It is sad to see some comments from senior members providing the worth of a share without a cogent rationale.

Moreover, it is unfortunate to see the aspersions on the ‘honestness’ of a promoter in the times where most managements trumpet above 40% growth and then deliver a dud while saying it’s a one off or some other reason. While I may be wrong but with the past track record of the promoter I have nothing concrete to believe the management is making fun of minority shareholders. Out of context may be, but if you were to listen to NRN’s commentary during Infy’s heydays, you would not have held onto the company for long. He was conservative but was growing at 40%. I’m not equating both the companies here though.

We need to understand how much commitment it takes to create wealth that PI Industries has created over the many years and during this long term wealth creation there will be times where the growth engine hits speed bumps and this is COMPLETELY natural and therefore should be expected. It is only during this period management differentiates itself from the rest of their ilk. The SAME problem but of different magnitude based on the sector specific issues was plaguing companies like Page. Strong managements come out successfully and during this period the returns will be below normal sometimes frustrating so because of opportunity cost while during this period the ‘hot’ sector of the season makes the merry.

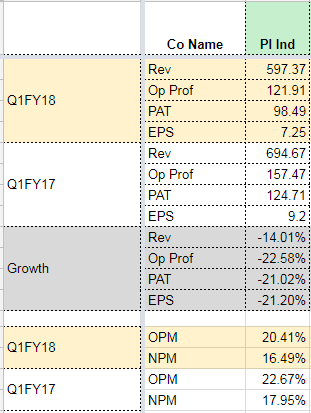

Now, coming to the PI Industries stock price per se, though last year’s EPS was ~ 33.5, I would like to consider it as 30 in order to account for the lower tax rate. I believe PI might end with 34 thereabouts for FY18E and FY19E should be around 40 with global agri-chemicals sector turning around along with the domestic business uptick + the CAPEX contributing to the revenues by FY 19 + possibility of new areas fructifying by then and contributing small share to the EPS. So PI would be a 15% EPS grower and add 1% for dividend yield.

So, what PE would I attribute to PI? (now, this is more subjective part of the analysis).

-

16 times FY18E EPS is straight forward answer to make it PEG=1. (I don’t believe in this PEG stuff much, though).

-

I personally would give a premium valuation based on the below points -

- No or little debt

- Superb return ratios (RoCE and RoE)

- More than 6-7 decades of history, promoter integrity

- Capex based on internal accruals

- Marquee partnerships with global names like BASF etc. and revenue visibility in CSM

- Long runway of agriculture yields improvement story in India where PI has an important role to play.

-

While the pricing pressure in its Nominee gold product which forms 20% of the revenue might be a risk, but given PI’s history it has the ability of bringing new molecules to compensate for the business loss but there might be delays in the interim.

-

USD INR rate inching 63 is going to risk the exports revenue, no? I have not read if PI has any forex hedging policy or not to nullify this as this is secondary to the business.

Now, carefully weigh the risks vs. rewards and give a valuation you are comfortable with while taking into account the opportunity cost of investing in hot sectors and how much heart burn you might have? With respect to this point, PORTFOLIO ALLOCATION comes into picture. I certainly have exposure to NBFCs but I cannot have 100% allocation to NBFCs and metals, right? In this context, companies like PI deserve an allocation that is commensurate with your risk profile.

Disclosure: I hold PI in my portfolio and I may sell for reasons that may or may not be stated above as and when my opinion and facts change and my perception to those facts.