I had made some queries to the Management. Below are the answers they gave.

1)Impact of GST

Impact of GST on profitability would be very low. Some of the G&A expenses like food,insurance,etc. which are not eligible for GST credit will move from current 15% bracket to 18% bracket

2)Sensitivity of Forex

The sensitivity in our case is approximately 40bps to very 1% change in exchange rate. However, we are adequately hedged till January 2018. So, there will be limited impact at the PBT level in the current financial level.

3)Why promoters are decreasing the shareholding

Dr. Anand Deshpande-Promoter-Founder-CEO has neither sold any shares nor has nay intention to sell in future.His father MR. Suresh Deshpande is 80 years old and wants to donate his entire wealth to charity. HE had announced twice in the past that he would be selling his shares for donating money to charities. The sale is nothing to do with company’s performance.

I would like to add my observations on Persistent.

IT is undergoing disruptive changes - where customers are demanding reduced prices on application development and maintenance services which has been long time revenue generator for Indian IT industry. Companies who are moving from this traditional model towards IP based and product model stand to gain in this changing scheme of things.

Coming to the point, Persistent is one of such company, which seems to have made good moves in right direction. Its tie up with IBM for AI based product offerings in terms of IBM Watson should gain better momentum going ahead. IBM Watson is a platform based on AI and cognitive science coupled with RPA (Robotic Process Automation) capabilities. Currently there is increasing demand for RPA, Cloud and AI capabilities and Persistent’s alliance with IBM Watson - though with its own impact on OPM - would help it to gain more market in these areas.

In FY16-17-Q4, Digital revenues as identified by Persistent has gone up by about 9% QoQ and product based business (Accelerite) has demonstrated 7.7% QoQ growth. Some of these developments should help Persistent grow better than some of traditional IT companies.

We need to observe the margins carefully going forward. Margins (OPM) may take little longer time since company seems to be moving towards IP based revenue model which can affect OPM for some more quarters as per my experience in IT industry.

Disclosure: Invested at around 600 levels, and views could be biased.

sorry to butt in here. Some industry insiders think IBM branding of its AI initiatives is not good enough.

Disc - No stakes

Do you have any basis for saying tie-up with IBM for IBM Watson is a move in right direction?

IBM Watson is marred with series of failures. Even Persistent is loosing money on this one.

Hi All,

I would like to study further about the tie-up and IBM Watson in detail to comment more on it.

My point was that, company seems to have moved in direction where I can see some traction going forward. I would like to wait and watch for next 3-4 quarters to see whether this move and other initiatives benefits Persistent or not.

Overall sentiments about IT in general are not good but things can change in years to come for companies which have offerings in products apart from services. We need to see it from this perspective.

I came across one news item which highlights negative of IBM Watson. https://www.axios.com/ibms-watson-gets-no-love-on-wall-street-2458652758.html

Summary of news article: Chamath Palihapitiya of Social Capital (VC) termed it is joke. He terms it as product of PR operation rather AI science. Wall Street is skeptical of IBM Watson.

However, failure of partner should not be considered as big negative for Persistent. It is normal manageable business risk. The investment in it certainly is not make-or-break kind of risk for Persistent.

Any one from Mumbai attending Persistent AGM ??

Tells, How AI & IoT has become necessity of today!

IBM Pitched Its Watson Supercomputer as a Revolution in Cancer Care. It’s Nowhere Close.

We should distinguish Persistent from Large OEMs or platform companies. For former this is a way to get into cognitive and from what i know, they are doing well. They are not tied to fortune of any specific company or platform.

Second, I think we tend to hugely underestimate the effort needed to make a shift from bodies based arbitrage driven business to where you’re responsible to deliver on cutting edge. Persistent is ahead of some of the larger peers but long way to go still…

Dis- watching. Not invested

Recently have tried to analyze persistent.

Company Background: Technology based mid cap company with focus on digital transformation, data, how internet of things and IP based products

Four business areas:

• Digital: Focused on our digital ecosystem by bringing together technology partner ecosystem solutions and architecture for Digital transformation

• Alliance: Focused on IBM partnership on Watson and Internet of things through digital transformation

• Services: So custom services for software in product development through agile methodologies

• Accelerite: Forecasting products for enterprise Telecom and public sector

Some Industry data on opportunity and perspectives:

How is digital and IoT market growing from deals perspective

which IT vendors will succeed in digital world

As we know, IT industry is going through turbulent times with many challenges mentioned below:

- Traditional revenue sources are stagnant in terms of growth : Does not looks an issue as company is still growing at 20%+

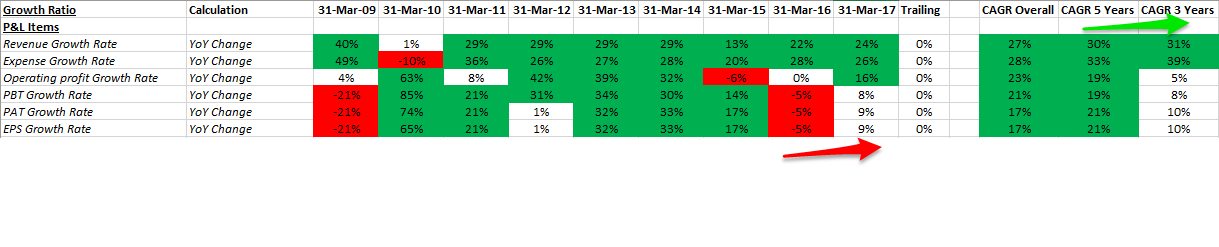

- Margins are under pressure : Yes, profitability growth has been 1/3rd of revenue growth highlighting margin pressure.

- New emerging areas need new approach, skill set: We will see this later, anyway revenue growth does not seem a risk

- Currency risk has been high off late: Could this be one of reason for margin pressure? let us explore later

- Localization risk raising doubt over on site-off shore IT model : What is on site to off shore ratio to overcome this risk, let us explore later

So, let us see , how persistent has been doing off late on each of these key issues by analyzing persistent numbers:

Also, let us see , by investor key metrics how the business is doing?

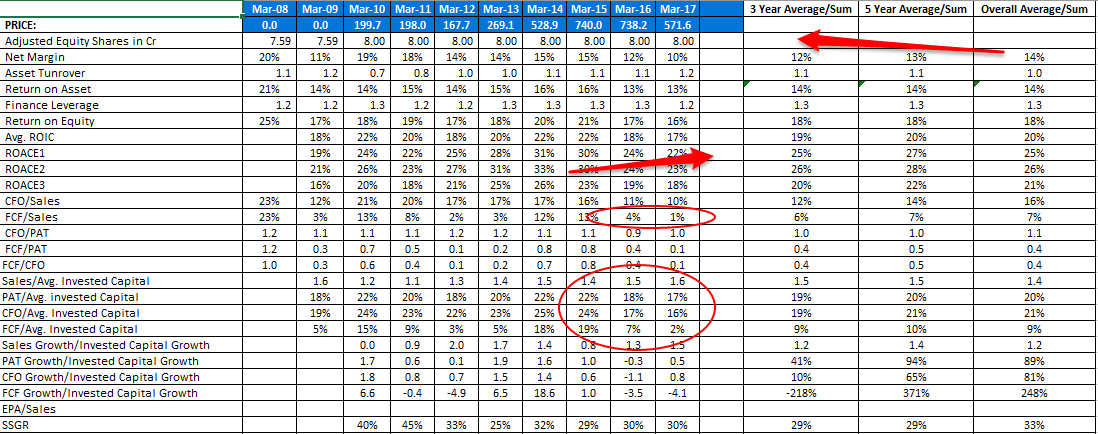

- Net margins have fallen though no impact on asset turnover

- Most of ratios like ROE, ROIC, ROCE has fallen primarily due to 2 reasons:

- Fall in net margins

- Lot of capex evident from very low conversion of CFO to FCF

- FCF faces double impact of low margins as well as CAPEX

Why it is happening? Is it permanent? How does future look like? Was the margin fall due to poor business quality/short term factors/some long term strategy?

Let us check quality of operations compared to its history

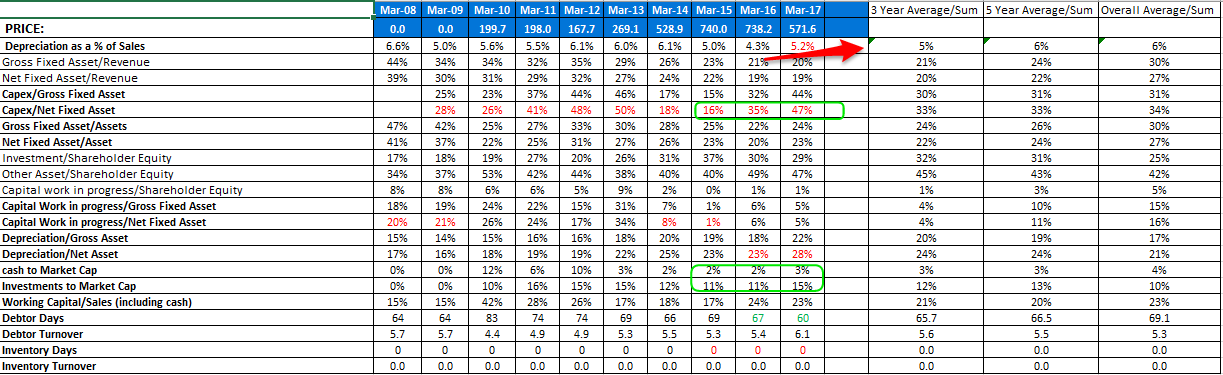

- In last 2 years, CAPEX rate has been higher also reflected in higher depreciation in FY17

- Company has more than 10% of market cap in cash and investments and it is a 0 debt company

- Not much change in working capital, debtor days etc.

So, Now , the unanswered questions or exploratory areas are:

- Revenue growth does not looks an issue as company is still growing at 20%+ (see unique things happening section for the detailing)

- Why PAT margins are under pressure : profitability growth has been 1/3rd of revenue growth highlighting margin pressure.

- Is persistent prepared for new type of IT business - SMAC? (see unique things happening section for the detailing)

- How currency risk has impacted PAT Margins? What is long term impact ?: Could this be one of reason for margin pressure? let us explore later

- Does Localization risk raising doubt over on site-off shore IT model? : What is on site to off shore ratio to overcome this risk, let us explore later (see unique things happening section for the detailing)

- Why it is happening to free cash flow and why falling? Is it permanent? How does future look like? Was the margin fall due to poor business quality/short term factors/some long term strategy?

- Where the CAPEX is being deployed? How it will give returns in future?

So, let us handle PAT margin & currency issue, capex deployment issue and FCF issue one by one.

-

Why profit margins are falling and related impact of currency?

-

Where so much of capex has beebn deployed, what is future capex plan and how FCF is expected to behave?

-

UNIQUE THINGS HAPPENING:

So, these are the unique things happening i see: -

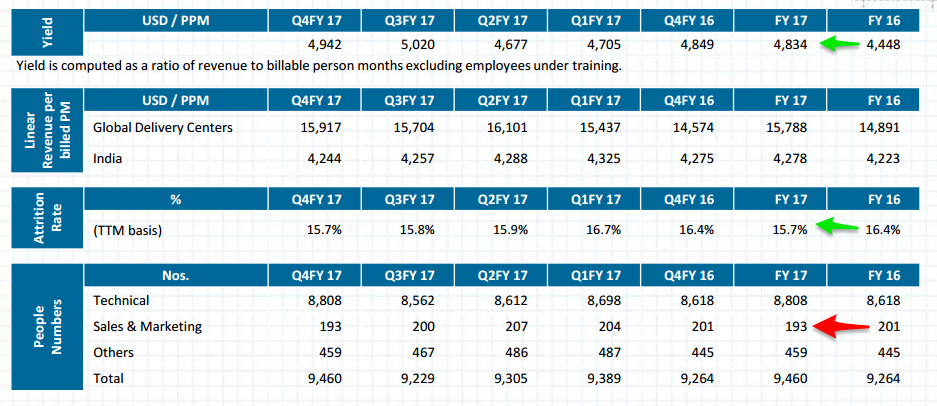

Company is shifting from labor based model to revenue share model : The growth in yield and ratio of revenue growth to headcount growth proves apart from management commentary. Whether this non-linear revenue growth will lead to non-linear profit on upward trajectory, is yet to be seen.

-

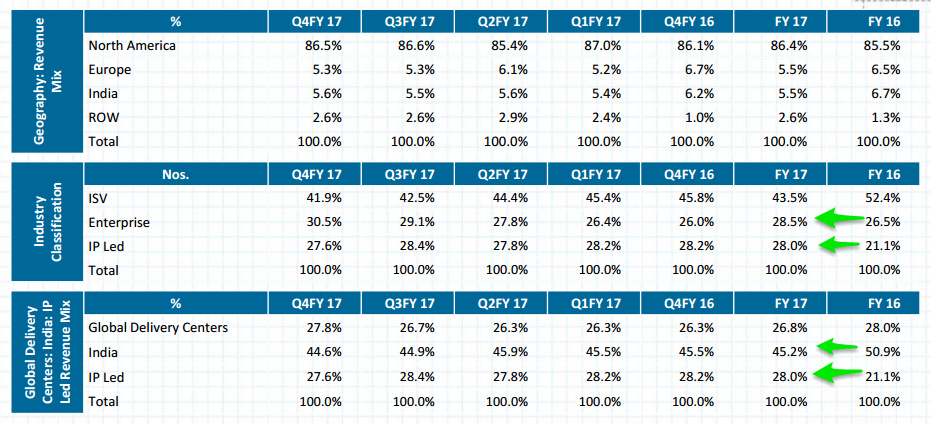

Company is sifting from traditional outsourced product development model to digital , iot and product

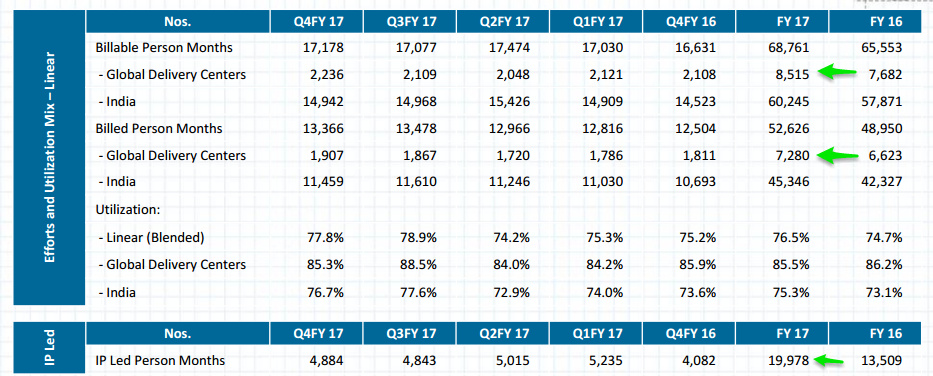

IP Led share is increasing andGDC work is increasing. High GDC work is a reflection of more digital work coming in against OPD.

-

Let us compare if they are living up to what they are saying as every IT company talks about automation, machine learning etc.

-

The company has been able to improve its yield. Is it due to automation or low effort, high revenue business, why it did not convert into margins?

-

The company has been able to reduce lot of offshore revenue contribution which means more and more work is being done from global delivery center. Also, due to this company has 48% of hiring done in GDC and their salary close to new US rules means they will have minimal impact of wage and VISA policy (2-3%). Infosys declaring 10,0000 hiring in US is a sign in similar directions but persistent is already there ahead of curve due to nature of business

-

Above point is also reflected in increase in mean salary growth where as median salary growth is still similar which means the salary distribution curve has been heavily incrementally skewed towards right, again, reinforcing

-

deployment of resources at global delivery center

-

Infy talks of SMAC and new generation IT but looking at their mean employee salary growth, yield, revenue to headcpunt growth ratio, all of them confirm that they are not doing anything different until and unless it is not visible because old business is de-growing heavily and new one is growing heavily,still, leading to muted growth. The new gen IT resources are not cheap, so, are they ramping up their new gen resources? numbers do not say so

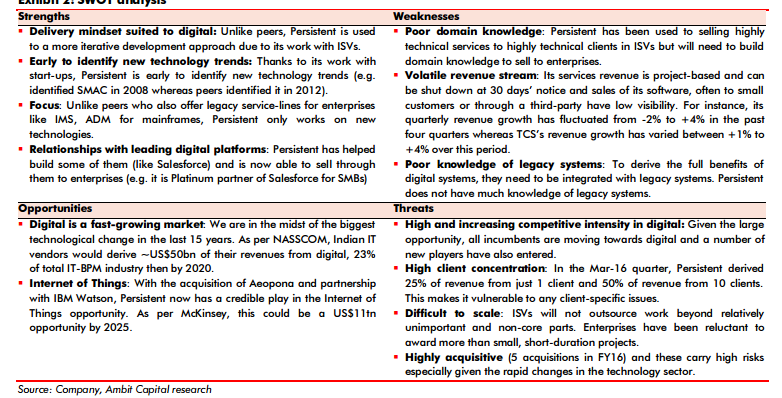

a SWOT analysis by Ambit

Ambit says due to lack of domain knowledge and legacy system, TCS and Infosys will have edge over persistence in digital deals. However, numbers don’t reflect anything thing special about Infosys. Also, if one sees HFC digital deal report , IBM has taken 33% digital deals , 10 times of TCS n Infosys. So, key question is will persistent be benefitted by IBM digital deals for its enterprise business or it will be an isolated effort ,even if let’s say persistent lacks legacy system and domain knowledge , not to forget ability ,time to respond n product mindset r key to success in digital . Also, digital IT deals ao far hace been of smaller ticket size. Further, IoT does it need legacy knowledge ??

So, the new set of questions/uncertainty/risks are:

- What are the key areas persistent does not posses to succeed in digital?

- Legacy system knowledge

- Domain Knowledge

- Salesforce to enter into enterprise accounts

- What persistent is doing to overcome these challenges?

- Contractual employment

- Partnerships based sales model

In Summary:

Opportunity:

Growing in right areas with double digit growth

The space on technology side and on industry size and its mix has huge opportunities

The hit in margin has been more to invest in IBM partnership, new hire for new kind of businss, spend in onsite model for new kind of business rather than margin pressure

Management is ethical, honest and have high regard for Anand Deshpandey intellectual, people and ethical strengths

Management tone for future is positive

Company is protected from protectionism risks due to onsite offshore allocation

Yield improvement, onsite offshore ratio and employee salary suggests that company is really working in new directions and also getting more revenue generated from same or lesser employee, the new type of business model

Second line fo leadership is emerging

Risk:

- Concentration of revenue to few accounts

- Currency risk

- Lack of domain knowledge for larger contracts

- Highly Competitive industry

Disc: Contains 6% of portfolio

My notes from FY 17 annual report:

Industry Perspective: In terms of market potential, IDC forecasts that the worldwide market for IoT solutions will grow from $1.9 trillion in 2013 to $7.1 trillion in 2020. An IoT platform implies the integration of a set of different functionalities provided by individual Components. The functionalities involved can be broadly classified as data capture from sensors, transfer of the data over networks, storage of the data at various stages, analysis of this data, and applications that make use of this data. Each of these can be independent functions, but it is when they are integrated together that they provide those coveted “aha” moments and deliver the most value. Without integration, most of those functions are simply discrete components used individually. Applications make use of the analysis to improve functionality or provide rewarding end-user experience.

Major development in technology industry:

• Technology transformation is a continuous process

• Software is eating the world

• Iot driven digital experience Business models and monetization

• Data leading to actionable insights

• Data digital and iot are interwined

• Interacting through API

• Software force is inspired from industry 4

Business Performance Analysis:

• Recent initiatives have led to more than half of revenue coming from IP LED and digital transformation projects. Also the same is growing at a healthy rate

• In FY 17, the company ended with rupee 28784 million revenue and 3015 million profit.

• 22% of revenue growth in dollar and 24.5 percent in rupee. The revenue contribution of 4 verticals is as follow: Service - 45%, digital 16%, lines - 29 percent, accelerate - 9% . Revenue share of OPD reduced from 52% to 44% . Enterprise share increased from 27% to 29% . IP led revenue increased from 21% to 28% through contribution from IBM watson iot platform

• Coming to profitability, EBITDA was Rs 4,653.47 Million as compared to Rs 3,915.08 Million in FY 2015-16, registering an increase of 18.9%. In terms of percentage of revenue, the above works out to 16.2% for FY 2016-17 as compared to 16.9% in FY 2015-16 • PAT amounted to Rs3,014 Million as compared to Rs 2,773 Million in FY 2015-16, an increase of 8.7%. In terms of percentage of revenue, PAT was 10.5% of revenue as compared to 12% of revenue in FY 2015-16. • As at March 31, 2017, your Company, on an unconsolidated basis, had cash and cash equivalents (including investments) amounting to 8,159.98 Million as against 7,610.69 Million as at March 31, 2016. • The total dividend for the financial year 2016-17 would be Rs 9 per share as compared to Rs 8 per share in the financial year 2015-16. • Personnel Expenses for the year amounted to 19,826.63 Million against 15,654.23 Million for the previous year, showing an increase of 26.65%. However, as a percentage of revenue, these expenses increased to 68.88% during the year as compared to 67.70% in the previous year. The main reasons for increase in Personnel Expenses are as below: • The personnel expenses have mainly increased due to the salary cost of the employees joined at the overseas locations through acquisitions. • Pay-hike which is effective from July 1, 2016 • Increase in employee stock compensation. There was a new ESOP scheme introduced as a Silver Jubilee celebration of the Company during the year. • Basic earnings per share went up to Rs 37.68 per share, compared to Rs 34.74 per share in the previous year, recording an increase of 8.5%. Diluted earnings per share was 37.68 per share, compared to ` 34.66 per share in the previous year, recording an increase of 8.7%.

Key Business points:

• Your Company successfully completed the integration of teams acquired from IBM, as part of the agreement entered into with IBM during last financial year, to support and extend the IBM Continuous lifecycle Management and Continuous Engineering product suite. New sites were established in Guadalajara, Mexico, Rehovot, Israel, Ottawa, Canada and Edinburgh, Scotland during the year

• Your Company’s strategy to build platform based solutions has seen very good growth in the Salesforce and Appian business. Your Company is now a platinum consulting partner for Salesforce. Continuing the focus on platform based approach, your Company has partnered with Google Cloud Platform, Amazon web Services, Dell Boomi and this should result in good growth in business in the coming year

• This year, your Company continued with the Technothon initiative, where the campus hires work on new technologies (IoT, Machine learning, Block Chain, Dev Ops, AWS, MEAN Stack, full stack). They build and exhibit end-to-end mini-projects. Around 80 such mini projects were exhibited after the ETP.

• Hosted very large databases conference in India after 20 years

• Partnered with 25 government Ministries to conduct a hackathon

• Company got recognition from Zinnov, Appian, Oracle, Forrestor, IBM.

Key business focus for future:

• Company will leverage our global footprint to address the opportunities in the digital and IoT space which require presence closer to the customers.

• Committed to increase the enterprise value with focus on efficient allocation of resources and increasing the share of solutions-led business, while continuing to invest in growth areas.

• In line with the market demand and the need to focus on IoT, your Company brought together market-facing IoT groups from the Alliance and Accelerite as one unit. This will strengthen the IoT offering by leveraging the IP, solutions and device and sensor partnerships across a wider set of platform partners

• Your Company has signed a strategic collaboration with Partners Healthcare to develop a new industry-wide open source platform to bring digital transformation to clinical care. This four-year collaboration will bring together the world class clinicians and researchers at Partners HealthCare with your Company’s innovative healthcare technology and product engineering expertise. The co-developed digital platform will be based on SMART (open, standards-based Technology platform) along with FHIR (Fast Healthcare Interoperability Resources).

• Your Company has partnered with USAA, a financial services provider that serves members of the US military and their families. USAA has been an innovator in securing authentication and financial transactions through a process that extends beyond user passwords and security questions. The development and intellectual property rights granted to your Company stem from innovations that USAA uses to identify and verify members, while also protecting their privacy. Through this agreement, your Company will extend these technologies and address a growing market opportunity for digital security products and solutions in the financial services industry. Your Company will focus on authentication and security solutions based on concepts such as micro-trust, risk-aware, contextual and personalized, in conjunction with technologies related to biometrics, risk modeling and dynamic proofing.

• We will continue to build solutions for digital world using data at core of software driven business. We will invest in newer technology and pre-build solution for micro-verticals like healthcare, loan origination, KYC, Insurance claims, Digital media content distribution etc.

• Nonlinear growth through focus on IP continues to be a core part of our strategy. Accelerite has built a set of connected infrastructure products that help a modernizing enterprise realize its growth opportunities. We have developed Rovius, a private cloud that is available for use in hours instead of weeks and scale to support large ecosystems as big as public cloud with the same capabilities and ease of use

• Partnership with IBM is helping generate leads and your Company is setting up a center in IBM’s Watson IoT world Headquarters in Munich, Germany enabling better access to IoT Customers.

• We strongly believe that digital India will be significant transformation for India and has tremendous potential for us.

Human Resources:

• Your Company recruited 2,310 employees on a consolidated basis consisting of regular employees, trainees / interns, consultants, business consultants, contract consultants consisting of (technical and non-technical) professionals.

• As on March 31, 2017, your Company employed 9,460 professionals (including trainees and associates) on a consolidated basis spread across 18 countries. The technical strength was 8,808 employees which comprised among others, 4,969 graduates (Engineers and Technicians), 2,043 post graduates and 26 Ph.D.s. Your Company is going global and there was a significant increase in the distribution of overseas employees which now constitutes 15.97% of the total work force as against 12.28% in the last year.

• The median remuneration of employees of the Company during the year 2016-17 was ` 865,300.

• In the year 2016-17, there was an increase of 7.6% in the median remuneration of employees.

• As on March 31, 2017, there were 7,790 permanent employees who were on the payroll

• The attrition rate during the year was 15.69% which was less than the attrition rate of 16.43% in the previous year.

Key Risks:

• Protectionism is being discussed and witnessed in various countries and we are ready to address the same. Focus is on hiring of local talent and also enabling professional exchange programs for appropriate integration. Pursuing diverse opportunities also exposes the company to unfamiliar risks that many and difficult to evaluate. We have a robust model to handle Global Compliance and Regulatory requirements and an exhaustive risk management process to address operational risks those may prevail in any country or geography

• The Company derives a substantial part of its revenues in foreign currency while a major part of its expenses are incurred in Indian Rupees. This exposes the company to the risk of fluctuations in foreign currency rates. During the year, the Company has increased its global footprint whereby there is an increase in expenditure in foreign currency, which has resulted in a reduction in net foreign currency exposure. Accordingly, the Hedge Reserve (net of tax effects) as at March 31, 2017 stood at a credit balance of 208.44 Million as against a credit balance of 91.49 Million as at March 31, 2016. Please refer “Other Equity” under Statement of Changes in Equity in the consolidated financials for details. The balance in the foreign currency translation reserve was 73.65 Million as at March 31, 2017 as against 184.13 Million as at March 31, 2016, due to a translation loss of ` 110.48 Million on account of volatility in exchange rates of currencies in the financial year 2016-17. Please refer “Other Equity” under Statement of Changes in Equity in the

Consolidated financials for details.

• Customer Concentration: Dependency on few large customers can be a risk. Growth in the revenue from top customers further increases this risk. About 53% of company’s revenue is derived by top 10 customers.

Other Points:

• Mr Anand Deshpande is father donated 75% of his personal equity for charity

Yes, going by history, looks so. I am taking a bet on the future based who is better prepared for future and more agile to changes and I could be totally wrong. Also, I hold few more stocks in IT portfolio like tata elxi, accelya and Cyient. Its never about picking one stock but overll portfolio. The theme I am playing in IT when in last 1 year many have written off the sector is : mid cap against large cap, new gen IT vs old IT model, more product based focused (whatever available in India) with reasonably good financial quality and valuation

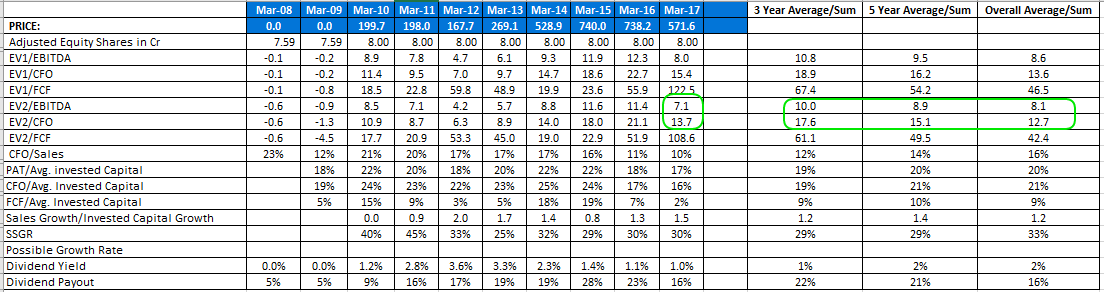

Also, specific to persistent, I think , apart from the data you have highlighted , I would like to highlight few more data points to give a longer historical tenure for a holistic comparison which may not look so bad for the price being paid considering future and last 12 months of activity (look at yield analysis of persistent vs infy for example)

There are reasons for last 2 years of weaknesss of metric which I believe has relatively lesser to do with body shop margin pressure and more to do with creating organization for changing needs of IT which I have tried to highlight through chaging product mix contribution to revenue, changing onsite offshore mix etc which looks more or less constant in a large cap like infy.

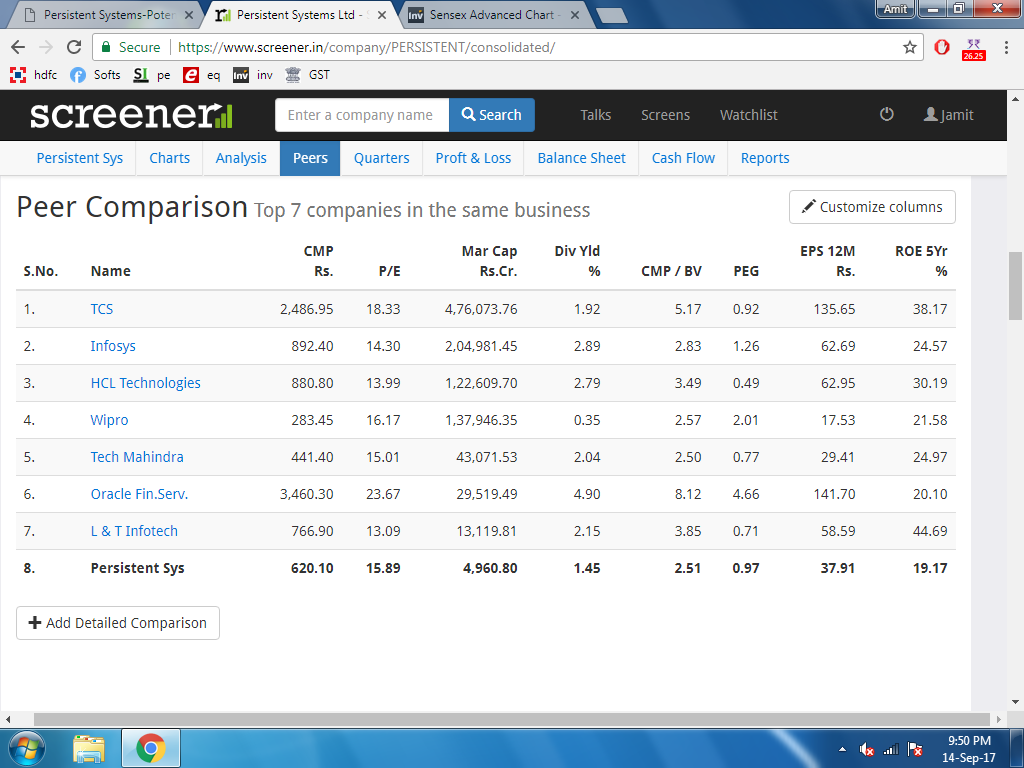

Persistent is a small cap company. Small Caps are sought out for their strong growth numbers, which clearly surpass the numbers of their larger counterparts. However, that is not the case here.

MCap of TCS is a 100 times that of Persistent Systems, yet, TCS is showing better growth numbers. Therefore, it feels more sensible, if in near future Persistent Sys or Cyient start showing much improved growth numbers then one would start moving capital into them. Until that happens, it appears risky considering the small size.

Its PE is about same as TCS (and others). If the price tag was super attractive, then it may be one factor to consider. But, currently, that is not the case.

Are you sure that TCS are showing better growth number than Persistent and Cyient?

As per you own chart the PE of Persistent is 15.8 whereas TCS is at 18.3. This a difference of 15%.

I think the central point is conviction of investor in growth. Do you believe TCS can grow revenue at 20-25% whereas Persistent seems to be doing so?

With due respect if you can quantify with numbers because I am not able to understand if you are taking 1,3,5,7,10 year view. Also, once we agree about history we can debate how future could be different from history. There is lot of scope to disagree qualitatively but let us be in sync first quantitatively. Please respond with clearly quantified metrics and why you are picking this metric and ignoring other metric (like why only 1 year not 5 year view)

Also, would suggest if you can share your views on traditional IT, newer IT, your views on quality of business of TCS and Persistent of traditional IT vs Newer IT, their revenue contribution to each company.Where you see better prospects of growth? Who is well poised to grow in the high growing areas, why so. I have tried to do that analysis of Persistent and Infosys through numbers to validate the same and to be unbiased highlighted the risks of persistent. So, request to take this discussion forward with clearly quantified numbers , metrics and rationale.

In case you disagree with the inferences I have tried to make through analysis in above post, kindly highlight disagreements with supporting data so that we can collectively get a better picture.

I understand your screener 1 year data to highlight persistent weakness on ROE and margins (revenue is better on all year views i ve shown) and in my post I have tried to highlight why margin looks weak.

Hi Saurabh,

Really like your detailed analysis of Persistent. It would be really helpful, if you could narrow down your thoughts (just like a tweet  ) and bring members attentions to focused point you are trying to make. How are you looking at the future and where do we need to monitor/put check points to know if the company can realize that future.

) and bring members attentions to focused point you are trying to make. How are you looking at the future and where do we need to monitor/put check points to know if the company can realize that future.

Thanks. Please ignore if not relevant.

I am not too good at analyzing a stock, and definitely not an expert on IT sector… but I try.

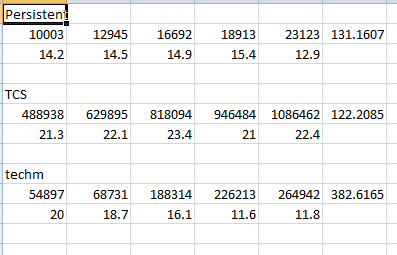

These are sales and Net Margin figures. Persistent is not stellar in sales growth, only 131% growth in four years. TCS is tad behind, 122. But, TCS gives a lot of predictability as a large cap stock.

The Net Margins are also very low. So, I do not see the advantage yet.

This article from IBM blog talks about IoT Continuos Engineering. I think this is the area where Persistent partnered with IBM. Looks interesting.