Are there any indian FMCG companies that have the ability to increase prices by 20% for all the product categories they sell in one go , especially in backdrop of events that unfolded last quarter ? From what i understand , milk procurement prices have been depressed and benign for past few years in line with international prices and they have been going up recently , since there is no centralized mechanism for hiking milk procurment prices in the country they rise at different pace in different states based on local factors but ultimately converge after a time lag . Procurement prices in maharastra where parag procures bulk of its milk from have seen the rise last quarter . Other states where parag’s competitors procurement happens seem to be seeing a upward trend in milk prices now .This could have hampered its ability to pass on milk price hikes fully to some extent . Company has taken 8-9% hike this quarter , this is on top of similar increase they took for some major product categories like ghee etc in Q2. i will wait for end of june quarter before writing off the company.

I think more than the company’s inability to pass on rise in milk prices, it is the huge volatility and company posting an operating loss is what has spooked market the most. Given no other dairy company has been hit this hard. Also the sudden QoQ increase in sale of Skimmed milk powder which impacted gross margins also does not augur well. Moreover the management commentary in the concall left much to be desired so far that an investor vented his frustration on company’s reporting standard towards the fag end of the call.

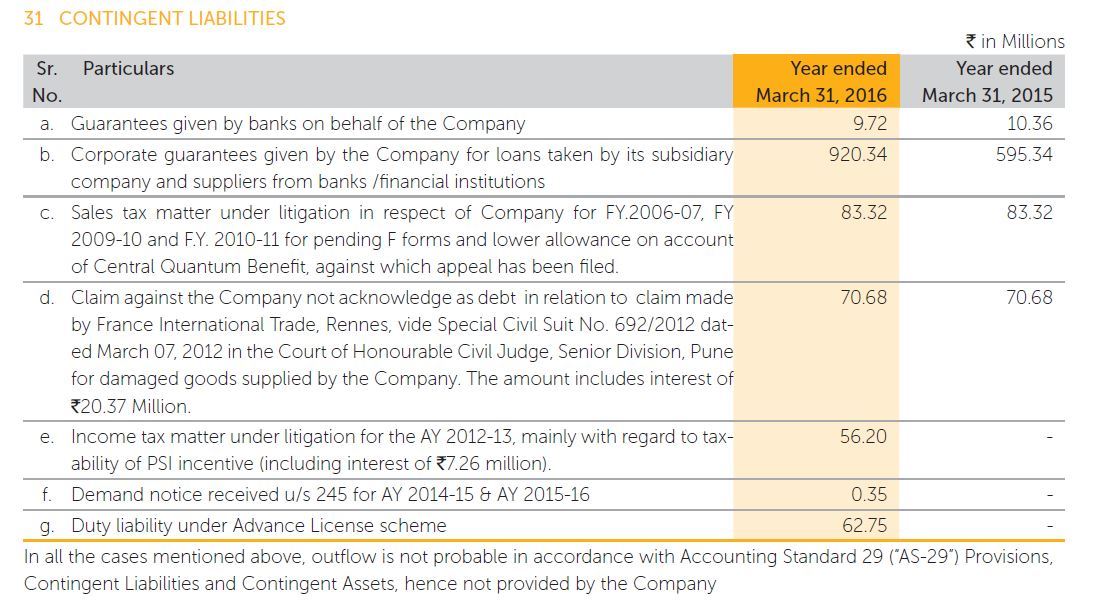

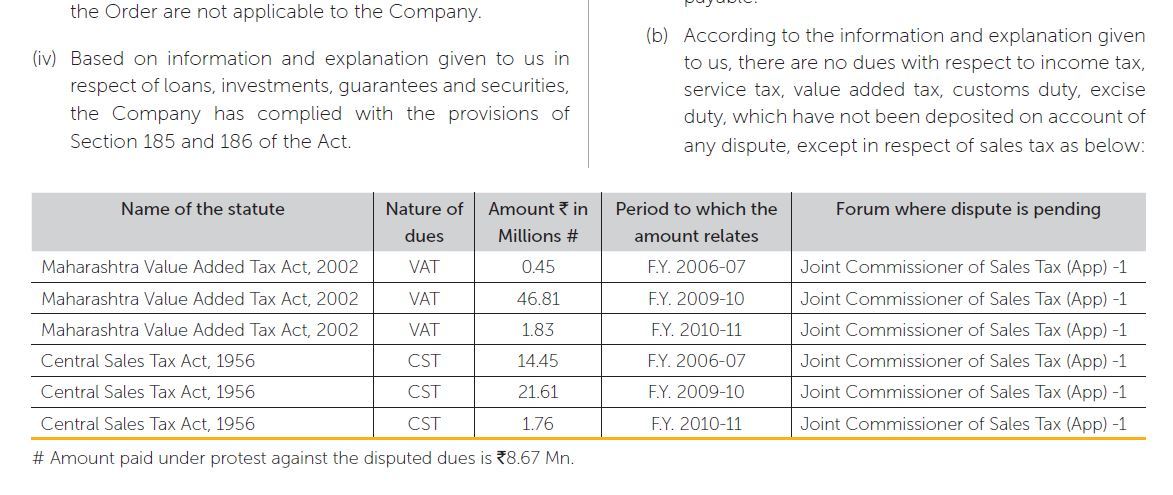

Company coming out with a recent IPO should have been more forthcoming on all pending issues and contingent liabilities. All the company mentioned in the AR 2016 was these

and Sales Tax disputes. But out of the blue company was hit by 164.94 Million in VAT from past years.

This reflects badly on Corporate Governance front.

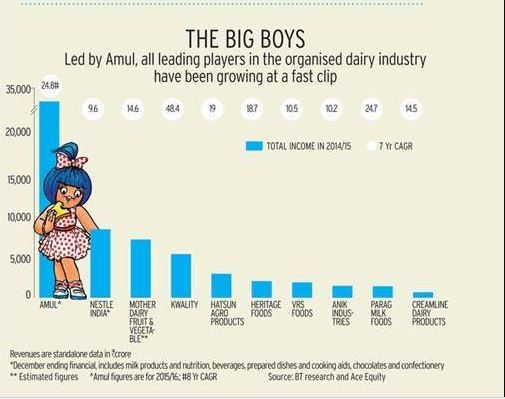

Understanding the dairy sector and competition landscape is extremely critical. We at VP, very often miss out on this aspect. This article gives some very nice pointers on the opportunity and with respect to Parag.

Here is the competition landscape and key players.

Backward integration is one key differentiator for Indian markets,

The fact that the value-added products volume is still picking up and the supply chain is so complex has often frustrated multinationals. it was these factors that led to the exit of Fonterra in 2001. While Fonterra is almost four times the size of Amul in terms of turnover, its strategy was just to procure milk and convert it into commodities such as milk powder or unsalted butter and sell it to dairy companies across the globe, which in turn would convert them into value-added products. This made it a high-margin business. But collecting milk in India was perhaps too much of a logistic issue for the company,

Varun Berry, Managing Director, Britannia Industries, agrees that dairy business in India cannot be viable unless a company invests in a collection model. “The dairy business of Britannia is a Rs 400-crore business and we are going back to the drawing board. We have ambitious growth plans in the dairy sector, but we will invest in a collection model.”

Parag knows it is a small player among the big bulls, hence it has differetiated in strategy while making sure, it has invested fairly well in the collection model of its own.

“Our strategy is to differentiate. It doesn’t make sense to take Nandini and Amul head on. They are too big and well entrenched in the liquid milk category since the past five to six decades. Therefore, we decided to move up the value ladder and grab the upper layer of that category,” points out Devendra Shah, Chair-man, Parag Milk Foods.

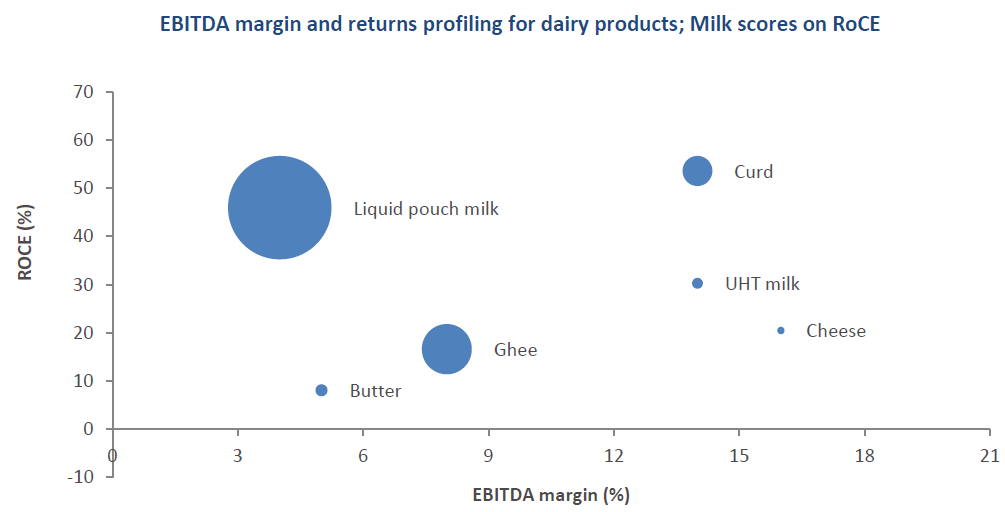

This report from Edelweiss gives very critical inputs on the industry.

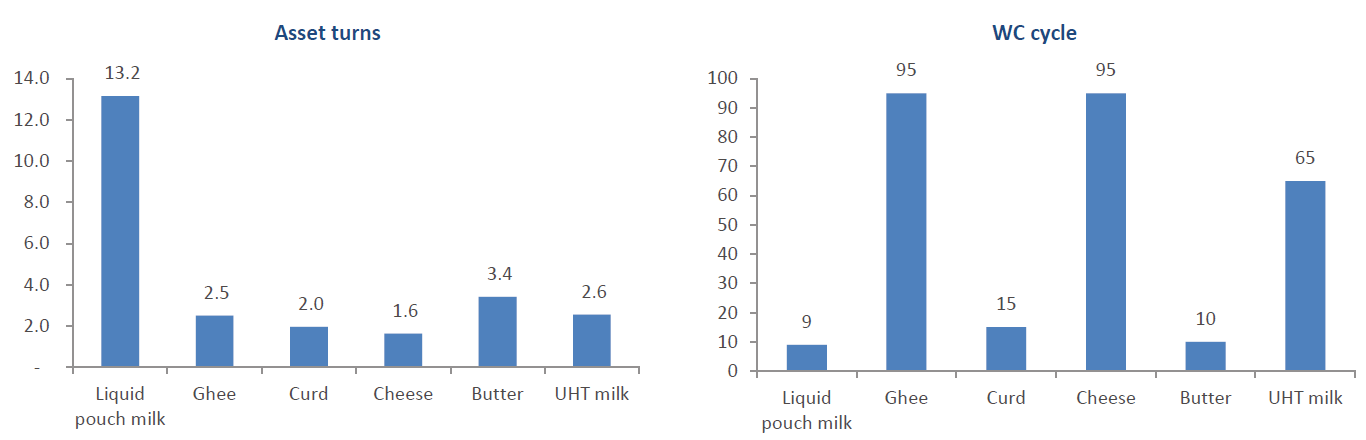

So while liquid milk appears to be the low margin commodity product every one is doing, it is the higher asset turns which leads to a superb ROCE and help as the cash cow to fuel the growth in other value added products.

There are mid shelf life products like Curd and Butter which yields 1.5-2X margin than liquid milk but are not a drag on the overall Working capital cycle. The key problem with high shelf life products - Ghee, Cheese and UHT Milk are they come with the double whammy - heavy capex requirement and very high working capital cycle from storage, production to the final high shelf life. Thus companies - like Parag - with heavy presence in Cheese and Ghee will be always weighed down by large working capital requirements.

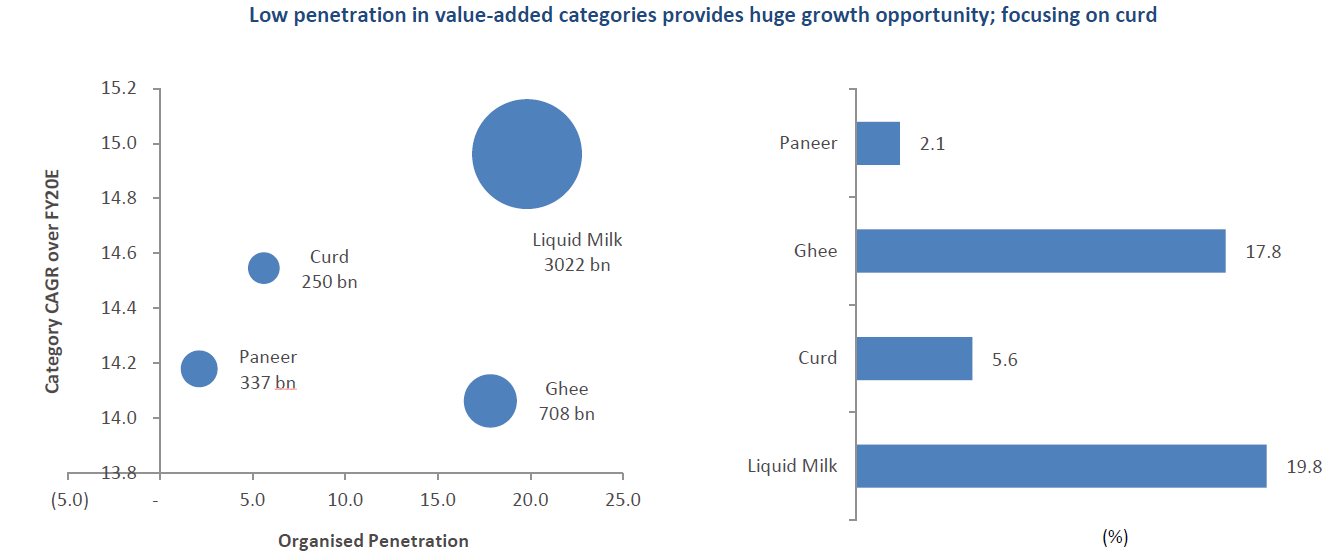

What then is driving companies like Parag into Ghee and Cheese ???

The size of the opportunity and very low organized penetration. Thus there is huge runaway for growth in value added products, but it needs to be prudently balanced with a optimal mix of low margin high asset turn milk sale.

I remember in one of the heritage food con call, mgmt spoke similar things why they are focusing more on curd in value added dairy n intentionally ignoring ghee

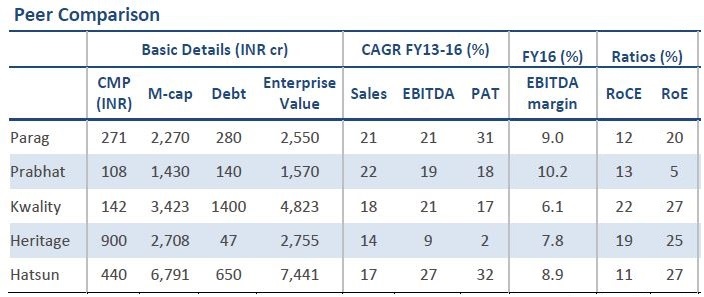

Yes, that part is pretty evident in the numbers too. Quoting from the same report see how the ROCE suffers for Prabhat and Parag - who are into high shelf life products. This is still without Heritage divesting the loss making Retail division, so the comparison will be even starker.

Ya, numbers speak  . Now, i think as loss making retail business is gone, nos would be even better (though not sure how the reliance dairy acquisition is going to impact the nos but opefully, should be better than capital eating retail). Considering Heritage has much better leverage position compared to Hatsun and Kwality, it would be interesting to see its ROCE,ROE numbers after 1-2 quarters. Disc: Invested in heritage, no trades in last 6 months

. Now, i think as loss making retail business is gone, nos would be even better (though not sure how the reliance dairy acquisition is going to impact the nos but opefully, should be better than capital eating retail). Considering Heritage has much better leverage position compared to Hatsun and Kwality, it would be interesting to see its ROCE,ROE numbers after 1-2 quarters. Disc: Invested in heritage, no trades in last 6 months

Parag Milk Foods is gaining traction in last 2 days. Anyone following this script closely please comment.

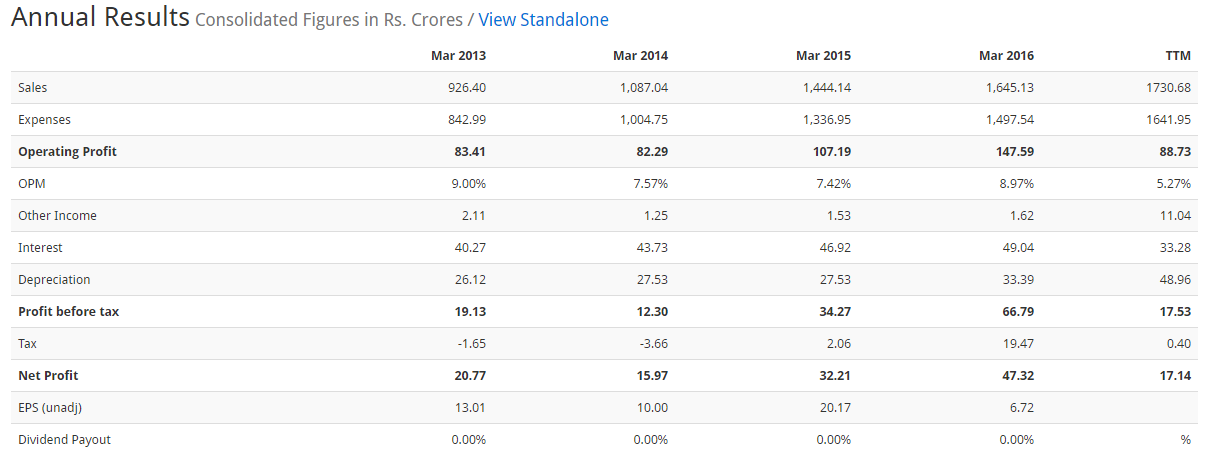

The financials of Parag Milk foods looks good.

Although the company is reporting repeated profits, it is not paying out dividend

Source: Parag Milk Foods Ltd financial results and price chart - Screener

I thinks it’s nice industry to play for a long term.

As demand will keep growing.

There is a huge gap between demand and supply currently.

Increase in raw material price can easily be pass on to consumer.

E commerce retailers have hardly any chance to play in this industry.

No discount need to be given if there are new enterents.

Milk and milk products to be consumed in a short period.

Hence short life of products.

Coming to Parag milk foods, currently the milk availed by them in market through Dmart is 9 to 10 RS. Cheaper then AMUL per litre.

Hope company would be making profit with this prices.

Company seems to be aggressive in marketing.

Recently

Also Ashish kacholia is holding the stock and has raised the stake QoQ. promotor has raised the stake.

Hello ASP,

Thanks for your response. Hoping Q1 results would be better.

There was an analyst/Institutional investors meet on monday July 17-2017, its also possible that analysts know something that’s not there in public domain yet, just guessing.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/b0fd3a7e-8e59-41fa-a2ab-1f0b7e173c80.pdf

there was also a large buy on monday for 10.5C @ 247.75 per share.

Yes indeed. What was the logic of considering state sale as interstate sale? If it was on the advice of a tax consultant, what liability is fixed on the consultant?

It’s a cool writeoff of ~193 million as exceptional item.

Explained by just 3 lines in Note 36 to the Annual Report of FY16-17

The P&L mentions note 36, whereas notes to accounts - relevant no is 37,

Auditors - Haribhakti & Co LLP, signing partner Anup Mundhra…

Why didnt it affect other dairy players?

Even though whey is growing at 7% globally and may grow at 10% in Indian. In India market is still very small. Even if Parag captures 20% market share by 2020 and assuming its dairy products businesses also grows at 20-30%, basically Whey will comprise of only 10% of their revenue.

Parag milk has posted decent results with top line increasing by ~17%. Bottom line isn’t comparables with previous year as the previous year quarter had negative profit.

But the best part about the current quarter results is that company’s PE has dropped from close to 50 to 25. So with PE at 25 and a good portfolio of value added products the company is trading at less than half of PE ratio average for peers which are trading at more than PE 60

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=75b010f4-5508-4284-af44-b526ae77bca8

In 2017 Annual report, the chairman(Mr. Devendra Shah) and MD(Mr. Pritam Shah) increased their salaries by 75% & 82% respectively. The best for any investor is 0 salary for promoter What is the opinion of experienced members on this?

Parag ropes in FMCG professionals to fortify leadership team

The acquisition of Danone’s dairy factory will help Parag Milk expand its footprint in North India and strengthen distribution of milk and milk products in Delhi NCR and Haryana, says chairman Devendra Shah

There was a news recently that milk prices have hit rock bottom in Maharashtra so much so that farmers are distributing milk for free. How does this impact Parag Milk Foods? Isn’t this an opportunity to make long shelf life products like whey powder and expand the margins?