Today in the interview management said that even with this rainfall we should expect revenue rise of 10-15%. Am I missing something? With the order book they have, shouldn’t they be expecting more growth if the rainfall is good? Sale of their products as well as the sale of their clients products should rise.

I think 10-15% growth mentioned should be for the agri space while CSM growth could be higher.

4 Likes

Nominee Gold: Finally competition at doorstep (Edelweiss report 5th May summary)

The Central Insecticide Board (CIB), in its recent meeting, granted

registration for indigenous manufacture of bispyribac sodium technical

and formulation to 2 players. We anticipate competitors to launch the

products soon. Consequently, PI Industries`s (PI) largest selling product,

Nominee Gold is likely to face heightened competition. Our stress test

analysis suggests our FY17/18E earnings faces downward risk of 8-10%

and RoE of 27-28% could moderate by 150-200bps going forward. We

believe current valuation factors in the impact to some extent and thus

downside looks limited. Maintain ‘BUY’.

1 Like

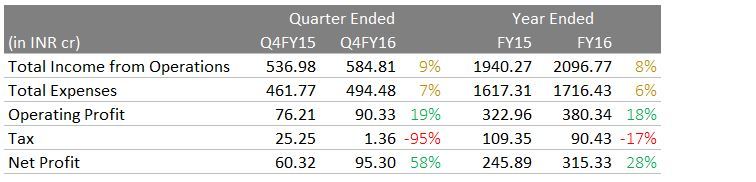

Q4 Results announced. Very mediocre results. Net profit is higher due to lower tax.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=30cb6e95-0432-4975-9be1-7b5c3dcec496

PI Industries Q4 and FY16 results

Why lower tax? Need to wait for detailed press release which might be out soon.

- Board approved proposal of entering into a JV with M/s Mitsui Chemicals Agro Inc., Japan for the purpose of registering Mitsui products in India.

- Appointment of Mr. Ravi Narain (co-founded NSE in 1994) as an Additional Director on the Board of the Company.

- Commenced commercial production at third unit located at Sterling SEZ facility, Jambusar w.e.f Jan 11, 2016

Hopefully 15-20% sales growth will resume in FY17 considering the strongest El Nino in nearly 20 years is behind us now…

Disc: Invested

2 Likes

They are entering into a JV with Mitsui Chemicals and also incorporated name Solinnos Agro Sciences Pvt Ltd.

Some margin expansion has led to not bad a growth on Operating profit.

As @lustkills said, the reasons for lower tax should be watched. There maybe some tax benefits from Jambusar SEZ but they cant be so high.

These are good results on the operational front. I will look for amount of sales contributed by CSM. It will remain a 20% compounder for years to come.

Press Release:

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/39D9DB80_E7C8_41FD_ABB3_13781C942BB7_205136.pdf

Key points:

-

In Q42016, 17% increase in domestic sales, 6% export. FY2016 6% domestic, 10% export.

-

Better tax planning on SEZ operations & extension of R&D operations

-

New herbicide “Legacee” to be introduced in Kharif 2016

-

Initiated business in Pharmaceutical Segment

The last part is an interesting development. Does anyone know more about this? We might get some answers tomorrow in the concall.

1 Like

I agree…the results are much lower than expected. NP is up only due to lower Tax. Had tax been constant, we would have seen a lower PAT…

csm order book further improves from 790mn to 850mn dollars mgt seems pretty confident from now , mayank singhal suggest on cnbc

3 Likes

Expect 18-20% revenue growth in FY17: PI Industries.

Did anyone attend the concall today?

@idikasony, he mentioned 18-20% minimum. Let’s see how it unfolds.

Disclosure: Invested

All eyes are set on the first year of launch of generic version of PI’s key product Nominee Gold…although it’s a well known fact that it’s a 100 cr. + brand, but some industry guys put it at 200 cr. and therefore the impact of price reduction v/s volume growth is keenly watched.

Rgds

Disc.- No Holdings.

Motilal updated report

http://www.motilaloswal.com/site/rreports/HTML/635998506793879182/index.htm

1 Like

Interesting article in Forbes.

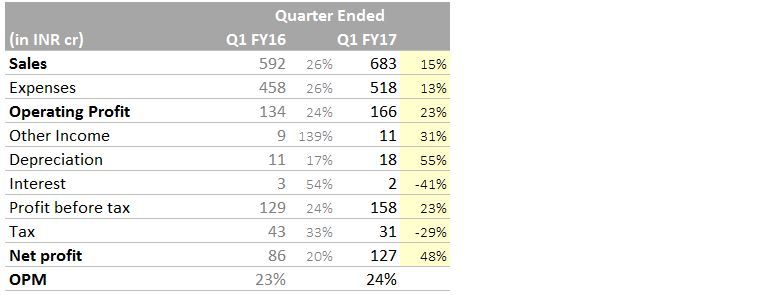

PI Industries Q1FY17 results are out. Revenue up 15%. PAT up 48%! Good results.

6 Likes

Why the TAX out go is low. Due to SEZ operations?

4 Likes

Concall Details:

-

Revenue performance was robust at 15%. Exports saw increase of 20% YoY during the period whereas India business displayed healthy growth of 10% despite a delayed onset of the rainfalls. The scale-up in production at Jambusar on account of additional capacities in place together with execution against robust order book is contributing towards incremental growth

-

PI focused on its product-mix in order to drive a superior performance during the Kharif season. The company maintained its disciplined approach to channel sales thereby resulting in an improved inventory position.

-

The company has launched eLegaceef, a new herbicide available in key markets and has seen a healthy initial response from farmers. This herbicide has been launched in a co-marketing arrangement with Bayer Cropsience. Management intends to launch 1 more new product in FY17.

-

Q1 FY17 EBITDA stood at Rs. 166 crore, up 23% YoY on the back of expected growth in sales. Margins saw enhancement by 154 bps from last year’s levels on the back of favourable product-mix.

-

Profit before Tax during Q1 FY17 was at Rs. 157 crore, higher by 22%. Q1 FY17 Profit after Tax was at Rs. 127 crore, up 48% YoY. This follows the increments seen in revenues in the same period and the tax benefits accruing from exports out of the SEZ facility.

-

Management is optimistic on global and domestic agrochemical industry in FY17 following good monsoon in key domestic markets and traction in exports. However, high channel inventory remains a concern in near term. Management is optimistic for next quarter and confident about its growth prospects, led by judicious product mix and focus on developing innovative products.

-

The company has maintained its FY17 growth guidance of 18-20%. CSM business is likely to grow at 18-20% YoY in FY17. PI has guided for 100-150 bps YoY jump in EBITDA margin in FY17.

-

The company has guided for low tax rate of 22-23% (earlier 24-25%) for FY17 on account of tax benefits arising from higher contribution from the SEZ units.

-

Net Debt to Equity ratio stood at 0.09x, as on June 30, 2016 (0.11x as on March 31, 2016).

-

The company expects to incur capex of Rs 150-200 crore in FY17/18, primarily towards setting up another unit at Jambusar, setting up a facility for manufacture of early grade pharma intermediates, expanding the Udaipur plant, de-bottlenecking the Panoli plant, and construction of an admin building at Jambusar

8 Likes

All I can say is PI story keeps getting better with time. 2 dedicated plants already started and foray into pharma taking shape is a big positive.

In short term, EBITDA expansion and on top of that the lower tax are an icing on the yummy cake.

5 Likes