Provided below are some statistics for members’ reference :

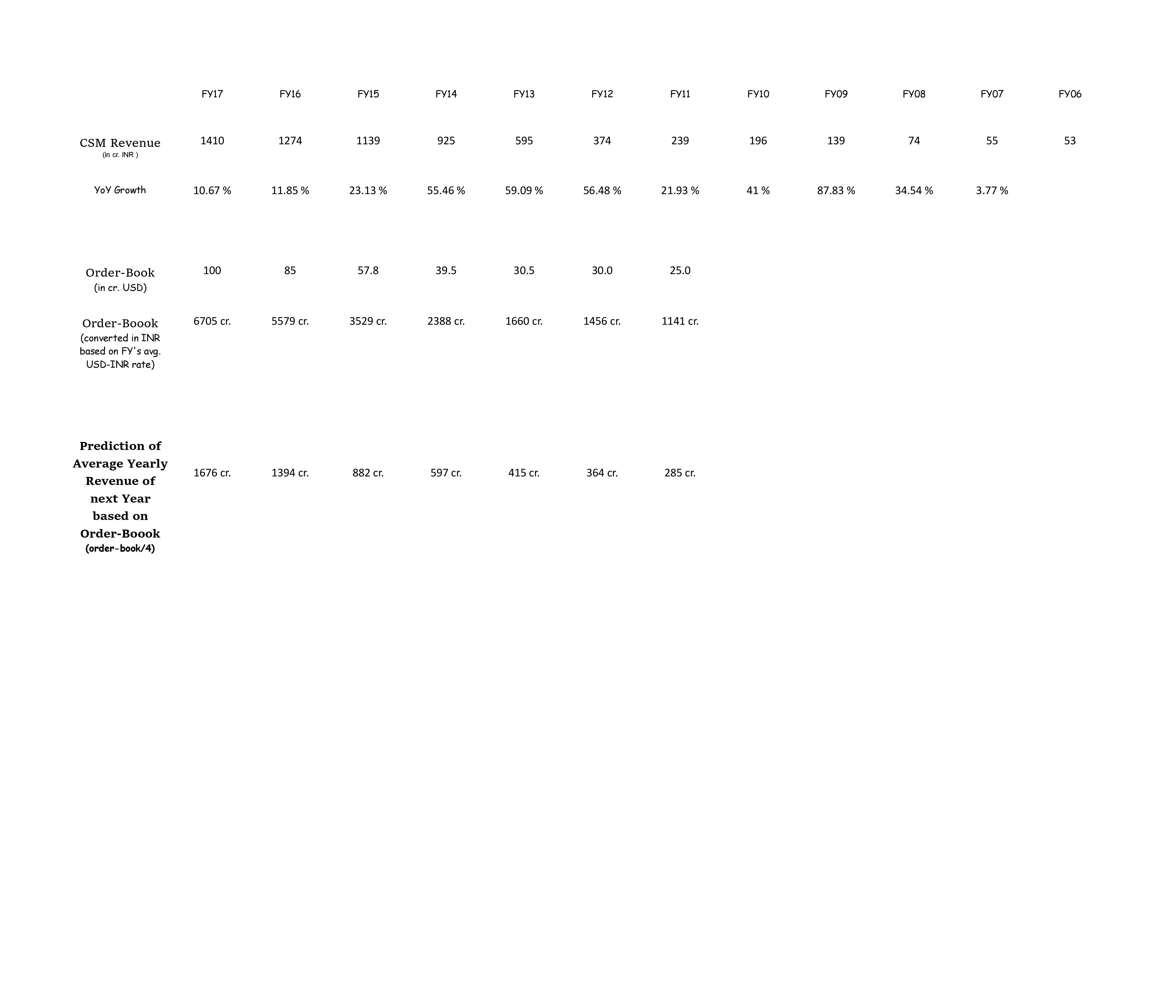

PIIND CSM Segment last 12 Years’ Analysis :

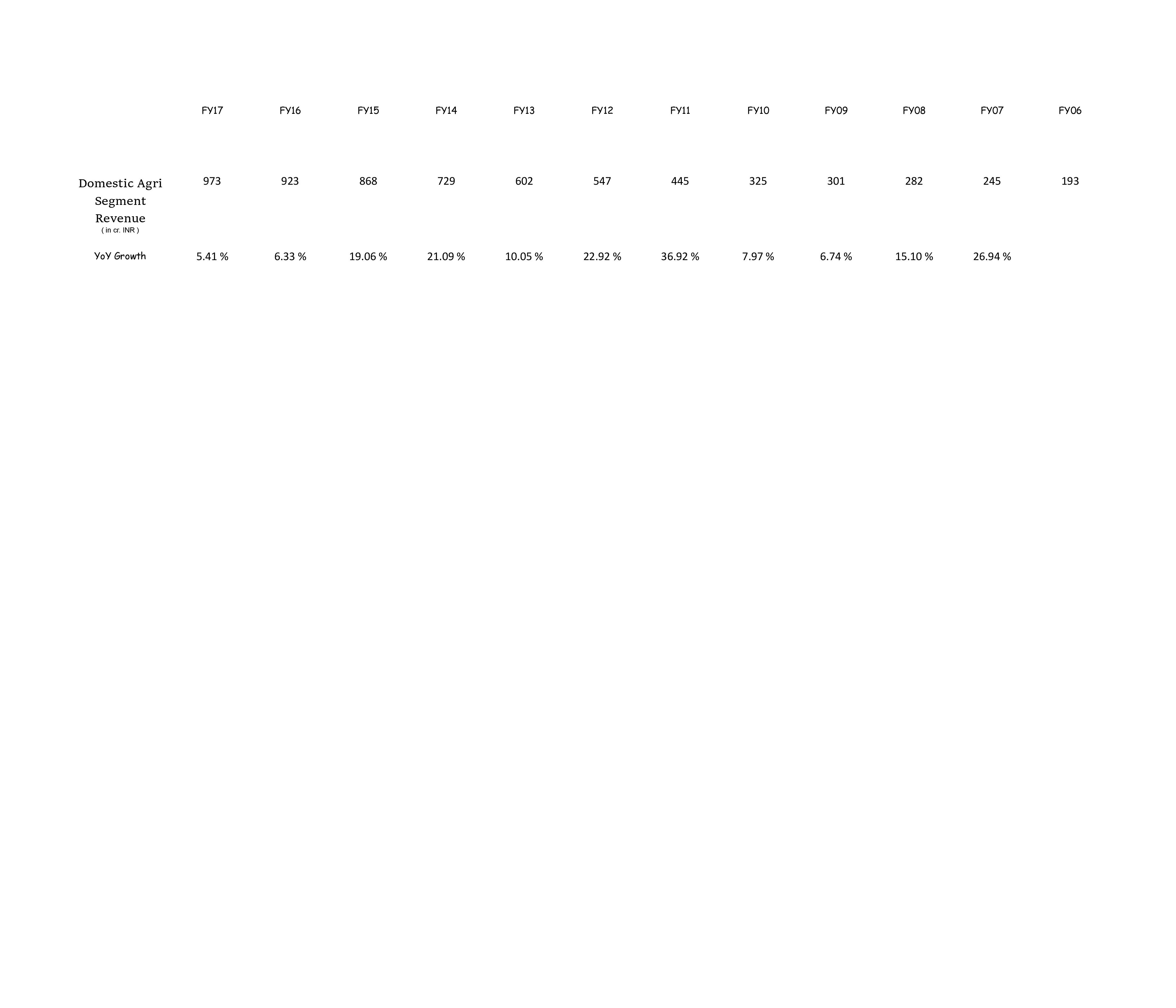

PIIND Domestic Agri Segment last 12 Years’ Analysis (past data adjusted for IndAS) :

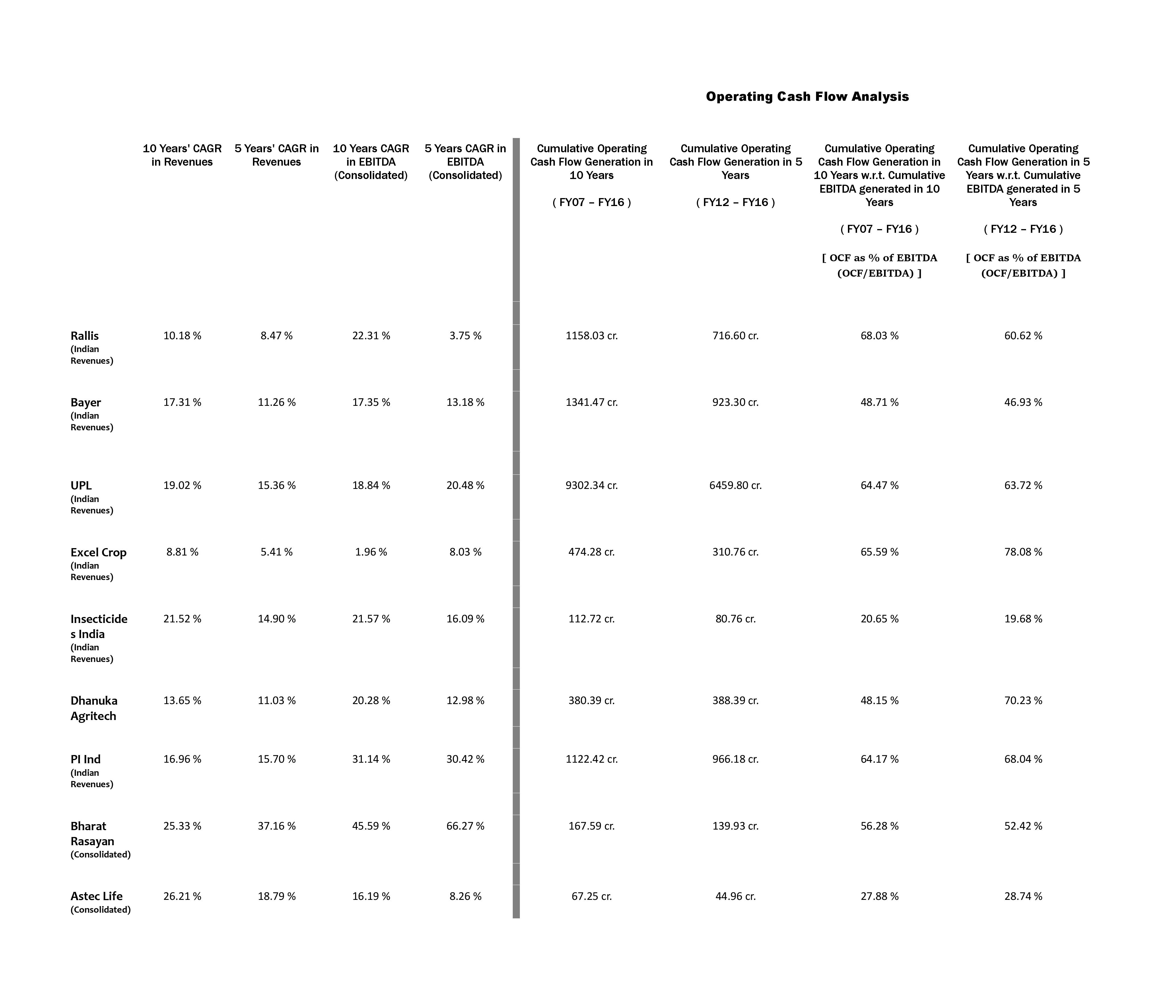

Last 10 Years’ as well as 5 Years’ Revenue & EBITDA CAGR analysis as well as OCF Analysis of all listed Agrochemical companies :

**Now, there are three main concerns with regards to PIIND atpresent : **

(1) PIIND Domestic Agri segment has grown in single digits since last two years and it is underperforming peers.

(2) Nominee Gold has lost its exclusivity and its realisations could suffer going forward.

(3) CSM segment is showing muted growth since last two years.

Regarding first concern, we need to understand the segment and its operation itself to judge whether this concern holds ground. In domestic agri segment, key is your reach and your ground network. Second most important aspect is your product selection. Third aspect is your marketing and distribution strategies. Now, even if a company is strong in all, still, you will find in some years its peers outperforming and in others the company outperforming its peers.

This is because in one or few particular year(s), some factors are more favorable to products and reach of a particular company than others. What we need to check is whether a company is consistently underperforming its peers. If this is the case we need to assume that there is some structural issue with the company and company is on verge of losing its marketshare considerably.

If we look at the factual data posted above, we find that whereas PIIND has slightly underperformed some peers on 10 Years’ CAGR basis, if we look at last 5 Years’ CAGR, company is the fastest growing entity. Here, we need to exclude Bharat Rasayan and Astec Life as both of these players are majorly B2B players and if we want to compare their revenue CAGR then we need to compare it with PIIND CSM segment revenue CAGR which stands at 38.32 % for 10 Years and 30.39 % for 5 Years.

Regarding second concern, yes. This is a valid concern as Nominee contributes ~250 cr. to PIIND revenues. However, here, if only realisations are going to suffer with its reach remaining intact, then, that can be compensated by other products but, if competitors completely eat up Nominee’s marketshare then there could be a problem. PIIND management doesn’t seem to be fool enough to let the competition do this easily as in any case, if its only price differentiation on which competitors are playing on then that can be very well matched by PIIND. Only time can tell how the things will unfold but logically, at worst there could be a cut of maximum 70-80 cr. to the topline because of this that’s what my study makes me believe.

Regarding third concern, we are looking at 10-11 % p.a. growth of CSM segment in last two years but are not looking at one critical aspect i.e. order-book. Why clients booked orders even when they were under pressure and globally industry was suffering ?? If one looks closely at the data posted above, one will find that for no fiscal uptill now, PIIND CSM segment has missed posting revenues which are derived based on dividing order–book by 4 years (the average tenure of execution of order-book). Based on this, FY18e CSM segment revenue comes to 1676 cr. v/s 1550 cr. as guided by management. Let’s see what happens.

Company has 20 commercialised molecules and 25 molecules in R&D pipeline. If revival comes as expected, what happens is there is increased offtake of commercialised molecules and such increase is not covered in order-book but is normally booked under fresh annual contracts. In addition, company plans to commercialise 2 molecules in FY18 too. So, what happens is the size of order-book provides stability in the form of muted growth in bad times and in good times, aggressive growth could also revive quickly (not at a historical pace ofcourse because of higher base).

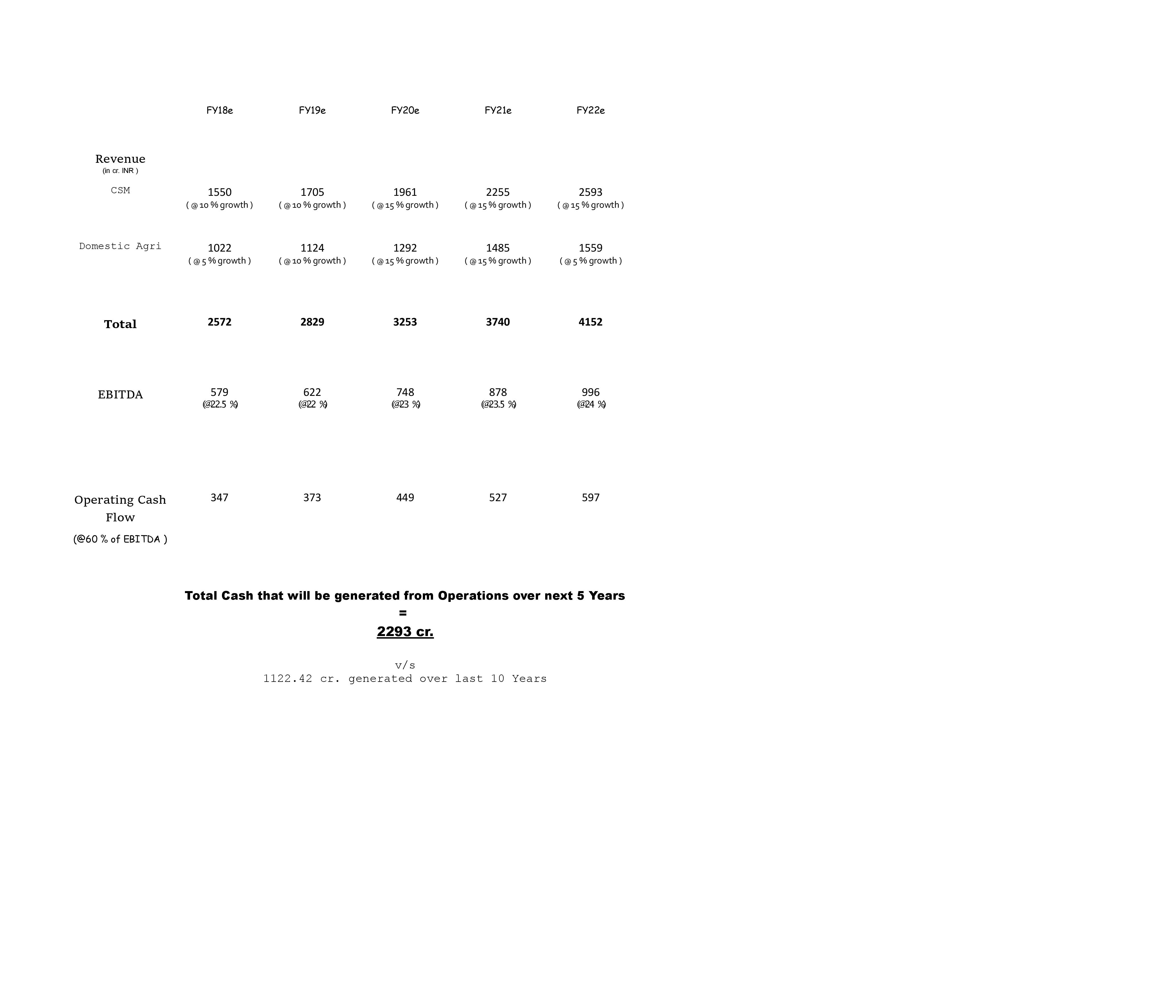

Last critical aspect we all seem to be ignoring is cash generation that is likely to happen over coming years that could be used to fuel aggressive growth even on current higher base. Again, refer to ‘Operating Cash Flow’ analysis data posted above. Company has converted 64.17 % of EBITDA generated over last 10 years to operating cash which increases to 68.04 % of EBITDA if we consider only last 5 years. Now, if we remain conservative and assume a 60 % EBITDA to Operating Cash generation over next 5 years then also the company will be generating 2293 cr. cash which is almost equivalent to current topline of the company.

What I did is a simple rough work of coming 5 years financials based on following assumptions :

(1) A 10 % p.a. topline growth for next two years in CSM segment which will increase to 15 % p.a. growth for 3 years after.

(2) A 5 % growth in domestic agri segment in FY18 considering the fact that competition will heat up for Nominee as also products from BASF tie-up will be launched. A 10 % growth in FY19 and 15 % p.a. growth for FY20 and FY21 as newly launched products will gain traction by then. Assumed again a muted 5 % growth in last FY22 to factor-in any deviation in between.

(3) We have assumed reduction in EBITDA margin (as opposed to management guidance of stable margin) to 22.5 % in FY18 and a further reduction to 22 % in FY19 to factor-in expenses related to aggressive product launch in tie-up with BASF (as per industry sources, one of the product to be launched via this tie-up is a very promising innovative product like Nominee and management will be going all out to create market for this product). From FY20 we have assumed slight expansion in EBITDA margin every year.

(4) We have assumed 60 % conversion of EBITDA to OCF v/s 64.17 % of 10 Years (FY07-FY16) and 68.04 % of 5 Years(FY12-FY16).

Last notable point is, over last 10 years, PIIND has done a CAPEX of 1056 cr. and generated incremental revenues at 1.74x CAPEX done. Also, last 10 years’ average Sales/GB has been 1.97x.

Rgds.

Discl. - Invested in PIIND

Note - These statistical data are only for study purpose and nothing else. One should not consider this as any recommendation of any kind. This is only part of a general discussion.