Can you provide guidelines for evaluation of finance companies? What parameters should we look at?

I want to do a fair price valuation of piramal.

Last year they hired group head of Analytics who has 15 year + experience with BoA in risk and retail credit analytics. So, I am assuming it is for retail housing finance

More awards and accolades for Mr. Piramal

1 Like

Capital structure simplification started with amalgamation of Piramal Finance Ltd and Piramal Capital Ltd. with Piramal Housing Finance Ltd.

Frankly, I don’t have the answer to your question. But, in my opinion, we’re hassling ourselves by excessively scrutinising these transactions. I reiterate, I’ve no clue whether the transaction was legitimate or a payoff. But, it’d be a disservice to ourselves to have unrealistic expectations of promoters. At the end of the day, promoters are just like you and me - Prone to mistakes and errors of judgement

Payoffs, though immoral, are the cost of doing business not only in India but in most countries. That’s just how it is.

To me, what’s important is the promoter’s intention to generate wealth for himself as well as minority shareholders. I believe, Mr.Piramal harbours the intention to create wealth for shareholders.

14 Likes

Philosophically speaking, I agree with your point. Not having clarity on this issue is a matter of concern. But as an investor, our job is to see if there are more telltale signs of such “missteps” or not. I am ready to ignore if it is “one off” mistake as they say “to err is human”.

Having said that, it is going to be individual’s call whether to show faith and stay put or sell out on first sign of trouble. I have tried both the options in the past and have regretted  . So in this case, I have decided to avoid knee jerk reaction and spent more time researching about Piramal’s. Having gone through most of the information available in public domain about the company and its promoters, as of now I feel it seems like “one off” issue and hence I am ready to given them longer rope. But need to remain watchful.

. So in this case, I have decided to avoid knee jerk reaction and spent more time researching about Piramal’s. Having gone through most of the information available in public domain about the company and its promoters, as of now I feel it seems like “one off” issue and hence I am ready to given them longer rope. But need to remain watchful.

4 Likes

See the flashnet issue tells a simple story, Piramal’s are no holy cow. One would appreciate that somebody dug in to find this and there could be many more.

This is no way a worry for investor but yes for those saying corporate governance and all that, they need to understand that holy cows do not yield, businesses do.

So if the corporate action is for business growth, creating shareholder wealth or taking away the wealth from minority shareholders.

This question shall be asked and answer would be pretty clear.

1 Like

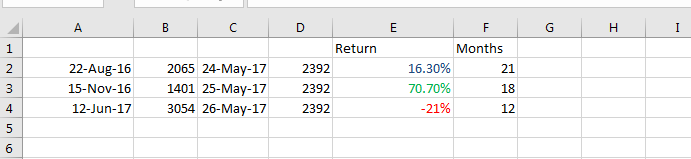

Those who bought during demo period made the money…while people who might have bought on 52 week are staring at 20% drawdown…and some who bought 2yrs back made a modest returns ![]()

5 Likes

Results are out

• Revenue :

Up 24% at Rs.10,639 Crores during FY2018 vs Rs.8,547 Crores in FY2017

Up 21% at Rs.2,991 Crores during Q4 FY2018 vs Rs.2,463 Crores in Q4 FY2017

• Normalised Net Profit*

:

Increased by 24% to Rs. 1,551 Crores for FY2018 vs Rs.1,252 Crores in FY2017

Increased by 21% to Rs. 375 Crores for Q4 FY2018 vs Rs. 311 Crores in Q4 FY2017

Dividend of Rs 25 (1250%) declared. Interesting to note fast paced growth in the housing finance. Please see excerpt related to housing finance from the declaration as below

1 Like

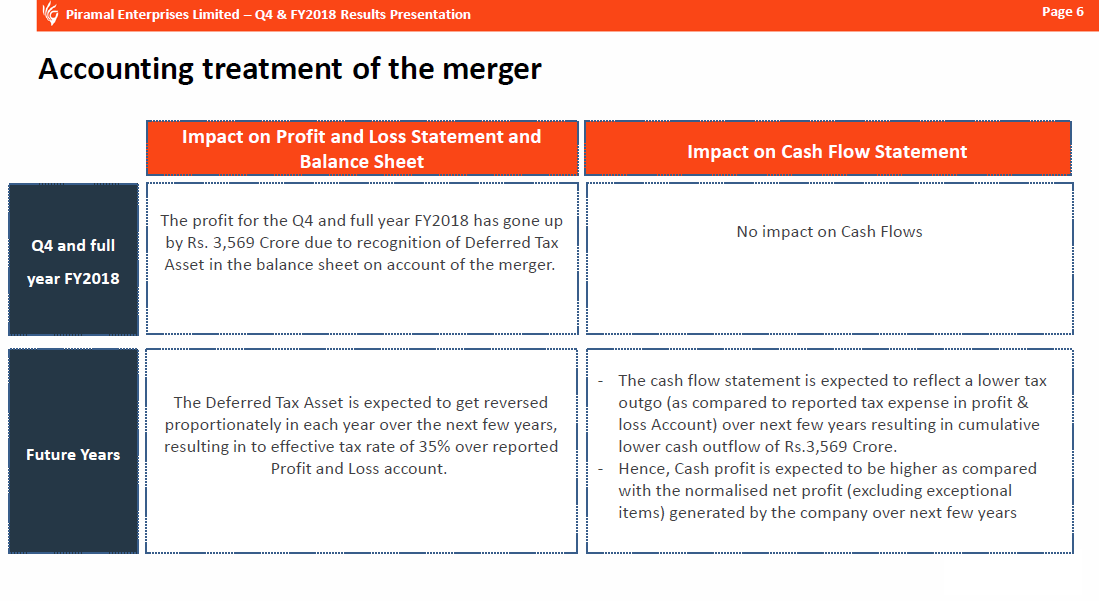

what is this deferred tax on mergers?

will it not pay this tax?

Deferred tax on account of merger of subsidiaries (3,569) - - (3,569)

One more results presentation

How many years will this deferred tax asset be spread over? If it is spread out over the next 5 years, then cash profit will be higher by 700cr for each of the years. What impact will this have on the dividends, reserves or book value?

Any idea how was such a large deferred tax asset created? They would need to have losses of ~10,000 crs to create such a large deferred tax asset (Assuming 35% tax rate)

As per the concall details this is on account of the amortization of goodwill on account of the merger. This will reduce the tax rate to around 25% in the coming years from the current 34 %

1 Like

Here Ajay Piramal talks in details on deferred tax.

1 Like

why the screener is showing PE of piramal as 8.68 now after the results?

Is this due to deferred tax? any insights pls?

yes… it is due to deferred taxes… Screener does eliminate the impact of one time or extra-ordinary items.

So what will be the correct PE now? should be same as earlier 30 ?