Hi All,

This thread is to discuss stocks which are in my watchlist and/or portfolio.

Hi All,

This thread is to discuss stocks which are in my watchlist and/or portfolio.

Added few Bajaj Corp today and in last few days around 205 level.

This thread is for discussion and suggestion from valuepickr folks.

Updating it with your watch list and stocks you bought without giving your analysis and rationale will only clutter and spam valuepickr .

I meant individual’s portfolio suggestions and discussions .Mere updating everyday with only buy sell detail without putting the rationality forward will be futile

Dear Sourabh, Good to know Value Pickr community hasvigilantmembers like you. This thread I have created to discuss about my portfolio stocks/companies and get valuable suggestions from ValuePickr community on stocks mentioned. Discussion includes anything including reasoning. I want to assure you that this thread is not created to posts my daily buy/sell.

**

**

There are two aims for creating this thread

**1)**From valuable feedback received on those stocks/companies from ValuePickr community, I will do course correction before it is late.

**2)**maintain this thread as an investment dairy and so I can take mylessons (mostly fromfailures) by peeping into past posts.

Buying Bharti Airtel below 300. It fits the bill of “Relatively Unpopular Large Company” theme.

Positives:

)- Leader in sector it is operates: No 1 telecom operators in India.

)- Professional management and ethical, first-generation promoter.

)- Valuation are attractive.

Triggers:

)- Voice call tariffs are in upswing so even little increase can increase net profit significantly given volume growth they have.

This forum is for mutual sharing of thoughts. If you want a one way gains from seniors without putting your rationale behind your buys, it will not attract seniors to share their thoughts. Here you have to build your own credentials.

Dear Manish, Agree with you. I will take some pain to gain more.

One reason for being bullish on Bharti Airtel: profit rises first time in last 4 yrs. It has woken up from long slumber.Rise is attributed to a lower competition and higher voice call prices and seems very good turn around story.

Just wonder what effect will introduction of voice feature by Whatsapp will have on voice call rates for these Telecom companies?

Whatsapp and other messaging services have killed SMS revenue for the telecom operators. Now they will have to find new avenues of revenue once voice call feature becomes prominent.

One stream of revenue is dying and new will emerges. Free Voice appswill give rise to data consumption and they will make more than loss in sms/voice revenue stream. Once these new streams of revenue will stop emerging, such things will be realexistentialthreats and hence for this reason it should not be bought and hold forever.

Anyway, You play such"Relatively Unpopular Large Company" for20-30-40% gain and then you move to your next"Relatively Unpopular Large Company"prey.

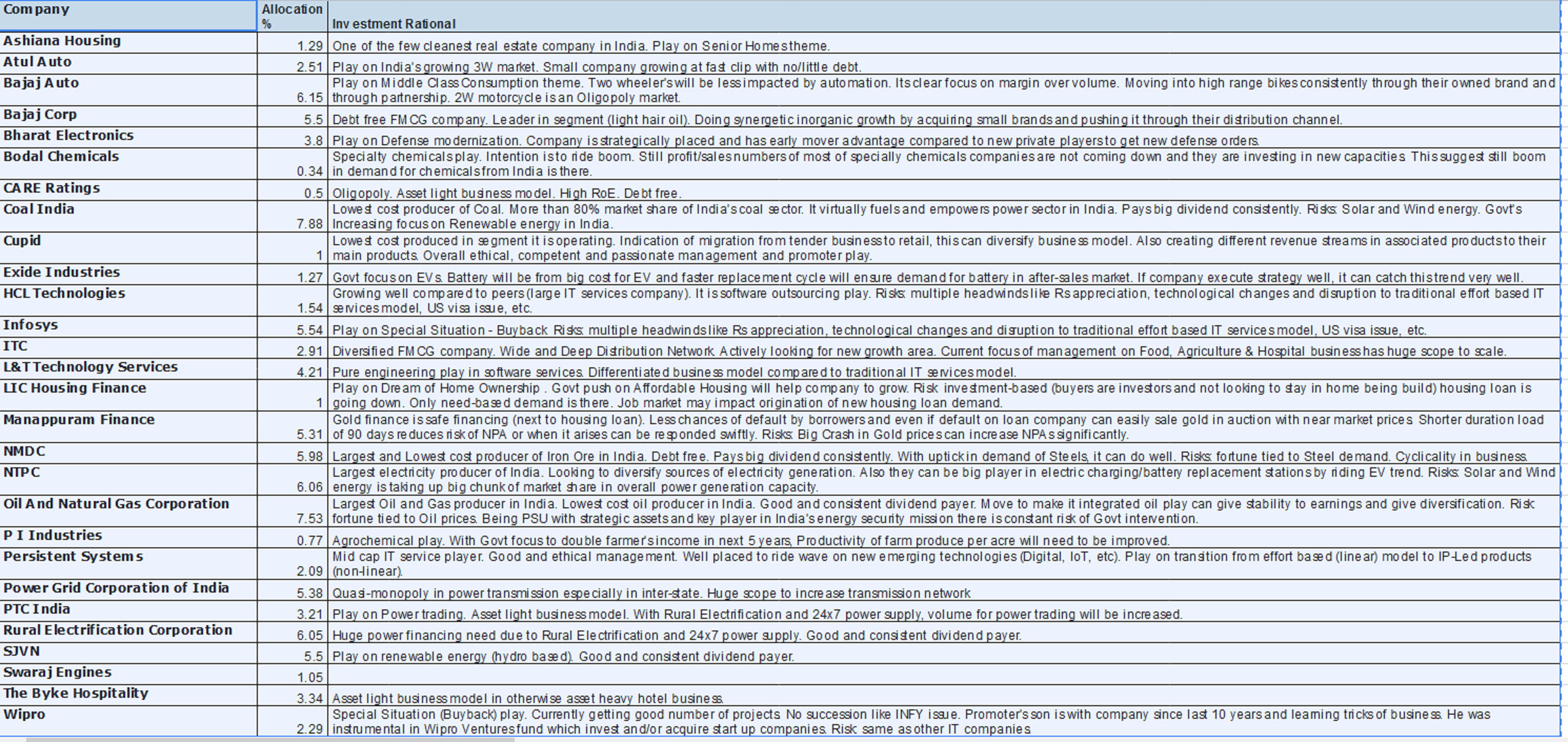

Attached below is a my current portfolio. Most of ideas (especially small/midcap names) are sourced by reading from VP forums and respective threads are available in respective VP forums.

Due to past bad experiences (more than 5 years back) from small/mid caps and good and positive experience from large cap, my portfolio is heavily skewed towards large cap stocks.

Going ahead, looking forward for good experiences and more gains from small/mid caps as that is the space which can help to generate big alpha over index if tracked and understood well.

So far I was not reading annual reports, earning con calls, analyst call of companies I am invested in. But now with increase in portfolio size (mostly due to new surplus fund from Salary added to portfolio and less due to return from already invested funds), I am keen to read annual reports, con call, etc., at least of companies I am invested in, to learn and track about businesses actively and build own conviction rather than borrowed conviction. As per transaction data and taxes paid on LTCG and STCG, last 4-5 years performance is positive and index beating with wide margin considering only invested fund into direct equity (i.e. excluding cash, debt funds, etc funds waiting to be invested.).

Request VP forum members/senior investors to scan portfolio and provide valuable suggestions/feedback . All suggestions/advice, positives and negatives, are welcome with open heart. I will learn from suggestions/feedback, integrate learning into my investing operating system and adjust my portfolio accordingly.

Can you share your expectations from your portfolio ?

Around 40% of your portfolio is from PSU’s.

Another 10% is from large cap IT sector which is already having tough times.

In my honest opinion, you are having many stocks with less than 2% of allocation which does not make any sense.

You need to work on asset allocation first of all. Also need to ask yourself that if Bodal chemicals or CARE ratings becomes even 100 bagger from here on, how much difference it is going to make in your overall portfolio. It would be negligible.

Maybe you can classify your bets based on earnings and profits conviction in near future and allocate more funds to your high conviction ideas by trimming positions in those stocks where allocation is very less.

Hi @saurabhricha

Thanks for taking time and screening my portfolio and providing valuable feedback.

Please review my thoughts on your feedback and let me know if they are inline with your thinking or you recommend further course correction.

I have mentioned in my rational that Infosys and Wipro are Special Situation play. For Infosys I assume 40-50% acceptance ration and for Wipro I assume 70-80% acceptance ration. With this allocation % to IT sector will be reduced by 40%. After that I will take call how my allocation should be. As sector is not doing well I will try to not to increase allocation.

Yes, you are right. my portfolio is skewed towards large cap in general and PSU stocks specifically. But the thing is PSU stocks, luckily, has given me handsome total return (dividend and appreciation). So I am OK with higer allocation % for now. Also, some of stocks (Coal India, NMDC mainly) were/are in cyclically downtrend and cycle is hopefully turning around at least for NMDC. With increase in stock price in them I will book profit gradually which will naturally reduce allocation % towards PSU stocks (by the way I am selling PTC India to book profit and take advantage of sudden run up). As I have mentioned I was not actively tracking small and mid cap space as have to spend more efforts and time in tracking them compared to bigger names or PSU stocks for that matter. Now, I am readying myself to spend more time and efforts on small/mid cap names so I will have good number of names in my track-list/watch-list which I can use to buy in next correction or crash, whenever it comes, in overall stock market.

Agree with you. My target is to have 80% (core portfolio, high conviction bets) allocation to 15 or less stocks. Rest 20% (satellite portfolio, low conviction bets) allocation are kind of experimentation or short term play. Satellite part of portfolio is tail part. Occasional multi-beggar in it does not make much positive difference to overall portfolio at the same time, on positive side, dud in it does not make negative impact on overall portfolio.

Completely agree. 100 beggar with 30% allocation makes life. 100 beggar with less than 3% allocation may make career (only if you are investment professional as you cans how record and attract more clients). 100 beggar with 0.5% may makes only one year rosy and then life as usual.

I am convinced on your idea of having and maintaining positive correlation between conviction and allocation %. I will definitely work on this. Higher allocation % should reflect high conviction and vice versa. Conviction (self and not borrowed ![]() ) building is definitely a thing I need to work.

) building is definitely a thing I need to work.

Again thank you very much.