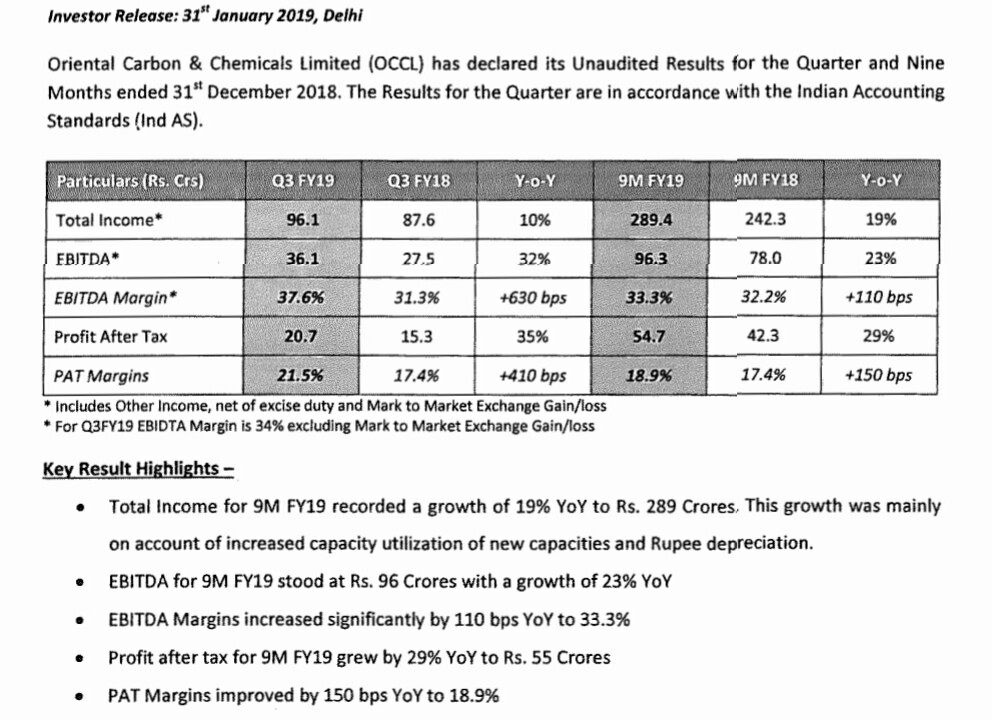

Reported good set of numbers with improved margins. Utilized 56% of 3.5 cr buy back. Paid up capital down to 1017.78 lks from 1031.13 lks. https://www.bseindia.com/xml-data/corpfiling/AttachLive/8897c1aa-9d29-4208-b947-805eb477151a.pdf

7 Likes

Continuous EBIDTA margin expansion…

This company is unbelievable… EBIDTA Margins are highest since I am tracking this company and the trend is always increasing… people say it is commodity based company… but its financials never experience such a cycle to great extent… They just keep improving and keep expanding… I beleive with such a high growth and high margins and stability, company should trade 25x its EPS (Historically, highest it has traded at 28).

p.s. I have invested at price of 900 and holding as of now…

5 Likes

Q3FY19 Concall Highlight:

• Started the production of Phase 2 expansion for Insoluble sulfur as planned.

• New trend in automobile industry supported the higher quality of tire driving the domestic demand for insoluble sulfur.

• Radialisation in new truck segment stands at 70% in new trucks OEM and 40% in replacement market. This helped to higher volume growth. In addition, antidumping duty for China helped domestic market growth.

• Capacity has increased to 34000 now along with increase in capacity utilization.

• Current earnings in Q3FY19 include Rs.3 crore MTM gain on currency against loss of Rs.3 crore in Q2FY19. For 9 month, MTM number is not big.

• Realization in international market has remained more or less same.

• Management is not expecting much growth in prices of insoluble sulfur in dollar and euro terms. Currency fluctuation is expected to drive the realization.

• On the other hand, realization for Sulfuric acid was on the higher side which helped improve margins.

• Capacity utilization of phase-II is not optimal but management was expecting it to be optimally utilized by FY20 which will drive the growth.

• Management is mulling on the expansion plan and working towards approval in May 2019.

• Management has given the EBIDTA margin in late 20s.

• Management commented that depreciation, interest and deferred tax has peaked out and expect it to reduce in future.

• Subsidiary Duncun Engineering Ltd has seen a turnaround for the quarter which also included few one-off and management is expecting things to improve here onward.

• Management is targeting addition of one line every 2 years.

• Commenting about USA market, management commented that USA is very matured market and they are making inroads and trials are going on. All the ground work should pay off from next calendar year.

• Slowdown in tire demand has not been felt by OCCL reasoning the possibility of lag effect. But this slowdown in tire demand is expected to substitute by increase in Radialisation.

• Company has very small market share in China. So, slowdown in China won’t affect much to the company.

• Globally, capacity utilization stands at 85%.

• Management expects the global IS demand to grow at 3.5% CAGR while Domestic IS demand to grow in double digit CAGR for next 2 to 3 year

18 Likes

I am quoting the icicidirect report “It operates in a closely guarded technology space with

small industry size (~| 3500 crore) and low asset turnovers (~1x). This

limit the competition in the marketplace. Therefore, given the impressive

utilisation of the expanded capacity, the next leg of capex is on the anvil

for OCCL. However, with low asset turns (~1x) and B2B nature of

business profile, we expect limited scope RoCE expansion from the

current levels, which will limit the valuation multiple expansion, going

forward. From a fundamental perspective OCCL remains a steady

business model wherein asset turnover is ~1x, EBITDA margins is ~30%

and net working capital cycle is ~75 days with consequent RoCE at

~20%. Going forward, over FY18-20E, expect sales, PAT to grow at a

CAGR of 12.3%, 19.7%, respectively, wherein we build in 230 bps

expansion in EBITDA margins to 32.2% in FY20E” Since the major tyre manufacturers are expanding capacity and it has high entry barriers, at best it can be a steady compounder right? In this market that is probably the space to be in.

Discl: I am invested in OCCL

12 Likes

3 Likes

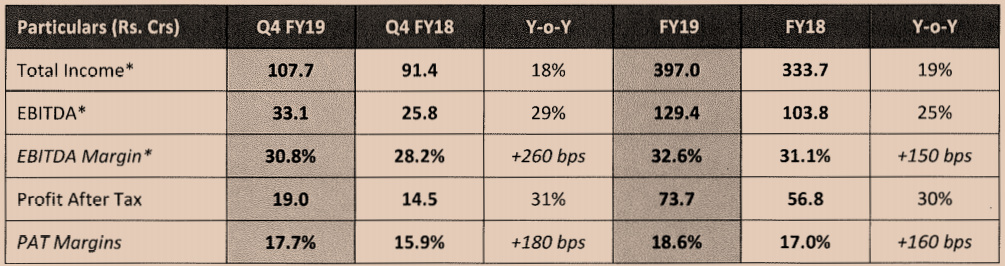

Once again… fantastic result by OCCL… and new expansion plan…

OCCL Q4FY19 results.pdf (862.0 KB)

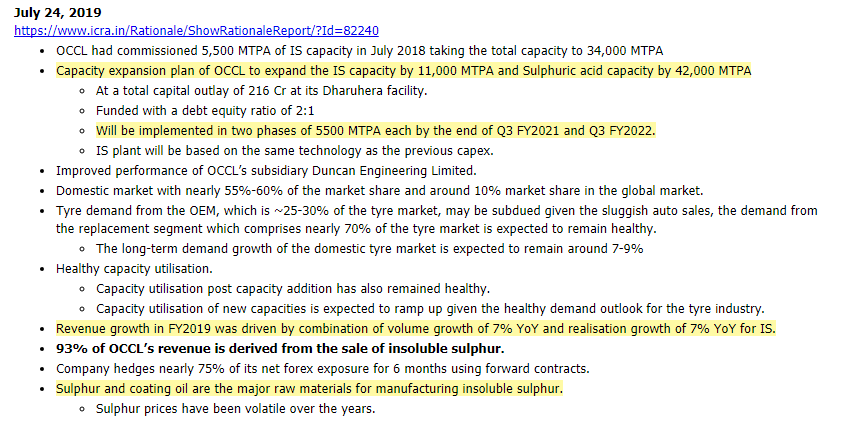

Project announcement:

The Board of Directors of the Company has approved expansion of its Insoluble Sulphur capacity from

34,000MTPA to 45,000 MTPA over the next 3 years at Dharuhera, Haryana in two Phases of 5500MTPA

each along with addition of Sulphuric Acid Capacity of 42000 MTPA with an investment of around Rs.216

Crore including Rs. 7.5 Crore for Working capital margin. The First Phase of Insoluble Sulphur Plant and

the Sulphuric Acid Plant are expected to be commissioned by the third quarter of FY 2020-21. The steam

produced from the New Sulphuric Acid plant will cater to the requirements of the New Insoluble Sulphur

Plant. The expected Project /RR is about 20%. The Project is proposed to be funded by a mix of Loans and

Internal accruals with a debt equity ratio of 2:1

13 Likes

With tyre industry suffering at such a big scale, how is oriental carbon able to increase its sales and margins?

2 Likes

I feel almost all major domestic tyre companies reported 5 to 6% increase in revenue… but still… Could you share the data on tyre industry… (Vol if possible)? Historical as well as current… it would be really helpful…

Investor Presentation.

1 Like

Oriental carbon AR 18- 19 notes

- Kick started brown field expansion of 11,000 MTPA of insoluble Sulphur capacity at Dharureha in 2 phases

- The first phase is expected to be commissioned by the third quarter of 2020-21.

- 216 crore will be total capex for the expansion.

- Net sales increased by 17 % yoy from 328 cr to 383 cr.

- Operating profit improved 25 % yoy from 103 cr to 129 cr.

- This was the result of timely capacity investments, cost reduction and growing customer wallet share.

- OPM % strong at 34 % , D/E stable at 0.16

- Margins grew during the year mainly on account of favourable exchange rate even after absorbing the increase in Raw Material prices during the year.

- The company achieved profit targets, it shifted to greener fuels and optimed energy footprints

- The subsidiary Duncan Engineering for the first time has posted profit in 6 years .

- The Subsidiary reported a profit of B2,77.93 lakhs .

- The subsidiary repaid loans during the course of the year, enhancing its liability lightness and auguring better prospects across the foreseeable future.

- The company is optimistic about the future prospects – mainly due to their long standing relationships with major tyre manufactures and also their improving wallet share with customers.

- Although the end market is growing at a slow pace of 3-4 % , company is confident of achieving much better growth rates due to greater increment market share

- Indian tyre industry is poised for double digit growth due to anti dumoing duty imposition on China

- Company’s low exposure in large China and US Market is a great opportunity.

- Company will double its sulphuric acid capacity.

- The highlight of the Company’s performance during the year under review comprised the launch of predispersed Insoluble Sulphur , a specialised vulcanising agent for the tyre and rubber industries. The testing of this complex and critical product was concluded and offered to customers to commence trials in their laboratory and production lines.

- Light commercial vehicle and trucks and buses only have 35- 40 % of total market radialised. There is a lot of scope for tyres to move to radial here and hence increase the insoluble Sulphur demand.

- Company has started sales in US markets which is looking up due to curbs on Chinese tyres imports by the US.

- Apart from US , company is targeting south east Asia by adding new customers.

- The Pabrai Investment Fund IV, LP has exited the company completely.

The Annual report was very detailed this time, highlighting the nature of the business, performance of the company, market conditions and future prospects of the company. The company is very optimistic about the future prospects.

Disc - Invested

25 Likes

Hi All,

Sharing my notes from the credit rating report.

Regards,

Yogansh Jeswani

Disclosure: Invested

11 Likes

Q1FY20 Results:

Total Income for Ql FY20was up by2% YoY to Rs. 95 Crores as compared to Rs. 94 crores in Ql

Rs. 16 crores in Ql FY19

stood at 27.9%.

• EBITDA for Ql FY20 stood at Rs. 27 Croresas compared to Rs. 29 crores in Ql FY19.EBITDA Margins stood at 27.9%.

•Profit after tax for Ql FY20is Rs. 23 Crores as compared to Rs. 16 crores in Ql FY19

2 Likes

Occl remains a longterm hold specially for holders like me who first bought it in 2012 -13.

A lovely example of wealth being created by simple act of holding long in cos where promoters are ethical and executing well; opp size limited but growing; a big moat due to oligopoly in true sense leading to superb margins n Roce; gradual capacity expansion.

If one gets above combo in other cos simply stay put and see the wealth being created without getting impacted by volatality in stock prices.

12 Likes

4 Likes

Due to drop in rubber price and slowdown in OEM (consumer), top line will be very poor but bottom line might sustain!

1 Like

Q2 19 Results

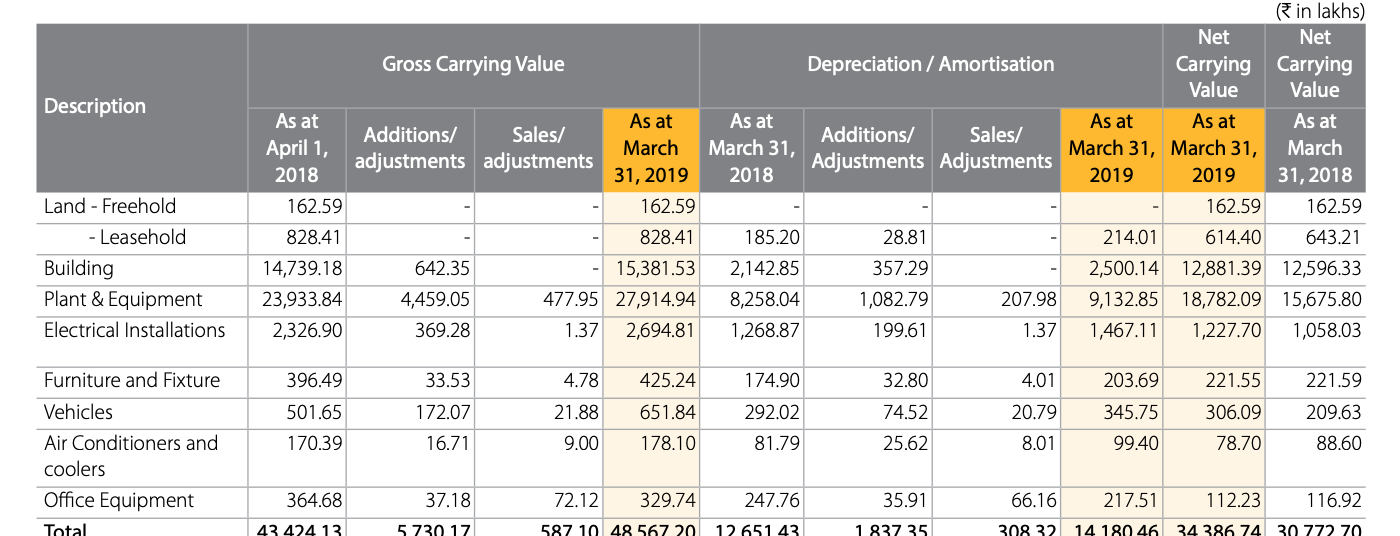

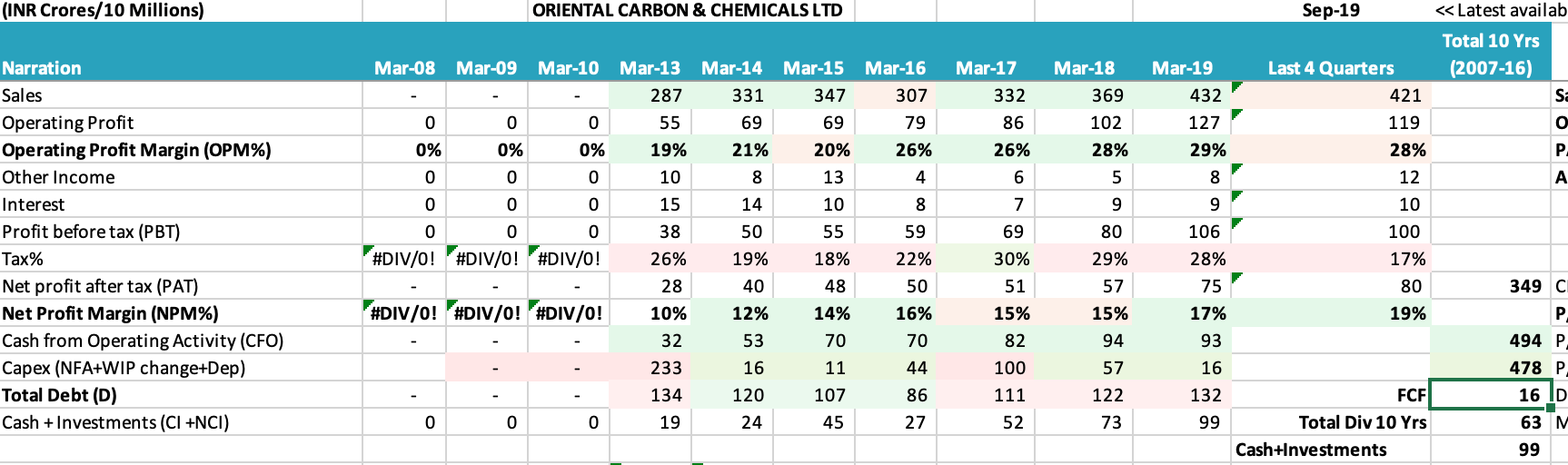

In FY19, OCCL recorded depreciation of INR 14 cr on buildings + Plant & equipment with gross carrying value of INR 387 cr - thats a depreciation rate of 3.6% which translates to a useful life of 28 years. Are OCCL’s assets truly that long lived? If not then the profitability and return ratios are overstated.

Moreover, OCCL has done capex of INR 478 cr in the last 6 years while its fixed asset turnover has averaged 1.25. Therefore, for incremental sales of 421-287 = 134 cr from Mar-13 to Mar-19, OCCL should only have required about 107 cr of growth capex. Therefore, we can assume that in 6 years, OCCL has required 478-107 = 371 cr of maintenance capex to do revenues of 2404 cr from Mar-13 to Mar-19. Thats a maintenance capex rate of 15% vs OCCLs long term accounting depreciation rate of ~ 5%. Again raises questions whether OCCL is accurately estimating depreciation.

10 Likes

Can you please point out the source of 14 cr depreciation ? I see 485 cr gross Assets Value, 18 cr Dep and 343 cr as Net AV. 18 cr at 343 cr is ~5% which is fine.

I have not checked where they have invested in last few years, but I am assuming they had started new plant as well hence will require to dig to understand where they have invested the gross block. Can you please find out?

1 Like