Yes, looks like break down in Page is a signal that things will start looking better. Usually, in the last phase the strong stocks break down as people sell the ones which fell less in order to switch to more beta names to get that quick buck. This may be the reason why Eicher, Ajanta broke down today intra day. I may be wrong here!

Good that Page is holding 13000 on a closing basis.

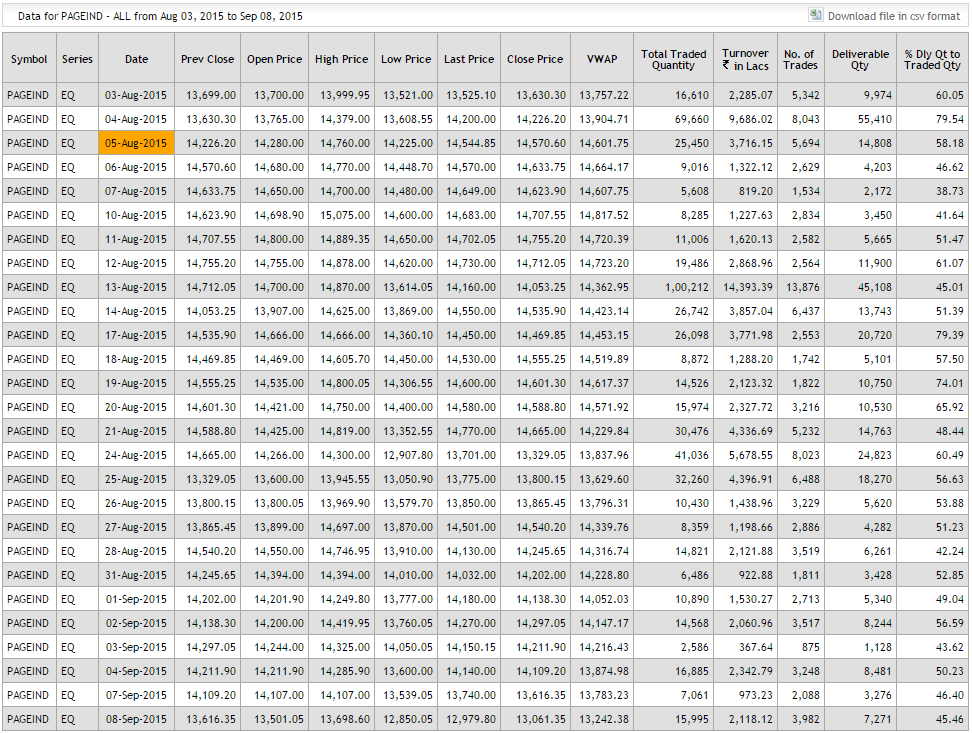

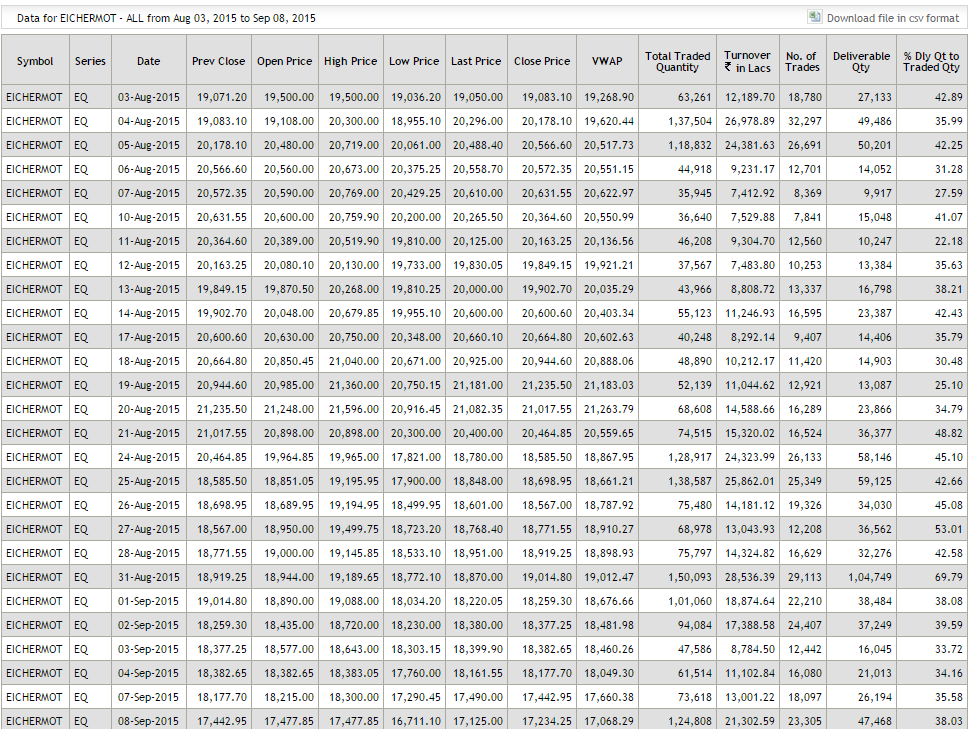

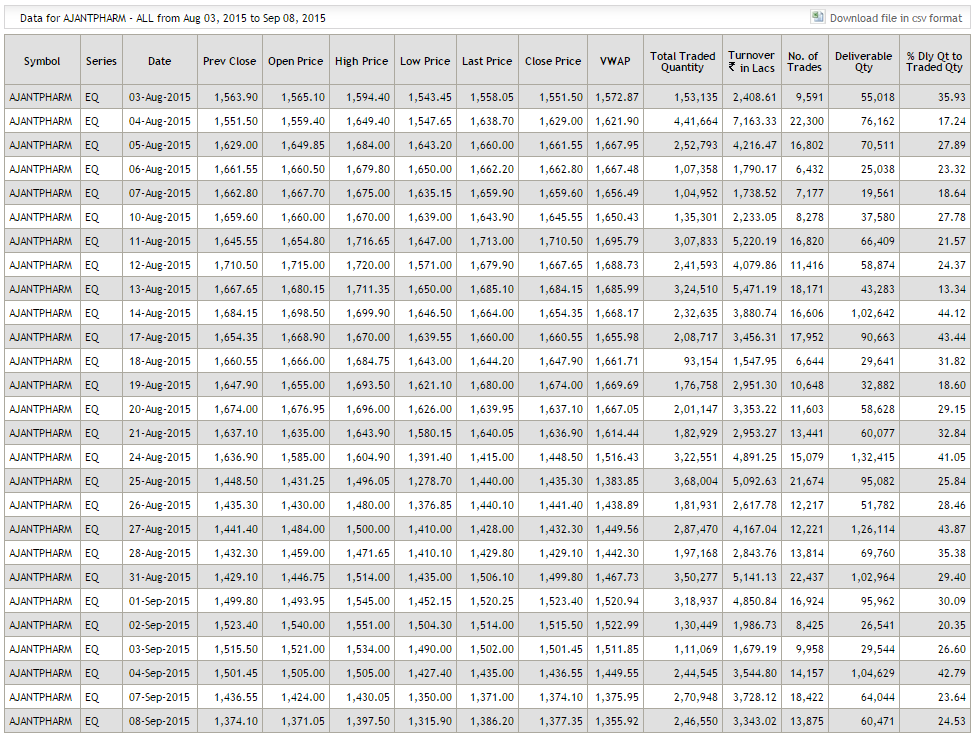

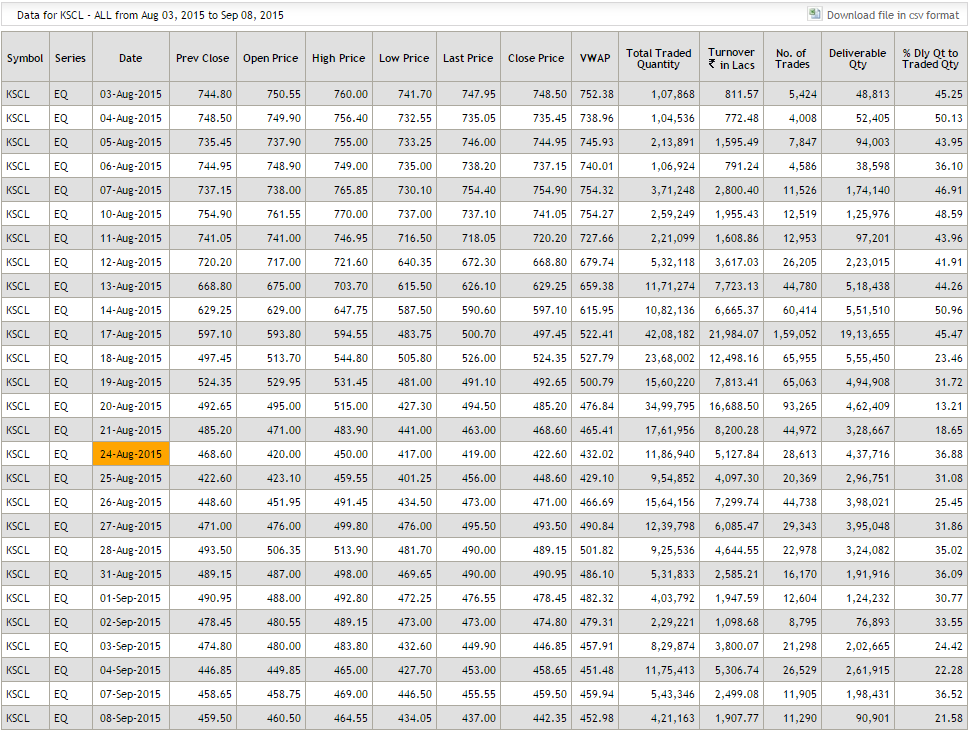

To aid us understand richdreamz PoV - here is the delivery details for the past month for Page, Eicher, Ajanta and Kaveri. Remember all are F&O listed stocks. Apologies for cluttering the post - unable to post the link.

seems to be very weak. continuously falling by about 2% every day. currently down by about 25% from 52 week high. still at 70 pe though. is the pressure due to some fund selling out?

Agree, it appears to be a bit weak. Since we are already into 6 months of FY16, may be we should look at FY 16 PE at which it is currently at about 54 PE (235 EPS approximately). Page can maintain around this level given its strong parameters of sustainability and predictability. Disclosure: I hold.

I feel for a quality company like page with a strong cash flow business model we should value it for FY17. I might give an EPS of 310-320 for FY17. so currently its trading nearly at about 40PE for FY17. If some wants to load it its the time to accumulate again.Disc. Holding it for a long (since 2010) and largest holding in the portfolio.

I got wrapped on the knuckles a bit, when I did comment once on price based discussion but yes, Page appears weak. I am very concerned since it has not fallen this much in recent times, from the peak levels…I am planning to add more (already my largest holding), if it comes around 12k

May be we should look at past data - Page touched 200 day moving average during the August 2013 correction. The present correction reminds me of that time. We are a bit below 200 moving average now and Page getting into F&O will have its impact on volatility both on the downside and upside. I think even on the upside Page could rise viciously.

ya it could rise viciously provided it again start to run on the same 25+ sales & growth track. Actually last qtr. result was the main reason why its soo weak. Moreover everyone is waiting for a imaginary fall of Nifty towards 6800 and delaying the purchase. can’t find a fault there.

Absolutely agree with you, 16% sales growth for the last quarter is on the minds of the investors. Management has clarified (hopefully, they are right) that it is one off and growth should resume from Q2. Given that it’s at high PE as well market is taking its time. But once Q2/Q3 provides the normal growth Page usually sustains, the price should catch up - as you rightly said.

I usually go back to what was said in investing books during these times (Buffett, Lynch) - there might be quarters where the growth may be a bit slack but companies of Page QUALITY generally over time recovers. This is usually a good time for accumulation.

This is a market where Nestle with a growth of 10% and problems like Maggi is valued at 43 times earnings why not Page with better industry position and business quality trade at 70 times? For me Page is a business that must be held for many years to come and it would be premature to sell it out citing valuation. For people who don’t have it yet in their portfolio it is entirely their call to buy at this valuation because the market is full of opportunities and there are always other ideas that can provide valuation comfort. Disclosure: Invested from lower levels

right. in the past, it used to fall by about 10% from peak. now by 25%. but i feel it shouldn’t have gone to 17k in first place. thats why the fall looks steep. for long term investors with buy and hold strategy, these kind of things can create a lot of confusion.

Well, you guys need to be aware of the latest developments. Mgmt has indicated to a few analysts that even second qtr is panning out to be like first one. The corrective steps will have positive impact only third qtr onwards. I have different take on Page’s performance. Page’s ability to take price hikes is dented like Hawkins since inflation is in negative. Large part of Page’s earnings have come from annual price hikes along with volume expansion of 15-20%. Volume expansion has declined to below 15% which is quite good in this slow growth environment. PPI deflation is getting difficult to handle. If the earning growth is just 20%, real growth is 25% (20%-(-5%)) where PPI is -5% from previously real growth of 33%-8%=25% when 8% was inflation and high earning growth. But our mind is wired to look at nominal growth.

To me it looks like more than a bull market correction and it could be a process to de-rate Page. Mr. Market has its own mind and interesting things do happen.

Thanks Sumit, nice points for discussion. Couple of points though -

How can we generally have both deflation and volume expansion de-growth? With prices falling shouldn’t people start buying more of what they need (pent up demand)?

With economy turning around (IF), I’m looking at this high volume growth to offset the no/lesser annual price hikes.

IF there is volume de-growth coupled with inability to increase prices for a company like PAGE, imagine what will happen to other consumer companies like Whirlpool, Hawkins -> Disaster!

Asian paints with 10% (approx.) growth commands a good high PE, so I think Page could sustain premium valuations ALBEIT may not be as much as we are used to?

Deflation always comes with volume de-growth. Just take a look at Japan as folks postpone purchase in anticipation of lower prices. However, this doesn’t apply to Page since it is like staple consumption which can’t be postponed indefinitely

Disaster already happened with all major consumer brands like Hawkins, TTK,Cera or whirlpool but Page was standing tall. In case it falls below 5 digits, it will be a good opportunity to add.

Eco turn around is quite sometime away but Page could recover even before that.

Argh…Japan: India in the near future can never have a scenario like Japan as we are a growing economy. Deflation is only for this year as it’s an YoY comparison and while we move onto next year it would be inflation in low single digits.

Agree, If Page falls, it would be a very good opportunity to ride the economy turnaround.

Disclosure: As already made, I’m invested in Page. I read somewhere that stock markets discount any macro positive turnarounds about 6 months ahead and any negative turnaround markets will be a bit late to discount

Sumit, Page in 4 digits. I thought 13400 was a good price some time back. Had bought some then. So much of FII holding and if they start to unload then why not…

What makes you think that 13400 is a good price? Can’t be attractive just because it corrected 20% from top. I had learnt my lessons in previous crash. Clearly those highs were not justified. IMO if we are in bear market, we might see much lower levels and indication is that the process has started. It requires timewise or pricewise correction for the rest of the FY.

My reasoning was: 1. down 20% from top and 2. availeble at 38 PE FY17e. But now that the earnings have been downgraded too, the price corrected further. Your observation of time/price correction throws up another query: Why is Page (given the quality of the stock) not going thru a time correction, like GRUH? Gruh has been hovering around 240’s for a long time.

Gruh first corrected from 300 levels and is hovering near 240 which is 20% down. Page has indeed corrected the most from its top in recent history. But volatility has seen a general increase in this counter since inclusion in FnO.

Page is my top holding and at 45x 1-year forward (my estimate) its starting to look interesting. If it follows same pattern as Gruh then there will be ample opportunities to buy.