Predictors are not sure…heard predictions on both sides…here’s the latest one! https://www.bloombergquint.com/markets/2017/03/08/el-nino-seen-arriving-too-late-to-hurt-india-s-monsoon-rains

Hi, is there any official estimate of the size of global CSM/contract manufacturing opportunity, Do let me know in case there is any report that can help. Thanks

There are some times in a Business (we are invested in) that we get the sense that the business has crossed the “chasm” and reached the next level. Its extremely important (for those invested and tracking) to recognise and take advantage of these moments.

Such a moment was on us in Feb 2016, when PI Management “quietly” dropped a line - we have set up 2 dedicated plants at an investment of 150 Cr each, dedicated to 2 independent customer products. We all know - the trajectory of the business/market perception of performance since then in PI Industries. (thought this was irrefutable evidence that PI business had become much more stronger and crossed over to the next level, but was surprised to see none of my-invested/tracking friends paying attention).

I believe probably another such “moment” may again be visible to be detected in PI Industries business choices being made. So, here’s an attempt to ignite spark in those curious to think more/and thus find out more - whether PI business is again about to get much more robust?

Questions for PI Industries

Agri-Chem - Factors

Consistent Revenue growth ahead of industry growth - the secret sauce?

Consistent Market share gains over last 6-7 years?? - result of conscious choices made?

Distinctively unique Product segment choices - Nominee Gold (Rice herbicide FY16 210 Cr), Osheen (Rice Insecticide FY16 150 Cr), Biovita (FY16 100 Cr), Keefun (Insecticide cum fungicide for Vegetables FY17 70 Cr) and Vibrant (Rice insecticide FY16 30 Cr) - continue to drive ahead of the market growth? New brands like Vibrant & Keefun 100 Cr+ individual brands (potentially)?

New launch Vibrant (API – Thiocyclam) rice insecticide - uniqueness of the product - action on two common insects i.e., stem borers and leaf folder. Competing Fipronil and Rynapyxyr (Dupont) market size 60 Cr, and Fiprolin 25 Cr. Product can be extended to cotton and vegetable crops?

Upgraded version of Biovita (~ 60 Cr revenue size in FY15/16)?

Nominee Gold - currently 10% of rice acreage (42mn ha)? Potential target segment for Nominee ~30% of rice acreage?

Basmati Rice seeing good jump (up by Rs 400/100kg) in realisations - agrochemical use likely to be more robust

Increasing crop-based approach? Rice based Portfolio predominantly; Cotton, Fruits & vegetables ~ 12, 15% growths

Role of farmer engagement (farmer profiling) and better quality fruits & vegetables portfolio - as compared to Bayer?

Increasing scope for Herbicides 28% and Fungicides 23% - much lower adoption vs Insecticides 50%?

In-licensed products ~70% of domestic revenues? Can be maintained?

Top 5 products - 60-65% of PI’s domestic sales??

Role of Distribution Network ~29 branches/10,000 distributors/Centralised SAP and clear Distribution Policies

Schedule of 2 new innovative product launches every year - Visibility?

Distinctively unique Product segment - how robust is that development/under trials/test data pipeline - to continue to support crucial Business Model choices??

More than 70% of domestic agrichem market is generics? Continued scope for growth of innovatives?

Impact of Modi Crop Insurance/Soil Health Card schemes - on increased pest control usage

10-15% segment growth expectations over next 5 years? Or, higher?

CSM - Factors

Agrochem CSM market size US $5-6 Bn growing 5% annually - Addressable segment? PI Market share

Addressable Market expansion from non-agrichem presence - Fine Chemicals, Imaging, Electronic chemicals?? US $20 Bn

Positioning/Competitive Strategy vis-a-vis Saltigo? What about Lonza or SDM - these don’t look like direct competitors? Whom do you benchmark yourselves by for achieving a full-service CSM provider capabilities?

Long duration contract negotiations? Especially for large capex investments?

20 molecules under active production

Non-agrochem molecules pipeline? 30%??

Enquiry growth rates at current juncture - offering visibility for growth coming back?

Schedule of 2-3 new patented commercial molecules every year - visibility?

future capital expenditure- planned only against contracts which have either been signed or are being negotiated?

Orderbook/Revenue ratio - changes? Deliberate? $850 Mn orderbook >3yr visibility

Jambusar III 2 new dedicated plants to individual molecules - 300 Cr investment - Peak Asset Turns of 2.5x? - contract-manufacturing visibility of 7-10 years??

Revenue share from non-agrochem molecules (early stage pharma intermediates, imaging chemicals, electronic chemicals, etc) - upto 25% over the next 5 years?.

PCBM/Negolyte -13000 T??

Average revenue realisation for CSM molecules ~500/kg, but PCBM/Negolyte electronic chemicals much higher at 1000-1500/kg??

200 strong R&D - 120 Scientists

SONY JV finally producing results? Any Intellectual property (Patents) commercialisation benefits from there?

Increasing Product enquiries - led by China Increasing Cost pressures -20% escalation? Environmental issues in China too??

25-30% plus segment growth expectations in CSM over next 5 years?

Jambusar brownfield expansion space left? Out of 88000 sq mts

Why won’t the same happen in India?? Soon enough?

Knowledge/Execution services across Agrochem Value Chain

JV for Agrochemical registration in India with Mitsui? Why did it need a JV - big scale, exclusivity??

Why does it not cannibalise potential PI in-license introductions from Mitsui in Indian market?

Margin/Cash Flow Expansion - Factors

From 16% in FY10 to 22% in FY17 - both segment mix changes, and product mix changes within segment; also consistent margin improvements season on season

CSM seg enjoying 4-5% points higher margins than Domestic? Implies as CSM segment contrib keeps increasing, margins are set to trend higher up in coming years?

Share of hugely commercially successful products (2 new plants) scale up should provide further margin cushions?

Increasing Share of non agrichem CSM molecules in next 5 years will shore up margins by another 3-5%?

Working Capital cycle improvement? 90 days to 68 days Reasons? Further scope?

Operating Leverage at play from FY14 onwards - EBIT increasing by 1.5 to 2x for every Rupee increase in Sales? Looks to be sustained over net 2-3 years - over next 400 cr investment cycle??

Expected Incremental Fixed Capital investment rate - closer to 10 yr avg 40%??

Expected Incremental Working Capital investment rate - closer to 5 yr avg 16%??

Positive free Cash flow generation spiral to easily continue??

Subsidiary Roles - how much of a factor are they?

PI Japan - only marketing activities (agrichem)?

PI Life Sciences - only custom synthesis, no manufacturing?

Management - Factors

Introduction of 2nd level professional management

Expansion of Senior Management Talent/Bandwidth - focus?

Global Talent entry/exit on Board?

Risk - Factors

Margin erosion for largest brand Nominee Gold - generics challenge

In-licensing model under threat? - data exclusivity reduced to 3 years; and as Japanese/Other MNCs enter Indian market. Nihon acquiring Hyderabad Chemicals; IFFCO and Mitsubishi JV; Sumitomo-Excel Crop care acquisition (60% share; 45%+15% Nufam shares)? Insecticides India JV with OAT Agrico; Dhnuka with Nissan Chemical Industries

High inventory levels in domestic agrichem channels/chinese generics

Deferment of CSM off-takes

Tightening Pollution Control norms

First/Second Supplier CSM position

Global agro chemical sector going through challenging environment. Saltigo experiencing declining sales (despite higher selling prices in 2016)

What proportion of CSM today is CRO (not related to front-end sales of Innovator clients)?, and what proportion is CMO (related to front-end sales)?

What is the genesis of the Globally challenging environment - Inventory/Stocking levels at Distributors?

This is the 3rd year of slowdown. Once destocking gets over in FY18, will see proper revival? FY16 and FY17 CSM growths - are probably bottoming out?

Pharma chemicals presence beyond intermediates - leading to USFDA inspections? Or, strategically you are not getting into APis but sticking to Intermediates only

Global M&A consolidation in Agrochem space - e.g Bayer (existing customer) acquiring Monsanto - being seen as a big opportunity for PI to harness. It could also work in the reverse?

Those curious about the Investing craft may find it instructive to “parse” above information base for clues on the changing picture?

30 Likes

Another positive development http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/58476202-c637-45ac-8b36-8dc47268a0b9.pdf

6 Likes

PI Industries partners with Germany’s BASF for crop protection solutions

3 Likes

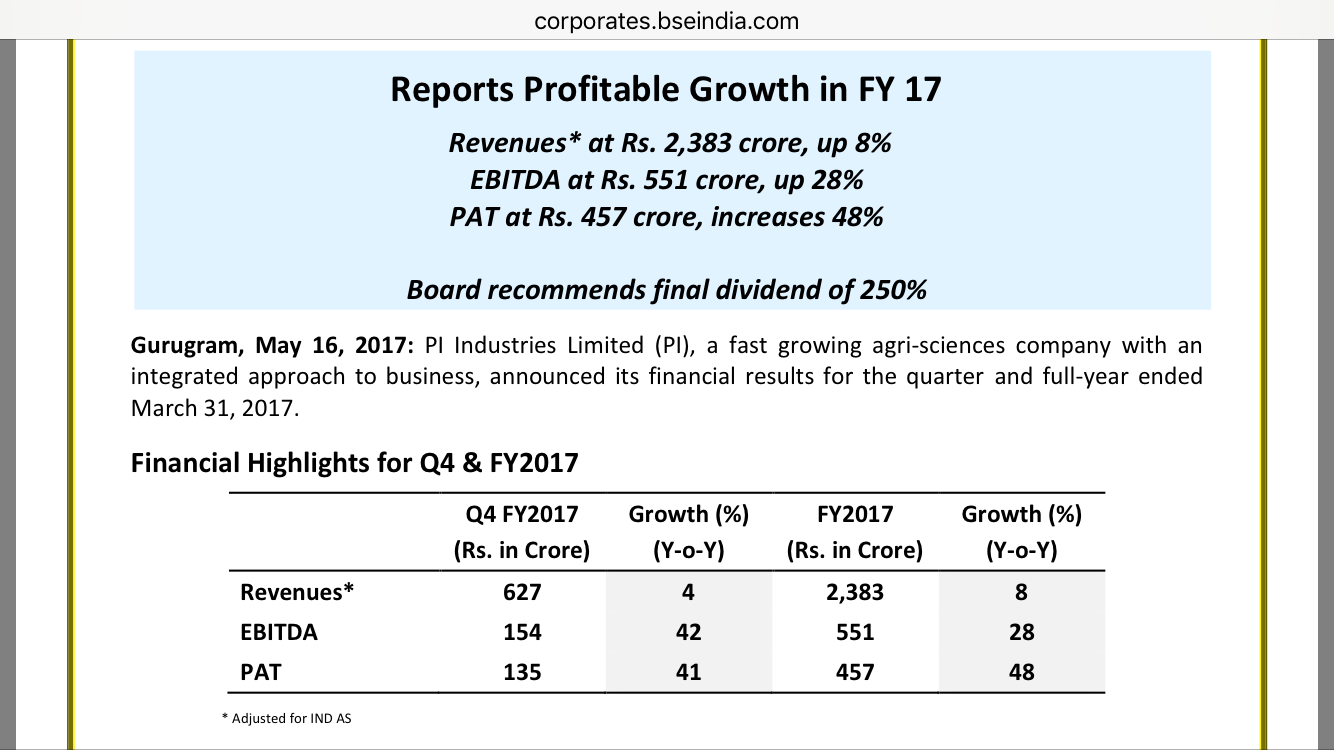

Q4 Fy17 Results:

3 Likes

My notes form conference call:

- 8.4% growth topline in fy17 and - healthy cash generation

CSM:

Expect global agrochem industry to rebound by second half of 2018.

Exports grew 10% in FY17 - expect fy18 10% exports growth mainly in second half

Order book 1b $ with 8-9 molecules

expect global agrochem industy to revive

- commodity price may be revival

- inventory in channel with companies in global has reduced, time for replenishing this will come soon as last two years inventory has been reducing

- purchasing schedules and volumes increasing by 2hfy18 - industry will rebound by 2018- clearly seeing hints in this

There are several new client additions to r&d pipeline

agrochem has 17-18 customers totally.Top 5 have more than 50% revenue share.

Creating capacities for new products based on negotiation with customers

Next tranche of investments in next couple of years, enough land in jambusar for 5-6 plants

Exports have lesser working capital requirements mainly due to less receivables

Margins, capex, tax rate:

Margins - 23% maintainable

Jambusar 65-70% capacity utilisation

Much lower tax in fy17, Fy18 - 20 odd % tax rate

200cr capex in fy18

INR appreciation - every new purchase cycle renegotiated - very less impact of INR appreciation

Domestic:

PI signed comarketing agreement with BASF - PI will be exclusive partner for these two products.

- 4 molecules in 9(3) - mainly used in rice horticulture maize - have good potential

- Not seeing increased intensity in nominee gold in fy18

Significant revenue potential in BASF products for next 3-4 years

domestic growth around 10% in fy18

Business model:

Business model is non conflicting with innovator. Do not want to get into generics etc currently.

Cash flow to be invested back in business instead of returning back to share holders.

Due diligence in on pharma ongoing, soon will be concluding on this proposition. Premature to talk now.

Farmers trust PI brands

Trust with global agrochem companies for their IPs

Guidance:

export and domestic both around 10% for fy18

Medium term mid high teens - based on agrochem and other fine chemicals and getting into pharma will secure those kind of projections

Buidling capability in pharma - Bala Ganesh appointed as director will be the technical person in board for science and technology company

http://www.cmmacs.ernet.in/cmmacs/Personnel/balganesh/

21 Likes

Nice summary Ananth…company seems to be taking all the right steps to ensure scale up from a higher base. BASF tie-up is really interesting and order book crossing 1 bn. USD is heartening. Pharma segment acquisition will be key monitorable as considering history of management, it might be an interesting step forward.

Rgds.

Discl. - Invested in PIIND

1 Like

Hi,

Do anyone has idea how this order book works? If we consider it as 1 billion dollars it comes to be around Rs.6500 crs.

Thanks

Prashant

Its an order-book executable over a 4-5 years period. Majority of the orders have take-or-pay clause.

Rgds.

Mahesh Bhai… Is it worthwhile to buy/hold a 10% grower at 25 times trailing? Numbers look visibly good as they are not paying taxes. As they have said that from now on they will be paying around 20% as tax…there will be a visible impact on bottom line.

It is a good business due to the visibility and longetivity without doubt but what about the valuation…as they will not be growing as they were in past.

3 Likes

I can’t comment on individual investment/divestment decision and any of my comment should not be taken like that. Since I have tracked this company for long, I feel time is ripe for next wealth creating opportunity to unfold here as many factors seem to point towards that :

– Increase of CSM order-book to 1 bn. USD is key notable as it only comprises of 60-70 % of the orders to be executed and other 30-40 % comes from Annual Contracts related to order-book but are not strictly covered in order-book. This provides exceptional visibility for CSM segment for next 4 years even on current higher base. Now, there aren’t many companies who, even on only current order-book, have 1600 cr. p.a. revenue visibility with decent margins (24 %+).

– BASF tie-up for domestic segment seems a very good one as it will combine strength of both companies — high-potential products of BASF and marketing and demand creation strategies of PIIND. Over next few years this tie-up might bring in considerable revenues to the company with good margins.

– Recent appointment of Dr. Balganesh on board signifies seriousness of the management to expand meaningfully in non-agri-CSM space. It is to be noted that Dr. Balganesh was the key person because of whom Astrazeneca was able to set-up and build a robust R&D centre in India and was therefore made VP- Discovery & R&D and Executive Director of the Centre. After him moving on to CSIR, Astrazeneca closed the said centre.

Whereas 10 % growth seems to be in a situation when global as well as domestic agchem industry itself is struggling, in case of a rebound, which is widely expected in next 2 years, company might be a major beneficiary and return to growth path. CSM order-book enhancing by 20 % even in current bad times is heartening. It will be improper to value a company only on one valuation multiple basis. However, even on pure P/E basis, Rallis is trading at 26.93x, Bayer is trading at 45.76x, UPL is trading at 24.08x, Excel Crop is trading at 25.42x, Insecticides India is trading at 24.52x, Dhanuka is trading at 33.12x, Astec Life is trading at 61.34x, Bharat Rasayan is trading at 23.42x, Syngene is trading at 33.88x and Dishman is trading at 33.18x. All these companies have some sort of business that can be compared to PIIND. As opposed to this PIIND at CMP of INR 820 per share is trading at 24.67x and if we take Tax Rate @20 % then its trading at 27.68x.

Don’t interpret this as my comment on valuation of specifically PIIND or any company v/s others, but, I just pointed out the facts in response. There seem to be many triggers inplace in FY18 for PIIND that’s what I believe and if in FY18 it can manage even a 10 % topline growth with 23 %+ EBITDA then it will be a good launch-pad for FY19-FY20 when all 5 plants of Jambusar facility will be working in full swing and pharma initiative must have taken shape.

Rgds.

25 Likes

and market does see future and next year market may discount all the above

Excellent point made,if I m not wrong u are the who followed or should I say invested from 2011, so u know more about the business dynamics than most of us , sir what could the margin in domestic agri space is 20 or above 20

Domestic agri space margins should be in 16-18 % range.

Rgds.

1 Like

By margin do you mean OPM ? or margin of one product?

Margin is equal to OPM only if working capital cycle is 365 days.

By margin I mean ebitda margin of the segment in question i.e. Domestic agri input segment.

Rgds.

Considering tax rate @ 20% next year v might not c significant increase in net profit is my assessment correct or m I missing something

@ Mridul

Sorry to interject thus, in between your discussion,but since I was going through this thread, on PIIND, for the first time at valuepickr( I am invested in PI for quite some time), I am curious to ask you , on what basis do you call," PIIND a 10% grower"?

When we compare a Company’s growth to its PE, we are taking the “Earnings” into account. And if we take, Earnings growth of FY2016-17, its at 48%, so PIIND in that sense is a 48% grower, with a PE of 25, when CMP of 820 is considered.

1 Like

@Deepali - This is just a mental model to evaluate if it merits investment at the current price. One can compare p/e to bottomline, but there is a problem here. Bottomline here from last 2 years is not being reflected ‘accurately’ due to lower tax outgo. This year they have paid just 9% tax. Last year as well, it was pretty low than the average they have been paying from last 5-7 years. Average tax rate for PI is close to 28%.

So considering if we extrapolate, PI has been growing their bottomline around 19-20% in last 2 years. Not 47-48%.

One can say that eventually it all comes down to earning. But, there is a limit as to how much a company can improve on its margins, which are already quite high (24%). So, i like to take into account both topline and bottomline growth to merit an investment. From last 2 years, topline is growing at 8%. So the question.

1 Like