PC Jewellers F&O settlement will be in physical mode from December contracts onwards. See NSE Notice. Will this help in curbing the volatilty in PCJ share price?

In their annual report they have not mentioned clearly about the revenue recognition policy. If they push the goods to their franchisee and record it as sales then the entire profit loss picture is different from what has been presented. On the other hand , if they claim to recognize revenue at sales then having such high receivables means only one thing - everything is badly cooked.(Receivables of TITAN as on 31st march is only 192 Cr.) Had it been the first case , the promoters should have started buying at present price as their is some value in the business. In second case they have no option but to keep faking the records and pray for some miracle.

Regards

Disc: invested and in loss

Own stores are 80 and frenchisee only 16 i think.

I’ve been going through the voting results for the recent AGM (here) and found that a significant amount of public non-institutional shareholders (~25%) voted against most of the resolutions, including the adoption of the FY2018 financials. Any ideas about why this might have happened? Are these disgruntled shareholders who were hoping for some better response from management about the low stock price?

Also if anyone here made it to the AGM, how was it?

The missing connection with Vakrangee was gold. It looks like auditors were complicit but why PCJ got involved except changing the colour of the money.

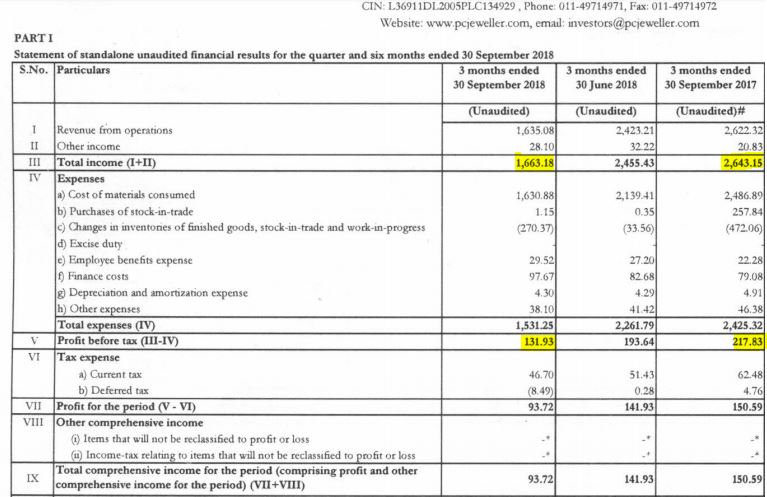

Q2 results out- Disappointing set of numbers but not sure how much of this is already factored in the price because of the crash from earlier this year.

Complete results here:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/edf5f377-57b4-49a9-bc0a-7ce92dfc84a4.pdf

Also there is a conference call today at 4:30pm for anyone interested.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/300f677f-27b0-4acd-bdc3-a40d89e629ef.pdf

Disclaimer: Invested. Tried to catch a falling knife and learnt a good lesson.

Investor call recording : https://www.researchbytes.com/webcast.aspx?WID=165512#audio

Management presentation on Q2 and HY1 results

I heard the concall. Overall I felt the management was not able to answer all questions properly.

Here is the summary of the discussion.

Issue 1: If the company is paying debt and reducing debt from Rs. 4064 crores to Rs. 3685 crores then why has the finance cost gone up from Rs. 82.38 crores to Rs. 90.08. Management was beating round the bush and not giving a good answer

Issue 2. The management says export business is primarily run on credit which leads to high receivables. The domestic business is primarily run without giving any credit. In this quarter the export business was only Rs. 85 crores vs. 771 crores in Q2-2018. However trade receivables have gone up from Rs. 1761 crores (March 2018) to 1976 crores now. This does not make sense. Management’s answer was not satisfactory.

Issue 3: Why do they have export business at all? If they are expected to get Rs. 1976 crores from the export business within say March 2019, they can close the export business and concentrate only on domestic business. However the management is targetting Rs. 2000 crores revenue in the full year from their export business.

Issue 4: In the previous con call (Q1) they had said that they would be reducing their debt by 1000 crores but they have only done by 400 crores. Management answer was they are going to do it slowly.

Issue 5: Why are they not buying their own shares? They did not respond and said NO COMMENTS

Issue 6: When Titan is growing at 30%, why are they saying that domestic business environment is not conducive and so on. In addition to this they have also increased number of stores. Management did not give any proper answer.

After hearing to the management and how they are handling the question, it does not seem that they are able to justify what actions they are taking and the numbers that they are showing.

Regards,

Roshan

8 Likes

Thank you for the ‘summary’, but you have hardly presented management’s view. Why were answers not satisfactory? What did management actually say?

Just wanted to highlight a few things on some good issues you have raised;

Issue 1: If the company is paying debt and reducing debt from Rs. 4064 crores to Rs. 3685 crores then why has the finance cost gone up from Rs. 82.38 crores to Rs. 90.08. Management was beating round the bush and not giving a good answer

Mgmt did disclose in their presentation itself and explained on the call as well the reason for increase in interest cost and I quote: "Finance costs - the company’s finance costs have increased in this quarter due to shift in the mode of utilization of its bank credit lines from SBLCs towards fund based facilities. This shift has happened mainly due to stoppage of domestic MGL facilities by various banks. "

Issue 2. The management says export business is primarily run on credit which leads to high receivables. The domestic business is primarily run without giving any credit. In this quarter the export business was only Rs. 85 crores vs. 771 crores in Q2-2018. However trade receivables have gone up from Rs. 1761 crores (March 2018) to 1976 crores now. This does not make sense. Management’s answer was not satisfactory.

While I agree that their responses on trade receivables related questions were dodgy at best, their intent to markedly curtail their export business is a step in the right direction. Further, to specifically answer your question as to why the level of receivables is higher - again they clearly stated in the presentation that it is due to marking to market the USDINR value from 65 levels earlier to 72 levels now. Again, I am not saying this completely answers the questions, but they did attempt to throw some light.

Issue 3: Why do they have export business at all? If they are expected to get Rs. 1976 crores from the export business within say March 2019, they can close the export business and concentrate only on domestic business. However the management is targetting Rs. 2000 crores revenue in the full year from their export business.

There were some suggestions on the call to close down their export business which management said they would consider. I suspect management is already pursuing that strategy except that they wont like to admit till they collect their export receivable dues as it might become difficult to collect them in case they announce that. However, we need to remain circumspect on this and need to watch what they do rather than what they say.

Overall, I do agree that management clearly did not deliver on their own objectives in terms of reducing debt, nevertheless the direction of movement in debt is still a mild positive. As regards to buybacks, I think they are once bitten twice shy with them not getting approvals from their bankers.

Disc: Invested, and hence views may be biased despite trying to be objective.

3 Likes

I am also a fellow boarder which is why I was looking for some positive from the concall but I could not find any significant positive. I also could not find the answers to be very objective.

On the export business part, they initially said Rs. 2000 crores is their target.

If the management acknowledges that Export business is not doing good at all and there are so many problems, why does it need to be suggested in a concall to stop the Export business. I just feel they are behaving unprofessionally and in a very immature way.

That is my overall take.

I’d like to add here that they did point out the reason why their receivables didn’t go down. I believe the older receivables have DSO of greater than 180 days which is why they haven’t come down (but I’m not 100% sure about this). But if it’s true, then it would make sense why they said that going forward “they will only target customers where DSO is between 60 and 180 days”. What I think is happening is that in order to reduce exposure to export business, they had to first effectively reset their customer base. That is also why there were such low sales in export business during this quarter. They have done ~800-900 cr of export business in 1H19 and will do another 1200 cr in 2H19. But that would raise the question: “shouldn’t this 1200 cr raise receivables again?”. Fortunately, this was also asked on the call and that is when they commented about the DSO of future sales in the export business (that future sales would have lower DSO, therefore overall receivables would still come down). They have already reduced receivables by 200 cr (they mentioned this on the call).

On the debt reduction, again I sort of get their reasoning (although I’m disappointed). They said that all the debt reduction came from cash on the balance sheet. Prior to the slowdown in the industry, they probably would have expected to generate more cash (presumably 200 cr) and used that to pay the remaining 200 cr. But since they couldn’t, for various reasons (credit crunch etc etc), they were forced to reduce it only by 800 cr. The cash that is now left of the balance sheet (158 cr) is the amount that is probably the minimum required to be kept as per loan covenants

While I am disappointed with the results, I do believe the new direction highlighted by the management is a huge positive. They still have to deliver but so far they started to show a few positive things. I think their “talk” on this call was believable. Whether they can “walk the talk” is a different question.

2 Likes

Thanks @patnaikroshan, @paramsv and @baadal791 for compiling your thoughts. Below are my observations based on limited understanding.

-

Issue of debt reduction target of 1000 cr not being met ( half yr target not Q2 target): Frankly, they were able to reduce it by 800 cr and i am fine with that (not overly positive but fine). Atleast it is a good positive step in the right direction and yielding results. No issues here for me.

-

Understanding what exactly they are doing with exports: Frankly i am a bit lost here. Is the long term strategy to completely phase this out ? if so, why still have a 1200 cr target for remaining yr ? or is it too just reset the base for a new collection cycle to start and for them to lower their receivables and then continue/restart exports ? I do agree with the last caller on the call, it is high time they look into shutting or spinning this unit off and concentrate on domestic sales.

-

Does anyone have info on average sales and expenses per store( both company owned and franchisee). I want to understand the economies here to see if they have same store sales growth or is it stagnant and only way to grow sales it to keep adding new stores…

The company also mentioned targets related to debt reduction, reducing receivables etc. As long as they meet or are even close to the targets, i would be a happy camper. My expectations are a bit limited given the price of the stock and i believe most negatives are built in (if the price was what it was in Jan 2018, i would be much more demanding on the management).

Disclaimer: Invested and hence opinions may be biased.

When the stock price takes a severe beating, the management loses all incentives to manipulate the results. Now, we can expect that the results are close to reality if not exactly true. I have a strong feeling that the export business has been actually a no business. It was just a tool to manipulate black money. It was used extensively after demonetization. A sharp fall in exports has no other justification.

5 Likes

Points to ponder before investing in PCJ for the long term

The Negatives:

- It is a Delhi based company

- periodic stock dilution, means the business needs more cash than it generates. Capital intensive. Its borrowings has doubled in two years. Looks like the management is taking in money in every possible way… coupled with the export business, appears shady.

- Working Capital changes is erratic. Mostly on the negative side. In Titan too. Where is all that capital going… could someone look into it? TItan does not need to raise capital for WC changes, and has eliminated all debt. But, PCJ is unable.

- ROE, EPS growth, sales growth, debt to equity the basic numbers are ok. But, the constant need for capital is bothersome.

Two things stand-out among all others:

- Constant Equity Dilution

- Increased Borrowings -> Increased Inventory from last year. Significant jump.

Increased inventory 1070 >> Profit before tax 736

- Sales are growing, but Cash from operations is disproportionate. But, same is with Titan.

This does not look like a business that doles out big cash. This is a cash hogging machine.

Sales are growing but the CFO is not showing that growth. Is because the company might be recognizing revenues when channel stuffing their franchisees?

I actually do not see the problem in this working capital issue. At the pace they’re growing, they should require huge working capital. It is because for every new store, they’ve to keep a lot of inventory, it’s a retail business.

Plus older stores will also be increasing their inventory size.

I saw this because I come to small towns … and the quality (as in 22 carats vs. 18 carats) of the gold given is quite drastic - from the stories i’ve heard. Hence a lot of people are flocking to these jewellery chains (rather than old standalone jewellery shops).

Though the non-confidence of the market on this company is unnerving.

This can be utilized as buying opportunity, general rule of investing, buy when blood is on the street. Apart from 2 % gifting or selling by promotors, nothing abnromal is found, PCJ opened 8 new store and shutdown 2. Current owned stores are more than 80 plus 15 frenchisee store. Margins are better than titan. Debt reduced by 800 cr. Export stopped to focus on receivables. Opening 95 stores is not a cake walk hence compitiin will be limited to 2-3 organized players. Titan quote at exorbitant valuations due to presence of marquiee investors. Titan vis PCJ PE is 65 vis 6. Fair value of business is quiet huge, risk can be taken on corporate governace issues,

2 Likes