if you are new in the market and have a small corpus/not much time for market my suggestion its better to start SIP in some good consistent MF which are run by excellent fund managers.

2 Likes

Awesome thread and thanks for all the knowledge sharing. I have a very basic question about MFs. So even if one wants to invest in MF for a very long term (keeping faith on MF manager), does the action of other investors in the same MF (especially “mass redeeming” when market goes down) affect the MF returns?

First of all, rapid fall in the market is generally what leads to mass redemption in which case most if not all MFs will want to sell a lot to a) provide for redemptions and b) since most of the MF managers are under a tremendous peer pressure (for example AMC1 wants to measure itself against AMC2 on almost a day to day basis) - they generally have the tendency of acting in a herd mentality.

So even if one has tremendous faith in MF manager, one can see a lot of selling induced by redemptions. Now when a lot of stocks are sold two more bad things happen a) small and mid caps liquidity vanishes particularly for large sellers like MFs and as such the impact on price realised is disproportionately negative which hurts the redeeming shareholders and/or b) the overall portfolio weightage itself may change for existing investors as well because of point a) - as fund manager would rather sell low impact cost large caps like Infosys much more than a high impact cost small/mid cap like Kajaria - this may tilt the portfolio further towards a more risky small and mid caps in a falling environment.

Also high temporary fall in NAV may induce some ‘fence sitting existing investors’ to sell.

Basically in a rapid fall of market type scenario, my 2 cents is that only fund managers who are able to practise the art of value investing (buying stocks which are getting cheaper by investing the cash in the portfolio which was already not invested because markets were high earlier) and resist selling - would create value for investors - both existing and new. And such a practice is very difficult for most fund managers in MF becuase of peer to peer comparison which happens almost on a daily basis in the industry. Only absolute return minded investor would do well but if you read interviews and see cash positions of MFs, you will find that most of them are relative return minded and hence wouldn’t dither at all to sell and not buy in a falling environment.

12 Likes

does anyone have idea why SEBI website not showing recent month fund mgr performance

http://www.sebi.gov.in/sebiweb/other/OtherAction.do?doPmr=yes

Hi prudent equity is good. I heard stockaxis is also ok.

Hi Sarvesh, I was going through this thread and read your comments. Being an Investor in PMS for few years now, couldn’t help but to add to what you have said. In the last 5-7 years, the quality of disclosures have gone up substantially and its’ not difficult to get the relevant information if one knows what he is looking for.

I though this will help the forum members.

Since PMS is lightly regulated, it is possible to create a portfolio highly different from benchmark and hence deliver an alpha far superior to a MF. However this is a theory, it cuts both ways. A great/very good equity fund manager can hence deliver a much higher return in a PMS set up compared to when the same fund manager operates in an MF setup because his hands are tied up much less. For instance, an MF will normally have 30-40 stocks in a portfolio while it is not uncommon for PMS to just have 15-20 stocks in the portfolio. However, at the same time, an average/poor quality equity fund manager will produce returns much lesser than an MF guy as he will concentrate and towards small caps in general - where mistakes can be far more costly.

Why do you say that PMS are lightly regulated. Are they? As I understand they need to take SEBI’s permission to launch a scheme, appoint a custodian to overlook affairs, get their affairs audited and reported to clients at the end of every year. They even share the purchase price and selling price with respect to their holding unlike MFs. I would think PMS are much more transparent vis a vis MFs.

You made a good point about a good manager and an average manager and that I think is the crux of the matter. The performance is less to do with large caps/midcaps, diversified or concentrated but the longevity of the investment philosophy and discipline of the fund manager to implement, over a reasonable period of time. There are fantastic managers who have done well in MF space with a concentrated portfolio (Motilal Oswal Most Focused 35 Multicap Fund) as well as a diversified portfolio (Mirae Asset Emerging Bluechip Fund). Similarly there are PMS with diversified portfolio (30-35 stocks) and concentrated portfolio (15-20 stocks) doing well. Its more to do with philosophy, discipline and a good match of investor’s expectation with offering of the vehicle (MF/PMS). Most of the times, fund managers do well over the life of the fund but investors don’t because they end up taking unnecessary actions in between the journey basis their temperament.

At the same time, the performance data for a MF is much more reliable than a PMS (as explained in my post above)

I also read your earlier thread on performance data of MF vs PMS. There seems to be some misunderstanding at your end.

I quote you ‘So let’s say the first client was added to PMS when the NIFTY was 6000. Soon enough market rises to 9000 and 10 more clients were added to that levels. In this case assuming the PMS bought the entire NIFTY, it will show its performance as 50% since inception, even though 10 out of 11 clients will be at 0% returns. Now let’s say market falls to 8000. In this case, PMS will show its performance as 33% even though 10 out of 11 clients will be sitting at a loss of 11%. This is the single biggest anomaly of PMS firms and the same applies to investment advisory firms. Most investors don’t realise that proper investment management performance assessment can only be done if its a pooled vehicle and not a non-pooled vehicle.’

To be fair, most of the PMS, report consolidated numbers to their clients/prospects exactly the way MF reports. As Yogesh mentioned, in TWRR format. The performance is not singled out and represents all the clients PMS Co manages. So, it’s quite easy to compare MFs vs PMS performance over any short/medium/long term one wishes to. It’s apple to apple.

In general, PMS are oriented much more towards small caps, because most investors have exposure to large caps through MF already. This means in rising markets, like what we witnessed in the last 3-4 years you will see PMS firms outperforming MF and vice-versa. This is because small caps tend to outperform general market in a rising market situation and vice-versa. However, please note that a small minority of PMS fund managers will outperform in all conditions just like Warren Buffett - these are the really talented and risk-averse managers with the right incentives.

To give you a fact here, two largest PMS schemes of the industry (ASK and Motilal) run diversified portfolio and have a good long term track record. Like you said, we have seen quite a few new PMS managers emerging post the last bear run in 2009 focusing on small cap space. While they are good, the returns have been further enhanced by the run of the index. It will be good to track them over a business cycle and see how they fare to make a fair judgment. If small caps do well in a rising market, one can always participate through mutual funds, if one wishes. DSP Micro Cap, SBI Small & Midcap, Reliance Small cap and Mirae EBF have done very well over last 5 years.

So what should investors look for in a PMS manager. Well I would look at few things - a) risk averse mindset - this can be checked by calculating the weighted average portfolio price to book and price to earnings and comparing it to the normal market. This can be especially helpful since it is difficult for an investor to figure our individual stock proxy but the overall valuation of the portfolio will give some sense of how it will perform in falling markets. Lower the better. b) alignment of interest - where has the manager invested his own money, how much money he makes as a fixed salary, how much is the fixed part of the fees and how much is profit share. Higher the profit share and lower the fixed fees and salary, the better. c) how much of the PMS manager own money is invested in the funds being manager. What is his % of networth d) Pedigree - does he come from the high pedigree and can he do his own independent valuation rather than relying on already compromised sell side research. Can he do some primary research and figure out the truth hidden behind the numbers. and e) Size - what is the size of money he is managing - higher the size lower the returns, most PMS firms become or will become victim of their own size as their performance will not be replicable once they are well known in the market and have a lot of funds to invest - particularly at the top of cycle.

This is a pertinent question and should be explored further. To start with, it would be good to match the manager’s philosophy with yours. If you are P/B, P/E, BV driven investor, you will not be able to appreciate a manager who is growth focused. For eg, most of the leading managers have been holding Bajaj finance, Page Ind, Eicher Motors, HDFC Bank, Gruh Finance etc. Which may not fit into the typical ‘value’ filter but have worked for growth focused managers. So a good match will help in maintaining conviction during tough times.

To know a manager’s salary and how much has he invested in the scheme is a little tall ask as such information are not available. It may not be relevant as well. Though it is definitely comforting to know. Performance during bull and bear run is definitely helpful. Most of the managers now offer fixed as well variable fee structure and as investor, you can choose what you are comfortable with. If I am convinced about the manager, I will always choose a fixed fee structure. Why share more

On your comment about the size. While I largely agree, this is yet to be proven convincingly. Also, with increase in India’s market capitalization, this is a moving number. A 5000 Cr scheme could be considered big in 2007 not any more. Few examples of schemes with large corpus doing well – HDFC Top 200, HDFC Midcap Opportunities Fund, ICICI Pru Discovery, ASK IEP PMS and…

‘most PMS firms become or will become victim of their own size as their performance will not be replicable once they are well known in the market and have a lot of funds to invest - particularly at the top of cycle’ – This will equally apply to MFs as well, isnt it?

3 Likes

Hi Sumit,

Good points. Let me explain to you my thoughts on these.

True for active investors in PMS schemes like you who have both time, inclination as well as an understanding of financial matters (such investors in PMS schemes constitute <10% of PMS investors) as well but not true for most others who either have no time or no understanding of financial matters ( this category constitutes 90% of the PMS investors). Overall most investors are too unsophisticated to understand, ask or being able to decide in the right way - unfortunately, this is as true for most large HNIs as it is for retail investors.

MFs deal with retail money - so the obligation and regulation increases a lot. For instance, when shit hits the fan (relevant for debt funds), MF asset management company in India is informally obligated by SEBI to pay the investors or get sold out (if it doesnt want to do that), there is no such requirement for PMS funds. I think SEBI now wants MF guys to even disclose the salaries of MF managers. So, I was talking about regulation in a relative sense where MF is more regulated than PMS. For instance, PMS guys can do whatever they want like have a 6 stock portfolio which no MF scheme can afford.

Well, this is a bit technical and I can explain to you some of the ill practices offline as I am an insider on this knowledge. In any case, because PMS is a non-pooled vehicle, striving for consistent performance reporting, in my view, goes against the interests of the client. The reason is what I have explained earlier in my below mentioned quote.

Being growth focused is fine but growth at any value is a strategy which will underperform the value strategy in the long term in terms of absolute returns and will massively underperform if you consider the risk adjusted returns. Numerous studies done around the world with data for the long term have shown the same (for starters one should read about the famed NIFTY 50 stocks in the US in 1960s, Nifty Fifty - Wikipedia). The problem is that most of the fund managers forget the fact that Buffett says that he wants ‘great company at fair value’ - the important term is fair. Buffett, for instance, knows that Amazon is a great company (he admitted in this AGM) but is not buying it still while most of instituational guys are lapping it up even at current valuations. Not everybody but many such growth oriented MF and PMS managers are buying what I believe is without margin of safety. Even if they show returns, their actual risk adjusted returns are not good because alternative scenarios (major negative local or global events) have not played out although there was a chance of them playing out - which would have caused massive depression in the valuations of such companies, much more than a value strategy based on the sound principles of margin of safety. I would consider for instance buying Dmart at 100 times earnings equivalent to gambling and I think we all know who are the fund managers in both MF and PMS space who are buying it. It doesn’t matter even if Dmart does great from present levels just because a scenario where there could be a massive depression in share price didnt play well (Remember RK Damani himself partly sold out at 300 Rs while investors and many such growth investors are scrambling to buy at 800 bucks). I have given Dmart’s example just because you mentioned some extremely high priced stocks which many of these growth investors love to buy.

It is as relevant as knowing the Promoter’s shareholding in the company and the directional nature of the same. Best of the fund managers (and I guess none of them will stick to a Mutual fund or a non-owned PMS/hedge fund for long) are all majorly invested in their own schemes (eat their own cookies).

Exactly, but in the similar vein, if the manager is convinced of his own ability, then a) he will move out to a structure which is more based on profit sharing and b) he will start charging a profit share. The only scenarios where he wouldn’t quit is a) he himself is not sure of his abilities and b) he cant match his fixed salary because his AUM is too large in which case his primary motive would be to increase or atleast maintain AUM than show returns.

Since I have managed these things myself, market cap is just one the factors for fund managers; volatility, liquidity and impact cost are equally important. A stock like Repco for instance is a nightmare for most of the fund managers because of liquidity and impact cost even though market cap may be decent. Overall liquidity situation for most stocks beyond Top 200 remains very weak in India and not amenable to large sized funds.

6 Likes

I was reading a book by an acclaimed investor and found something which accurately describes my position on performance of many MFs/PMS firms. As quoted verbatim from the book below - words of wisdom:

"I dismissed an investment in mutual funds quite quickly

because I was familiar with findings that the vast majority of mutual

funds underperformed the market indices on an after-fee basis. I

also became aware of the oft-neglected but crucial fact that investors

tended to add capital to funds after a period of good performance

and withdraw capital after a period of bad performance.

This caused investors ’ actual results to lag signifi cantly behind the

funds ’ reported results. Fund prospectuses show time-weighted

returns, but investors in those funds reap the typically lower

capital-weighted returns. A classic example of this phenomenon is

the Munder NetNet Fund, an Internet fund that lost investors billions of dollars from 1997 through 2002. Despite the losses, the fund

reported a positive compounded annual return of 2.15 percent for

the period. The reason? The fund managed little money when it

was doing well in the late 1990s. Then, just as billions in new capital

poured in, the fund embarked on a debilitating three-year losing

**streak."

1 Like

there are good no of PMS available in market to invest from , it is imp to choose wisely where your thought process matches the fund thoughts. can help you if any advise is sorted , mail query on mail query on djrish@gmail.com

I had a question on regulatory requirements PMS have. I am aware that they need to report performance and that it’s available for us to see on SEBI website. Do they publish their holdings somewhere ? MF’s do that but not sure about PMS.

Is anyone aware?

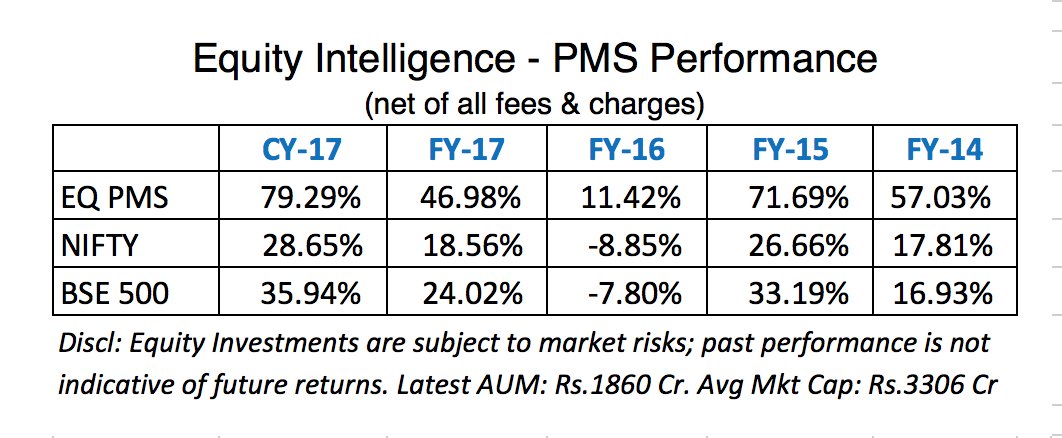

Porinju’s PMS has given 79% returns this year. Unheard of so far to me in India.

Any idea about other PMS returns?

1 Like

Maruti gave 83% returns for CY17 and HDFC Bank 55%. Is it worth going for these PMS funds esp those that take exposure in unknown companies. The risk reward ratio in these companies does not seem to be favourable. Moreover, this PMS return is gross return and the performance fees is yet to be deducted…that will reduce the CY17 return of the PMS to be less than reported. The MARUTI’s of the world are the best!

1 Like

Hi Yatharth,

Thanks for this data. When I look at this data, I can’t help but comment because I somehow find too many gullible investors fall for statistics at exactly the wrong time. So, for the benefit of all, I want to lay down few points.

- Compounded Annual Returns is something not intutive to human mind.

For instance if I ask you what will be your net retuns per year in 5 years if your performance is like this : +40%, +40%, +40%, +40%, -50%. Most likely it wouldn’t seem to us that performance CAGR drops to a mere 14%. However someone who does +20%, +20%, +20%, +20%, 0% achieves 16% - a seemingly small but important 2% point difference. And much better even after achieving just half of the returns shown by the first guy in 4 out of 5 years as he manages to save the investors by not becoming all go-go investor in the bull market. Still if this 2% difference per year doesnt excite you, assuming you are a PMS investor at the age of 40 and you are working somewhere else and want a comfortable retirement - this difference of 2% per year will create a differnce of 50% difference in wealth when you retire at the age of 60 - this will give you a different standard of living all together as 50% difference will all fall in your discretionary expenditure - very important for the standard of life in retirement.

So bottomline of first point is - Compounding of wealth is magical but making money isn’t as important as retaining it is. It is very important to not have massively down years and the thoughtful portfolio manager’s portfolio is tilted towards this consideration. So avoid risk but more so when markets are appearing expensive.

- There are three kinds of lies - Lies, Damned Lies and Statistics

Now this is interesting. Why would a manager who famously invests mostly in micro-caps and at best small caps compare his performance to NIFTY and BSE500 rather than a index like BSE Small Cap (which by the way is also not representative for many of the micro and small caps bets). Less than 15% of BSE 500 companies have market cap less than 3000 cr and again is not representative to bets. A 79% looks massive compared to 28% of NIFTY but not so great when BSE Small cap index which is an index of more than 700 companies is itself up by 60% in CY17. The answer is simple : because the Alpha of returns comparing it to BSE500 or NIFTY looks much more great. I bet many such managers start comparing themselves to BSE Small cap index in a bad years - as BSE Small cap will get massacred in a down market and it will again make the underperformance look better relatively speaking.

- The concept of Risk Adjusted Returns

Unfortunately, most of us are inclined to look at returns only as they are far more objective but not look at risk adjusted returns. Classic Corporate Finance theory tells us that returns can always be expected to go higher if risks are. While I believe that there are a set of distinctive portfolio managers who will beat this equation and show that market anomalies exist so that returns can be increased without taking excessive risk but then not everybody belongs to this elite set (and I bet any manager who is regular on twitter and CNBC don’t belong to this elite group either). Now this was a year when taking massive risk led to massive performance. Forget BSE Small Cap Index which is up 60% or this Portfolio which is up 79%, BSE Realty which maybe consists of most volatile and low quality company is almost up 100%. Taking higher risk is like driving fast - you may reach early sometimes (like managers who took higher risk this year) but sometimes you will just crash. Unfortuanately we feel pity for the guy who died and we hail the guy who came first - while we should pity both. Shouldn’t we?

This is what two of the world’s best investors - Buffett & Seth Klarman say about performance to their investors:

“I have pointed out that any superior record which we might accomplish should not be expected to be evident by a relatively constant advantage in performance compared to average. Rather it is likely that if such an advantage is achieved, it will be through better-than-average performance in stable or declining markets and average, or perhaps even poorer-than-average performance in rising markets” Warren Buffett, Partnership letter 1960

“The true investment challenge is to perform well in difficult times. It is unfortunately not possible to reliably predict when those times might be. The cost of performing well in bad times can be relative underperformace in good times. We have always judged that a worthwhile price to pay” Seth Klarman

Bottomline is the go-go managers who outperform the index in a year like this should be evaluated cautiously. Best of the managers will probably underperform as the bullish market stays strong as they get more and more risk averse before the market actually tops out. Hence they are psychologically prepared to take full advantage of bearish markets since they dont loose much and actually have cash to invest as well. As opposed to that, go-go managers get wiped out massively both psychologically and performance wise.

“A market downturn is the true test of an investment philosophy” Seth Klarman

- So if performance data is not useful, then what is useful. While performance data in ultra bullish years like this one is not useful (even a chimpanzee throwing darts can get great returns in a bull year like the one we had, BSE Small Cap index itself is up 60% in CY17), performance data in down years is very useful. Very important is the fee structure - now tell me wouldn’t a portfolio manager like the one above better off is he just charged profit share - if the manager is confident about performance across cycles which one can be only if one is a bit risk averse - they will mostly charge through profit share rather than the other way around. What should we learn about some of such managers propensity to still charge a hefty fixed fee while knowing very well that they could have earned much more if they charged only profit share - are they smart or are we dumb? Very important is why the manager is investing on the stocks he is investing - is it hopeful investing, does that carry margin of safety in terms of valuations, how does portfolio valuation metrics compare to market benchmarks etc.

Unfortunately, too many investors remain focused on just the return metrics that too in the bull market. They get swayed into investing with the go-go managers at precisely the top of the cycle and then when burnt badly exit at the bottom with heavy losses, promising to never return again. Soon after a new bull cycle begins which brings in a new wave of fresh gung-ho investors as well as a new crop of managers who take highest amount of risk and show mouth watering returns and the cycle continues.

One data point I read recently was particularly sobering, as well all know 75% of the fund managers in the USA (including private equity, hedge fund and mutual funds) over the long term fail to beat the benchmark. Many people did the research recently and found that a majority of investors actually underperform these fund performance itself which are anyways underperforming the benchmark - due to a dangerous cocktail of bad skill of managers and bad timing of investors.

So when we read such startling returns we should all remember Buffett who said - be greedy when others are fearful and be fearful when others are greedy. What goes up very quickly comes down equally fast as well. Always remember that risk and returns almost always (not always though - this is the space where best of the managers play) are correlated. And remember that driving fast will make you reach your destination earlier 9 out of 10 times but would you rather do that and die in that one scenario. Or would you prefer to reach destination maybe slightly slowly but surely.

With these thoughts, I wish you all a very happy and also safe (given where we are in terms of valuations) new year.

Cheers,

Sarvesh Gupta

80 Likes

A great perspective. We usually get carried away with Statistics without understanding meat of the matter. As rightly said in post, time is ripe for many to fall in trap with such numbers. What is achieved by Porinju is commandable, but need to read it with both eyes open to understand the context beyond plain conveniently tabulated numbers.

Excellent post. Sincerely appreciate your going to great lengths to differentiate between returns and sound investing philosophy based on risk adjusted returns.

I wanted to explore the thoughts of other investors here and hence quoted Porinju.

Porinju and a couple of others have shared their returns on twitter. Personally, I find difficult to invest in small caps, having seen earlier performance and management quality in many of these.

This year, after 2014, has been exceptional. Any good portfolio, with discipline could have given similar or better results. I am sure that several, if not most on VP, may have got that.

A stable PF of 6-7 quality large caps consisting of good Private Banks, NBFCs, Auto, Auto Ancillaries, Consumer companies; have even performed better this year.

Once again, thanks.

Very Nice post Sarvesh.Write more often.

Very well explained Sarvesh…

no data available on stocks they are holding

monthly reports available on sebi website depicting aum and no of client etc but nothing material to return.

can ask for disclosure documents to PMS for checking any gray areas of management and get proper data as this is the same as submitted to SEBI

some pms give model portfolio returns and not weighted avg returns of all clients so be careful. also some give returns net of fees and exps while some do not so while comparing be careful.

if any questions unanswered pl email on djrish@gmail.com

I have invested in Motilal IOP, Motialal NTOP and ASK-India Select

I have also invested in mutual funds.

With all due respect to @8sarveshg and other veterans, the biggest plus point of PMS over Mutual Fund is the consistency of returns. A 5 star rated mutual fund you invest in today could become 3 stars down the line in 2 years (case in point DSP Black Rock Micro Cap)

With PMS there is more “faith” as the portfolio is managed by seasoned professionals and unlike mutual funds, the managers do not change that often. Gives you more credence to hold your portfolio during turbulence times.

Again, nothing could beat direct equity investing provided you have the time. Also, the choice between Mutual Fund, PMS, and Direct Equity also boils down to individual investment styles and risk appetites.

1 Like