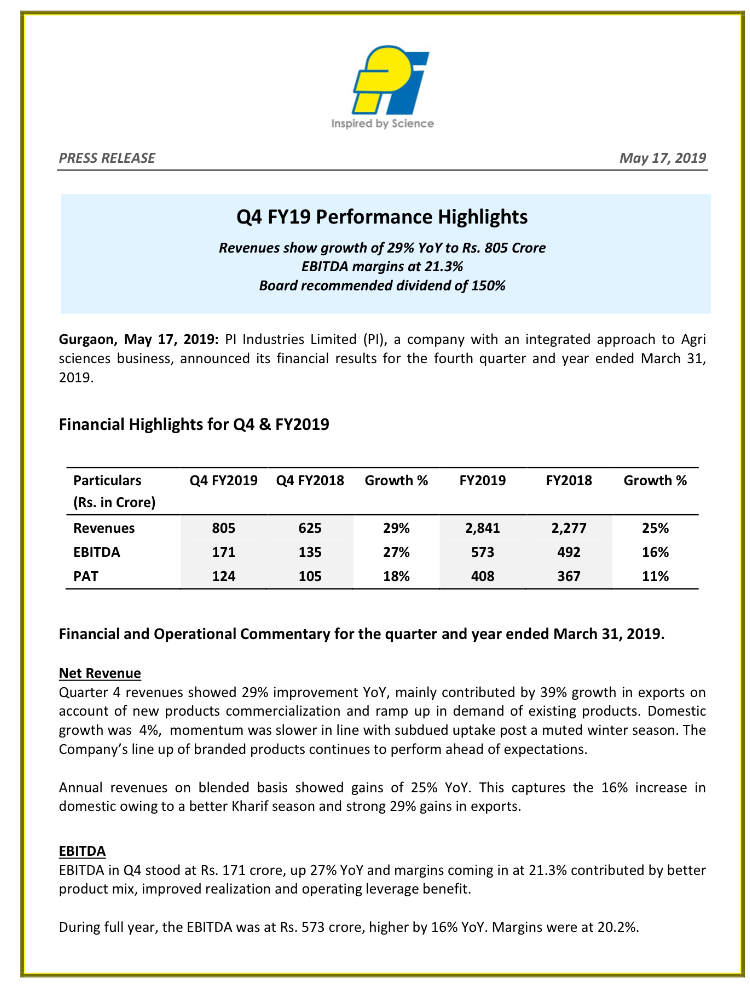

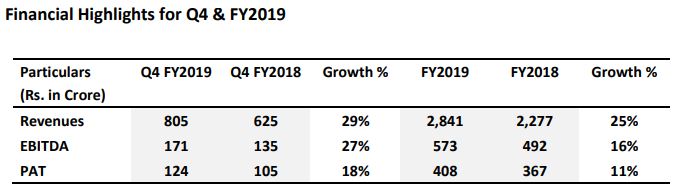

Q4 Results:

Not much update on their pharma foray

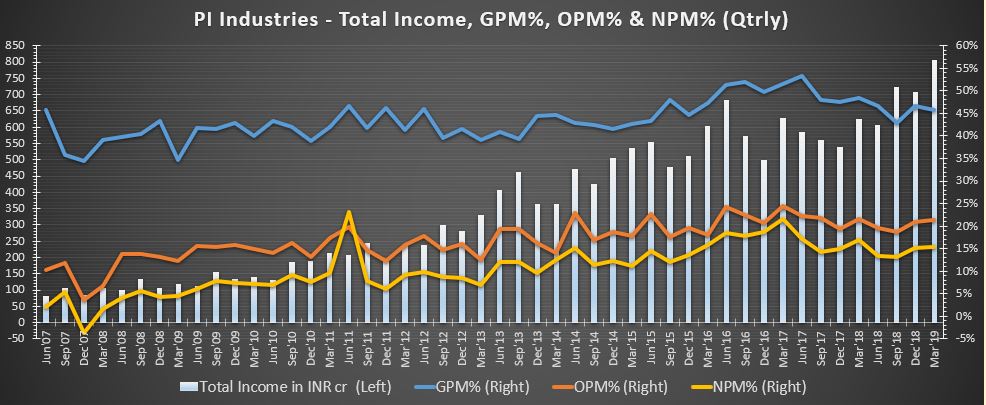

Relatively good Q4 and Fy19 for PI. Performance mainly driven by strong CSM franchise.

- Q4 CSM exports growth was 39% on account of new products commercialization and ramp up in demand of existing products.

- Q4 Domestic growth was 4%, momentum was slower in line with subdued uptake post a muted winter season.

- Fy19 CSM exports growth was 29%. Driven by pick-up in global demand, ramp up of new molecules and some growth in the base business.

- Fy19 Domestic growth was 16%. Driven by the four products which were launched along with BASF in FY17 have done good and improved growth by Nominee Gold.

The China clampdown on pollution has impacted PI in negative (high RM prices) and positive (sharp increase in number of molecules in the pipeline) ways.

- High RM price has prevented non-linear bottom-line growth in Fy19.

- Monetization of growing pipeline to happen in the coming years.

Outlook

- Expect to launch 2-3 products ahead of the key cropping season. (One of high potential product is weed herbicide awaiting approval; it has a potential equal to or even greater than Nominee Gold.)

- Momentum in exports to maintain on the back of easing global inventories and firm requirements from innovator customers. Commissioning of additional capacities to support improvement in run rate of the business and launch of 3-4 new molecules will drive the growth.

Q4Fy19 earnings conf call (on 05/20 04:00pm) would provide insights on the following -

- Commissioning timeline of three new MPP plants (expected in Fy20).

- Any significant change in no. of molecules in pipeline.

- Backlog order book size.

Source -

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5efa6651-c629-44db-9770-279cbb4b9f04.pdf

Press Release: https://www.bseindia.com/xml-data/corpfiling/AttachLive/2cac4ebb-aca5-4208-9cc9-a04ab93b2384.pdf

10 Likes

The accounting footnotes to the Q4 result more or less seems to be confirming this, the specific term used is “revenue booking over time rather than booking revenue at a point in time”, this is specific to the CSM business. Let us see what they say on the conf call.

My sense is that like to like CSM growth is much lower than the 29% reported for FY19. Actual number is likely to be less than 20% as per old accounting method. This also has implications for how the order book translates into revenue - the conversion will be much more predictable and more under the control of PI Ind than it was before.

Long story short - I think growth is reverting to the long term guidance of 16-18%, nothing beyond. Does not make sense to look at the 29% YoY growth number for CSM in FY19 and extrapolate into the future

10 Likes

Monsoon progress in India is not good and many areas are under rain deficit could impact agrochemical business.

Globally world leader BASF is not happy and forecasting H2 profit slowdown worst than 2008 crisis…

https://www.icis.com/explore/resources/news/2019/07/10/10389609/insight-basf-profit-warning-signals-major-chemicals-slowdown-in-second-half

https://www.bloomberg.com/news/articles/2019-07-08/basf-cuts-2019-outlook-citing-trade-conflict-industrial-output

Should we worry?

Disc - invested in PI

1 Like

For near term, maybe! For long term not at all. I’ll average down If price corrects.

Disc: Invested for long term.

3 Likes

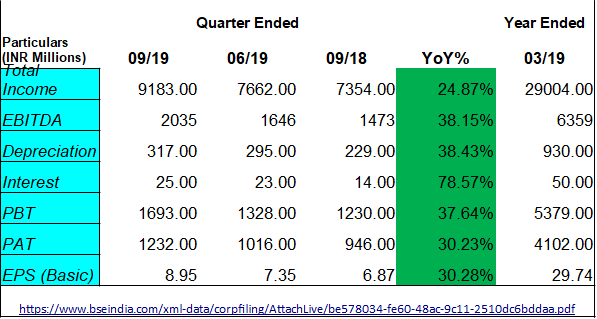

Q1 Results: Revenues 25% up, PAT 24% up YoY

6 Likes

My notes from Q1FY20 concall

CSM grew 59% on lower base last year, domestic declined 13%. Consol rev up 25%. Margin 20.1% despite pressure from domestic and expenses of new plant. EBITDA was up 28%.

CSM/Exports- Generates more margins, lower asset turns. Higher ramp up cost

-

Utilization was 90% in Q4. De-bottlenecking existing capacities. Guiding further volume pickup. One plant started in Feb 2019.

-

Will commission 2 new plants in Q3 (new tech block, mix of back integration and incremental revenue) and Q4. Something to do with specialty chem, but not pharma. Working on 2 more plants for H2 2021.

-

Launched 1 product in Q1. H2 will see 2 more molecules.

-

Innovative molecules of PI still seeing demand. Not much affected by vagaries of trade war etc. Very clear visibility for existing commercialized products, not only this year but coming years. Not seeing any reversals or deferments. Customers are also confident of raising volumes. Molecules entering into new countries every year.

-

R&D pipeline is robust. Conversion has improved in last couple of years. Lot of business flowing to India because of China issues.

-

Fine chemicals?? Gradual diversification- electronic chem, imaging chemicals, Pharma early intermediates. 10% of R&D pipeline, some in pilot stage 5-10 ton stage, not very small but not large either.

Domestic- Generates more cash on investments

-

Launched 1 insecticide. Branded portfolio helped. Wheat herbicide got approved, will be launched in Rabi.

-

Higher trade inventory in industry, expect flattish /kharif season. At best low single digit growth.

-

Monsoon improving in July, sowing increased sowing. Domestic business should pick up in Q2-Q3.

-

Can do high single digit growth for full year, but difficult to predict Rabi season now.

Outlook of 20-25% revenue growth and 50-100 bps expansion in EBITDA margin, over and above IndAS impact. Order book $1.4bn. Cash surplus 165cr.

Always very cautious of capex. We like to get long term understanding before putting capex. Lot of good opps coming our way. Capex of 400-450cr is based on our current understanding (130cr done in Q1). If more large products get converted, we may review our plans upwards. Plant initial volumes are low and gradually reach 80-85% utilization in 3 years, with asset turns of 1.25-1.5.

12 Likes

PI executes an offer for acquisition of 100% stake in Isagro (Asia)

- Executed an offer with Isagro S.p.A (Italy) for acquisition of the business of Isagro Asia, who are engaged in Contract Manufacturing, local distribution and exports of agrochemicals through acquisition of 100% shareholding of Isagro Asia.

- The transaction value is estimated ~INR 345 Crore net of cash and debt

- The consummation of the proposed transaction is expected in Q3FY20 subject to finalisation of definitive agreements, customary closing conditions and regulatory approvals. The parties have entered into exclusivity agreement for this purpose.

- PI sees encouraging growth opportunities across its business model and seeking initiatives to augment business progress.

- The proposed acquisition will provide PI access to additional manufacturing capacities to meet growing demand of global customers and synergy benefits of adjacent manufacturing site while de-risking the supply chain of few products.

- In addition, will help PI strengthen its position in Indian market by leveraging complementary product portfolio and distribution channel of Isagro Asia

Source: Media Release

- Isagro (Asia) plant

https://www.isagro.com/en/about-us/plants/panoli.html - Adjacent to PI Panoli plant

- Buy v/s Build

- PI has decent free land and capabilities to augment Jambusar plant; however, build takes time

- Seems co is running short of capacity. US-China or something may have triggered orders rush in (speculation). Thus PI preferred buy over build?

Note: Trading at very rich valuation currently; no margin-of-safety for anyone planning fresh entry

7 Likes

Isagro Asia Private Limited is a company based in India and active in the manufacturing (through a plant located in Panoli – Gujarat), registration and local distribution (through a distribution network in India), with export activities.

The divestment is part of the process of redefinition of Isagro’s assets allocation, on a world-wide basis. The relevant proceeds will contribute to reduce Isagro’s net financial debt and will also be utilized to support the Group future growth.

Isagro has only one plant outside Italy. Located in Panoli, engaged in the synthesis of the main active proprietary ingredients of the Group and their intermediate products and formulation and packaging of different products bound for the local market. Employee count=122. Since 2003 it produced, with increasing volumes and a gradual improvement in efficiency, the M-Alcohol intermediate product, used by the Group to produce Tetraconazole

The site covers a total area of 154,786 sqm, about 34,425 sqm of which are covered.

It had revenue of 150cr for H1CY19, EBITDA of 18cr, Net profit of 11cr. It was about 20% of group’s revenue

6 Likes

Now that Monsoon is very good in all parts of India, esp in West, South and Central India, i feel the agrochemical businesses will do very well in Q3 and Q4. what is your view

Pi management did indicate that they expected a Pickup in Q2 but its quite possible that lot of regions have recieved too much rain, which could be counter productive. However rabi season should be very good with high reservoir levels.

PI is paying Rs.345 crore for the Isagro acquisition “net of cash and debt”. Isagro Asia is debt free and has Rs.145 crore of working capital. So if I understand this correctly, PI is paying Rs.200 crore for fixed assets such as land & building, plant & machinery etc. These assets produced sales of Rs.300 crore in 2018 and Rs.150 crores in H1 CY2019. Assuming current numbers hold going ahead, the Isagro acquisition adds to Rs.300 crores in revenues and Rs.22 crores in PAT per year, which increases the EPS by roughly Rs.1.50 per share. At current P/E of 40, this translates to an upward impact of Rs.60 on the share price.

What is not known is the capacity utilization of this plant and whether PI will have to make further investments in this plant to scale it up. The above calculation assumes plant is operating at full capacity.

8 Likes

The article may have some relevance to this thread…

3 Likes

There was a good update by Motilal on the Isagro acquisition.

-

PI Industries has announced the acquisition of Isagro Asia from Isagro S.p.A for INR3.5b. Isagro Asia operates in India and is engaged in contract manufacturing, local distribution and exports of agrochemicals.

-

PI will acquire 100% shareholding held by Isagro S.p.A in Isagro Asia, either directly or through a subsidiary. The deal has taken place at a valuation of ~15x P/E FY19. PI will fund the acquisition partly through internal accruals and partly through debt. The proposed transaction is expected to be completed in 3QFY20, subject to finalization of definitive agreements, customary closing conditions and regulatory approvals. Company remains confident of integrating Isagro Asia’s operations with itself in FY20.

-

Isagro Asia generated revenue of ~INR3b in FY19; of this, 65% was contributed by the domestic formulation business and balance came in from the contract manufacturing business. In the domestic formulation business, Isagro sells in-licensing products, generics products and proprietary patent products. Three key in-licensing products include (i) insecticide – mitigate, (ii) fungicide – domark, and (iii) biostimulants – siapton. PI intends to leverage its distribution network and firm up its position in the domestic market by leveraging the complementary product portfolio of Isagro Asia.

-

In the contract manufacturing business (exports), Isagro Asia exports M Alcohol – a technical patented product to its parent company (Isagro S.p.A) and also operates a small CSM business. Post-acquisition, PI intends to continue supplying M Alcohol to Isagro S.p.A.

-

Isagro Asia has two technical lines that are currently operating at 30-40% utilization level, which PI intends to scale up post acquisition. Moreover, PI will also derive synergies from the acquisition, such as having an adjacent manufacturing site and de-risking the supply chain of a few products.

Isagro acquisition- MOSL.pdf (290.3 KB) **

7 Likes

PI Industries (PI) has reported an accident on one section of its multi-product plant (MPP) at Jambusar. This accident caused two fatalities, while nine others are injured.

source; https://www.thehindubusinessline.com/markets/pi-industries-buy/article30503098.ece

2 Likes

Q3 results notes:

- Consolidated Revenues 849 crs 20% up, PBT 169 crs 21.5% up, PAT 121 crs 13% up YoY (Lower PAT growth due to higher tax rate - ETR 27% due to change in SEZ share)

- Domestic business 24% up, exports 19% up YoY

- Board of Directors approved fund raising of upto Rs. 2000 crs to support next leg of growth strategy for business

- Recent acquisition of Isagro will be reorganized by transferring domestic distribution business to Jivagro Limited (wholly owned subsidiary of PI Industries) and rest of the activities will be merged into PI directly

- Total consideration paid for Isagro was Rs. 455 crs including Rs. 111 crs towards surplus cash

- Net debt 252 crs

- Interim dividend of Rs. 3

- Maintain FY20 guideline for ~20% in performance Y-o-Y backed by healthy order

position, commissioning of additional capacity and contribution from newly launched brands

Results:

Press release:

Disclosure: Invested - Do not recommend buy or sell. Not an investment advisor and Investors are advised to do their own due diligence.

4 Likes

PI has been earning superior returns on invested capital and reinvesting majority of cash earnings back into the business at high returns. Classic recipe of compounding machine (as we all understand). This cycle worked beautifully.

PI decides to change gears now. Intend to invest/ deploy up to 2000 Cr new capital (QIP) in the business. Seems sensing mega opportunities; Q3Fy20 conf call provides some glimpse.

Quick notes follow (non-exhaustive) -

QIP objective: To deploy capital mainly into three areas (evaluation in progress) -

- Current organic business growth; further expansions and scale up

- Scale up of newer and niche technologies that co has been working for last couple years

- Diversifying into adjacent verticals - CDMOs, CSMs, pharma, specialty chemicals, nutraceuticals, imaging chemicals, etc

Timeline: Anytime in next 1 or 1.5 month

Thinking: Build the war chest. Opportunities available; evaluation in progress. Whenever co find right opportunity, then deploy this cash. Make PI ready so whenever opportunities come can tap them. Enough things in the pot that are boiling currently.

Up to 2000 cr enabling provisioning; not decided on final size, granularity/iteration and exact timing at this point.

Near term organic capex: New MPPs that are likely to start up in near future -

- One new MPP starting in Q4 Fy20 (most probably this month)

- Second expected to be commissioned by Q1 Fy21 end

- Third coming up in Q3/Q4 of Fy21

Equity dilution v/s raising debt:

- Will be diversifying and also investing in scaling of new and niche technologies

- Co believes it is better to invest through equity route in these new models

- At appropriate time can take a call on debt as well

Demand:

- Seeing increase in demand of existing products and significant flow of new inquiries

- Number of new projects in R&D pipeline is constantly increasing

- Attributable partly to China; China one of the reason; not the only reason

Today v/s Going forward:

- Today - In CSM area, co work on technologies shared by customers (CSM)

- Going forward - Scaling newer and niche technologies where co is developing own IP; these technologies can be used in different verticals not limited to agchem

Isagro capacity:

- Working on aligning Isagro capacities currently

- Significant opportunities of increasing Isagro capacity utilization (one of the key drivers of the acquisition)

- Aligning available capacities with CSM export product basket

- Gradually fitting CSM products in available capacities and re-purposing capacities

- In next 6-9 months, will be able to fully align capacity with demand pipeline and orders in hand

- Aim - maximize capacity in next financial year

Strong demand:

- When probed about i) Three new MPPs coming in next 12 months, ii) Isagro capacity coming online shortly and iii) looking at portion of QIP to further expand capacity organically business growth - Co confirms seeing very different shift in demand momentum vs what has been seen in last 3-4 years. Certainly seeing demand upsurge. Agchem continues to show promise; seeing agchem business growth continuing for next couple of years.

New targets expected to be from non-agchem area. Will have certain synergies and leveraging opportunities with PI’s existing capabilities. Will certainly look for some interesting technologies, interesting markets, customer segments, etc.

Have necessary environmental approvals (both, EC and GPCB) for basket of products that co has been currently doing and evaluating in R&D

R&D strength and pipeline:

- More than 300/350+ scientist in R&D area

- Two broad categories in R&D - one is CSM (process research) and other is own niche and new engineering technologies that PI has been developing - both in chemistry and process area

Strategy & Risk:

- Q: Without any leveraging, chances of another PI size co getting created in next 3-4 years with 2000 Cr (QIP) investment. Haven’t seen such kind of aggression in industry earlier. Any risk involved considering large capex, overcapacity, overinvestment, which may unfold in next 3 to 5 years?

- PI has been very conservative in planning, investing and targeting all past investments over last several years and quarters. Same approach today too. Rather than overinvestment in a particular area, co is gradually diversifying in to new technologies and new verticals. Co is investing in specialty area; not in generic or high volume/ bulk area where risk is high when market demand goes haywire (not investing in these areas; not evaluating also). In nutshell, PI will remain cautious before making any investments.

In next 3-4 years, co sees topline potentially doubling without compromising margin and return rations.

Looking at opportunities and options in India and outside India as well; open to look at global platforms.

35 Likes