They use naphthenic oil in their process which is linked to crude oil.

2 Likes

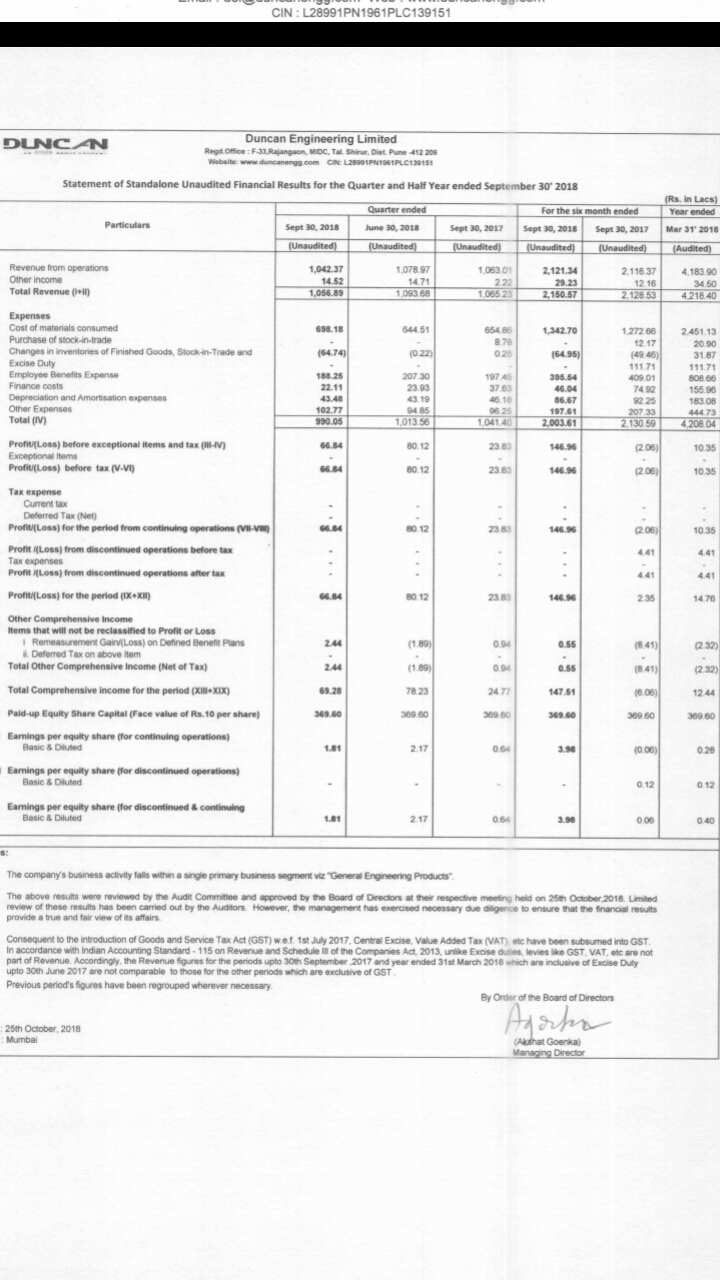

Duncan engineering - Good result. Management managed to convert it into profit making business from loss making business. This shows the quality of management. They did what they said. Overall, results were excellent driven by the reduction in “Other expenditure” and reduction in finance cost. Finance cost reduced 45% QoQ.

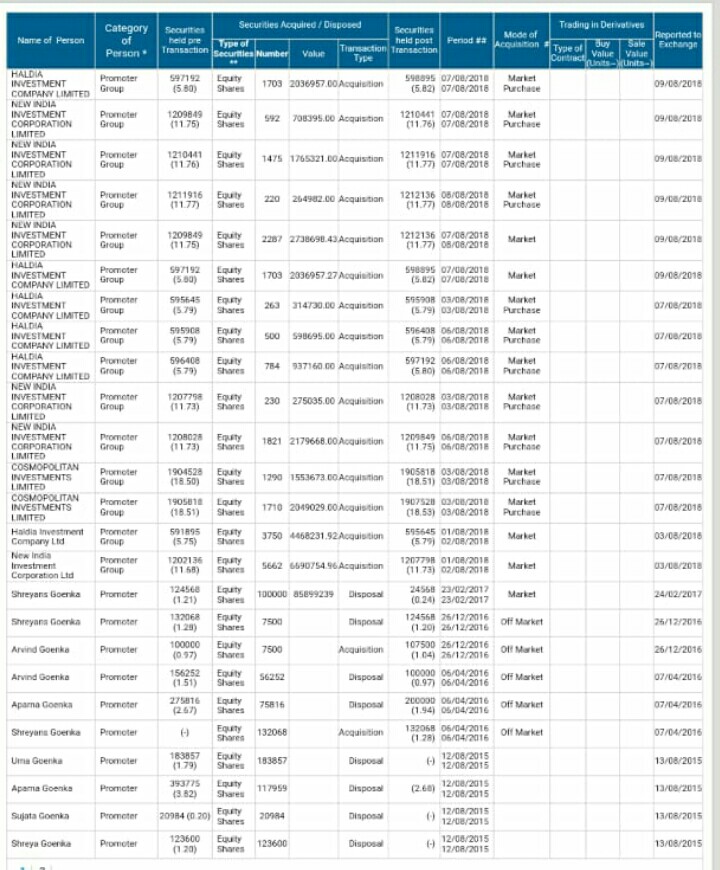

Any inputs/view on this sudden rush of buying from promoter group?

Disc : entered with very small position for tracking purpose,have plan to add more.

2 Likes

Cant read into this much as only 3 Cr worth of shares(market cap is 1100cr plus) has been bought by promoters, if they are raising stake pretty fast like what happened in VIP Industries , then its something worth exploring more.

2 Likes

Can anyone explain the use of Insoluble sulfur in tire industry in leymans language?

Also, if OCCL is facing loss on Sulfuric acid plant, then why are they continuing with the business?

Insoluble Sulphur is used as a vulcanisation agent. I suggest you read a bit on Vulcanisation. You may have come across this term in elementary school science. This is essentially creating cross-links between layers of polymers. In the tyre industry, rubber is vulcanised with insoluble sulphur which increases the elasticity and strength.

2 Likes

Hi

There is a very nice document available in public domain. I am attaching it to this post. I think it is a must read if you are interested in this area. The document covers:

- Types of tyres

- Components of a tyre

- How performance of a tyre is measured and what uses each type has

- Ingredients in making tyres - both polymers and fillers (this is what is of interest to us mostly but other sections are imp)

- Processing

- Various properties of a tyre

etc.

Do have a look. Maybe I have shared it before but I do not recall.

Tyre Compounding for Improved Performance.pdf (656.4 KB)

Regards

Deepak

10 Likes

What is ‘radialisation’ and how it is going to change the tyre industry, can someone please explain it in layman’s term? I tried to google it but concept is not that much clear to me.

The expansion plan of various Tyre manufacturers augurs well for OCCL (from https://www.alphainvesco.com/blog)

Capacity Expansion Plans : The Indian tyre industry is expected to see significant capacity expansion in the upcoming two to three years. All major players in the industry have announced their plans

MRF has announced to set up a new facility in Gujarat where it plans to spend ~Rs 4,500 crores over next few years

Apollo tyres laid foundation for their fifth Indian facility in Andhra Pradesh which they will manufacture passenger vehicle tyres. The company is spending ~Rs 1800 crores in the first phase of the project. The facility is expected to commence operation in two years from now. Apollo is also planning to expand its T&B capacity at the Chennai plant which is expected to commence operations in this financial year

JK Tyres: In 2016, JK Tyres acquired the Cavendish tyre business from the BK Birla group to enter in the two-wheeler segment. JK Tyre now plans to expand its T&B tyre capacity by ~0.6 mn units at the Cavendish facility by investing ~Rs 275 crores

CEAT has announced a capex of ~Rs 3,000 to 4,000 crores over next 4 to 5 years. The company is entering into the OHT (off-highway tyre) segment with a new facility in the Amber Nath. The company has started its operations at a very small scale and plans to expand it further to capacity of ~100 MTPD. CEAT is also planning to expand its capacity significantly PCR with a greenfield expansion in Chennai which Is expected to come online in line with Apollo’s Andhra greenfield facility. It also has plans to expand it T&B and 2/3-Wheeler capacity by brown field expansion at Halol and Nagpur plant

Balkrishna Industries is coming up with an additional greenfield facility in the US with a capex of $100 mn (~Rs 700 crores) which will manufacture 20,000 tonnes of OHT tyres every year. The company is also spending ~Rs 500 crores in its domestic Waluj plant which will generate incremental capacity of 5,000 tonnes every year. Balkrishna also plans to set up a 140,000 tonnes/year carbon black facility

Bridgestone India is planning to spend ~$304 mn to increase its current capacity of 15,000 tyres per day to 41,000 tyres per day Looking at the above expansion plans it seems there could be a competitive scenario amongst the tyre companies to gain market share as majority of the capacities have similar timelines. The tyre companies might grow at a decent pace by selling more tyres however, their margins and return ratios might take a hit in order to achieve market share

Excerpts from https://www.alphainvesco.com/blog/understanding-the-indian-tyre-industry/

9 Likes

Hi,

I used to hold OCCL earlier and don’t track it much now.

If my memory serves me right, not all of India’s IS demand is fulfilled by OCCL, good portion is still imported, not because OCCL cannot supply but out of preference I believe. Exports constituting 2/3rds of sales in fy18 corroborates the above statement. More so, OCCL is looking for markets outside India to grow, US and China. The ratio of imports to domestic sales in India could further give insight on the above.

Though a lot of tyre capacity is coming in India, the question remains if OCCL will significantly benefit out of it?

The plausible reasons why tyre manufacturers in India import IS is because it’s cheaper to import or may be OCCL can’t match up to the gradation/ customisation.

Its also possible that market in India at present is really small and keeping in mind the tyre manufacturer’s need to have diverse sources of supply, OCCL can only sell as much in India. (Again, ratio of imports to domestic sales in India can prove/disprove this point.)

Even I’m gung-ho on domestic demand that will arise for IS as a product but it remains to be answered how much will OCCL benefit.

I could be ludicrous in my thinking and open to opinions.

Thank you.

1 Like

Yes, mostly IS costs only 1-2% of total tyre cost to tyre manufacturing company but it improves the quality drastically. In addition, companies don’t trust the other IS suppliers easily. They test it for atleast two years before finalising it. So, in case, if they depends on only one IS supplier and face any problem from that supplier, their manafacturing will stop. So, it is kind of precautionary measure to diversify the risk of supply issues… so if you see, it is common for every tyre manufacturer to have at least 2 IS suppliers… This is the reason why OCCL can not accquire 100% market share or even >90% market share in India even after the fact that it is the only domestic player… price is not at all issue in this contex…

8 Likes

Should offer the buyback above Rs.1200…

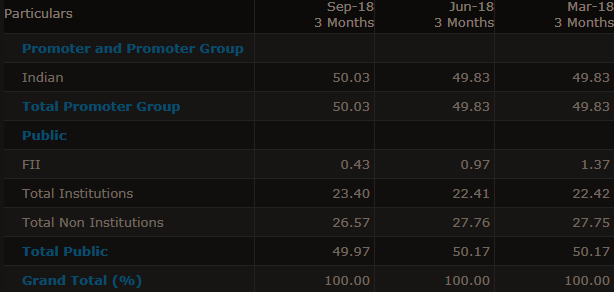

Also, note that, management and institutions has increased their stakes in the equity capital…

Source:Cogencis

Looks like management is confident of the busienss…

3 Likes

great set of results

-Total Income up 31% to Rs. 99.6 crores as compared to Rs. 76.1 crores in Q1FY18 lead by a mix of increase in quantity and price.

-EBITDA up 32% to Rs. 31.6 crores as compared to Rs. 24.0 crores in Q1 FY18.

-Profit after Tax up 42% at Rs. 11.7 crores with Margins of 17.7%

company declares and interim divindend of 4 per equity share.

Company declares a buy back of 35 cr at a rate of Rs.1150 per equity share.

“Continuing with our Company’s philosophy of rewarding the Shareholders, the Board of Directors have approved the share Buy Back programme of Rs. 35 crores at a maximum price of Rs. 1150 per share. This will in no way hamper the growth/diversification plans of the Company and the Company will continue to pursue growth and expand its business in the coming years with the help of a strong Balance Sheet.”

10 Likes

Can anyone tell me where can I check the sulphur rates (Used in production of insoluble sulphur)?

What are the current rates and past trend?

Also,

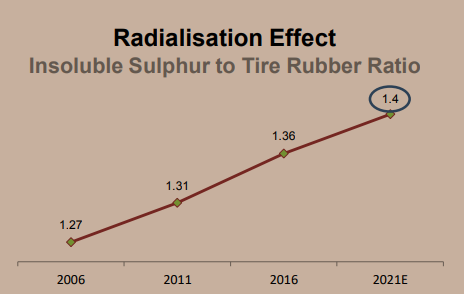

What does this implies?

Does this means that IS used in tire manifacturing is 1.4 time more that rubber?

2 Likes

Management hinted in their concall that they may comeup with further expansion plan and also, may diversify their business by acquisition route through NCLT. (Also, buyback offer suggests confidence.)

they said they were looking at bidding for a company through NCLT route, but that has got dropped.

2 Likes

Update on Buyback offer

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=2a57f9b3-a8be-4735-97bf-96b14da2bea8