Axis Direct’s research report on PI Industries

PI Industries- axis direct.pdf (600.2 KB)

With reference to company�s press release dated May 30, 2016 titled �PI Industries and Mitsui Chemicals Agro, Inc. to establish a Joint Venture for Agrochemicals Registration in India�, PI Industries Ltd has informed BSE that M/s PI Life Science Research Ltd (subsidiary of M/s PI Industries Ltd) has transferred 51% stake held in Solinnos Agro Sciences Pvt. Ltd.(“Solinnos”) to M/s Mitsui Chemicals Agro Inc., Japan as approved by Board of Solinnos in its meeting held September 01, 2016. This is in pursuance of the joint venture agreement entered by PI with Mitsui.4F9CAC25_A95B_4B97_A1C5_BFBE6550BCF4_195934.pdf (248.8 KB)

PI Industries plans foray into pharma sector

http://economictimes.indiatimes.com/industry/healthcare/biotech/pharmaceuticals/pi-industries-plans-foray-into-pharma-sector/articleshow/54276965.cms

via The Economic Times App(Download Now):

http://ecoti.in/etapps

Is there a paid service who provides historical summary of con calls transcripts in form of document?

Researchbyte.com makes available concall transcript, research report etc. Though not sure about a very long look back period for historical files.

BTW, also taking this opportunity to acknowledge the value addition that your diverse perspectives is offering to this forum.!!!

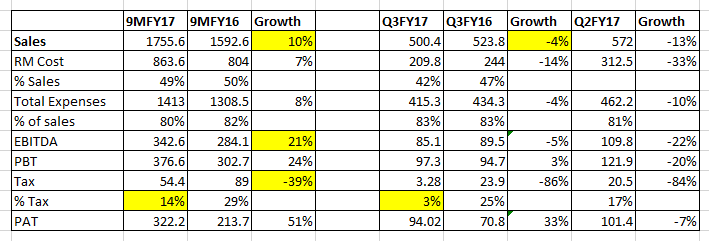

Superb results by P I Industries - Sales up 19% yoy. Profit (PAT) up 77%.

Total Income 572 Cr from 476 Cr YoY

Net Profit 101 Cr from 57 Cr

Need to understand why the tax rate has reduced from about 28% to 16.5% yoy.

Due to starting of new plant and sez benefits last quarter also benefitted and this will go on for some time

I attended PI concall today…Here are my notes. I may be wrong in understanding some things. Please add if I have missed something.

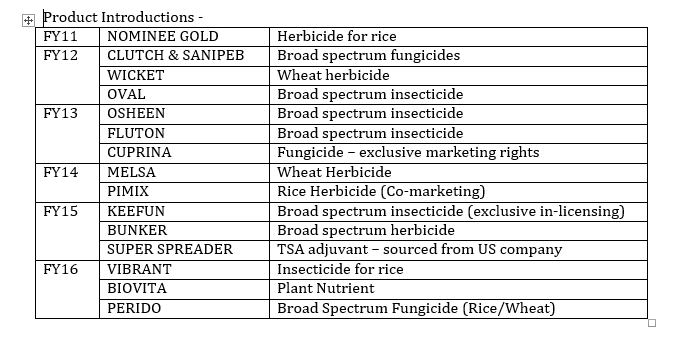

CSM-Past launches are gaining momentum. Jambusar is ramping up as expected. Right now 75% utilization.

On domestic side there is low pest infestation- Insecticides have been a key challenge. Herbicides also reduced but Fungicides are OK.

Tax rate for full year FY17 and FY18- for FY17 should be 18%, next year 22% coz of some benefits on SEZ will reduce from 100% to 5% on completion of 5 years. This is for all the units at Jambusar.

Revenue Breakup

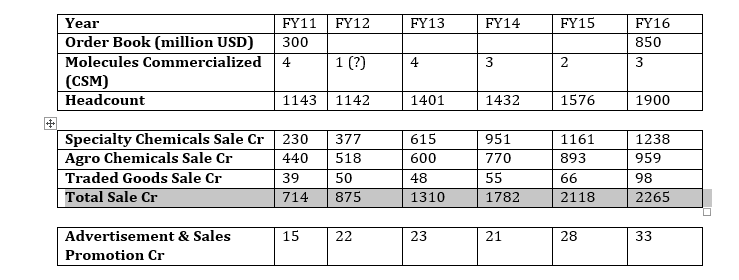

Order book around USD 800mn, down from 850mn due to execution.

Guidance

• Earlier guidance was 18-20% for FY17….now there is a moderation in guidance to 15% for full year FY17 for both domestic and CSM. Rabi is expected to be good but some areas like Tamil Nadu are not good.

• Outlook for CSM- commodity prices, weather etc hasn’t been good for last 2 years. Its cyclical and expect pickup in commodity prices in FY18. Channel inventory is at pretty high/peak level. Besides this there are currency headwinds. All these factors have been effecting performance of global players. Things are better than last year.

• Are you building buffer in guidance? No we want to be realistic. Understand current global situation and factor that in. For PI, it depends on individual products- For some we had to advance our schedules/supplies while for some there was a slowdown/deferment of supplies. Products we will supply in H2 are not doing good globally and hence a lower guidance.

20 odd products that have been commercialized till now- These are global products, not specific to any 1 geoagraphy. Good pipeline of 20-22 pdts in R&D at any time. Good visibility of 15-20% growth for several years

Pharma initiative-

• Actively evaluating couple of options. Started 1 and got 2 more. In coming Qs we will take the next step.

• How big can pharma be in 2-3 yrs down the line? Too premature/speculative to comment. Not in a hurry.

Other operating income higher due to export credit/ duty drawbacks. This part will continue as per new scheme by govt. Other income - forex gains and interest income.

Nominee generics have been launched so whats the impact- Doing fine, got some growth. Market has expanded so we havent been impacted. Consumer mindset remains for premium brand.

Osheen, Keefun, Vibrant- as per expectations. some challenges but nothing too much. They will be substantial in next 2-3 years.

Mitsui JV for registration of products- Discussing development plan for 2-3 new molecules. Will go for registration in 2 years. Focus on cotton and rice in Mitsui JV- will reduce dependence on rice.

150-200cr capex by end of year.

Consolidation in agrochem space- Will help us in sustaining growth because it will provide more opportunities of outsourcing to large companies. We have deep relationship and partnerships with these large companies.

China behavior post Syngenta deal- Any change in location based outsourcing deals? Possible. China cost+environment situation is becoming challanging. India is getting many opportunities due to this…even in bulk chemical industry.

I was reviewing my portfolio holdings in detailed manner & following are notes from my reading. This thread covers almost all the points below. The notes below can be seen as summary of the thread in a way.

BUSINESSES

AGRI INPUT

Industry (Cliché Information)

Top 6 companies, Syngenta – Bayer – BASF – Dow – Monsanto – DuPont, command 75% of sales in global crop protection market.

Indian agrochemical industry size is ~2.5bn$ (Growing at 9%) & export market size is ~2.5 bn$ (growing at 15%).

Average yield per hectare in India is half that of China & crop protection chemical at 0.7 kg is lower than that of even Pakistan (1.3kg).

In India, there are 125 producers (60 large & medium) who produce 60 technical grade pesticides. Around 70% of these are off-patent pesticides. Also there are more than 1200 pesticide formulators present in India.

This cliché information satisfies one of the investment criteria that the products have large market size (domestic & potential for exports) for several years.

Business Model

Products

Product Categories

There are three ways in which products are created –

The company has products in following segments – rice, vegetables, sugarcane & cotton

Some of the key brands comprise - Nominee Gold, Osheen, Foratox, Fosmite, Biovita and Roket

Sales & Marketing

The company has 40,000 retail points, 9000 distributors & 29 stocking points across India as per AR FY12-14.

ARFY15 mentions reduced number – 8000 distributors & 35,000 retail points.

AR FY16 mentions – 5000 distributors & 40000 retail points.

(Above average marketing organization?).

Strengths

Due to large number of producers, low awareness & spending power of farmers, having pricing power is difficult in this industry. Company seems to have moderate pricing power due to some hit brands & strong marketing setup.

Risks

Monsoon & climatic variations remain one of the key risk areas for this business. A bad kharif season in FY13 caused inventories to rise leading to price erosion.

Crude oil is one of raw materials & price variations also pose risk. Raw material to sales ratio has remained constant at 55% for last many years.

Government regulation & price control, low spending power of farmers also remain one of the long-term risks to this business.

CUSTOME SYNTHESIS & MANUFACTURING

Industry Information

Only a handful of global innovators innovate on new molecules due to high cost of discovery to commercialization (~0.25 bn $). The average time taken for this process is ~10 years. The global CSM market size is pegged at 85 bn $.

Business Model

Services Offered

Customers

Clients are based in these countries – Japan, Europe as per AR Pre-FY13. Later company got award from Bayer – that is also another customer.

Sony Corporation

In January 2011, a Joint Research Center was setup with Sony Corporation at Udaipur. The potential areas for molecules are flexible TV, Solar cells etc.

Risks

Any violation of confidentiality agreement, IPR violations would ruin the reputation of the company & can cause long lasting harm to CSM business.

POLYMER COMPOUNDING

This business was sold to Rhodia, S. A., French multinational company due to profit margin pressure in April 2011.

NUMBERS

RESEARCH & DEVELOPMENT

Company has good research organization & research focus areas include – Agrochemicals, Fine Chemicals, Specialty & Photographic Chemicals, and Pharmaceutical chemicals.

Formulation Development Lab was started at Udaipur that is engaged for the development of new Agri formulations.

Strong R & D focus with move towards more complex molecules remains one of the major reasons that evoke interest in this company.

MANAGEMENT

Depth

Rajendra Dev Kapoor

Listed as Director in Monsanto India since 2006. Listed as director on PI board in 2015. Seems to have left company in 2016 to become MD at Sollinos agro.

Devendra Kumar Ray, Head - Operations

Head of operations for ~3 years, total 25 years of experience.

Rajnish Sarna, Director, CA

25 years of experience, focus on CSM exports - turning R&D & Operations into service models.

Prashant Potnis, CTO

25 years of experience, worked in BASF, Clariant, Syngenta.

Average employee salary has grown at an impressive CAGR over last few years.

GROWTH AXES/ENABLERS

SUBSIDIARIES

MISCELLANEOUS

AR FY11

AR FY12

AR FY13

AR FY15

TOOLS

Company mentioned it uses following tools to obtain latest information –

STN

STN is basically database of all IP, scientific information worldwide (sepecially in the world of chemistry). STN tools review 95% patents in world, world’s top 25 pharmaceutical companies use STN. STN seem to be providing a very good interface to search information.

SCIFINDER

It is another search tool that allows search by author, journal, chemical structure, reaction structure etc.

CHEM-OFFICE

ChemOffice Professional is an integrated suite of scientifically intelligent productivity tools that enables researchers to capture, store, retrieve and share data and information on compounds, reactions, materials and their properties.

REAXYS

TODO

The latest models of GC-Mass, HPLC-Mass, And Preparative HPLC & ICP are used for spectral analysis & preparation of standards. (What are these models & standards??)

Overall, PI remains an excellent company to invest in due to best or above average setup in all the areas of business like – Sales & Marketing, Brand Building, Research & Development, Operational Excellence, Financial Management.

It has products that are retail in nature as well as B2B in nature. The products are getting more complex & more interdisciplinary in nature by the day. This creates very high entry barrier for competition.

The operating margins have started improving in last few years & levels should be maintained or expanded.

The management seems to have good integrity & there is no evidence to say otherwise.

There are still several axes of growth that are not fully exploited.

The areas to watch out for are as follows –

Management depth - Mayank Singhal is still very young but still need to get a good reading on whether company is one-man army or there remains an intelligent team at the helm.

Also size would become an anchor for growth going forward.

The stock is well discovered (32% holding by FII + MF) & richly valued.

Disc - I hold, not a buy/sell reco

@rupeshtatiya thanks for your hard work. Such work makes VP the best place to look for information. PI is generally considered an agrochemical company selling pesticides but over the years custom synthesis business has been contributing a growing share of the revenue. This is also a high margin business and that’s what makes PI’s margins one of the highest in the industry. However, I did not find much information on custom synthesis business except for the following line in AR2014-15.

Your Company’s custom synthesis exports, now accounting for more than half of revenues.

More than half is significant and I think this business will be main driver of profitability in future. Can you share your thoughts on this business?

@Yogesh_s Check quarterly concall transcripts.will give you some idea n visibility in its order book , future projects n related expansion areas they r targeting in next 2-3 years .Disc - invested

I don’t have anything else to add than what has been said on this thread, particularly by @Mahesh. Since these are IP sensitive & confidential agreements, not much information has been made available to general public.

Tracking headcount (esp. scientists), order book position & management commentary are what is easily available information. If we can get hold of some employees of either PI Industries or global majors who interact with PI, that could provide some more clues. Other than that, I am open for ideas on getting more information on CSM business.

Regards,

Rupesh

PI Q3FY17 results -

Regards,

Rupesh

The december quarters have always been down when compared to other 3 quarters.

Some points discussed in conference call

–3 product launches for next year

–Tax expectation - expected 16% in Fy17, 20-23% in FY18.

–177cr domestic revenue vs 157 cr domestic last year

–323 cr - export revenue vs 366 cr last year degrew by 12%

–domestic growth impacted by demonitization and scanty rainfall

–order book CSM - $850 million

–CSM business - commercialized 3 molecules in initial stage

–subdued topline growth last year and this year due to global challenges.management state this as a cyclical abberation. target of 20% topline growth over the years.

–Capex Plan - 200 cr per year over next 2 years

–Fourth facility to come up end of next financial year.

–Pharma opportunities being evaluated - more detailes in a couple of months

Axis Direct’s research report on PI.

is 2017 monsoon expected to be below par ?