When ever I have invested in Gruh, it has been overvalued compared to other HFC’s. As I observed the stock over a long period of time I realized that it doesn’t come down drastically during market crash. So I started parking funds in it when the market is overvalued. This is possible only because of it’s consistent performance over a long period of time. So far over a period of 5 years it has given me an IRR of 42% when corresponding sensex has returned 8.6%(equitymaster). It is a 20% kind of compounder. When it goes below that we have to be cautious.

4 Likes

I think Hitesh’s point is very valid. In the on going bull run, investors want to make a quick buck. And, with PI management making a remark of soft H1 result, people are likely exiting PI in a hurry for greener pastures (or flavor of the day, IPO!!) Definitely time to reassess some of these high quality businesses and if one’s investment rationale remains intact, one should buy such stocks (of course with adequate MoS)!

Disc: invested

1 Like

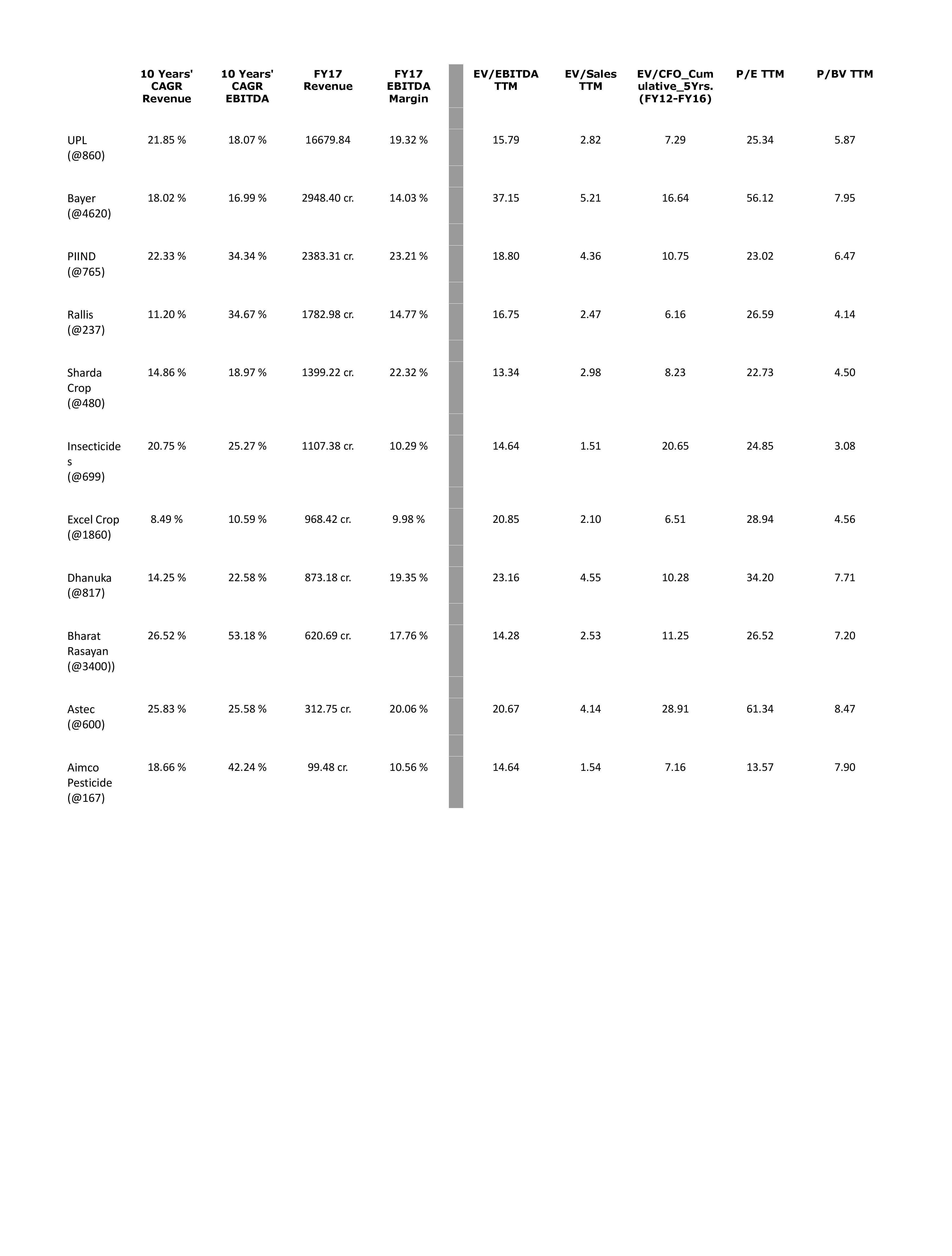

PIIND has (thanks to the price correction it has witnessed recently) reached an interesting point right now wherein markets seem to be discounting the worst despite its consistently superior past financial performance v/s all its peers. If we refer the data provided in above table of almost all the listed agrochemical players of India, PIIND has exhibited a relatively great consistency in revenue growth performance with an extreme focus on profitability v/s all its peers. A decade is not a short time-span indeed.

Today, if we take consolidated financials into consideration, PIIND is the third largest player in the listed space operating at highest EBITDA margin. And, not only this, PIIND has exhibited one of the best OCF to EBITDA conversion ratios amongst all peers and its ‘Cumulative OCF generation as % of Size of Operations in FY07’ is second best amongst all listed peers (almost twice of each one).

So, the question arises (as is raised in this forum) asto why despite such a superior performance history, PIIND is losing its mojo when almost all its listed peers are finding increasing attention of long term investors/fund managers and their share price is appreciating (or at worst remaining stagnant) v/s depreciating share price of PIIND ?? Infact, because of this contradictory trend, players like Insecticides India & Bharat Rasayan have narrowed valuation multiples gap with PIIND despite their weak business model as also weak cash generation and balance sheet management history. Bharat Rasayan has infact started trading at premium to PIIND if we take some valuation multiples into consideration while Dhanuka and Astec are trading at premium to PIIND on almost all valuation multiples. The answer to this contradictory trend could be that markets discount the future and not the past. So, does PIIND future look so bleak v/s its peers’ future ??

Here, if we take just one known aspect, i.e., Order-book of CSM segment into consideration (1 bn. USD) then also it gives revenue visibility of 55 % of current scale of operation for next 5 years. Forget here the tie-ups/JV route PIIND has taken for its domestic agri-input segment which could give great stability to domestic business over long run.

Management has guided for soft H1FY18 but, if we look at history of such companies which possess strong derisked business model like PIIND has and high pedigree management which PIIND possess then in such phases share prices of such companies go into stagnation rather than depreciation. They take time correction as opposed to price correction untill and unless there is some question mark on long term sustenance of their business model. With PIIND there doesn’t seem to be such risk (atleast visible to me). Hence, the current price correction (which is amplified by peers price performance as well as market performance) could be because of one of three reasons (as per my thinking) :

(1) There is some unknown coming,

(2) There is a big shareholder/group of big shareholders (like institutions) which have a big lot to sell and till that quantity gets absorbed prices will correct/remain subdued,

(3) There is some reasonable fund raising via stake sale is on cards which will be at lower than CMP so share price will find that level and remain there till the event is passed.

Rgds.

Discl. - Invested in PIIND and Adding

14 Likes

I think market’s concern is rightly justified given the valuation of PI. PI is also a kind of business where investors pay for stability. In such a scenario, a soft H1 might have come as a surprise to many and that is being priced in.

Bad news doesn’t come in one dose, it’s comes in installments. No management ever says that next couple of years are going to be bad. they lower the bar every quarter so that big investors get time to exit. PI could very well start posting good numbers in couple of quarters as expected but bad things have a tendency to turn ugly before it is all done.

1 Like

Could you expand on this pls? On what basis do you make this comment and any examples you can quote for better learning?

Thanx

RR

Just my observation over last 15 years of investing experience. Take for example Divi’s. Last quarter they said impact of import ban will be only 5% on revenues. Now they reported a 20% drop in revenue and a 40% drop in profits for Q1. They are saying all is well. Who knows when is the next shoe is going to drop? Story has gotten from bad to worse.

2 Likes

Hi, i feel portfolio allocation is very important. More than 20% allocation to single stock poses a big risk. As mentioned by the seniors many times, they keep selling winning stocks if it crosses limits like 15 or 20% of PF and also to keep portfolio allocation correct. I learned my lessons in very hard way but now i follow rules and makes my portfolio balance intact. Though it may be off for some time but i will not allow my portfolio balance to be off at any cost. It is painful to sell your most trusted and profit making stock to sell but with my exp…i now believe it is still good to sell and give importance to PF allocation…others pls share your exp too…

2 Likes

Yes…there are many examples like this almost everywhere… mgmts go off mark all the time…but from this we cannot infer that they are “deliberately downplaying with the intention to help a big investor offload”. If you have no examples it’s fine…I was just keen to know how a management perceived as good/great can do such a thing. All the same, many cud be doing this but it’s tough to believe they would be seen by investors as good/great mgmts having built good/great businesses.

1 Like

Hi Saji

But now Gruh at 475 will not fetch any return for 1/1.5 years atleast. Moreover during sharp correction there could be a cut in price of about 15%-20% as noted from past trends.Not sure how you handle this.Same goes for HDFC Bank. Both go thru time correction as noted from the past.In 2012 I had to hold Gruh for 2 years without any movement before the bonus issue and sudden jump happened

The character of the stock also matters like individuals. PI is not a fast mover unlike some other stocks. Also operators are not interested in this stock. May be as someone said there may be something more which we do not know

I’m beginning to not be surprised any more about the underperformance of PIIND( past one year at least) , and why others are racing ahead. And I will not even pish posh this underperformance by saying that markets has its own whims and fancies. There is a reason why the Ajantas, Ceras, Kajarias, Finolex cables of the world( with fundamentally very sound past, but not so sound present, and also past few quarters have been terrible) are not performing and no point in envying why the Caplin points, Asian Granitos, Ram ratna wires, and Kei industries of the world have been simply outstanding. The answer is simple, the PIs and Kajarias have had a fantastic past, but the nos. especially Revenue growth has been dismal when compared to its own growth of 30+ in the past. Whereas the latter group of Caplin points, and Asian Granitos seems to be running on all cylinders ( for how long is anybody’s guess). But for now the markets are applauding this performance of uphill and outright rejecting slow growth.

1 Like

When you wrote that , " No management ever says that next couple of years are going to be bad", This generic statement does not fit in for a fine management like at PIIND. I believe the Singhals at PIIND have been realistic, they have never outplayed or downplayed anything. Their ONLY focus has been their business and not the stock price movements. There are such umpteen number of companies with shady, manipulative management, that is more interested in stock price than running the business, but that is not PIIND management. If you have any connection with Udaipur you will know what I’m talking about. I may have not made any money in PIIND, but management accusation will NEVER be on my mind.

2 Likes

@Peabody It is true that the stocks go through time correction and Gruh is no exception. I do systematic investments and withdrawals depending upon the market situation. When the market is getting heated up I do SIP into Gruh/HDFC bank and when opportunities are available all around I withdraw from it and deploy elsewhere. I don’t allow the portfolio allocation to go below 3% so that I will get the benefit of averaging when I invest later. I will wait for the time correction to happen. In any case if you look at weekly/monthly charts of Gruh/HDFC bk they are more or less smooth curves. So far it has worked for me. I find it very difficult to keep cash.

5 Likes

Mutual Funds Increasing their stake

3 Likes

then who are selling ?

Although this data is irrelevant in the investment case of PI, according to June SHP, FPIs have reduced their holdings and MFs have increased.

“PI is in final stage of duediligence to acquire a Pharma CSM asset in intermediates segment” says a visit note by Axisdirect PI Industries - Visit Note - Axis Direct.pdf (593.7 KB) Is this the reason for the recent market reaction?

3 Likes

May be. Most of pharma companies trade at lower PE than PI.

By ‘recent market reaction’ you mean the downfall in stock price? If so then, it’s not recent, it’s gradual and slow since six months, and only got aggravated after March qrt.

If it is ( pharma CSM asset acquisition), so negative then why MFs have increased their holdings in June qtr , when compared to March quarter, I wonder.

I can anticipate only two assumptions now. A. On the positive note , MFs have been increasing stake and thus maintaining the stock price at lower levels till they are finished with their buying, as retail investors are the most vulnerable ones, who catipulate very easily, and the also the number of floating shares are not massive like ITC, so all this is possible too.

B. Like Mahesh pointed out, something unknown, may be out shortly.

At this stage, for me, it’s no longer no profit no loss, it is loss in pi for me, but I want to wait for 12th August and then decide. If 'June 'qtr is not good, it’s not good, not good at all.