in a rising market everything goes up. reverse is true in falling markets.

since no asks for a reason during the former, they shouldn’t for the latter

as well!

disclosure: holding and applied for rights. I feel stock may fall below the

rights issue price of 2380 if the correction continues.

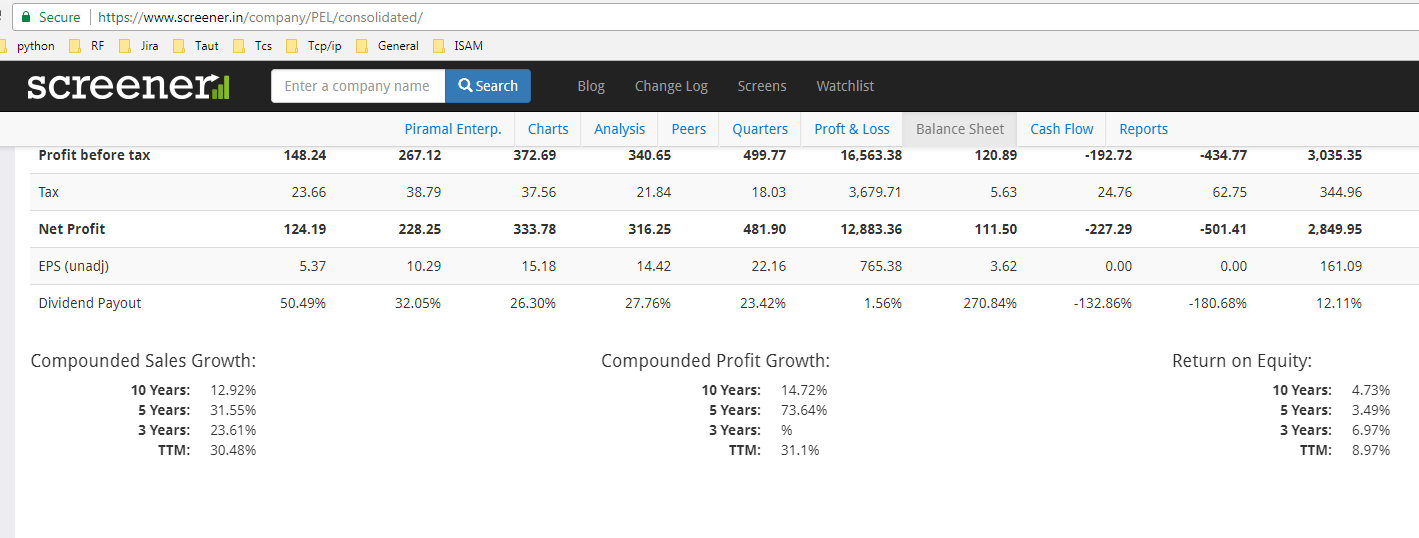

When computing the ROE you would have to make suitable adjustments to the book value of PEL. As on 2017, they had a goodwill of 5427 crs ,Other intangible assets of 3080 crs and intangible assets under development of 147 cr. If you make these adjustments you would arrive at an ROE of 20%-21% which is more in line with what the group is making since they account for a significant proportion of assets. There are some other adjustments that one could make to arrive at the carrying value of operating assets. However, the point is that the reported ROE is much less than the actual ROE. As far as cash flows are concerned , I think your queries have been clarified.

in the q3 earnings call, the management was talking about stock price returns and comparison with nifty. is this normal?. till now i have never come across any good company ( i mean companies considered good) talk about it in the earnings call.

disc: not invested.

When company need to raise money through QIP / Right Issues / NCD, they must create positive environment among investors about return ! It’s marketing tricks which all good or bad companies normally follows !

Ajay Piramal - It’s all about recognizing the risk correctly

In the early days, when we were hunting for acquisitions, I faced more than my share of criticism. Analysts didn’t believe in our story. There were voices of dissent – we had no organic growth to show, we were driven by only acquisitions, that is not a good strategy and so on. But it worked and worked beautifully. In the history of pharmaceutical deals, we got the highest multiples ever. When I bought these companies, I bought them at a third of their sales value. But when we sold them, we sold at nearly 10X sales. That itself gave us a 30X return!

Currently, there is so much criticism around our investment in real estate. Lending to developers is risky; the banks have to provision additional capital as risk weight. But for us, it is almost risk-free. You have the project as a security. If you lend with a safe margin and the developer does not execute, you can take over the project at half the value, complete it and make your money. It is one of the businesses where you get to take over the assets without any baggage like labour or other costs. A bank can’t take over a project and recover its money, but we can. We have execution capabilities.

It has already been replied and check the AR’s of last few years ROE is close to 25%…made screener has certain predefined algorithms to calculate certain area’s i believe

Understood to some extent, this means some companies doesn’t have goodwill in the Equity base? Or Is that screener is wrong in including goodwill only in the case of PEL?

Screener does a pretty good job in most cases of calculating the ROE. However in case of PEL - or any company that has grown through acquisitions - it is always better to get into the line items of the balance sheet and edit out items that dont represent operating assets. PEL balance sheet contains quite a few of these items. Its not a simple balance sheet for sure but unless one does these adjustments it would be difficult to arrive at a reliable valuation by just looking at screener ROE numbers.

Thanks Bheeshma, for my understanding I would consider PEL has as an exception while comparing ROE, I believe adding goodwill to balance sheet is a confidence boosting for investors. This makes Price to Book value appealing for investors, If I compare with similar company for Berkshire Hathaway, Goodwill has been increasing every year.

The idea of Goodwill is to capture the difference between the actual book value of the acquired entity and the sum paid to acquire the entity. There will always be this difference. For example, Microsoft bought LinkedIn for 39 billion USD but the actual value of LinkedIn is way less. So where would the difference go? That’s exactly what Goodwill captures. So if a company never had any acquisitions there wont be any Goodwill. Berkshires Goodwill is increasing every year because it is acquiring companies every year.

If you watch Aswath Damodharans session on valuations in YouTube, he goes into detail about it.

Does Ashwanth Damodaran also exclude goodwill while calculation of ROE?

As an investor, I wouldn’t care how a company generates its returns. If the company keeps money with them as opposed distributing to shareholders then they should generate returns higher than the investor’s cost of capital. If the company invests in an organic project vs acquiring another company, my return expectation from the company will not change.

PEL does have a low return on equity. The NBFC business is generating 20-25% ROE. The pharma and the analytics business, which are acquired, is where they are generating low ROE. They invested a lot of money in acquiring these businesses and building an India wide distribution platform. I would expect PEL to reap the benefits of these investments in next few years. And ROE should be higher than our CoC soon.

Disclosure: Invested and very bullish on the stock

I dont think taking out the goodwill out of aquisition is the only right way. Ideally both metrics should be carefully looked at in order to judge the performance and numbers. Seeing RoE in isolation of goodwill will mean that any business aquired at crazy mutliples should also be looked in a good way which may not necessarily be the right way. Lets say there is a business with 25% RoE and is aquired at 5 times price to book - so the computed RoE would be 5% while excluding goodwill will show 25%. Only looking at 25% means isolation of assessment of whether this business was worth buying at 5 times book and whether current and future profits are looking great enough to justify the price. Similarly only looking at 5% as the number is also wrong as it excludes the future potential of the business which is the prime reason behind paying so much of goodwill.

I don’t remember him talking about Goodwill and RoE. But Goodwill is already paid and it should be captured in the cash flow. Since it’s intangible, ideally it should be amortised over a period. Therefore it would make perfect sense to remove it from shareholders fund to calculate RoE.

Goodwill never Gets Amortized but it is checked regularly(at least Annually) for any impairment.

If any impairment is recognized than that amount will shown as loss on income statement and goodwill is reduced by that amount.

Piramal have lots goodwill because of previous many acquisition in pharma. As pharma has lots of off-balance sheet cost such as R&D.

Piramal story below. As I read it, a line caught my attention. Amongst the people he admires he names Jamshetji Tata for laying the foundation of Indian Industry and giving it back to society.

Laying gratitude where it belongs is very important. My years spent figuring out the dark and evil British Occupation of India, one beacon that lit up the darkness time and again has been the House of TATAS : their foresight, nationalism, entrepreneurship and defiance of the British through setting up Industry: steel, hotels, shipping and on and on. .

Once the ICS was open to Indians, TATAS funded the aspirants because the money needed to appear for the exam in London was huge.