PEL to sell it’s arm Piramal Imaging to Alliance Medical Acquisitionco.

How will this sale proceeding reflect in revenue? will it be a one off other income? will it be eps Accretive ?

good decision. it was a loss making business. the molecule development business did not pay off for Piramal and was shut down. accumulated losses from the imaging business would help offset profits from finance and pharma businesses.

now awaiting disposal of the DRG business as well which is low margin and taking up precious management bandwidth.

disclosure: holding

2 Likes

Annual Report is Out

Observations on the Annual Report

Finance business

folding its lending businesses into the housing finance umbrella is expected to result in higher margins going ahead.

investments in Shriram group is taking time to pay off. value of investments have barely doubled in the last five years. We have to see how Piramal’s team is able to restructure the Shriram group of companies.

ROE of the finance business is expected to improve as the funds raised from the rights issue get deployed in the coming quarters.

Housing finance business is going to newer cities. Management is talking of very low NPAs in the housing businesses. We have to keep an eye on this.

pharma business

A few steps closer to the pharma business being demerged from the finance business.

EBITDA margins in the pharma business is scaling up. From 14 per cent CAGR in 2013 it is now up 22 per cent. in organic growth in the sector is continuing.

Desflurane is expected to be launched in the current FY which will add to both top and bottomline.

Within the pharma business, special focus seems to be on the consumer products portfolio. IMHO this will need to be watched out for in the coming years. PEL says it aims to be among the top three OTC companies by 2020.

Last year it faced some problems due to GST which seems to be behind the company.

Revenue is growing at a CAGR of 18 per cent. but operating efficiencies are expected to add majorly to bottom line going forward.

No compete clause with Abott is expected to end soon, so expect PEL to enter some segments.

Information Analytics business

this business is a slow grower which Ajay Piramal had gotten into after the Abott deal. While the finance and pharma business have scaled up, the DRG business has not. Could be Ajay Piramal is waiting to sell this since this seems to be dragging down PEL’s ROE.

Any sale of DRG will be a big booster for PEL.

disclosure:holding

shiv kumar

11 Likes

Product innovations continues

Piramals Corporate Finance Group has financed

-

Renewable energy companies which has been struggling with low power tariffs in the last year

-

Sterlite group which is faced with closure of copper plant in Tamil Nadu and closure of mining activity in Goa

-

Other companies with sub premium credit rating such as RSB moulds, Indo shell moulds, Apollo Logisolutions, Smaaash Investments, NCL industries, Sanghi Industries etc (A detailed search on google would yield even more results)

Most of these companies would have a credit rating below A. Coupled with the Real Estate lending (which is anyways a risky business to be in), significant component of Piramals loan book would fall in the risky category. I presume at least some of these loans would have a moratorium period at the start. Once the repayment due dates kick in, any adverse macro economic / industry vide or political even can cast doubts over recovery of principal lent.

At the moment, the investor presentations mention the negligible credit costs. But in my opinion, it is highly unlikely to have such low credit costs in the long term in such a business.

Therefore, Piramals Financing business remains a high risk and high reward business whose true

colours would only be revealed after 3-4 years.

Disclosure - Tracking with a small investment made in 2016.

8 Likes

NCL industries- has publicly committed to replace the Piramal loan. Check Q4 call. Already paid 50% of Piramal debt. Because of certain clause, not able to repay

3 Likes

1 Like

The revenue of DRG has degrown continuously for the last 3 years from 1,516cr in FY16 to 1,222cr in FY17 to 1,209cr in FY18. But there is hardly any analysis or explanation for this dismal performance in their annual report.

I’m an investor in PEL as well. But I have reduced my stake considerably and am thinking of exiting completely. One of the reasons is that as illustrated by the example of DRG there is seldom any frank and honest discussion of the issues or headwinds facing the company. The annual report and other communication from the company is like a marketing material prepared by the PR department focusing on only the positives. In my view, annual report should contain an honest discussion about the issues facing the company and any failures should be acknowledged.

14 Likes

Seems like you were reading my mind ![]() . DRG was / is by far the biggest acquisition in nominal amounts by Mr Piramal, who has a reputation for building via acquisitions. DRG was a non performer even before 2016. There has been little information or honest assessment, on failures. Worse, DRG continues to be touted as a wonderful business. At the time of acquisition I learned that DRG was pursued for many years before it was acquired. It has leverage in its books that is yet to be unwound (was supposed to be unwound from its earnings).

. DRG was / is by far the biggest acquisition in nominal amounts by Mr Piramal, who has a reputation for building via acquisitions. DRG was a non performer even before 2016. There has been little information or honest assessment, on failures. Worse, DRG continues to be touted as a wonderful business. At the time of acquisition I learned that DRG was pursued for many years before it was acquired. It has leverage in its books that is yet to be unwound (was supposed to be unwound from its earnings).

Some years back I heard that it was to be put on the block…and Piramal may want the best price for its sale. So makes it even more difficult to be honest about performance (the lack of it I mean). Keeping quiet about results, while keeping loud about activity is the next best alternative. Which is what’s being communicated. Just like its drug discovery foray, if you recall…the breakthrough was just around the corner, till one fine day it was called off…and the tax losses that can be set-off from all its sunk investments became the bright spot!

5 Likes

In India, I have observed that the annual report and other communications are seldom of any value to the shareholders. These are used as mouthpiece by the management to sing their own praises.

But because Mr. Piramal is touted by many value investors as the equivalent of Warren Buffett in India. Hence, the expectation from him is higher in terms of communication and disclosures. Which has been sorely lacking, unfortunately.

If you look at Warren Buffett’s record, he has been upfront about his mistakes. Whether it be his investments in the airline business or the Dexter shoe business. When the economics of the newspaper business (or the encyclopedia business or the textile business) began to change due to the disruption by the internet (in case of newspaper and encyclopedia and China in case of textile), he was frank and upfront about it in his communication with the shareholders. Even before the businesses deteriorated and the wider investing community became aware of the fissures, shareholders had been warned from WB himself.

Sadly, despite his reputation such honesty is not forthcoming from Mr. Piramal.

12 Likes

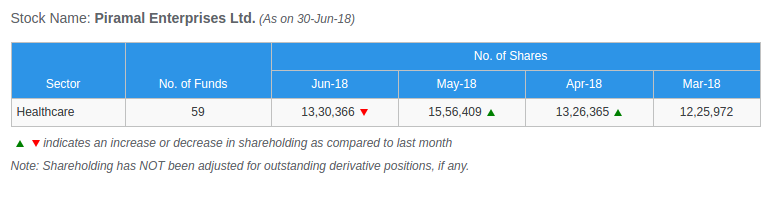

Mutual Fund holding of Piramal Enterprises Ltd has shown a decrease in the month of June’18

Source : https://www.rupeevest.com/Mutual-Fund-Holdings/100302

Yes Kashif, absolutely.

Yes, and I think you have captured it very well. Measured against this yardstick, Piramal falls way short. Buffett sits every year and takes questions for 6 hours without any knowledge of what will be asked. Piramal sent a defamation threat when an Intelligent but unfriendly reporter wrote a factually correct piece questioning certain transactions - a Buffett test to managers on measuring reputation.

On the other hand, I also find it inescapable to note that Ajay Piramal has built value and partnerships that are unique and unparalleled. (Disc.: I had also been a material investor & made satisfactory returns, sometime back)

It presents some kind of moral dilemma (one the one hand good, on the other, bad) and reminded me of the Rajat Gupta insider trading case. Bill Gates, Kofi Annan, Ambani and 1000s of others wrote saying Rajat is such a wonderful human being and has done so much good to humanity, in relation to the puny gains made by Rajat in the case. Judge Rakoff who pronounced Rajat guilty, brought blinding clarity to this “Friends of Rajat” moral logic by saying, “If Mother Teresa were here and charged with bank robbery, the jury would still have to determine whether or not she committed the robbery,”

In other words doing a lot of wonderful things to humanity, however large, does not give you a licence to commit wrong, however small.

19 Likes

Although I agree that Piramal has not been very open about his failed aquisitions(which gets sold eventually at loss), I think it would be unfair to compare him with the gold standard of stock market i.e. Warren Buffett. Forget about Indian companies, but globally very few would come any close to Buffett in terms on openness and transparency.

Coming to DRG, in perfect world I would love to have more information about this business vertical. But considering it contributes only 10% of the sales (and reducing every quarter due to high growth in Financial vertical) and hardly any contribution to the profitability, I am ready to ignore it. It is almost becoming a “side dish” . Hence as long as main dish is “sumptuous”, I can live with “bad side dish” as long as package is available at the “right price”(which I believe it is right now  ). This is my personal opinion and others have right to feel differently.

). This is my personal opinion and others have right to feel differently.

9 Likes

Does anyone know when is the ex dividend date for 25rs or will it be only know on AGM date?

1 Like

Piramal Consumer Product Division aims to make a big splash in the consumer products market and triple its current revenues to $10 billion by 2020. @bsindia https://t.co/5jkjYKAVs6

its 10 billion Rupees