Hi Hitesh,

Thenthis should help Kitex also ? Imean cotton prices drop ?

Hi Hitesh,

Thenthis should help Kitex also ? Imean cotton prices drop ?

Hi Hitesh,

Thenthis

Page does not pass on the decline in RM prices to the end customers by reducing the price of it’s product, hence it goes straight way to it’s bottom line.

**Not sure if Kitex can do the same as they are not selling to the end customer.

**

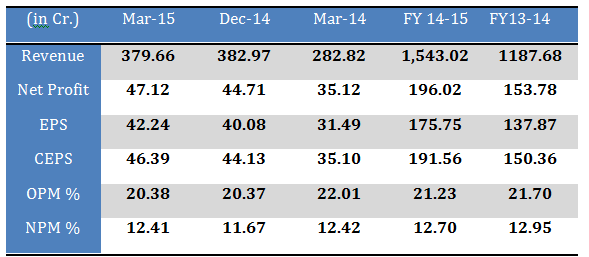

Page Industries Ltd has announced the following results for the quarter & year ended March 31, 2015

Excellent results from Page Inds as expected.

Next year should be a bumper year for Page due to low cotton inventory.

But even projecting a 50% increase in eps for fy16, one gets an eps figure of 267. Even stretching it a bit to 280 or 300 levels, the stock is quoting at 50 times forward.

Its been no use arguing valuations in Page and as long as growth continues it seems valuations will sustain. It seems in absence of any meaningful competiton, Page has an open runway to run as fast as it wants to.

As always, they have played prudent and not shown full benefit of cotton price surprise in Q4 but increased ad spend (+50% yoy) etc. This long term vision keeps valuation stretched all the time. Dividend keeps coming every quarter with increase built in.

The ride was heady today with a new 52 week high (nothing new there) 17,000. Personally, I could not accept this huge valuation and inspite of STCG, I pared down my position substantially. with P/E reaching almost 3 digits, I felt that this is it. I can take it no more. To me, the entire market cap exceeding the opportunity size of 18k crore was a rare occurrence and that was the trigger. I wish it had been a bit more gradual but I take what comes and go with the trend. Learning continues

PS - Again, not a course of action that is to be viewed as recommendation. I am not a certified anlyst. Please do your due diligence.

Every time I get tempted to exit Page (fearing high P/E), I look at the following stocks -

What is driving these premiums? Probably scarcity of quality stocks.

“If the job has been correctly done when a common stock is purchased, the time to sell it is - almost never” ~Philip Fisher

"Investors do not lose because of high PE. They lose because of faulty management or growth coming down." ~BM (if I recall correctly)

Sandeep - Agreed. But, I also had seen the experience of twiddling the thumb in an earlier era with Infy, with such high valuations. It can work both ways. As I said, my trigger was when the market cap exceeded the opportunity size, I felt that this is it. Having said that, I have given myself the liberty of being wrong (yet again) and I am still retaining the 60% of the holding !!

PS - You can also add the ever green ABB with its 3 figure plus P/E to the list

Hi Kalyan, Just curious, What is the source of 18K market opportunity (Can you share the link)? I would appreciate if you can shed some more light.

This is an old report but you can do the 13% math for 3 compounding years

There are some new, paid reports circulating around and they roughly give the same figure

(one of my analyst friends bought this report http://www.slideshare.net/daedal/indian-innerwear-market-trends-opportunities-20142019-new-report-by-daedal-research

@orasparkle pl don’t attach much importance to my sale. I am still learning and humbled by the depth/returns/quality of this forum. For me, the risk to reward ratio looked a tad tilted towards the former and hence went with it. For all you know, I might have the remorse shortly. I plan to get back the same quantity or even increase it by 25%, when the prices correct (if at all)

IMHO, searching over the web to get the Market size of any sector is no use. We will get different numbers ,different opinions altogether . We don’t know which we could trust as these figures are unauthenticated and developed from assumption. Many times for emerging brand , supply creates demand , like if somebody open McDonald shop , people start buying the burger , if it is not there people don’t by that.

@amitayu I never proclaimed that I am THE expert and these are the figures you should die by. I wrote my reasoning and if you disagree (which you have a right to), be civilized while disagreeing.

A very interesting read on Page by Prosperotree

Page Industries -Jockeying Towards 100x Earning Multiple

Read more at: http://prosperotree.com/investment-ideas/242-page-industries-jockeying-towards-100x-earning-multiple

I don’t think I replied you in rude manner and that’s why i mentioned the opinion is my humble opinion (IMHO) , any way if It hurts I’m sorry.Also note that I am also a learner and gained lot of things from this forum.

@amitayu Let us call it quits buddy. no issue. For what it is worth, Page took a 8% cut (albeit aided by Rajan’s inaction) and I hope to get back to the same qty or more shortly. Also, the above give link of blog, coincidentally talks about the same point - market cap vs opportunity size

Buddy , For Page, 8% cut in a day , Rajan’s inaction nothing matters to me until the growth continues and it’s cash flow is positive.

“If it is a free cash flow company, then the stock price would not collapse in the long term …. the trick with these high PE companies is as long as their cash flow remains positive, one should not be in a hurry to sell them” : BM

Disc: I am a long term investor of Page and it is one of the stock in my super concentrated portfolio. hence views can be biased.

Page now is in f&o and I think there could be a lot more volatility and huge price swings due to that.

This could even lead to some swings in conviction levels of long term investors.

The last leg of run up has been on the hopes of a superlative fy 16 backed by low cost inventory.

If one were to factor in some projections for Page for fy 16 and assume something like 60% rise in net profits then one can assume an EPS figure of close to 280 per share. Based on that at around 16k, stock is quoting at 57 times earnings. In the past too Page has been able to sustain forward PE of 50 so it could keep at these elevated levels.

The key thing to watch out would be results for first couple of quarters and see how eps figures pan out so one can get a better idea about what to project for whole year.

Exactly! Somebody gave the argument of sector opportunity vs. mcap. Let’s check the website for the segments Page is in. They are into lounge wear, casual wear, kids wear etc. I don’t think it will be less than 50k cr if you add all those mini-sectors. As per analyst reports, they are relaunching kids wear in Q1 Fy16 which could turn out to be massive segment in itself. I saw a report sometime back that even UK had 5-6% sector growth in lingerie segment while everything else is saturated. Valuation is expensive on all parameters but look at past. When economy has grown 8% their sales growth have been 40%+ so the hope is they could be inching towards 35-40% sales growth again coupled with cotton kicker could take EPS to 270+ in FY16.

Hitesh,

Isn’t page growing at net profit of 40%. I did not understand the assumption of 60% in your calculations

http://economictimes.indiatimes.com/markets/stocks/news/whats-in-store-for-idfc-mfs-star-picks/articleshow/47809138.cms?from=mdr

With Kenneth Andrade’s exit from IDFC (Punam Sharma is supposedly the replacement), there is bound to be some effect on some of Kenneth’s picks