After IL&FS crisis and increased potential of defaulter of real estate developers due to liquidity crisis, what the risk PEL carrying? Piramal had landed aggressively to real estate developers before the crisis.

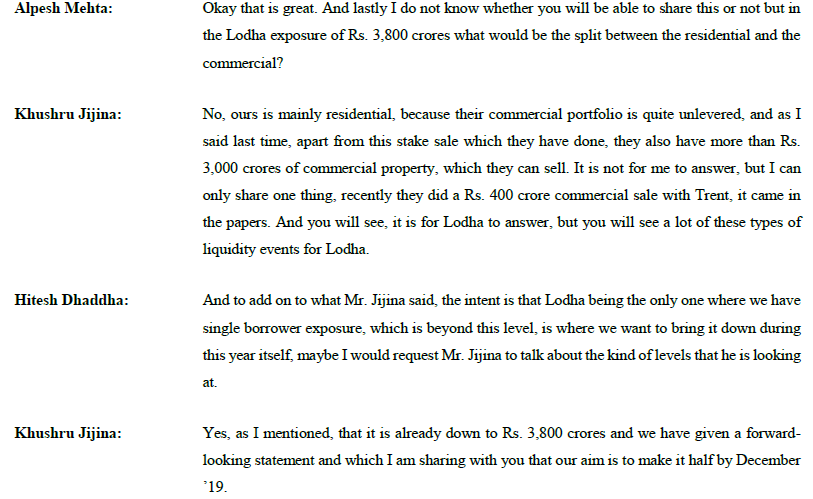

Current Lodha exposure is Rs 3,800 Cr and plan is to bring it below Rs 2,000 Cr by Dec 2019 as per recent concall

Lodha’s Palava project too has same complaints from the buyers there - that they are not allowed to visit the actual site citing “safety” considerations by the company.

This was even after the company delayed posession of the flats to buyers.

A friend of mine who worked at Lodha’s customer service call centre for a short period too didnt have much good words about them.

Having said the above, PEL has planned to reduce is exposure to Lodha and the above complaints of Lodha are not of the nature that cannot be rectified if the company wishes to do so. May be until today, they have been able to find buyers inspite of such lethargic and inconsiderate attitude towards the buyers and hence they never felt the push to improve their ways of doing the buisness.

Krishnaraj Raos channel on Lodha has created quite a stir and there are thousands who support him and the cause he is fighting for.

The channel is :- https://www.youtube.com/user/krishkkphoto/videos

This is customer agitation at a different level and highights the the risks that developers face i.e the risk of a class action suit. Class action suits are an important category of risks.

More power to Mr Rao

Best

Bheeshma

Just Curious…

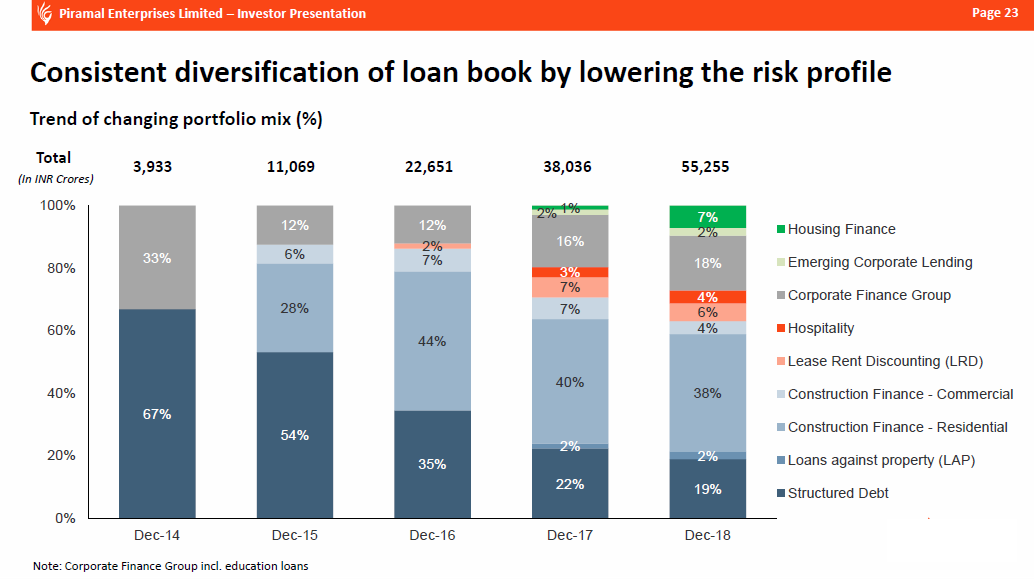

PEL has become a proxy bet on real estate sector in India.

Because of structural changes brought by GST/ RERA/ Social Media/ NBFC Crisis, a consolidation appears imminent in real estate sector.

In case of consolidation, non leveraged realtors with good brands are more likely to survive than others.

PEL has better returns as it lends to more risky group and thereby is able to charge premium. However, in case of consolidation, those surviving may not be open to premium thereby decreasing demand for such lending.

In that case, isnt it better to bet on good quality real estate players directly rather than betting on a firm lending to risky players ?

Regret if it seems a foolish hypothesis…

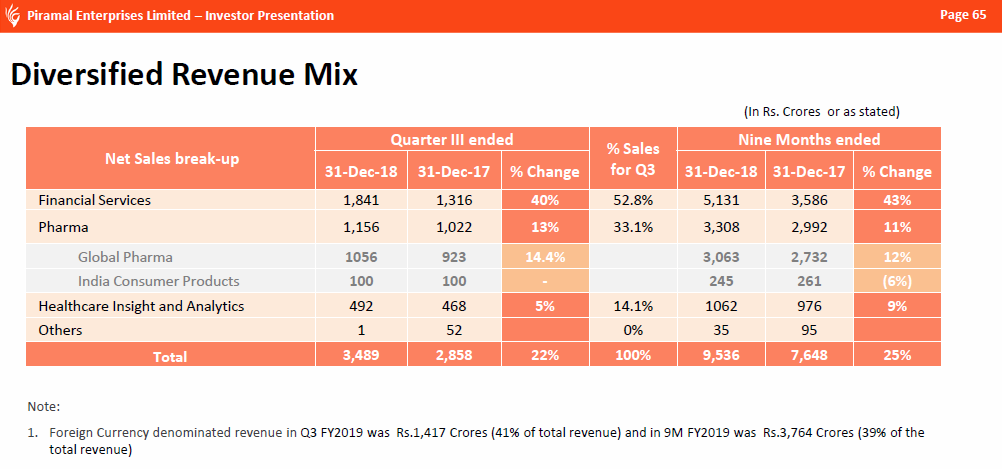

Around 36% of the total revenue of Piramal comes from real estate financing. See below

54% of revenue from financial services

66% of the financial services revenue from real estate sector as can be seen from above graph…

So I am not sure about the comment made above…

In my opinion, real estate financing is one of the major revenue (and profit )generator for Piramal but Piramal has many more business verticals than just real estate…

Piramal is a bet on both financial services and pharma.

The focus has been much on the financial services due to recent liquidity crisis but pharma is still a major share of their business and they are not totally pivoting away from it.

There are several greenshots which seem to be appearing in indian pharma and also in Piramal (Lift of ban on Saridon,introduction of new drugs in US market).

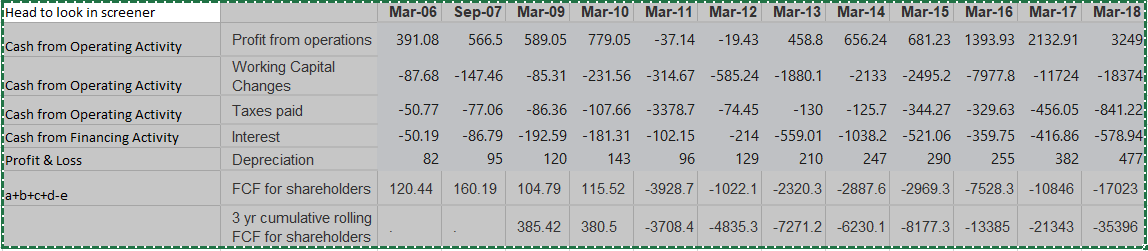

Free Cashflows will never be there for a finance company. Check any, even HDFC, HDFC Bank or Kotak.

Logically also, there can be no free cash flows as I take debt and lend money. Both are my operating activities. In case I earn more money / interest payments, I lend it to people and do not hold it in my balance sheet.

Disc: Tracking Position

#Piramal, Baring PE in talks to acquire majority stake in DHFL

In a move that may see change in ownership and management control at the troubled housing finance company DHFL, two sources close to the development have confirmed that Piramal Group and Baring Private Equity are in advanced stage of negotiations to acquire majority shareholding in DHFL.

Earlier this month, DHFL chairman and MD, Kapil Wadhawan had said that the company has engaged with large potential entities to identify and on-board the right strategic partner and are in advanced stages of discussions to achieve the same over the next 90 days.

Sources, however, confirmed that currently discussions with Piramal Group and Baring Private Equity are at advanced stage of negotiation and it is not just for entry as strategic partner.

“It may not be limited as a strategic partner but the talks are on for change of ownership,” said the source.

I dont know how it is beneficial for PEL shareholders if the deal goes through…will the dhfl be merged with pel? any senior boarders can throw some light on the nature of this deal…even though it is still speculative at the moment

It is speculative at this time. My guess is Piramal Capital or HF would be merged to DHFL and renamed. This way these entities will get listed which the management has indicated would pursue in medium term.

For PEL - DHFL has a lot of businesses, better idea would be to buy just the Housing finance business which PEL is trying to build. Considering the current share price of DHFL, PEL can buy assets at quite a low price.

For DHFL - any strategic tie-up with PEL will immediately reduce the liquidity concerns and the business should come back to normal.

Disclosure: Invested

DHFL is still a strong brand outside of the stock market. With PEL on board, DHFL reputation will be saved and PEL gets a ready HFC infra in place which has been making good profits.

This seems like a win win situation for both DHFL and PEL and minority investors of DHFL.

Is this the same PEL which previously mentioned that they are not interested in inorganic growth as they are not comfortable with the lending standards of other entities and boasted about how high their valuation and lending standards are. I would understand buying someone like Gruh, but Dewan looks very risky considering the type of news we have been getting lately. PEL already was a very risky stock considering most of their lending were to the most risky construction finance rather than housing loans. The purchase of Dewan will only increase this risk further.

Even when the talks are with bain Capital…Market seems to assume that PEL is behind every other deal that Bain is in talks…few days back it was DHFL and now Wockhardt