- Pabrai on PEL at 7.50 2, Suggest hear from the beginning because the discussion is in the context of the combination of high certainty + low risk to give high returns, 3. A Delightful interview in entirety…… https://twitter.com/twitter/statuses/1002434266762915840

As per recent con call, PEL top sector in its landing portfolio is Renewable Energy sector. When we look into history, this sector doesn’t have more earnings potential but increased competition made it worst. What PEL landing model used to allocate highest debt to this sector?

1 Like

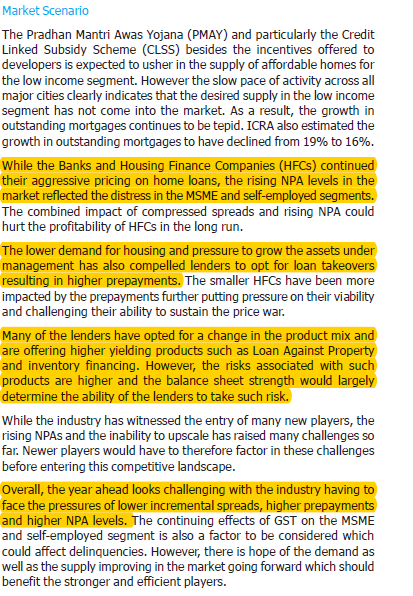

Expected market scenario in Housing Finance and Risk…from Annual report of Gruh Finance.

Days are not good as it were in past…increasing interest rate (higher cost of borrowing) and increase risk of NPA …could reverse the rally in HFC…Hope, after few quarter Basant will come on TV and disclose that he is no more super bullish on NBFC/HFC !!

5 Likes

Renewable Energy at one time = Piyush Goyal. A suave, genuinely educated politician with persuasive power can honestly convince of the sunrise sector fully backed by Govt. Policy. Cant help but see this equation. It translates: as investors we have t keep eyes and minds, both, open all the time.

I have tried to reach out to the Investor Cell to understand the deferred tax benefit. The explanation I got it, when the merger is price based, the difference between the acquisition price and book value will be treated as goodwill and it will be amortized over a period of time. On P&L, they will be showing the usual tax rate (35%) but in the cash flow, they will have a benefit (as they pay only MAT)

When inquired about the duration of deferred tax benefit, he said that they will be able to use it 5-6 years.

5 Likes

Thank you @naruto - this is also what Mr Ajay Piramal stated in his interview with Bloomberg posted above.

But this explanation does not make sense to me.

-

MAT is paid @ 18.5% of book profits in case taxable income is less than book profits. It is not 25% (as mentioned in the interview iirc). For a housing finance business (Piramal Housing Finance Limited), why should there be a material difference between book and taxable profits, I do not understand. So it is not clear why the company will pay at MAT rate.

-

However if PHFL is amortising goodwill paid, which is tax deductible as claimed in the presentation, and is not deductible as per book profits (why should that be…I don’t know, and haven’t seen such), then taxable profits will be less than book profits and MAT may kick in.

-

I don’t know what is meant by merger that is ‘price based’. If we assume it to mean cash consideration was paid instead of a stock swap, then the selling entities Piramal Capital et al, will have to pay capital gains on the consideration received from PHFL, in excess of capital invested. This would be at about 23% (20%+surcharge+cess); and can be said to comprise the goodwill and more because Piramal Capital was a profit making entity. This 23% is actual cash consideration paid / payable by the selling entities. But the Piramal presentation says no impact on cash flow, and I did not get that.

-

In case point 3 is correct, then PHFL will amortise goodwill on which it paid a 23% tax, which if not amortised will have incurred about 35% tax. Thus it will save about 12% in taxes on the amortised goodwill.

In summary, my current best understanding is that this transaction is a tax arbitrage between a lower rate of tax on capital gains and a higher rate of tax on business income.

7 Likes

Piramal Enterprise Ltd

Highlights of Q4FY18 and FY18 Annual results

Financials

- FY18

o Revenue grew by 24 % to Rs 10,639 Cr compare to last year

o PBT grew by 49 % to Rs 1,964 Cr compare to last year

o Net profit grew by 24 % to Rs 1,551 Cr compare to last year

Key Highlights - Company had create a deferred tax asset in balance sheet that has resulted in an accounting gain of Rs. 3,569 Crores.

- Effective tax rate is expected to go down from 35 % to 25 % for the next 6-7 years.

- Over last 7 years company had delivered a revenue CAGR of 29% and a normalized net profit CAGR excluding exceptional gain or losses of 55%

- Annualized shareholder return of over 40% as compared with 14% return by NIFTY over the last 5-year period

- Have returned over Rs. 5,600 Crores to our shareholders in terms of dividend and buy back

- For current year company had recommend a dividend of 25 Rs with 29 % dividend pay out ratio and 34 % after dividend distribution tax

- Raised Rs. 7000 Crores of capital last year out of which Rs. 5,000 Crores was in QIP and approximately Rs. 2,000 Crores in terms of the rights issue .Out of which 5000 Cr allocated for Pharma and 2000 Cr kept for pharma and other initiatives .

- As of March 2018 , out of total equity of Rs 26,447 Cr company have allocated Rs 9,275 Cr for lending and asset management business

- In Q4 loan book grew by 69 % to Rs 42,000 Cr , loans worth 23,000 Cr are approved but not yet disbursed

- PEL loan book has grown by 122 % CAGR in last 6 years. The company has consistently delivered 60% plus year-on-year growth in loan book in each of the last 13 quarter.

- Consistent growth is because of diversification with 22 products and business verticals added year after year

- AUM it has largely come from again the granularity in the RE wholesale book, it has come from HFC, it has definitely come from the 125% growth in the CFG and ECL.

- Credit rating upgraded from AA Stable to AA Positive which bought down cost by basis points. Company get clean report from RBI audit in December FY18.

- Developer sales is gone back to pre-demonetisation stage.

- Piramal Realty in the Mahalakshmi launch, Rs. 1,500 Crores sold in 7 days because of e good developer, the right product and the right ticket size. Similar launchers were done by company’s big developers in Mumbai , Bengaluru and Noida

- Ivanhoé Platform in the next three month will be announcing a slew of deals of equities for good developers of company on the Ivanhoé Platform

- Company had set up two teams , One for Capital market team to really map the market to go to the promoters and really give solutions and this will drive the CGL and ECL further.

- In HFC company is going into Tier-2 cities and opening in next 30 days in Nashik and then followed by Ahmedabad , Chennai and Hyderabad . In next 6 months company will open 4 branches.

- Looking for a fund d either it could be an AIF or partnership like Ivanhoe where company will play the consolidation story which is now happening in the renewable sector

- Lot of fee based income will be seen in FY19

Segmental Highlights - Financial services

o ROE expected to go up by around 2-3 % every year , so company is committed to deliver 20 % ROE in financial service business over long term

o Due to the synergies on account of merger of subsidiaries in the financial services segment the actual net profit reported for the quarter grew to Rs. 3,944 Crores and for the year to Rs. 5,120 Crore

o Real estate wholesale lending business.

RE book grew from Rs. 21,300 Crores to Rs. 31,800 Crores, it’s the construction finance (CF) book which really grew from Rs. 12,700 Crores to Rs. 19,200 Crores which was a 51% jump and lease rental discounting (LRD) grew from Rs. 1,200 Crores to Rs. 3,600 Crores which has a growth of 200%

o Entered into Hospitality sector and announced two deals one in Gurgaon which was Westin hotel and one in Bangalore which is JW Marriott where company had done a LRD transactions. This has fuelled the growth of RE wholesale.

o CFG(Corporate finance book) grow from Rs. 3600 Crores to Rs. 8100 Crores a growth of 118% during the year. - Housing Finance

o Loan book grew to Rs 1,200 Cr as on March 2018 , additionally the business has loan approved but yet not get disbursed at Rs 580 Cr at the end of March.

o Recorded a ROE of 25% plus over the last 10 consecutive quarter prior to the fund raised

o During the quarter the business generated a ROE of 19% a little lower than earlier quarter because company have now allocated, the entire allocation of Rs. 5,000 Crores from the capital raise to our financial services business.

o Gross NPA stood at 1 % for the last 9 quarters and Q4 of FY18 company gross NPA for 90 days remain healthy at 0.3 %

o Maintain provisioning of 1.8 %

o Launched housing finance business firstly in the MMR region which is the Mumbai metropolitan region . Till end of Mar FY18 launched housing finance business in Pune, Bangalore, Delhi, Gurgaon and Noida.

o In last 8 months company had approved 156 projects across 80 developers which AUM impact will be seen in next 6 months

o Innovative product which is getting famous is super loan

o It is a B2B2C business

o Formed emerging corporate lending group (ECL) for the upcoming corporates

Opened 5 locations Mumbai, Delhi, Chennai, Hyderabad and Pune

18 People team

AUM of ECL grew to Rs. 900 Crores with Rs. 200 Crores still to be sanctioned - Pharma

o Pharma growth after the sale of domestic Pharma business to Abbott has grown at 16% CAGR over the last 7 years

o Global Pharma which accounts for 92% of the Pharma revenue has delivered a strong growth in EBITDA margin from 10% in 2011 to 22% in 2018.

o Successfully cleared 31 US FDA inspection, 102 other regulatory audits, and 826 customer audits without a single day of production disruption.

o Global Pharma revenues for the quarter ended March 2018 grew 13% year-on-year to Rs. 1,245 Crores

o Margin improve significantly due to organic initiatives and high margin product acquisition.

o EBITDA margins remain at 22 % compare to 20 % in previous year

o Indian consumer product business registered a revenue of Rs. 346 Crores last year, which was an 8% decline over the previous year. Decline was due to GST and its implementation affected the industry and the wholesale channel . - Healthcare insights and analytics business

o Last quarter revenues grew by 3% to Rs. 234 Crores increase on account of growth in life sciences data and analytics segment which was partly offset by lower demand for research products that are being displaced with dynamic uses and big application

o Continue India expansion initiatives by on boarding 340 positions of Bengaluru and Gurugram offices, representing 29% of our total employees

Q&A

- In Financial services total net worth is almost 17000 Cr , so is 6700 cr come from pure lending to Shriram Investment , 9700 Cr from business and rest from AMC business ?

o Yes - Is the entire amount of 5000 Cr is included in Net worth ?

o Yes , there is a debt component, which under Ind-AS is also recognized, which is regrouped into debt. This also includes the increase in the fair value of Shriram Investment to the extent of Rs. 667 Crores and a share of profit during the quarter net of dividend that is how the overall reconciliation for the net worth is. - Kindly tell about major numbers ?

o ROA of 4.1 % in financial services business in quarter it was 3.1 %

o ROA drop has been 100 basis points but the margin drop has only be 30 basis points

o Cost to income ratio has not changed that much for almost 100 basis points drop into the ROA

o Net interest margin last quarter reported was 8% and this quarter is 7.7 % - In housing finance business out of total 1,210 Cr kindly bifurcate between housing loan and non-housing loan ?

o Roughly it is 75% retail and 25 % small construction loan - What is the average yield that company is getting on housing loan and non-housing loan ?

o On overall basis it is 9.55 % - Why does company profit not risen in spite of rising loan book growth by 69 %

o This year was full of tax of 35 % and so that’s why company don’t see the correspond effect in PAT - Explain in brief about fee based income ?

o In real estate and CFG all the deals which company is doing is also down selling a part of it now. So fees are going to come from down selling So whether it is in the renewable sector, in the road sector, whether it is in cement, etc., it could also be in the real estate. - Which are the top three sectors on corporate finance group ?

o Logistics, renewable and auto ancillary will be the top three sectors which may have like 50%- 55% of the book size and the balance will be across different sector. - Is this consortium lending or are you generally the sole lender?

o Generally company is the sole lender if the exposure is large then company down sell it for it company has prepare a team of like minded people for down selling in partnership which is formal - CGF loans would be of What ticket size ?

o Loan could be anywhere from Rs. 200 Crores to Rs. 500 Crores - How company was able to grow the lending business with competing Banks and other NBFC ?

o Because company is not a lender it is a solution providers - Did the expected tax rate of 25 % will start in next year ?

o It is cash tax rate. Effective tax will remain to 34 % , company have created this deferred tax assets on account of the amortization of goodwill. At MAT level and cash tax will be 25%, but the effective tax rate will remain 34%. - Explain sort of the ROA and ROE map and what leverage do you expect to run this business at?

o Equity infusion is of rupees 5000 Cr and debt to equity has come down to 3.7 so it will affect the ROE in short term. But it will do back to 20 % by 2020. Because at that time company will again have a Debt to equity of 4.5-5 .

o Company will get an ROE benefit on a cash basis of 1.5% to 2% and that is why with that impact in spite of the debt-equity going down and affecting the ROE company will still be having a ROE of 20 % - Why does cost to income moved up ?

o Because company is investing in housing finance business and opening new branch every month , so this will in short term skew the cost-to-income ratio. But it will benefit in long run in 2020 - What is the company strategy in IT business ?

o Company have added analytics to this space and a lot of that growth has taken place because of the people in India and therefore company have added 340 people in India which is in Bangalore and in Gurgaon.

o Focus is to make new products available to serve both the pharma industry as well as insurer .Company is providing Data to the customers and company is making it at a low cost in India

o Growth will come back from current year - What is the outlook on OTC business ?

o It was an aberration last year. Because of GST - What about launch of Desflurane ?

o It is available in other parts of the world, but the US which is the largest market company still have some things with the FDA and should launch it in the near future. - Rs 23,000 Crores is sanctioned but it is yet to be disbursed what is this disbursement linked to can you explain that?

o There are two parts of it . One side there are deals which is sanctioned but not disbursed and second is on the construction finance . 60% of the portfolio of real estate lending is construction finance.

o So what happens in construction finance that if you have sanction Rs. 100 you may lent only Rs. 20 because then when the next slabs come up you will give another Rs. 5 and so on and this Rs. 23,000 Crores is basically a combination of these two. - how will the growth rate in the loan book taper down somewhat because of syndication as well as prepayments?

o Large exposures will get down sold .

o Anything from 35% to 40% of the book company is looking forward for churning in fact if company this year itself had churned 50% of the opening book which is a good thing . So it is a part of business and when company budget their numbers for every year they take these things in account - Can the margin improvement over the last 3 years from around 12.7% today at around 18% at EBITDA level will inch upward more in the future approach ?

o Company expect it in 20-22 % range

o Targeting 15-20 % of ROCE

15 Likes

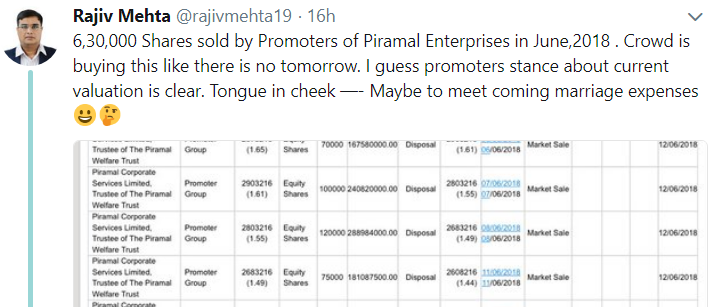

Promoters sold 1.7 Lakh shares 4th/5th June. This came as a bit of surprise. No wonder stock price tanked below 2300 on 5th June (although it was bad day for all small/mid caps).

Lets hope this divestment was to allow some influential investor to get in

I dont think it is a big deal since since only .25% equity is in question morover they more were than fully subscribed to the recent right issue.

what does the gift entries mean?

If you see gift entries, there are two entries for each quantity exchanged. It is a inter-promoter group transaction.

Someone in twitter raised issues about the REIT arm of Piramal which may very well extend into the direct lending as well, did some prelim google search but looks like no such information publicly available, anyone aware about any issues here?

Yes. I started that thread. I am an investor in their REIT funds. I think there is some stress there. Quiet a few of the RE players they have lent to are not paying interest too. Also, the kind of NPA they show in NBFC looks too good to be true. I am in the RE field and know what’s going on in the sector.

Having said that, I am not saying it’s a bad company. I had made a 8x on this company and held it for many years. It’s just that, I am a bit uncomfortable with their NBFC lending. That’s all. If I get my definitive answers on this, I am willing to change my view.

16 Likes

Thanks for your reply Sir,

Can you please also share or give some insight on the quantum of the issue it would be helpful?

2 Likes

Does their REIT arm is subsidary of PEL, or is it a seperate business altogather? Though I am also invested in PEL, but somehow I also could not digest the way in which they tell in almost every conference call that Housing finance is B2B2C (that looks little risky) sort of business for them. As per the last con call the yield is meager 9.5% in housing finance compared to the cost of fund 8.5%, This is just 1% spread.

its by the welfare trust. not for promoters. afaik, its for employee welfare.

2 Likes

Welfare Trust is also listed as Promoter group. Does it mean that employees have lost confidence in the near term growth of the company?

Can someone call or write to investor relations and find out the reason for the share sale by promoter entities. The contact details of investor relations is

Hitesh Dhaddha

Email : hitesh.dhaddha@piramal.com

Phone : +91 22 3046 6444

Devanshi Dhruva

Email : devanshi.dhruva@piramal.com

Phone : +91 22 3046 6376