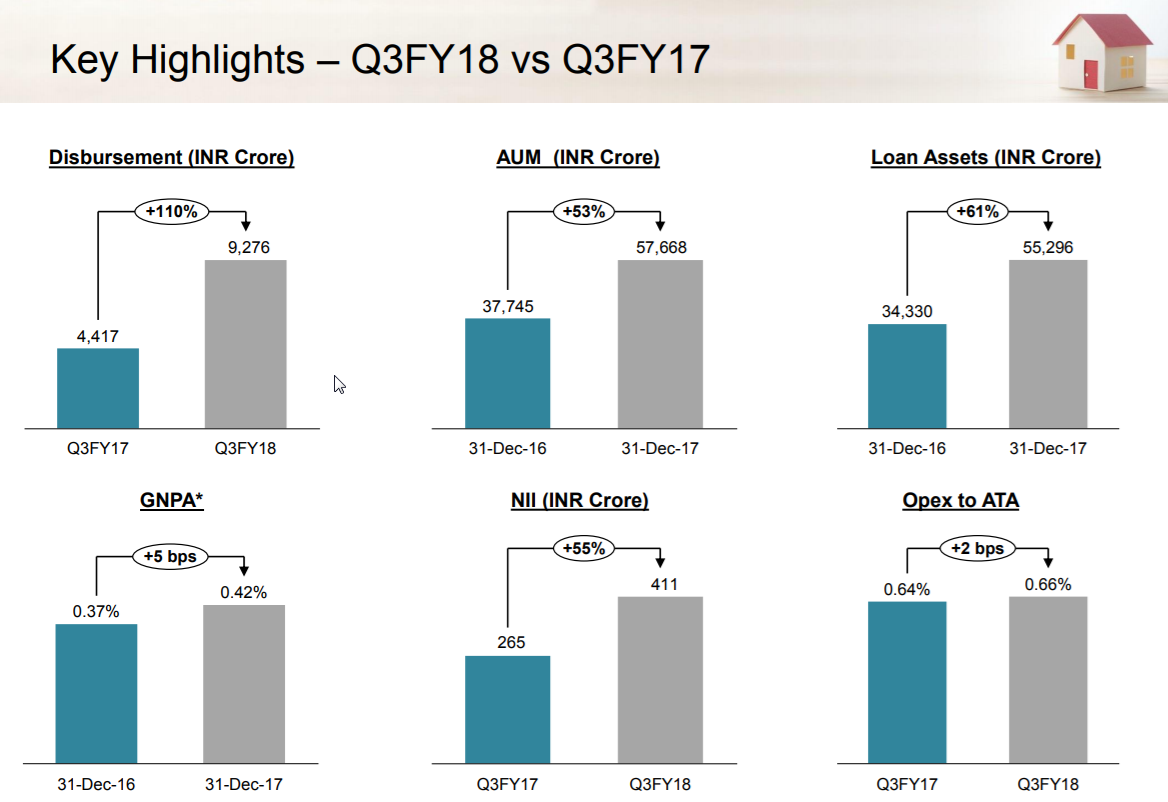

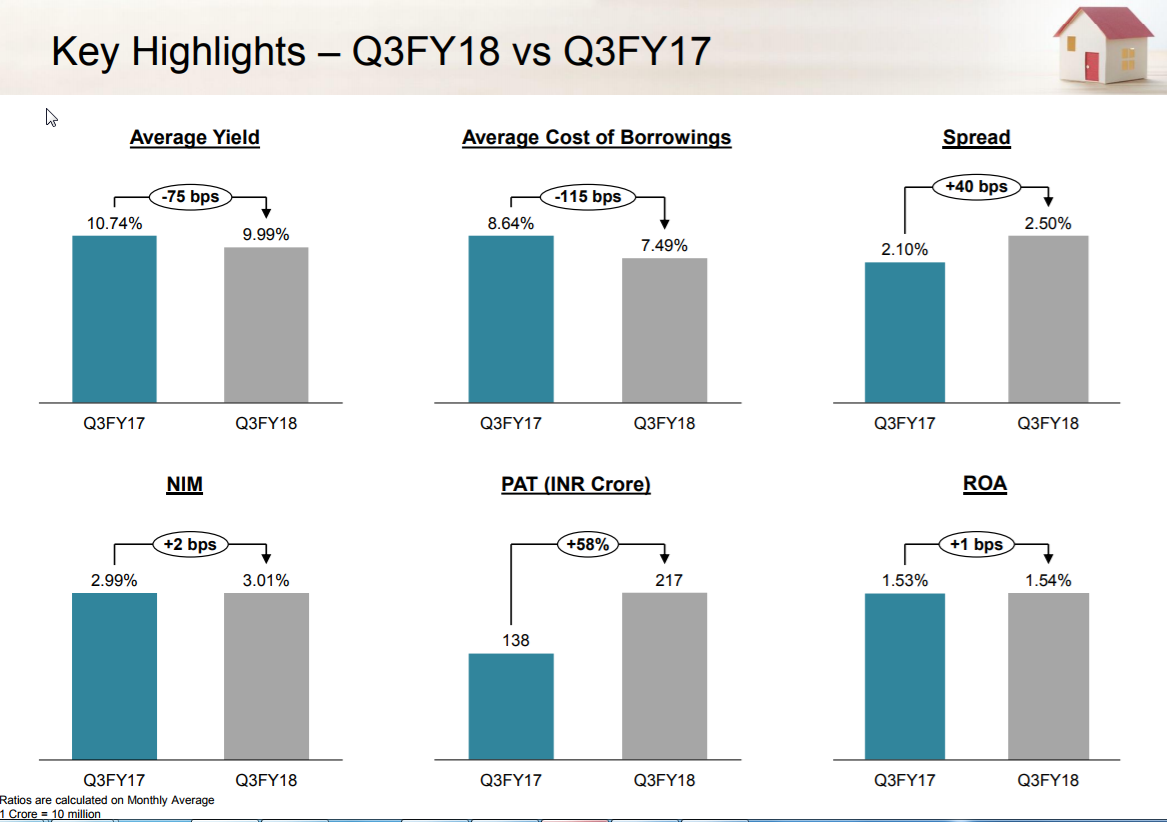

Results finally out! On expected lines, profits grew above 40%

PAT up by 51% while EPS grew by 44%, is this divergence due to the IPO ?

Results: http://www.bseindia.com/xml-data/corpfiling/AttachLive/96d4dd59-7962-4942-9f58-48587666a2c8.pdf

Press release: http://www.bseindia.com/xml-data/corpfiling/AttachLive/44da3675-ff33-4683-94df-d43b672b0541.pdf

Investor Presentation http://www.bseindia.com/xml-data/corpfiling/AttachLive/4eefccab-0c7c-4cfc-a2b1-ec799b912ad5.pdf

4 Likes

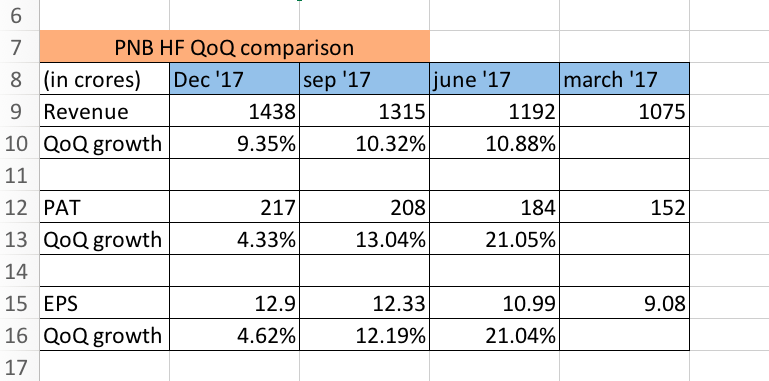

As YoY comparison isn’t effective ( at least until the effect of IPO goes away), I was looking at the past 4 quarters

I guess the fall in growth of QoQ profits is because of finance costs (rose by 10.6%) rising faster than revenues

3 Likes

your and other members opinion on the result pl keeping in view the current price?

Did you guys notice the CFO resigned on 21st Dec and left on 5th Jan? Until yesterday a new CFO is not in place.

it takes time to hire someone from outside. also the new appointee will

have to serve a notice period in his/her place of employment.

I am amused to see that the CFO didn’t have to serve a notice period at PNBHF!

1 Like