It is a PHENOMENAL idea to create a Long Long Term Portfolio.

All young investors or new investors are buried into the disruption of the world and companies going ‘poof’.

This does not happen to LnT, Tata Motors, HUL, ABB, and others, and even if it happens, it will happen to one of them, and the ones who are traders will say ‘look I told you’.

Even since 1999 there has been many that has gone “poof” (gone away), but they are just a handful like Lehman, Enron, Global Crossing and a few others in the US. In India, we have Satyam, PNB, Vakrangee and a few others that have given trouble esp. in the mid-cap category, but the rest have been OK and survived. TWO huge bear markets in India and only a handful gone (don’t talk about SmallCaps).

In short, I would ONLY pick from Nifty 50 and invest in the stocks of Nifty that you understand well. So, if someone says Infosys is going down the drain due to USD, you would be able to tap into your conviction and buy more when it dipped to Rs850.

In addition, the Nifty 50 is going to give you dividends with some regularity which none of the mid-cap and small caps will be giving, and hence you want to have these companies and then reinvest the dividends into other companies.

Make sure you make the portfolio script selection large enough that it acts like a Nifty50 on steroids. That means you need your high conviction small and mid caps added to it also.

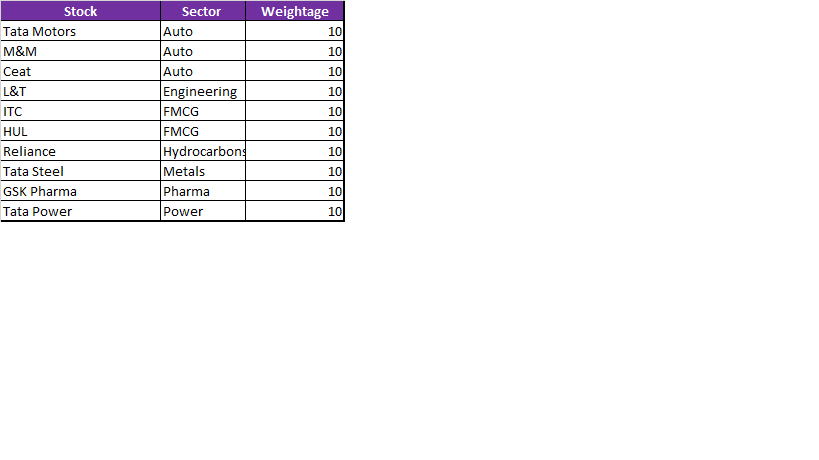

9: Lifestyle (12%): Tataglobal, United Spirts, Montecarlo, Cox & Kings

10. Real Estate (4%): Mahindra Life space

Leave enough space for new things if they emerge earlier than expected: 1. AI 2. Crypto 3. New transportation models (Electric mobility, capsules…) 4. Green technologies…

I think we all biases towards our favorite companies and invariably end up over-investing in them

without considering that black-swan events, unknown unknowns and competition can catch up to the best of breed.

Hence, it would make more sense to take a basket approach to minimize risk of permanent loss to our portfolio from events that cannot be forecast, especially when trying to forecast 20-25 year returns. 10 companies may be too few. Eg - I have invested in 5 HFCs even though I consider 1 one of them to the best of the lot. The hope is that they will atleast give me sector performance over the longer term

The longer the time-period more the need for diversification and choice of business that don’t change very quickly. Implication: Have to choose very stable businesses with multiple sources of revenue that are very very hard to displace.

Thinking like a businessman may make sense in this approach - how long will it take for me to get my capital out of the business so that there is no permanent loss of capital for me in the longer term. Although we cannot withdraw profits from a listed company like our own businesses, at least high dividend paying companies may provide some return of capital. Eg - Indiabulls housing has 50% dividend payout to its investors. Disclosure - invested

Companies that show quick adaption to their external environment and seize opportunities over a long period of time may be more suitable for longer investment. Eg - HDFC and its subsidiaries. Not invested. Eg Muthoot finance - 100 year old business that has adapted and come out of heavy challenges many times and grown stronger. Invested.

Its an interesting thread. Based on discussion with people from US/Europe, I find that they realized this buy & hold strategy much earlier (as it depends on stock market growth and investors maturity/education).

From the thread its clear that most participants want to hold primarily large caps/front-line stocks for long long term, then why not consider ETF (at low cost depends on stock selection by index provider) or active MF (slightly higher cost but active stock management).

Unless the portfolio is concentrated and few stocks outperform the Sensex/Nifty significantly, it is difficult to generate alpha over sensex/Nifty return. Indian market has not reached stage yet where MFs cant generate alpha.

So my strategy is to hold MFs over long term while looking for value stocks (multi cap but primarily small/mid) to ride the cycle and exit when valuations are rich.

One interesting theme I observed on this thread and seeing others post on twitter is related to ‘Disruption’. My personal take is that we have skipped a few steps and started mistaking ‘Evolution’ for ‘Disruption’.

If commute has moved from foot to horse cart to steam engine to diesel/petrol engine to solar/electric powered it does not mean the prior industry got disrupted so to say. The basic need of commute/transportation got solved more efficiently and thus evolved from one form to another. Both co-existed for a long period of time ie decades. Industry participants evolved in this period. Did Ford disappear? Let’s extrapolate, will Maruti disappear or Ather take over Honda & Hero? I am just thinking out aloud honestly.

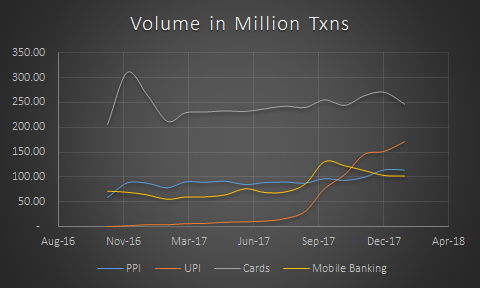

Disruption is quick and brings substitutes to a halt abruptly whether making it uneconomic to operate or redundant. For instance from 90s till maybe ~2012 SMSes were the primary way of non voice distant communication medium, how did whatsapp change this need. It didn’t utilize the same form of technology essentially. Today ~95%+ android phone users have whatsapp which they open everyday. How many send smses everyday now? In a matter of few years SMSes got disrupted and whatsapp took over. Today in the VP Bangalore Whatsapp group I see a lot of people sending money via UPI. Imagine what power payments on whatsapp will be. Will card usage decline? Will it be disrupted? I guess yes.

Now coming to specific data points/examples.

Look at UPI txns uptake below.

I see everyone is applauding HDFC bank’s one slide on digital banking. It is not disruption. I suggest to look at decks of RBL, YBL and Kotak too. Specifically Kotak. Goto https://developer.rblbank.com/ and see what kind of work RBL is doing. The banking space is evolving or rather has been evolving.

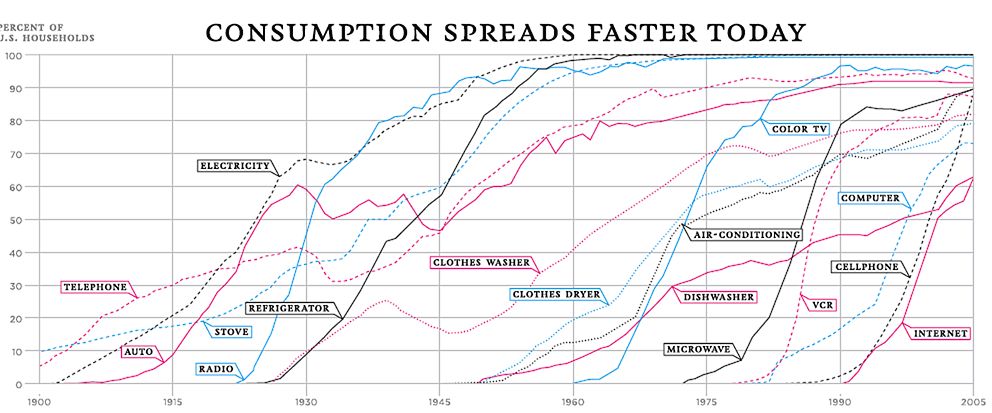

Have a look at the adoption rate of technologies. Though this is pertaining to the US market it can be used as a yardstick. 2-3 years is a very small time frame to disrupt a business in most of the cases.

By no mean I am trying to say technologies cannot make incumbents obsolete but it is associated with a probability which would be low. And the big players do evolve to adopt new tech. But there will always be Xeroxes and Kodaks.

Apologies I have not added on what my permanent hold portfolio would be, others have pointed out very good ideas. Liked the way @shreys put forward his way of thinking. I have my biases and I am quite sure I will not be able to hold any company for 10 years even though I should.

Sakaat points Venkatesh ! Glad to see really forward looking thoughts here and not the current favorites being part of 20-year portfolios with the assumption that they will continue to prosper as they have thus far. You are right that Maruti, M&M, Tata Motors will unlikely go out of business in next 20 years, but what if the disruption comes not from another auto technology, but from Rapid Mass transport? Namma Metro has already caused at least a few of my acquaintances to postpone, or cancel car upgrade plans. What if the aerial transportation, or rent-a-bike for last mile solves the transportation problem? From a 20 year perspective, I’d bet MRF which is the auto equivalent of selling shovels to the India gold ( car) rush! Tyres or wheels have been around for a few millenia and while materials might change, the basic circular motion is here to stay for next 20 years! Any shift in passenger commute preferences would hit Maruti harder than say a M&M or Tata which has CVs, Defence portfolio. Tata of course runs the Jaguar stable, which is altogether a new variable and panders to a different set of customers.

On banks, yes, disruption is upon us at least in terms of payment and intermediaries. Deposits and disbursals are yet to see that, but those will follow too. Bank of America has recognized the threat of cryptocurrency in its filings:

“[T]he widespread adoption of new technologies, including internet services, cryptocurrencies and payment systems, could require substantial expenditures to modify or adapt our existing products and services,” the bank said.

Perhaps I missed it, but I did not read an equivalent statement in HDFC Bank AR. Bank of America has one of the highest patents filed in Crypto-currency, so one can be sure that BoA is making attempts to survive and thrive in the new planet Crypton.

Interestingly, it appears not many people seemed to believe Insurance is something to thrive in next 20 years. As and when such opportunities are available, Education for profit may present opportunities for long term investment as well when such institutions go public.

This is a rewarding and yet simple strategy to hold the index for the long term (or an actively managed fund) and use market downs to load up on mid and small caps. We know that the index constituents change over time, and that some companies get added, while some are removed and we know the reasons as well - they lag capitalization growth and are overtaken by faster stocks and eventually are dropped. This means that at any point in time, there are laggards in the index, and there are replacements available outside the index basket ready to step in. This gives us two rules to construct the 20 year portfolio.

Avoid laggards, or minimize their inclusion in the portfolio.

Include fast growers outside the index

Simple, isn’t it?

So I did an exercise of Sensex Stocks going back to 1992 and picked a few of them that have survived the next 20 years and see if it makes a difference versus picking the index at 1992. So what stocks did I pick?

What did I avoid? Bombay Rayon, Century Textiles, Premier Automobiles, Hindustan Motors, Philips, Gujarat State Fertilizers, Ballarpur Industries…

Now take the index stocks picked in 1992 and compare its performance with the index. The current index has included such stocks like Infosys, TCS and everyone’s darling HDFC Bank.

Isn’t the result astounding ? The mere act of picking survivors has given index beating returns over the next 25 years! Did one know Premier auto and HM would not survive and Tata Motors and M&M would back in 1992? Does one know which of today’s sensex stocks would survive next 20 years? That is the question we want to answer here!

Excellent thread & good portfolio @dcoolsam. Just a couple of points I would like to make, for such a portfolio like you have already figured and others have pointed out the industry needs to be one that will sustain for 20 years. One vertical you missed out is insurance (though it is indirectly there thru HDFC & Bajaj). Given general industry features & return ratios, low level of penetration, growth potential in India and existence of strong managements this is a industry that is a must in any long term portfolio. Valuations may look expensive currently but from a 5-10 year perspective (leave alone a 20 year one) this will not matter. If nothing look at the exposure that Buffet, the baap of 20 year portfolios, has to the sector.

Also in FMCG, i would suggest ITC over HUL, i work with most of the FMCG guys, I find most of the MNC players have a very short term “make immediate profit or get out of the business outlook”. While this may look attractive on paper i think this causes them to miss out on major long haul opportunities, which is why HUL has made such a mess of it’s foods business. ITC on the other hand keeps a very long term outlook (5 year+) for any vertical it gets in, which will serve it well long term IMO because FMCG is essentially a brand building exercise. You spend on the brand initially and reap profits over the long run. Admittedly it is able to do so because of the huge cash cigarettes generates but as an investor that does not matter to me.

The comparison is interesting and throws unbelievable returns for stock picking over sensex. While 2008 till date ~9 times return is too good, I remember the fear in mind at that time. Stocks which I picked during that period (Abbot, oracle) multiplied much more. Comparison since 2013 shows real delta over sensex. ICICI Pru value discovery fund generated more returns (22.5% CAGR) over 5 year period, slightly better than stock picking.

Many times I ponder if the performance of my portfolio is worth it to spend lot of time in stock research. I found that my portfolio barely meets MF returns though i continue to invest (same amount as I invest in MF) more because I love investing including the high when the stock pick delivers.

Hi @sachinabhyankar

ETF is a good idea. I did this comparison few months ago. Most of the good MFs beat the ETFs. We need ETFs for BSE Small Cap to have a real alpha. AMCs are smart, they haven’t come up with ETFs following good indices so far. If Vanguard launches in India, they will make the AMCs run for money. Having said this, JuniorBees is still a very good ETF in my opinion. They have always been in top 25 across the timeframes. Check the screenshot below, they have favoured better than several MFs, Volumes are low though for ETFs in India:

Hi @deevee

Absolutely possible. Disruption is real and spreading fast. In the new age, companies might get wiped out within 3-5 years (Yahoo, Xerox, Nokia) if they don’t adopt. It’s scary the way you have put it, If maruti disappears, that would be real disruption. Currently 50%+ Indian cars are Maruti.

Hi @lastgenesis

I totally missed Insurance sector. Thanks for bringing that up. It needs to be added to the portfolio. I really like Bajaj Finserv, even though it’s not a pure play insurance game.It has proven management. I got an interesting forward today, it mentioned various PMS portfolios, most of the portfolios had Bajaj Finance and Bajaj Finserv more than 5% of the total size. No wonder the stock has always been expensive, except probably during DeMo. I find pure Insurance sector risky, their profits could be really eaten up if bigger claims come to fruition. ITC is a good play in FMCG. I fail to understand why it has lower PE multiples in comparison to the peers. Any idea about it?

Hi @arunsg Very interesting post and graphs. Sensex, Nifty and in fact all indices are momentum indices. They keep which are working and throw which are laggards. The strategy to follow could be: follow NSE 100/500 index, whichever stop drop out of Index, sell them off. It will definitely give better returns IMHO, but LTCG/STCG can be a spoil sport in this regard. Also, there would be a lot of churn in the strategy.

ITC IMO has lower valuations because a) cigarettes is a declining business and it is very susceptible to taxation changes every year. b) the other businesses till date have been taking up a huge amount of cash, with little profits. Cos like HUL, GSK, Marico, Nestle etc have mature brands, don’t enter new categories as often so generate huge amounts of cash which gives them their valuations, if you see most of these companies are also not showing great profit growth. The valuations are mainly for brand value, pricing power & great return ratios.

ITC enters a couple of new categories every year so while a Bingo or Sunfeast may be making money now, that cash is going into say a Yippee or a Fiama de Wills. But if I had to take a 20 year bet, I would say ITC FMCG will grow faster than the Colgates or HULs of the world, PE multiple will come somewhere along the way.

On insurance, I’d say life insurance doesn’t have much risk of huge claims at a time. General or reinsurance yes you need those pricing capabilities which as of now are unproven in the Indian scenario. Life I’d say is much more mature, euphemistically speaking one asset can only have one claim and big data is already creating the premium scenarios where the insurance company benefits. Poor analogy but in gambling, the casino always wins even if there is a jackpot on and off. In any case HDFC life is hardly going to be in an AIG kind of mess any time.

These guys are in a growth phase today but once the sector gains mass in 5-10 years it will be in the kind of virtuous cycle global insurance guys are seeing.

Hi. I am interested in building a core portfolio. I can contribute everymonth 10K-15K for that. What is the best way to build.

All the long term buy and hold companies seem to be always over valued. This deters our conviction for buying at such high price. Also at the peak of bull market, it is difficult to build.

All the blue Chip companies will always appear to be over valued.Bit if the time horizon is 5 years and above, most of them would give good returns. There would also be occasions when these blue chips will be lower by 5%to 15% depending upon sector individual company etc and then it should be bought eg bandhan bank highest price being 740 came down sharply to 612 two days back and then moved back to RS 700 in two days.Hdfc and hdfc bank are down by around 5% from their highest prices.

Wow going through this list makes me feel my pf is really on some tangent

That said, if MFs also invest in indexes, why can’t retail investors get into indexes directly without the MF costs??

I was recently thinking about creating a 50 year portfolio for my newly born daughter and was thinking about what will remain relevant after so many years. Its extremely hard to answer that question given that the pace of change in the world only seems to increase. We are very close to the point of singularity after which artificial intelligence becomes smarter than the human brain and change will really accelerate from there making the future even more unpredictable. Im note sure what will remain relevant but based on information available today and not too deep an analysis (my brain can see a lot less into the future than say Elon Musk!), it can be easier to determine which of these sectors are likely to become irrelevant.

The first that comes to mind is auto. Its clear that the world is moving into a sharing economy. That means that asset utilizations of cars have to go up (through the ubers and olas of the world) which will over a period of time automatically reduce the demand of cars as the same car is likely to be better utilized. However, more importantly, I had the good fortune of bumping into a pretty big VC investor in SF who was informed of the self driving car project at google and who mentioned that the car in its current state of technology (in 2016 ) can drive better than 80% of Americans. This number must be higher because it has been 2 years since. This is just google. Apart from them, apple and uber also seem to have made progress in this space. A sharing economy combined with self driving cars puts a serious question mark on the terminal value of Maruti into the future given that Maruti doesnt seem to be working on either of these areas currently.

I would have a similar argument with respect to Zee. It doesnt take huge forsight to see that the entire model of broadcasting and television is changing due to 3 reasons.

The ability to record and watch at convenience (Tata Sky) - with the exception of live events such as news channels or sports which are seen live, I feel that as more of the population adopts this, it reduces the ability of broadcasters to charge advertisers as viewers fast forward when ads come.

Advertising bucket of the world is common. Earlier there were avenues limited to hoardings, TV, radio, etc. However, over a period of time and more so in the future, digital advertising is going to consume more and more share of the overall advertising pie. It is going to become so much more targeted and hence will provide more bang for the buck. Take instagram for example. Its scary how specific the ads posted are. Traditional means of advertising such cannot match the efficiency of targeted social media and other online ads just because they have so much more data.

Netflix - increasingly the world is moving to on demand content. I think in the future, the world will increasingly move towards platforms such as Amazon prime and netflix. Enough has been said about it on various forums.

Again, I dont really see Zee as a company that will be able to adapt easily to these 3 trends. In general the headwinds down the line are going to be fairly intense again putting a question mark on its terminal value.

Whether these trends might take 20 years to play out or 50 or 100 no one knows. But 1 thing is certain. As time passes, it will start playing a more and more prominent role in the valuation of these 2 companies.

It is for these 2 reasons that these 2 companies will never form part of my 25/50 year stock list.

On a lighter note, self driving cars requires predictable and well maintained transport infrastructure (lanes, side walks, signals etc). With no sight of lanes anywhere in the country except for the NH, I don’t think self driving cars will have any future in India. So, my guess is Maruti will survive for a looong time at least in indian context.

Artificial intelligence never gets as smart as a human even in the next 25 years

India’s transport infrastructure doesn’t improve over the next 2 decades

Both of the above 2 points seem like they are not possible to achieve even after 25 years of improvement ( else after 25 years people will start seeing it as a possibility and risk affecting Maruti and pricing the stock accordingly)