Vivek,

The First Video in link shared by David on Piramal Financial Services day

Vivek,

The First Video in link shared by David on Piramal Financial Services day

Yes, he has pointed risks of liquidity and PEL is in good position since they already did CCD debentures, QIP at approximate price Rs2600, which will be converted in a year if we discount To that price buying at CMP 2400 seems a good deal. But I really don’t have the clear EPS history to understand the risk in investing now.

Interesting development for Shriram Group and hence, PEL. Needs to be seen at what valuations will PEL exit (if at all). Else, what’s the total worth (valuation) of the overall investment in Shriram group (post merger).

Dont go by the video label. Here Piramal speaks about NBFC situation and PEL’s financial arm(s).

This holier than thou attitude is unwarranted. Let’s be clear our Indian market doesn’t have availability 10-15 yr capital at affordable rates. Mismatches are bound to happen. Even if someone has long term capital at certain rate nobody will raise long term capital at fixed rate as we are a country of volatile rates and economic cycles. This cash flow mismatches will happen in future too and nobody can forecast it. It is also wrong to give blanket statement that low promoter holding is a sign of bad governance.

Honestly, I wouldnt be worried about Piramal Enterprises until Ajay Piramal is at the helm. One should buy this stock on declines.

[From Recent Interview of Mr Ajay Piramal ]

Contrary to the broader perception about the current Debt crisis, where’s many experts believe NIM compression for NBFC sector per se, Ajay Piramal is hinting at NIM expansion at PEL (time around 10:40 in the video).

Earlier there would be competition for the projects. PEL would do a lot of due diligence and offer developer rate and size for the project. When the other NBFC would then know that PEL has done the homework, they would provide a lower rate to the developer, thus taking a customer away from PEL.

Now, this will disappear, and the current crisis would allow PEL to charge higher interests. This will help them in NIM expansion.

I am not sure if this will be next quarter or over the next few quarters.

I think this is a bit too much. Am pretty sure other competing companies can do their own valuation and provide a competitive interest rate. It is not like only Piramal can accurately value a project like it is some kind of a moat. Besides it is very common for competitors to attractively price their product to win clients which Piramal is free to do as well.

Even Edelweiss is also claiming for NIM expansion after this debt crisis…refer recent clarification published on exchanges

Hi can you please share the interview link.

I need help getting some context on what Mr. Khushru Jijina said in his presentation on the Piramal Financial Services Day.

Here is the link: https://www.youtube.com/watch?v=EzkxplwfysE at 54.5 minutes.

He says that their NBFC is the only one who has a nuclear button, that will stop the customer from defaulting on Piramal.

Anyone who understand this statement and can provide more context on this, please do share.

Is he signalling that Piramal has first charge on the prized assets on the developer?

Thanks in advance.

“Nuclear Button” which Mr.Khusru Janna is referring to is that they can take over projects as they have a sister concern which is a real estate developer (so they do understand the business very well) so while sanctioning and disbursing the loan if they are able to maintain security cover and if their is a default then with the help of their realty arm they can take over the project and ensure that the loan gets repaid (ability to complete incomplete project as well as ensure sale of inventory)

Best way of looking at Financial Services of Piramal Enterprises is Loss Given Default (LGD) if while sanctioning loan and disbursing loan they take care of security cover (1.5x to 2.0x) even if their is a default, Piramal Enterprises would be able to take over the project and ensure that project gets completed and even if they sell at a discount (20 to 30%) they would still be able to recover the loan amount. (Most NBFC don’t have completion ability which prevents them from taking over projects mid way)

For Example - assuming worse case situation 40% of the loan book goes bad (Rs.40 goes bad) they still would have Rs.60 of security cover (1.5x) which in worse case can be sold at Rs.46 which means no loss to Piramal. They can sell upto 40% discount without much loss.

Thought it is old report, it is good to read it again -

Thanks for sharing.

If housing sales has de-grown by 8% CAGR between CY14 and CY17, what exactly have HFCs been funding that their share prices have gone up anywhere between 5x-10x during this time?

That’s a lot of inventory buildup i have been hearing about for a long time now. If it is hard for retail business to sit on inventory without being frowned upon, how have the developers been able to sit on their expensive inventory for this many years without a meaningful correction in prices (going by rental yields here)? Are these loans disbursed by HFCs merely propping up the sector by enabling the developers to hold their inventory longer?

The ambit report is pretty negative on Piramal Enterprises/Piramal Capital for running huge ALM mismatches and for having risker real-estate developer loan book and for having longer-tenure loans. I have found the idolising of Mr.Piramal in this thread borderline scary.

I have updated me comments with video and time in the original post.

There was, is and will always be a demand for idols. And, as Graham (my idol ![]() ) said, “…the demand being there, it must be supplied”.

) said, “…the demand being there, it must be supplied”.

PEL has the most ALM mismatch and so it was important to come out quick and aver with the greatest of confidence that things are fine. Because if you don’t market will get the better of you, and Mr Piramal knows that very very well!

I think there are 2 important things which Ambit report clearly misses out:

Further I would like to add one more thing here a general gyaan about real estate sales being slow is missing the real picture - the smaller developers are destroyed by demonetisation and RERA but the top 10 developers in each city (which is the focus of PEL) are gaining market share - you can just plot the unit sales & collection figures of the top listed developers and you would get a true picture, PEL is focusing on these developers and not on Real Estate market.

Yes, Real Estate lending has inherent Risks and we should monitor the book for defaults (my earlier answer about how having a sister concern with real estate development capability is a big advantage for PEL and allows them to take over projects in case they see default) but I feel PEL is moving towards lower risk book - they are diversifying the book and reducing the risk across the portfolio - from initial promoter funding which is the riskiest form of Real Estate lending they have now gone ahead and started home loans, LRD Loans, Hotel Funding etc

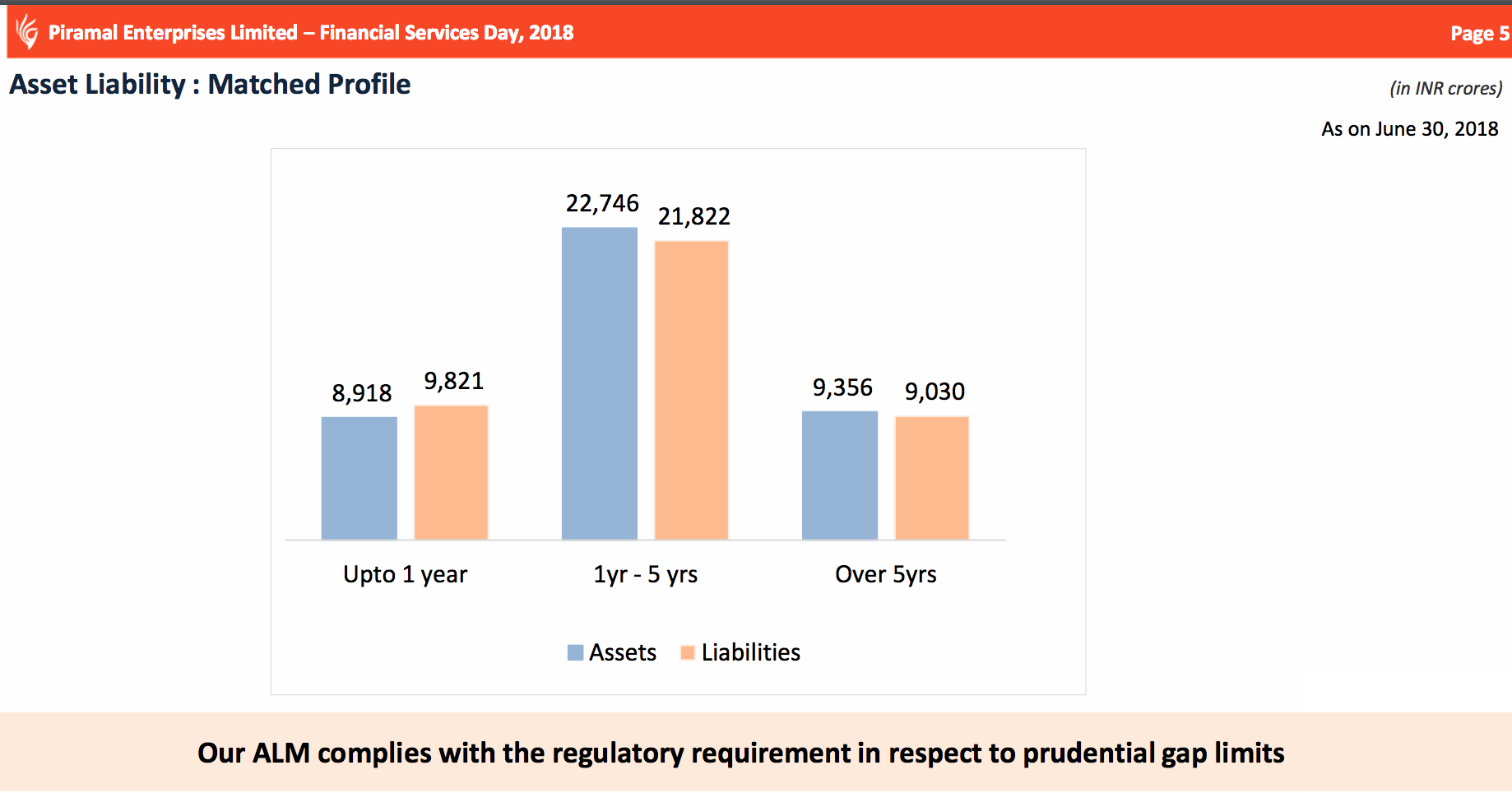

Following presentation clearly gives all the information related to ALM. Now the question is do we believe Ambit (how old is Ambit report?) or PEL(This report was on Aug 30th) …http://www.piramal.com/assets/pdf/fs-day/PEL-FS-Day2018-Treasury.pdf.

Mr Piramal is very very smart and very practical, based on track record. So it is highly sensible to assume they have ALM fully under control (as the subsequent chart shows), if that’s the point under debate.

And PEL can raise funds from the market faster than a snap of fingers.

Markets are like girl friends when you really need them they are not available

Hence, when you need money you would not get it or you would get it a high cost. So when market is giving you money you should take it and then figure out the uses (I know its counter intuitive but that is the best strategy and endorsed by Mr.Deepak Parikh).

Mr.Piramal being a smart promoter knows this and has cleverly raised Equity earlier in the year when he could - now he can easily ride out the small storm.

The CP market was being used by NBFC as short term funding was cheaper (50 bps difference over long term funding) and Mutual Funds were rolling it over at maturity (typical AML mismatch). NBFC promoters now realise this is not a reliable source of funding and would make requisite arrangements (Undrawn bank lines, Medium Term NCDs, Tier 2 bonds etc.) This would increase the cost of funding for NBFC by 50 to 100 bps and this would impact profitability in the short run while in the medium term they should be able to pass on this increased cost to end customer but one thing is for sure the high 25 to 30% growth rate we used to assume in NBFC has to be tempered - the growth would now be more sensible 15 to 20% growth with same or slightly lower profitability in short term and higher profitability in long run.

Leverage levels also would get moderated (no more the model of 10x leverage levels) so you would have moderate growth funded by either more equity raise or Tier 2 bonds or growth only with profits being ploughed back.

P.S. in the long run for India to grow at 6 to 7% we would need quality NBFCs and they would grow at 15 to 20% growth rate which is still very good with ROEs of 15+% (This can still give you an 10x in 10 years - as shown by Coffee Can Portfolio of Ambit - good Financial Institutions growing revenue at 15 to 20% at ROE of 15+% should give excellent returns at any time you buy them and we are getting them at a discount).