Orient Refractories (NSE:ORIENTABRA,

Mcap 470crs) â High risk bet

ORL is amongst one of the top

refractory manufactures in India.

Investment theme: Speculation cum special

situation

This investment is more based on market

rumours that RHI AG, an Austria listed company is planning to acquire Orient

Refractories. Please read this http://www.katalystwealth.com/special-situation-opportunity-for-may12

and this http://investingvalues.blogspot.in/2012/12/orient-refractories-heat-is-on_12.html?showComment=1355390934654.

I am satisfied that there is more than 50% probability of this deal going

through based on analysis put by Katalyst wealth and Ninad Kumar. The most convincing argument to me is that acquisition in

India is part of their three pillar strategy for expansion into emerging

market. Currently it derives only 12% of its revenue from Asia pacific. Orient

Refractories can add another 2% to its emerging market kitty.

Valuation

INR in

crores

Period

Sales

EBITDA

%

EBITA %

EV/EBITA

EV

Orient

Refractories

TTM

340

18.4%

17.4%

8.1x

479

Vesuvius

India *

TTM

555

16.8%

13.9%

8.9x

682

IFGL

Refractories #

TTM

593

12.1%

9.7%

4.3x

251

RFI

(INR @ 70)

TTM

12,929

12.6%

9.6%

7.9x

9,765

Acquisition multiple

Tata

Refractories

FY 2011

868

11.5%

9.1%

14.3

14.3x

*

Vesuvius India is trading at a

EV/EBITA multiple of 8x (TTM). [Angel broking expect revenue CAGR of 6% over

CY11-13E.]

*

Krosaki Harima Corporation acquired 51%

stake in Tata refractories in April 2011 at an EV/EBITA valuation of around

13-14x. Tata refractories EBITA margin average was around 9% (2006-11) compared

to 18% for Orient Refractories.

Krosaki

Harima Corporation acquired 51% stake in Tata refractories in April 2011

at an EV/EBITA valuation of around 13-14x. Tata refractories EBITA margin average

was around 9% (2006-11) compared to 18% for Orient Refractories.

*

RHI itself is

trading at a EV/EBITA multiple of 8x (TTM). Orient margin and return ratios are

much better than peers.

*

IFGL can be taken

as exception, as the company indulge in too many global acquisitions, many of

which failed to generate any meaningful return.

I expect the deal

to happen at aleast 11-12x EBITA multiple, implying upside of upto 50%.

Peer Analysis

Going through

historical ratios of Vesuvius India and Tata Refractories, it appears that

Orient Refractories (standalone only for refractories) EBITA margin and ROCE is

much higher than its other players. Of course sales growth was muted, as it was

very slow in capacity expansion. But because of that in FY2011, its capacity

utilisation was more than 98%. This is also reflected in EBITA margin of

Vesuvius India which is sharply lower than EBITDA margin of Orient

refractories. I am attaching the excel sheet containing historical ratios of

Orient and its peers.

Risk

*

In case the deal does not happen I expect the price may decline

back to INR 25, a downside of around 40%. But I think now that the company is

in play, if not RHI some other company should acquire it sooner or later.

This is my first investment and analysis of any special situation.

Disc:

Taken nominal position of 2%. Will increase if price falls back to around 35 or

more clarity on acquisition.

the promoters of this company are RHI AG a MNC based out in Austria. It specializes in producing heat resistant refractory products for cement , steel ,glass and metal industries. It has 7,900 employees, 250 sales offices and 10,000 customers from the above industries across the world. It produces 1.5 mn tons of refractory products each year. It acquired a 70 percent stake in Orient in 2013 for Rs. 398 cr to strengthen its position in the Emerging Markets.

Per capita consumption in India is very less compared to the other countries like US, Europe ,China. RHI AG plans to increase share of steel segment revenues from 57 percent to 64 percent uptill the year 2020. It also wants to improve its flow control revenues from 320 million euro to 400 million euro. Bulk of this incremental growth is expected to come from Orient. Orient at present has 62 million euro sales from this segment. Hence RHI aims to double Orients Revenue by 2020 to meet its targets.

Orient has 20 percent CAGR growth over the last 5 years, which is expected to continue. RHI sales network is a great thing for the company. It has 50 percent of its export sales from this network. RHI is also starting to source ISO Products from Orient which will be a huge export booster to the company.

ROCE ratios of Orient are pretty high compared to its peers. Orients is - 27 percent , while IFGL is at 10 percent and Vesuvius at 15 percent. This is due to lower cost of land ( of which 48 percent is underutilized) , and use of local technology. Orient plans to increase its capex by 50 percent in the next 3 years, but still we can expect ROCE ratios to remain high on the back of change revenue mix ( more exports).

Orient also has the highest gross margins among peers due to lower RM cost as 80 percent is sourced locally and rest 20 percent imported from China.

the company is generating healthy cash flow and margins over the years in a cyclical business, this signifies a moat in the business. it looks a good bet to ride in the reviving infrastructure and steel business .

Good analysis. I am watching this company, but not invested so far. The

doubt in my mind being - what if the steel as a commodity goes back down in

prices and demand. In my mind the best time to invest in this company was

when the commodities were in recession 12 - 18 months ago. I am doubtful

now whether there is upside or downside for the steel cycle. And today’s

news that China believes that even achieving a 6.5% GDP growth itself is

tough further increases the doubt. On the other hand, Trump’s declared

infra push is a positive ( though he had only spoken till now with no

action ) What is your view on the steel cycle.

Bulk of this incremental growth is expected to come from Orient. Orient at present has 62 million euro sales from this segment. Hence RHI aims to double Orients Revenue by 2020 to meet its targets.

48 percent of land is underutilized

Orient plans to increase its capex by 50 percent in the next 3 years

hi rvetri,

i think the good part of the company is how its margins have remained insulated from the steel cycle. also the infrastructure and steel industry is in the recovery mode i think. If the commodities were in recession 12 months ago , it means they havent hit the peak yet , infact there is a long time for them to rise and then hit the peak. Hence i find this story interesting to be a part of the recovery cycle.

With China cutting down unprofitable Steel Production, Refractory demand is going to rise. We need to be patient. Refractory has major consumption in Coke Ovens, rather places where heat is extremely high and one needs to change the refractory lining periodically too.

Isn’t below are the good things happening at this counter:

Dividend has been increased hugely @2.5 per share compared 1.45 rs. per share last year. Dividend payout stands at ~44% on a net profit of Rs. 68 cr for FY 16-17.

Zero debt

Huge cash of around 110 cr in balance sheet. They are giving back to share holders in the form of increased dividend payouts.

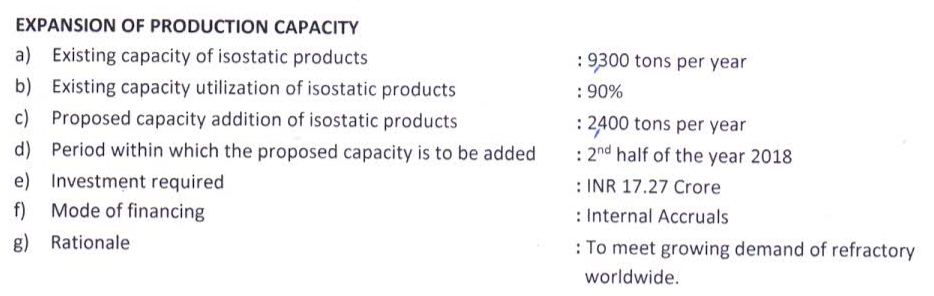

Increasing the capacity of isostaic products from 9300 to 11700 tons per year. (with cost of 17crs. which is from internal accruals)

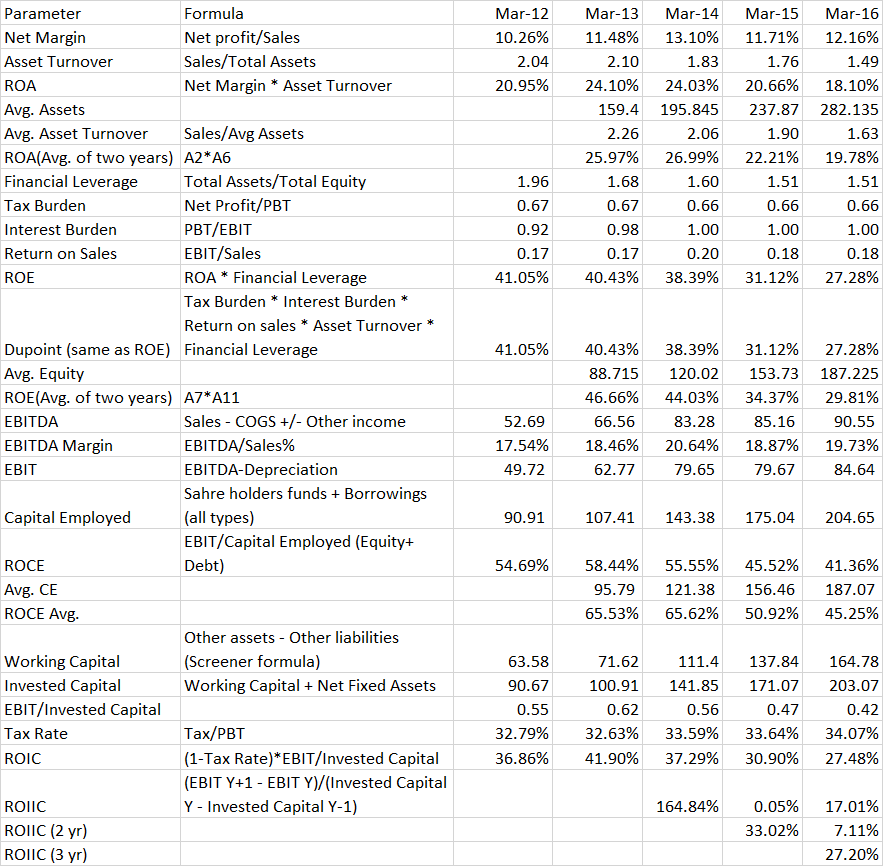

Actually looking at the numbers tells a different story. There is a fall in important ratios but are still at a healthy rate currently. How should we take on that? ROA at around 20% for a manufacturing firm is extremely good, isn’t it?

I want to learn how to use Screener custom data management feature and tried with Orient refractories.That was an excellent feature. Thanks to @ayushmit & others whoever involved in developing the great tool. Thanks to @Donald for his work Ajanta excel sheet which I used as a reference (I have got this from Art of Valuation thread).

From the data it looks like important Ratios are declining y-o-y.

Net margins are not improving much. Cost is not efficiently managed.

Sales are on a slower growth but are increasing y-o-y.

Sales per unit of assets is continuously reducing, that means they are not increasing the sales at the same rate as assets,

Debt is reduced zero and are paying tax close to ~33% every year, which is a good thing.

ROCE & ROIC are declining y-o-y but are still at healthier rate.

Now, I have the custom sheet available I will go ahead and try to compare with competitors to see how are they performing as a next step ( I think Vesuvius & IFGL are competitors).

Note: I still have doubts on how to calculate ROIC and difference b/w Capital employed and Invested Capital. The formula might be wrong. Data shown in Ajanta vs how Screener shows data now is changed a little bit. Still trying to get more understanding details. Please excuse if there are mistakes. You are welcome to correct them.

Disclosure: Invested(4% of very small pf) and not interested in buying until all the learning is complete.