PI Industries

Highlights of Q3 FY18 and Nine Month FY18

Company is focused on upgrading technology to get higher productivity. Active value chain and global partners support is very strong.

In domestic market company has suffered because of delay in monsoons which in turn reduced the investment by the farmer in farm segment.

Recent announcement in Budget like MSP, Gramin agriculture, increase in budgetary support in Farm credits, Fasal Bima Yojana and higher allocation of krishi sichay yojana these initiatives will help for a sustainable growth in agriculture.

In domestic there were availability issue in Tamil Nadu, Karnataka, Chhattisgarh has impacted company performance in Q3.

Company’s new products have a good yield and well accepted by the farmers. Full potential of these products are expected to occur in coming year. Export is also ramping up. Improvement in global market gave sentiment that growth momentum will be good.

In recent past, there was stress raw material supply from China impacted supply schedule of company exports. In short term, company will find an alternative solution for this raw material.

Company expect consistent growth because of healthy orders in pipeline.

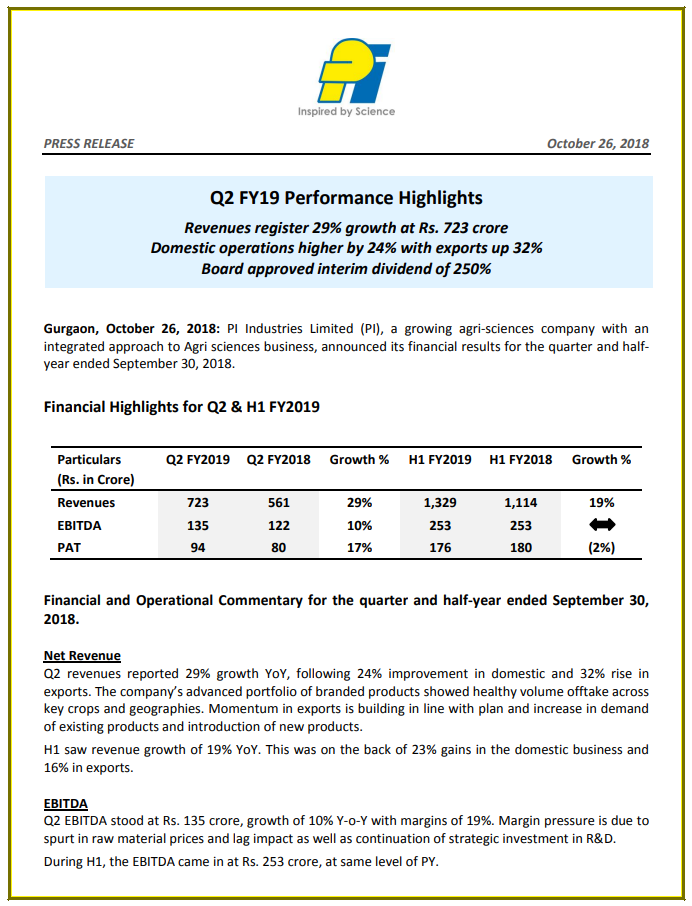

Financial Performance

o Q3 Performance

Revenue grew by 10.3% to 538 Cr this was driven by 3 % rise in domestic sales and 14 % in export

EBITDA came at 105 Cr with a margin of 19.5%. Product mix has impacted raw-material prices have result in shorter margin for the company.

PAT stood at 81 Cr

o 9 month FY18 performance

Revenue stood at 1683 Cr marginally lower YOY basis due to uneven rainfall in kharif , GST impact and lower export during FY18.

EBITDA stood at 358 Cr at margin of 21.6 %.

PAT came to 106 Cr. It is lower mainly due to effective tax rate from 14 % of last year to 22 % this year.

Net Debt-Equity stand at 0.03 and company be cash positive with available cash flow of 243 Cr as on 31 Dec 2017.

Q&A

Does the fall in EBITDA margin by 200 basis point is one time or it will be for longer time and how raw material supply impact further?

o There were multiple reasons for lower EBITDA margins most important reason was product mix given the agro climatic change in this quarter. Some impact was because of price increase in raw material. Demand softness was also there so these price increase, could not been passed on.

o In next quarter, this product mix cycle will not be there but pricing issue from china is concerned because there Chinese year is over by the end of Feb so things will again be normalised.

o On supply side there is a problem from China so all companies are trying to find the alternative raw material solution. Dependency of raw material which was 30-35 % has already come down to less than 20 %. In next 6-9 month it will further go down substantially.

What about demand side when company think that growth will come back to normal?

o Global scenario is certainly improving and today situation is much better compared to last year. The inventory level has gone down and this is clearly reflecting in many of these projects the demand is also coming back.

o Production Campaign is again starting, depression has come down. Company has done 14 % but yes company can do easily 20 % because business was there in hand. There were two Challenges

One is raw material supply from china.

o Whatever Company was expecting in Q4 will happen in Q1 FY19 . Situation is only improving in term of demand. Current order book is around 1.15 billion.

o Overall the Rabi season is expected good than last year.

Did company commercialised any new product in export market?

o Company has commercialised two new products and two products will be commercialised in Q4

What kind of growth company is expecting in export in FY19?

o It depends on raw material but company expecting growth is reasonably good.

Which segment saw incremental drop in lower EBITDA margin?

o It was mainly because of domestic area because product mix was not so good as expected as plan.

Will export growth come from internal molecules or new molecules?

o It will be from both because of slowdown of demand now market will revive and secondly new molecules are getting lots of enquiry and that enquiry are converted into business.

What CAPEX company has done this year?

o It is 150-200 Cr in current year and it will be almost similar in next financial year.

Lot of conversion is coming to India from china so what is the opportunity for that?

o It will be a great opportunity as if any conversion or attraction come to India Company is ready for it because company have experience of more than 20 years. This issue in china is reflecting very good growth in Indian chemical industry. So company will become preferred partner for the molecule.

What would be company’s view on farm economy right now?

o Even if 50 % of what company is getting and budget speeches happen on ground then it will be a great opportunity for the farmers and the whole value chain. On side MSP will increase and on other side it will improve lot of efforts of productivity for the farmer. MSP will happen immediately in some crops.

Company dependency on china is 20 % so does it will impact company for further few quarters?

o This cannot be seen from this point of view. Say for example to make product A, A raw material was coming from China but now there is issue there so whole A product get stuck. That is what company is trying to solve from last 6-8 month. In one-two quarter that little dependency will also get over.

Kindly give breakup of revenue from domestic and export market for 9 month and this quarter?

o In Q3 Domestic revenue was 170 Cr and Export revenue was 360 Cr.

o For Nine Month Domestic revenue was 680 Cr and Export revenue was 970 Cr.

Company is focused on Backward integration with CAPEX of 150-175 Cr next year so what opportunity company see to invest in and being an asset light business model will these types of CAPEX bring return ratio down?

o It depend on economic whether company is doing backward integration in-house or find a source in India to de-risking the leverage. If backward integration gives benefit to company financially then company will do it for sure. Company has already done backward integration in two product which give advantage financially and also to target new products. Once capacity set up then Indian intermediary will be company customer who was importing from other countries. Downstream product also comes from these intermediaries.

In a press release company has told that growth and demand will pick up back in next year FY19 so it will be First Half or second half of FY19?

o Again there are two face of it

First is global scenario that will change from First half of FY19 or calendar year.

Second is company have orders and business is there from current point only

What about domestic growth in volume in progressive state like Gujarat , Punjab, Madhya Pradesh where agrochemical is already in use ?

o If agrochemical condition remains healthy then yes company will perform very good in all these states. Because company is present in PAN India basis. Company has launch 5-6 product this year and there is big pipeline for the introduction of new products in next financial year and coming year.

In last quarter company was talking about 10 % growth in export market so is this look achievable or company want to revise it ?

o It looks difficult to achieve it company have business on hand and everything but achieving 10 % is really difficult today. Further clarification will be from next quarter.

How many products company is going to launch in next year?

o Most probably 2-3 products will be there out of which One will be for Kharif and one for Rabi.

In CSM business how much company have commercialised till date and what about pipeline?

o In these three quarters, company already commercialised two products. Two more products will be commercialised in next quarter. Going forward there will be significant pipeline in R&D and more than 30 odd projects and 4-5 must be in advance stage and will get commercialised in next year.

Name products name which recently launch and doing well?

o Wisma , Header ,Cover these product have done very well .

What efforts company is taking on Pharma and specialty chemical side?

o Yes company is taking many efforts in pharma and demand is there from last one year. Secondly there is dramatic change in outlook and valuation so it is little better. So company want to grow bit more on that side.

15 % growth will be there in next financial year?

o Company can’t comment on how much it will be but yes business is there, water reservoirs is also good compare to last year, there are many products in launch and some had already been launched . So all these factor give company confidence that FY19 will be good.

When the new product that company is going to launch will achieve their reasonable growth and contribute in revenue subsequently?

o For new product it take 3-4 year but yet there are some products that company had recently launched and they are contributing reasonable in revenue, they get a good size in 1-2 year only.

What would be the tax rate in FY18 and FY19?

o Tax rate expect to be around 22% for FY18 and will be similar for FY19.

In which segment company is going to launch new product. Kindly give in details?

o One of product will be in Wheat herbicides which is in the second season. One product also on rice segment and vegetable in insecticides.

Two new products which company launch recently are on which segment?

o Three product launched on Fungicide this year in rice segment. On herbicides company launch product name Hover Company has launch a plant nutrient this year.

There seems to be generic pricing pressure in Brazil and sales were down for full year for both Bayer & Dow Dupont. I am not sure they can bounce back & grow in this year. Rallis India Q3FY18 conf call also confirmed that there is Chinese competition in export market.

Thanks to wonderful work done by VP community, it was established that PI Ind. has significant relationship with Bayer. With proposed sale of some crop protection businesses to BASF, I am not sure if there will be impact on CSM side. Relative to market cap of Bayer, businesses that will be sold seem not so large in size.

Rallis India Q3FY18 conf call + PI Industries conf call mentioned about elevated RM prices in domestic market and imports from China. Although companies are trying to realign RM sourcing, margin might remain under pressure in the short term.

Punting or delaying of Pharma initiative. Working on pharma initiative and executing on it is something I was really looking forward to.

Disc - I have sold my entire position over last few days. I am absolutely negatively biased due to my selling & these views shall be taken with a pinch of salt. This is not a sell/buy recommendation.

[quote=“rupeshtatiya, post:1095, topic:227”]

Thanks to wonderful work done by VP community, it was established that PI Ind. has significant relationship with Bayer. With proposed sale of some crop protection businesses to BASF, I am not sure if there will be impact on CSM side. Relative to market cap of Bayer, businesses that will be sold seem not so large in size

[/quote

BASF will be acquiring seed business from Bayer hence no impact on the Agrochemical manufacturing contracts.

Most of the CSM contracts by nature have some raw material price volatility formula built in and at least in the CSM business which PI is doing for the innovative companies PI will be able to pass on this raw material price hike

This may not be relevant. I have been following PI industries for long and on the other hand, there is some interesting thing happening in the area where I live. (Pune)

People are getting more interested in chemical-free agricultural products and there are three extremely active groups in my area. They are zero budget natural farmers and customers. The activity is tremendous. Farmers in Pune district are being attracted to this farming style which emphasizes on no chemicals added to farms, using no modified seeds. Also, it is NOT organic farming. Even major farmers are turning towards this method and sooner it will be a major thing because of aggressive markets developing.

This farming style is created and promoted by Subhash Palekar. you can google and you-tube his videos and check that his camps are ever increasing.

I have been studying PI industries since last two weeks. Certain points have amazed me. I seek guidance of some expert on that.

1.Till annual report of FY.2015-16, company used to give bifurcation of Raw Material Imported and Procured Ingenuously, from FY.2016-17, that has been suddenly stopped. As far as I know that requirement comes from Sch.3 of Companies act,2013, and not from AS or IndAs, so switching to IndAs should not have bearing on that. The same is the case with Rallis but other Agrochem Cos. have reported the same bifurcation. Can somene tell me under what head now I can find the same bifurcation? Or have that bifurcation been removed altogether.

2. In sale of finished goods section previously company used to report under three broad heads, namely, “1.Speciality Chemical, 2.Agro Chemical and 3.Plant Growth Nutrients”, but from FY2016-17, they have switched them to “1.Active Ingredients and 2.Formulations”. Can someone help me regarding that?

3 I had been going through research report from motilal oswal on PI Ind. In that they have calculated the EBITDA margin for CSM business and Agrochem business, separately and according to them there was vast difference around 400 BPs in the EBITDA margin of both of the businesses. On the contrary, while going through one of the transcripts of recent concall by company where one of the analyst had asked question on the difference of margin of the two businesses and he was replied that company doesnt really treat both of the businesses separately, and more so margin of both of them is roughly equal. Now I am under great dilemma with regard to that. Who is right here, Does company want to keep that secret or its just Motilal People are bluffing to show their analysis more superior and fancy?

Commenting on the performance, Mr. Mayank Singhal - Managing Director & CEO, PI Industries Limited, said:

"FY18 has been a challenging year, where the muted growth delivered did not reflect the underlying potential of our business, brands and orders at hand. However, second-half onwards we have seen initial momentum in growth both in the domestic and export markets. The 5 new products that were launched in the domestic market during the year have all been well accepted by the farmers. We continue to invest towards a vibrant product portfolio covering a broader crop profile. There is visible traction in the solutions centric approach we are taking to business, where we are engaging closely with the farmer community through digital initiatives. Similarly, with the aid of modern real-time technology, we are expanding our connects with the retailers and trade channels as well.

Under exports, we saw commercialization of 4 new molecules in the year. Over mid-to-longer term, we can derive comfort from the significant increase in both the enquiries and scale-up pipeline. Further, we are specifically targeting the development of new building blocks in adjacent and novel chemistries with a view to increasing the scope of export opportunity that we can gainfully target.

In line with our objective of both broadening and deepening our presence in domestic and exports market, we will continue to expand our footprints by leveraging our strengths and capabilities. Looking

ahead, the various initiatives undertaken by the Government together with the pick up of demand in global markets are indicating a better performance trajectory in the upcoming years.

Outlook

A focused approach to drive an innovator-centric portfolio will be the key enabler for growth. We expect domestic revenues to grow on the strength of expected normal monsoon, various Government initiatives and realization of the potential of new and recently introduced products. The domestic market will witness 4-5 new launches in the coming year. In exports, we are expecting volume scale-up in the existing molecules, whereas we intend to commercialize 4-5 new molecules. The plan is also to develop and commercialize new chemistries as part of building new blocks in novel technologies. Whereas our efforts towards pursuing R&D continue to build solutions and expand our offering to the global innovators, our continued investments in capacity expansion in exports are expected to bring fruits in the mid-to-longer term.

This means management guidance of a single digit growth in sales for the year not achieved.

I remember in last concall they had still guided for a single digit growth for the whole year…which was to imply a 25-30% growth in Q4…and sales growth was just 3% in Q4…

Company had introduced 5 new molecules in Domestic market and 4 new molecules in export market

Company had doubled its R&D cost in compare to last year

Company had scale up its product capacity Financials

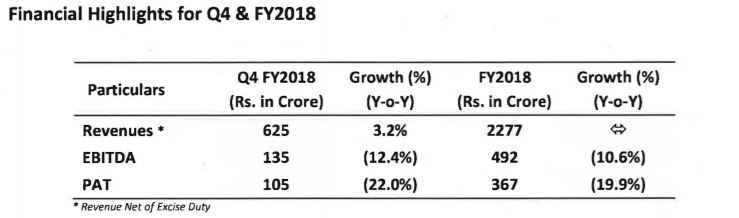

Q4 FY18

o Revenue grew by 4.2 % to 625 Cr compare to last year same quarter

o Revenue growth driven by 10.4 % increase in domestic business and 0.4 % increase in export business

o EBITDA stands at 135 Cr with product mix and high cost of raw material

o EBITDA margin stood at 21.5 %

o PAT stands at 105 Cr , due to higher effective tax rate

FY18

o Revenue stands at 2277 Cr flat compare to last year

o Revenue from domestic business was 822 Cr lower 1.9 % compare to last year

o Revenue from Export business was 1455 Cr higher ny 1.2 % compare to last year

o First half of the year was affected due to soften demand

o EBITIDA stands at 492 Cr

o EBITDA margin stands at 21.6 %

o PAT for the year stands at 367 Cr

o Tax rate for the year was 22.9 %

o Total debt for the year stands at 83 Cr with Debt/Equity ratio of 0.02

o Cash balance for the year stands at 283 Cr

Q&A

Why was the shipment get delayed ?

o Due to logistics issue from the company side

Does demand is in increasing trend ?

o Yes in global market demand is increasing trend and it will reflect in order . Company see FY19 as a good recovery year for the company

What was the matter of raw material shortage from China ?

o It was a One-off kind of thing

If demand improve and raw material supply goes on softening then does margin expansion can be expected ?

o Yes it will if all goes normal

What kind of geographical mix of business ?

o 40-42 % comes from domestic revenue and rest comes from export which inclue Japan, Europe , U.S.

What was the quantum of inventory that got delayed in shipment ?

o Worth 70 Cr

What kind of growth company expecting going forward ?

o 18 % growth in both domestic and export market in FY19 and going forward

What about order book going forward ?

o It will remain same , incremental order will be generated

What are the total number of molecule that are commercially active ?

o 24-25 molecules are active and also a very large pipeline is there in R&D . All molecules have different scale which were launch earlier and in current year

What percentage of revenue comes from top 5 molecules ?

o About 70 % of revenue comes from top 5 molecules

If the guidance of 18 % of growth is on constant currency ?

o It is volume based because there is lot of volatility in currency prices

From where main drop in EBITDA came from ?

o Revenue has been flat but investment in R&D increase for long term as lot of new molecules has been introduced so promotion is in place . Investing is going on in people , expansion program and it will continue to mid to long term

Can growth be above of 18 % ?

o It depend on capacity and company is investing a lot on it in current year in terms of debottlenecking and opening new plant . Company see robust growth in coming future

Is the launch of new molecules are first time in the industry or regular molecules ?

o It is mix of both

What CAPEX company had done in FY18 and planning to do in FY19 ?

o Company had done CAPEX of 170 Cr in FY18 and planning for 225-250 Cr in next year . CAPEX is majorly for export business

How does rupee depreciation impact ?

o It is positive for export business but same time the company become more competitive to others .

o In domestic it impact negative to increase price of import of raw material.

From launch of new molecules does any on them will be big ?

o Yes very much . It will be used in couple of herbicides and fungicides.

What are the component of other income ?

o Interest Income , Earned income on Cash.

Is there any plan of opening new plant in FY19 ?

o Yes company is planning for opening two new plants in FY19 which will be multi product . Both will be commission by end of December-January FY19 .

Is current gross margin will be sustainable ?

o Yes.

What will be the total number of molecules after commissioning the newer one ?

o Total will be 30-35 which will be proprietor patent . This is year there was 70 products in R&D . Majority of them will be on agrochemical side , One in pharma other in electrical chemical.

Will the growth will differ in first half and second half of FY19 ?

o Yes it will because in second half company will have 2 more plants commissioned so capacity will increase and order book also.

Current investment of new plant will be in existing plot or any other areas ?

o Yes currently new plant will be commissioned in same plot. Further in FY20 the expansion will be done in another plots.

What about supply of raw material issue going forward ?

o Company had solved it by developing 6-7 alternative vendors India . Company is focused on time bound method on developing Indian manufacturers and suppliers for all these critical raw material company is importing from China.

o Company is also diversifying geography in China to get sourced from alternatives

When will company again grow like it was till 2016-17 going forward ?

o There are some external factors that are affecting the company growth but in FY19-20 these all issues will get solved and company will get back on track

What was the R&D expense in FY18 ?

o About 60-65 Cr and it is doubled in current year compare to last year

What is the tax rate going forward ?

o In FY 18-19 it will be 19-20 % and it will be stable going forward

Can it be assume that the new molecules on CSM side will not be in large volume ?

o Yes these will not be in significant volume, because their demand will take place in next 2-3 years. It is not necessary that all the new or existing molecules must be there in order book . They are in order book at initial stage to build capacity and demand not in Mature stage

Does company will not get affected for 3-4 quarters if any issue come China side?

o Yes company will be comfortable , because company is developing alternatives and that is part of company plan . Company is expecting a smooth supply season

What percentage of raw material source from China ?

o Currently it will be 16-17 % of total raw material . In last couple of years this percentage has been significantly reduce it was more then 30-35 % previously. So company is not dependent on China

What percentage of products on which company is vertically integrated and what percentage does company buy from outside like technical ?

o Company business model is based on partnership where company bring products from innovators and then do unique formulations and then distributing it under branding . So company is more on value creator partnership side rather then vertically integrated

How would the regulatory change of import of molecule will affect the company ?

o It is not on manufacturing raw materials

Is the growth in CSM business is coming from existing molecules or new molecules ?

o It is coming from both existing as well as new molecule that company is commercialising

From company guidance of growth of 18-19 % what percentage will come from newer molecule ?

o 8-9 % , Two things to consider

Molecules launch last year they are well accepted and they will also grow

Newer Molecules will also grow supported by better monsoon

What would be the export in ratio in first half and second half , would it be 45:55 ?

o It would be around 40 : 60

What were the revenue contribution from domestic and export business in Q4 FY 18 ?

o It was 187 Cr from domestic business and 130 Cr from export business

What qualitative change does company see in last few years ?

o Ye lot of changes are happening

Customer Base is increasing

Getting more inquiries from existing customers and also from new customers

Most of the opportunity which was handle by innovators are also now coming to company

Lot of new technologies are also being developed . Company has developed two technologies which are for the first time in the world and very successful commercialised in terms of capabilities

Issues which are getting in China led Innovators to source products from alternatives so those queries are also coming to companies

Is the scale of contracts are getting big as going forward ?

o Yes there are certain place where the contracts are sizeable and there are some molecules where going forward the contracts will become sizeable

Company had plan of manufacturing sodium , how is that plan going on ?

o That is progressing well company had already applied for registration that will be done soon in a quarter

What are the duration of a molecules ?

o It depend on their demand . One molecule can exist for 100 years also . Normally it range from 20-30 years

Does the CAPEX cost include registration of molecules ?

o No it is a pure infrastructure CAPEX. Registration cost is also not significant

How is the current price trend on raw material front and how company see it in future to passed on ?

o It is uptrend prices are increasing although they are expected to be normalise . This situation had been faced by company every year . To settle it in domestic market a lot will depend on scenario of geopolitical , monsoon , and how season pans out and the competing scenario also exist .

Company’s revenue from operations for the year stood at Rs. 2308.71 crores, reflecting a decrease of 3.11 % on YOY basis. The operating profit for the year stood at Rs. 492.06 crores from Rs. 550.53 crores last year i.e. a decrease of 10.62 % YoY. The net profit for the year on stand-alone basis stood at Rs. 366.54 crores as compared to Rs. 457.36 crores in the previous year i.e. a decline of 19.86% on YOY basis which was mainly on account of higher effective tax rate of 20.9% as compared to last year because of certain withdrawal of abatement that your company availed n previous year. Our EBIDTA margin decreased 179 basis points to 21.31% in 2017-18 over 2016-17 and PAT margin stood at 332 basis points to 15.88% in 2017-18 over 2016-17.

Capex during the year was Rs. 169.58 cr.

R&D Exp of Rs.82.04 cr (3.5% of sales) in FY18.

Revenue: API = Rs. 1468.69 cr (Rs. 1472.03 cr in FY17) 64% of sales, Formulation = Rs. 828.58 cr (Rs. 903.23 cr in FY17) 36% of sales.

Revenue: India = Rs. 853.40 cr (Rs. 944.44 cr). Asia = 868.27 (Rs. 700.27 cr), North America = Rs. 319.08 (Rs. 540.64 cr), Europe = Rs. 191.08 cr (Rs. 126.79 cr), ROW = Rs. 76.86 cr. (Rs. 42.91 cr.). Export sales = 63%, Domestic = 37%.

3 formulations facility and 8 multi product plants at 3 manufacturing locations of company.

The manufacturing facilities include 5 multi-purpose plants at Panoli and, 3 multi-purpose plants at Jambusar. 2 formulation plants at Panoli help us meet the requirements of our local as well as global clientele.

R&D unit at Udaipur with 300+ scientists including more than 80 doctorates.

Our joint venture with Kumiai to manufacture and distribute Bi-spyribac Sodium in India and possibly beyond at a later stage. In this joint- venture, PI subsidiary namely PI Life Science Research Ltd., holds 50% equity and remaining 50% share is held by Kumiai Chemical Industry Co. Ltd., Japan. This joint venture shall help PI to bring superior innovative solutions in India to enhance farm productivity and also leverage manufacturing efficiencies of India under “Make in India” initiative”.

During the year, we launched 5 new Products , Header (fungicide), Fender (fungicide), Visma (fungicide), Humesol and Elite (herbicides).

Commercialized 4 new molecules during the year. We continued to strengthen our R&D prowess and initiated construction of two new plants. All these initiatives and hopefully a favourable operating environment shall enable us post a much improved performance in FY19 and beyond.

we are specifically targeting the development of new building blocks in adjacent and novel chemistries with a view to increasing the scope of export opportunity that we can gainfully target.

PI added 3 new co-marketing partners for Dinotefuran while achieving more than 100% growth in their own brand Osheen.

Despite facing fierce competition from generics Nominee Gold expanded its customer base.

The successful introduction of Humesol helped PI in increasing its presence in a rapidly growing bio stimulant market.

Your company’s exports grew marginally by 1.2 % during the year despite a slowdown in the global market situation and challenge in availability of raw material especially from China. In order to reduce its dependency on Chinese raw material suppliers, the company has developed 6-7 alternate vendors in India for 6-7 key raw materials that shall help the company in the coming years.

Lowering of crop prices, adverse climatic conditions in Brazil and many other Asian countries, higher channel inventories together resulted in the decline of expenditure on agrochemicals. As a result, the global agrochemical industry has remained flat or in fact has downsized a bit between CY2013 and CY2017.

Alongside these developments, the global agrochemical industry is dealing with the supply shock on back of the nationwide crackdown by the Ministry of Environmental Protection in China, one of the largest contributors to the global agrochemical Industry.

Initial indications of the slowdown cycle bottoming out are apparent, with strengthening of global commodity prices, drop in agrochemical exports from China, correction in exchange rate of Indian Rupee. Several agrochemical molecules, worth billions of dollars, are scheduled to go off-patent over the next couple of years, opening new opportunities for contract manufacturing and exports for the Indian companies

In domestic market, second consecutive year of good monsoon shall boost agrochemical demand.

Our focus in FY2019 will be on scaling up sales of new products launched during FY2018.

With considerable part of the target geographies yet to be tapped, our established products such as ‘Nominee Gold’ shall continue to drive growth.

Global crop protection market expected to grow at a CAGR of 4% over 2016-2020.

Based on FICCI, products worth US$2.9bn are expected to get off-patent by 2020 globally, providing significant export opportunities for India’s generic agrochemical companies.

Through our hub and spoke distribution model, we reach out to more than a million farmers. It consists of over 40000 retail points, more than 10,000 channel partners, over 2000 people, more than 30 countries across 6 continents, over 30 stock points, 8 plants, and 4 global offices.

Raw material prices increased, not able to fully pass on.

R&D expenditure increased.

New products commercialised which reduced the margins.

Domestic sales grew by 23% and exports remained flat, It’s difficult to pass on cost increase in domestic market.

China Impact

Last 6-9 months 5 factories were closed down in China, this scenario of closing factories for environmental reasons is likely to continue next year also.

To reduce the impact on our raw material supply chain we have started procuring material from alternative sources and also we have imported enough quantity and created buffer stock to negate the China problem in short to medium term.

2-3 years back we were doing more than 35% of our sourcing from China. Now it’s less than 18% of our total requirement.

China problem did not result in loss of revenue, in few cases deferment of sales (or delay) to next quarter may have happened.

Shutting down of units in China created a raw material problem but it is also beneficial to the Indian companies as customers are looking for reliable supply source in India. This has led to increased number of enquiries which is currently not reflecting in the order book. Keeping these increased enquiries we decided to increase capacity.

Capital Expenditure

Total Capex for FY19 will be around Rs. 250 cr.

Two plants to be commissioned by end of FY19.

Revenue potential after the capex is matured will be around 1.5-2 times of capex.

Capex in FY20 will be on same lines as in FY19.

Future Guidance

Sales growth projected for FY19 is 18-20%. Company is confident of this growth as the inventory levels in world agri industry are at very low levels and industry has started to rethink about this situation. Environment problems in China has resulted in clients coming to India for stable supply source.

Gross margins will increase, but EBITDA margins to remain at same level as last year.

New plants are in SEZ so tax benefit will be available.

Other Points

Order book at same levels at USD 1.1 billion.

Nominee Gold sales on expected lines. Despite competition from various generic products, volume increased during the quarter.

Other than rice we are doing good in cotton, vegetables and soybean.

In domestic market 1 new product was launched in Q1FY19.

In CSM segment we commercialised 1 product in Q1FY19, will be launching 2-3 more this year.

Formulation plant under Joint Venture with Kumiai Chemical is completed, waiting for registration to start commercial products. Kharif Season is main season and it’s already underway so this plant may contribute in Rabi Season (i.e. October-March).

IND AS 115 (financial reporting method) affected the reported sales and margin of the company this quarter.

My View:- Company gave guidance for growth in previous concalls also but that did not pan out as expected, will the company achieve the growth mentioned in this concall remains to be seen. As per the management commentary in concall IND AS 115 (new reporting guidelines) affected the reported numbers of the company and they claimed that the actual numbers were better than reported. Management explained the effect of IND AS 115 but I did not understand it fully as the voice quality of the call was a bit low. Would request other member who attended the concall if they can explain it.

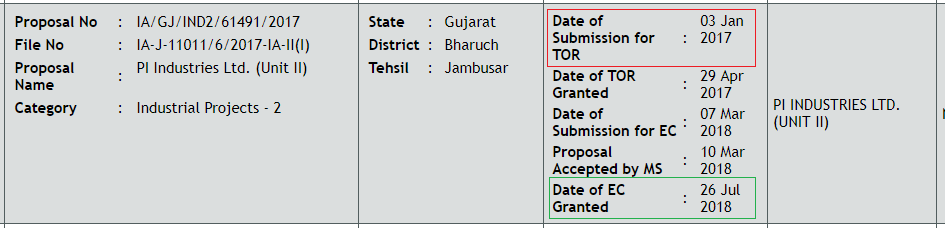

PI Industries has received environment clearance for new 43,240 MTPA capacity at Jambusar plant. Estimated project cost is 393 cr. This is after painstaking ~18 months long approval process. This project include fine chemicals, performance chemicals and specialty chemicals in addition to usual insecticides, herbicides, fungicides and their intermediates.

Seems road block is cleared for multi years of growth ahead.

PI Industries Ltd

Highlights of Q1 FY19

Financials

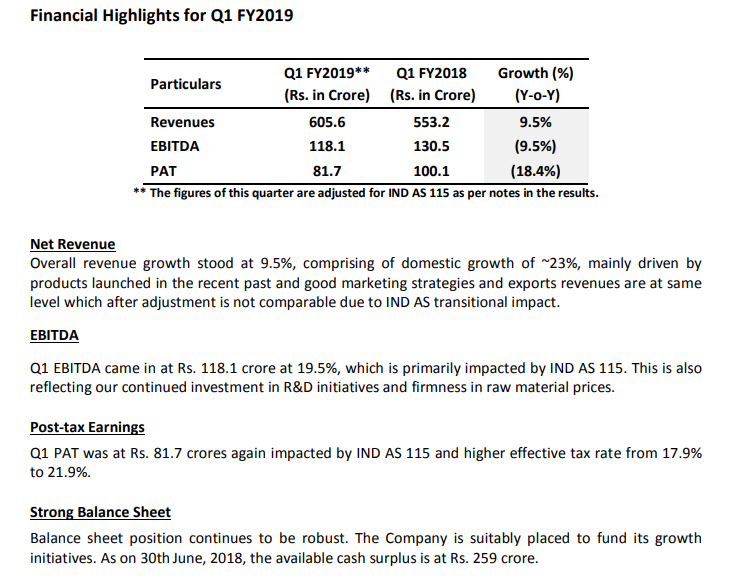

Domestic revenues grew by 23 % and similar kind of growth in production and export

EBITDA 118.1 Cr with EBITDA margin of 19.5 %

PBT stood lower at 18.7 Cr due to impact of IND-AS 115 as well as higher tax rate from 17.5 % to 21 .9 %. Primarily there was change in mix of tax free profit and taxable profit.

Cash surplus stood at 259 Cr for the quarter

Company is sitting at very good order from exports and there is a ramp up in production and de-bottlenecking the capacities for further ramp up production volumes dispatches which will reflect in the coming quarter and some capacity will also get added by the end of year .Company will commercialize three-four products this year.

Raw material price volatility remains challenge for the company and the suppliers while company was successful to get the raw material by developing new sources of raw material.

Company has adopted new accounting standard of IND-AS 115.

Q&A

Why there is decrease in export of 2 % in the quarter ?

o Last year there was adjustment of revenue recognition prevailing account standard and in current accounting standard the parameter are different from previous parameter . According to current IND-AS 115 the revenue which could have come to this quarter would have no recognized and some of the revenue push forward. So it is not comparable on like to like basis in a simplified manner that company is trying here. The next quarter will be line up with adjustments of IND-AS 115.

Where is company seeing the capacity constraint ?

o There is more than 25 % increase in manufacturing activity in operation and dispatches just because of the change in accounting standard it is not clearly reflecting but there is certainly ramp up over last 6-9 months and more ramp up company will see in coming quarter. Business is giving assurance of more than 20-25 percent growth which is already in hand so there is no capacity constraint

Kindly give more clarity on the raw material front which company is facing from china on two aspect supply and security and pricing aspect how will be the pressure in coming quarter ?

o Company is developing several other sources of raw material from India and other geographies to reduce dependency on china market. But some raw material which basic material remain in china so that will remain same . In China from last 6 month more than 500 factories has been closed down for various reasons like environment and safety and they came out with a statement that this effort will continue so there is some amount of uncertainty there in chemical industry but company have identified these kind of product where company is dependent on China and in that product company has already imported enough inventory or also clear some contingencies from other sources in these product rather than dependent on one geography and also having developed some sort of alternative in India so from short to mid term company have secured the raw material and at the same time continuing the effort to build the long term suppliers.

What was the order book for the quarter ?

o It remain the same as some supply happen in the quarter and to that extent company get new order of 1.1 Bn .

What is the duration of the execution of the 1.1 Bn order book ?

o On an average execution period is 3-5 years.

In CSN business is their any case where client is appointing the Chinese vendor directly for the product ?

o No

What drives the growth of 23 % in domestic market and on the gross margin side what has been the key issue that lead to such a gross drop ? Any pricing pressure on the nominee ?

o Domestic business driven by some of the key brands of the company that done well and give topline growth. Nominee is well in line what company had expected and company had perform better over last year. Great pushing and improving brand awareness in the market showing the growth. Nominee is a premium product and it is set in the consumer mindset and forwardly consistency will be very well establish. Actual EBITDA margin is 21.8 % after adding the adjustments and for this quarter also it is more than 20-20.5 % and company is going to invest in margins improving investment to grow in margins that will continue to hold on. Company is going to invest in R&D and recruit people at high level for better results in next couple of years. Company is also launching new products in domestic as well as export which will improve profitability.

What is the maximum length of contracts ?

o Generally they are from 5-7 years.

What will be the use of new technology adopted by company ?

o This is one of the key building block and it will commercialize in Delhi NCR which will de-risk of some of the molecules in existing products as well as open new opportunity going ahead.

What led to increase in capacity by adding new plants ?

o Company is having low capacity in respect of opportunity and the 2 plants which were added 2 years ago are also running at 90-95 % capacity utilization . Other capacity which is coming is in considering with kind of pipeline company have also company existing commercialized product upward and getting impression from own customer so company is backed for building these capacities . Seeing the global situation and interest of Global innovators to build more source in India they aggressively need investment .

Is there any plant dedicated or multiple plant ?

o All are multiple plant and some of them may work as dedicated if there are volumes to run them throughout the year.

What will be the impact of volatility of commodity prices going forward ?

o There is a good demand scenario from global customer of company . There has been a vast change in demand from what company was seeing a year ago . There is lot of disruption in the supply side and commodity prices. With this disruption the company is consolidating and there is already a challenge in supply in quantities. Company is definitely focus in working with new generation products in order to ensure the higher EBIT margins. Company has been very well in terms of innovative products. On the other hand the Chinese supply is also getting disruption which is giving an opportunity. So company is completely focus on more value added play in commodity market. So company is seeing demand with a mix of many issues from long term perspective not mid term perspective.

What growth can be expected in CSM business for the financial year ?

o 18-20 %

What is the 75 Mn that is adjusted in PBT ?

o This is the timing gap which will get clear till next quarter and also due to production process as there is so many changes. Things are not comparable between last quarter and this quarter. Nothing has impacted the company. It was part of the 260 Mn.

Is the decrease in the margin business is largely in the raw material cost because of increase in raw material prices ?

o This was in both areas in export product and import products because of following reasons

• Raw material price increase of which company was not able to pass on fully.

• There is lot of development with lot of new product got commercialized in both the area domestic and manufacturing area where there is development cost.

• Continuous Investment on R&D

o So margin conclusion is on both business

How much company is investing in the plants coming in this year at jamusar ?

o Company is doing 100 Cr investment in NCP-8 and almost 100 Cr in NCP-9 so around 250 Cr of investment as there are other utilities and areas also that require investments. At maturity company will be able to generate 1.5-2 multiple of Investment.

Why is the revenue difference come in company result as company always recognize the result after selling goods and How it will affect in next 5 months ?

o Because new accounting standard recognize revenue when product is in control with customer not when it is ready . Earlier revenue is recognized when company transit and deliver the product to the customer so that the reason some of the revenue doesn’t get recognized now in the new standard it is basis on control where there are certain criteria where is the customer and manufacturer intention get meet then when the product come into inventory its revenue get recognized whether it has dispatched or received the deliver so this is the basic difference. So for the product which meet these criteria the revenue get recognized immediately but if the product does not meet the criteria of exclusivity or long term contract so now there will be the existing method continue .So about 65-70 % of revenue comes from long term and 25-30 % from One year contract so in these contract revenue recognition is done after delivery of products.

Which geographies company is looking for as alternative to China ?

o Some of Countries like Vietnam ,Indonesia , Malaysia have grown very well in chemicals and some of the Chinese companies has invested in these geography to build alternative . Chinese situation has also helped European companies to again to do well because of the uncertainty in China so many European companies has revive so lot of these which were earlier coming from China are also available in Europe. Other major areas is India that has also get benefits to lot of products and also benefited to India.

After China disruption now the cost of raw material will increase so did it will impact company margins going forward ?

o Over last 1-1.5 year the prices in China is also rising So the thing to consider is not price but more toward availability . On prices there is no significant difference between the Chinese cost and the Indian cost . If the revenue of scale will get up than the cost will also get sum up

o In term of company in export contract the price is completely pass on whether it is a short term or long term contract. So whenever order is taken if prices of raw material has been doubled than company price will also be doubled and for customer also it is going to be on new level or abnormal. So it will not impact much in mid-long term but in short term it will affect for one year type of product where change in price has to be shared with customer.

Which are the company key focus crop now with key new product launches ?

o Nominee contribution has not reduced , so many company has come in the business but company was able to maintain the volume. Company is reasonably good in cotton , vegetables, soya bean and other segment so these are several other sector than rice where company is doing well and focused on build from last 1 year is also focusing in these crops .

Did company is looking out for MNA opportunity ?

o Yes company is certainly looking out for MNA opportunity but at current moment there is nothing in advance stage

Company had seen very good sales in North America in 2018 so how it will continue be in 2019 ?

o Company have commercialized couple of products . Major target is going to be America only so that is the key driver and some of the existing products are doing very well in that market so there will be good growth in that particular continent .

What percentage of sourcing was coming from China and what is current situation in terms of raw material ?

o Earlier 2-3 years back it pertain to more than 35-40 % and today it is less than 18-20 %.

Does company has loss certain revenue due to low availability of raw material from China ?

o No there is no loss of revenue the only impact happen is delay by 1-2 month.

From longer time the order book is stable and not increasing so when can increase in order book can be reflected ?

o It reflect in two ways

• In pipeline that company is building from last 1-1.5 year. Due to China disruption lot of enquiry and lot of new product inquiries are flowing to the company and existing order were increasing so the process of scale up take place first even before one go into long term contracting . So due to new product inquiry the work in R&D for 20-25 products has gone up to 75-80 products almost more than doubled.

• Scale up the stage those numbers has also multiplied sharply over last one year and that gives visibility that what kind of production requirement company is seeing in next one year to two year and what is the capacity available and therefore one need to build up additional capacity. So that is the visibility not the order book because once the scale up happen then company will go into the long term negotiations in the long term agreement and company is in several discussion to tie up for long term and those will be reflecting in the order book today.

What is the launch pipeline for the new product that company is going to launch ?

o About 4 products that company is going to launch and one product was launched in the quarter and remaining waiting for the registration . Company has commercialized one product and going to commercialized 3 more products in the remaining 3 quarters.

When will be the JV for manufacturing Disperic Sodium will execute and does company is putting separate plan for JV ?

o JV is already in place and Plant will be formulation plant and now company is waiting for the registration clearance . If approval got on time then yes company will launch a product for coming Rabi season.

How big would be the agro crams market in size ?

o Overall crams outsourcing is quite sizeable it should be more than 7-8 Bn dollar.

Did the growth in the domestic and CSM business would be similar ?

o Yes and the Gross margin would be higher and EBITDA broadly lower.

Did the new plants have any tax benefits ?

o All investments are done in the SEZ only.

Domestic business had decreased by 18% in FY 18 Q1 . Now in Q1 19 , it has gone up by 23% . So it is not actual growth, it remains almost same as compared to FY 18.

Last year due to GST bottlenecks, domestic business went down and it has recovered in this year. So what happened to real growth. The company has launched new products, it seems that there’re no real big molecules.

Real picture would come in Q2 . Last year Q2 sales base is high as the material that was not supplied in Q1 (due to GST) was billed in Q2. So last year Q2 was exceptional and contained some carry forward sales of Q1. This year Q2 does not have that advantage. Let’s hope the new molecule launches give some traction. Also Nominee Gold prices have further crashed this year.

a) EBIDTA of HI remains same as of last year’s H1 ,this is despite 32% increase in export. Export always give better margins. So can we assume that total profit from domestic business has decreased as compared to last year ( as domestic business growth is 24%)?

b) Let’s also keep in consideration that prices of almost all the molecules have gone up (15-20%) due exchange rate issues, tight supplies from China etc, so would need to check what is real volume growth in domestic business or it is just value (price-increase) growth and that too at lower margins than last year!