@bhaskarjain @marathon_runner @Hocuspocus32

Thank you for the very valid counter theories. I do believe I might be displaying a confirmation bias. I am going to relook at the entire theory and story this weekend and present a report. Would then appreciate if we could discuss it and get to the complete story of this company. Really appreciate the banter and strong opinions with advise that one can have with you guys. End of the day, that’s why I like VP.

3 Likes

Thanks valuestudent for at least acknowledging the other view.

I called up the CS and he said the pledge is to support the earlier pledges since share price of Omkar had fallen after demerger. He was clueless on why they disclosed 1 month after creation of the pledge. I wanted to ask about Dr. Omkar’s share sales but he kept me on hold for long time and I gave up. Would request all investors to call them up at their office numbers 0251-2697340/2690651 and grill them. They cannot take minority shareholders for a ride.

Giving media interviews, coming out with “Updates” and then shortly selling their shares. It may not be illegal per-se but it is highly unethical. Why do they give forward looking statements when they cannot walk the talk? This game has been going on for so long that they should feel ashamed of themselves.

6 Likes

Omkar is much talked about growth story. Many aspiring & vigilant investors like you might have taken positions. Perhaps many other good Small Cap are doing same practice on pledging/information etc but Omkar is being investigated deeply. But looking at stock trading around 160 for most of 2016-17, OMKAR PLUS LASA will give handsome return to investors

1 Like

Since last 1 year this sale of shares has continued even after repeated assurance of no more further sale by promoters…I think from 68 odd levels to currently 37%(reduced 3.4lakh in this month too)…but the most surprising part is that the price of share has not gone down…even currently if we add lasa it is still around 190 levels…so who is accumulating? In this quarter public shareholding… goldman sach and premier fund also not showing ?

Disc : holding about 10% of portfolio

Gentlemen. I will post my opinion on OSCL

OSCL (Standalone)

Data from screener.in

Part 1 - Exhibits

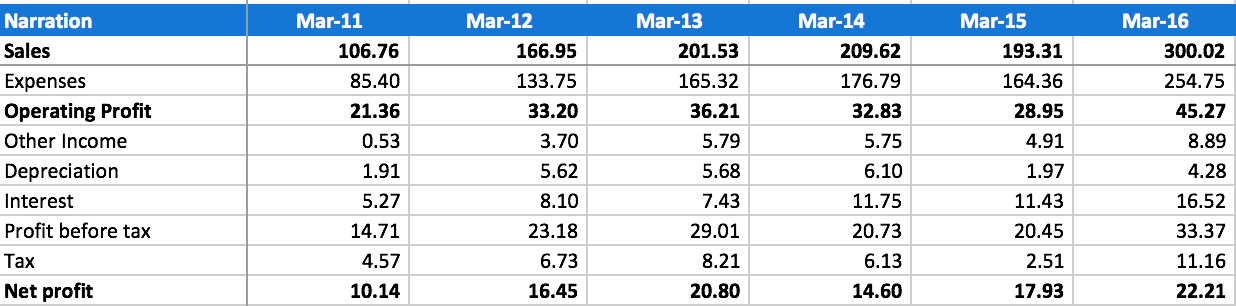

Exhibit 1

Sales & Profits From 2011 to 2016

I am not posting the data for 2017 as we know there was an exceptional write-off… and the data is available above and can be interpreted in many ways.

So, I would like to reach my first conclusion; that is, is the business growing and does the management have the ability to grow the business. You must infer your own deduction.

Exhibit 2

Sales & OPM

Exhibit 3

ROE & ROCE

Part 2 - Thinking it out aloud

Now, if we did not know the name of this company and did not know that it has a debt overhang and promoter pledging how would this business look to me and you?

Would be business die? Is there lack of customers? Is there a bad name for the company in the “customers minds” “not investors minds”. They have the highest certifications and all their plants are FDA certified. The customers are tied in to buy from this company because OSCL holds the patents. The are not getting a bad rap for quality of product, they are getting a bad rap for quality of management, more appropriately bad financial management. If the issue is sorted which it should be sooner rather than later, this… ok I am predicting now ![]() would be around a 20 PE stock. I keep trying to argue with myself but find nothing wrong with the “business”. Please one person, tell me “What is wrong with the business and why it cannot keep growing”. and Why is the promoter holding of lets say even 10% going to destroy the business? Is it even a destroyable business? The orders are fixed with their IP’s. Please please show me the other side of this picture.

would be around a 20 PE stock. I keep trying to argue with myself but find nothing wrong with the “business”. Please one person, tell me “What is wrong with the business and why it cannot keep growing”. and Why is the promoter holding of lets say even 10% going to destroy the business? Is it even a destroyable business? The orders are fixed with their IP’s. Please please show me the other side of this picture.

When we see a company go into the ground it has very few reasons; 1. DEBT, 2. LACK OF BUSINESS 3. LACK OF MARGINS. DEBT they will resolve with a rights issue or warrants very soon. They would not want to keep giving money interest free to the company. Then, does OSCL have the protection with it’s patents to command pricing power. The answer to me seems to be visible in the gross margins but I would like to really hear the other point of view. Of course, not to forget, there is always 4. CORPORATE FRAUD (In that case Pravin, Rishikesh and Omkar are going to play table tennis with Raju in some prison very very soon based on all the actions they have taken if they are fraudulent). This is a key one for us to answer. Manipulating share price with some press releases and disclosures of share sales will get them a bad rap and maybe a fine from SEBI and that unfortunately is how this world operates. Once they are done sorting their nonsense, the business will finally start being reflected in the share prices. I do hope my long term being 3-5 years is the same page you and me are on.

Now, if I were to think, the fundamentals are intact (you can please comment) how much longer will the pledging and sale go on? This drama will be over soon. Will they be left with only 10% equity after they have used their useless financial brains to run themselves into the ground? So then what will happen? Of course we will get a 15-17% grower at a PE of 1-2. Would I buy more? Regrettably, the answer to me still seems yes I would buy more, please knock me in the head if I am being really daft here.

Instead of making the post longer I thought lets ponder over “the business” and the impacts of the foolish financial decisions where promoters have been shooting their own selves and giving us their shares as a free gift at half the fair prices, for their stupidities, why should I not take their shares when they pay the price of financial harakiri with being forced to reduce their holding at lower than what it should be, and take pleasure in taking advantage of them for being stupid financially, when the business is fine?

10 Likes

Thanks valuestudent for your detailed post.

Your post is logical and there cannot be any arguments against it. But the only point is when the promoter’s integrity is in question, going solely by the reported numbers may not be prudent. If Dr. Omkar wanted working capital for Lasa, he could have pledged more shares instead of outright sale of the shares. Don’t forget he has interest in Amarnath Securities also, so he is not naive wrt finances.

If I may, we need to do more on the ground scuttlebutt to give credence to the reported numbers. Some areas that could be looked at

- Export data from GOI website and matching with the management’s numbers

- Talking to their major suppliers and customers if possible

- Talking to their bankers why they are not able to give or the delay in giving working capital loans

- If someone is living near Badlapur, visiting their plants

- Talking to ex-employees, current employees, maybe ex CFO

Of course its very easy to say to get all this data-point…

4 Likes

I share your thought process about Omkar that it is a great business with not so good management and poor financial acumen. Now Omkar being out of OSCL and Veteran Pravin who was the key person in the growth of the company, I also believe that sooner or later the issue of pledging and sale will be gone till then the share may underperform, , however this is the time to hold on to your investment and give it time and space. As long as the business is growing which is to be seen in the next few quarterly results, it should catch up its true potential in the capital market too.

3 Likes

-

I think this might be a right approach, first of all, one needs to ascertain whether the operational numbers are genuine given promoters dubious nature in telling lies - That means the sales number, whether the patents they talk about are consequential, gross margins, customer profile, opex number in the plant etc. Boarders like @giridesh3 and others may please throw a light on how to go about this.

If there is any major problem discovered in Step 1, then, of course, it’s a quick sell decision.

-

In case, however, all operational numbers are broadly correct, then one might look at taking a philosophical call. It’s perfectly okay decision of @bhaskarjain and many others - to have one’s own rule book and to abide with that. That, if the promoters’ non-sense reaches a certain level - get out regardless of the potential of the money to be made. In a long investing career, that will make one lose some excellent opportunities but will also save major losses in a lot of opportunities.

-

Now coming to the point of financing. I strongly disagree with @valuestudent that rights issues is a panacea for them. I feel promoters current personal cash reserves + money deployed in business by promoters as debt and equity + existing debt raised is less than what business requires - this is either due to sheer stupidity or some fraud/major siphoning or this may be an indefinite timing issue because of some large receivables stuck or some other such issue. I feel if the existing money was sufficient, whatever be the form, then this problem would not have dragged for so long and despite repeated promoters’ assurances.

3a. So a rights issue alone which is basically a transfer of money from one pocket to another is not going to solve the issue. They will have to get some external financing - and here is what I worry the most - if the business is so good and patented and all - why the hell they are not able to raise money from outside - in this monsoon of excess liquidity at crazy valuations. In fact, if I remember correctly, somebody I think had pointed out that IPO expenses as a % of IPO money raised were crazily high for this company - again a red flag. This is again something where I will ask senior boarders like @giridesh3 and others to comment.

10 Likes

@bhaskarjain @8sarveshg

First off, thank you guys for coming back with good… in fact great views.

My opinion if I was to put it into two bullet points would be:

The promoters are highly knowledgeable & intelligent when it comes to chemicals and processes. They are among the best minds and are also surrounded by very good other R&D team members in their company.

They have the financial brain of a fish and the mouth of a brag and they think the world will do exactly how they think it should do. Their ego is unbeatable. They keep mouthing off things like…

a. LASA will be listed by June end  How, do they own SEBI? Will they make sure SEBI does things to “their” satisfaction?

How, do they own SEBI? Will they make sure SEBI does things to “their” satisfaction?

b. Pledging: We know the saga very well. They do not realize and this is how now they are eating humble pie… let’s say the stock market cracked 50%. The holders of their pledged shares would have sold them in the open market. Basically, they also predict that a stock market crash cannot happen. Can’t run their own financials properly but think they know the world financials markets.

c. Their unplanned CAPEX was also a result of their “high quality” financial planning. It has nearly made them nearly paupers compared to where they were. Again, they were thinking, things will work out

Sarvesh, on the financials; I do not think they are financial frauds, but that can be known only in hindsight especially by me. I have no formal training in finance except for what I use to run my businesses, and my logic is business side and not financial forensics so it is easy for me to make a mistake there. I would totally agree with you on your notes on the financials as I have seen your posts and you obviously know the numbers side of the game very well.

Now, on the scuttlebutt as both of you have also rightly picked up, the one person who I respect for his knowledge here is @giridesh3. Girish, if you could find time to help us with your views and opinions, and help us get answers to some of the very good questions above from Bhaskar & Sarvesh; that would be a very valuable contribution to all of us here at VP.

7 Likes

Actually I do not have too much to add. Just few points I will make and then retreat.

-

Promoter actions are mind boggling. They are back at what they do best. Pledge, sell, transfer etc their own shares. We have no control over them. Here each investor has to decide for him self what to do if they don’t like all this nonsense. Don’t lose sleep over some Omkar. This is not the only game in the town. Make your own decision.

-

Only forensic auditors can unearth serious fraud, if any. The glance at statement and what we can do using published statements (especially BS and cash flow statements) did not indicate serious red flags. But then no one can be 100% certain in India. Their auditor is also some regular Joe. Not some top notch auditor.

-

Father- Son due do not get along. Son is selling Omkar shares to get out of it. Father may do the same when Lasa gets listed or later. That may put pressure on Lasa’s stock also. Any way looks like from now on both Lasa and Omkar will be on different path. They will have their own strategies and plans.

-

Situation is very confusing. In such confusing situation, the experience tells us that it is better to follow and track what these insiders i…e these promoters are doing. Because only they know what is happening. This stock is now mostly owned by retail investors who may not know much. Although you may get lot of free opinions. Personally I cannot take any of those seriously. Hence one should intensely watch what these Herlekars are up to. That may offer us some clues. Important thing is we should see their personal stake going up. May be down the line …we should also see them doing creeping acquisition in the open market. We need to see their intent and skin in the game.

-

How they use proceeds from Rights issue is critical. For example how much debt they will retire using that money to reduce risk. And how much money they will invest in any acquisitions. Investors will need to scrutinize these so called acquisitions. And if they will add any value or just empire building. But again we have no control over promoters. All we can do is to exit with our money.

-

Another key monitorable is the sale of the new high GM products, that they have developed for fragrance and fmcg market. They sound very bullish but not sure how much we should take at face value. But then about two years ago these guys had estimated sales of some 400-450 Cr for Lasa by year 2018 or 19. They had sales of 67 Cr then. It was shocking display of arrogant confidence. Let us see how it pans out in this case.

Disl- still holding Omkar.

Imp Disclaimer- But that does not mean I may not sell in future. I owe NO explanation or definitely No Apology Or any prior approval from any one to sell my shares at any moment. As said make your own decision and be at peace. If you are unable to make decision or analyze this stock then this stock is definitely not for you. It is high risk- high reward kind stock. It can go either way from here.

12 Likes

Hi Girish,

Actually as outlined in my previous post, I think what is very important (and something which will make our job much easier) is whether the business in itself has some merits and can the numbers be relied upon.

I think it would be great if you have some insights on the pure business, technology wise, scuttlebutt wise or if you have done some primary research - spoken to any customers/suppliers/vendors/competitors etc. given the state of churn in the company - if you can consolidate such views on the business (forgetting for once the sale, pledge, promoter issues etc. etc.), that would be very helpful for everyone on this forum. Thanks.

1 Like

All that has been discussed countless times on this thread. No one knows more than what has been discussed so far.

1 Like

On a non business note and purely on risk reward:

I think this is a key notable here and how I look at it as well. Of course the purchase price determines the risk reward and for me personally the safe buy price has been up to 150 ish pre demerger (75-80 post demerger price). From there the risk reward ratio to me is 1:10 and that is what I have been working with if my loss taking ability on that is 20%. These calculations have been taking OSCL + LASA into account and is only valid for people who have both of them and not only OSCL.

The prices of the stock for the courageous / stupid (sometimes I wonder which is which in OSCL+LASA) do represent all the bad news possible in the world (with the exception of any unknown) and they are generally to me safe prices. That’s how I see it.

Disc- Just as Girish said, I may buy more or sell at a moments notice.

Notice on board meeting to re-classify promoter group.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/613741fb-b95a-4c13-a9d8-66f7a17f68db.pdf

http://www.bseindia.com/xml-data/corpfiling/AttachLive/2c802c7d-a961-4f64-9354-ef68561898c1.pdf

They are going to remove Omkar Herlekar from the promoter group.

This way the promoter holding will come down drastically?

Lets wait and watch. It’s reclassification. Logic says the shareholding would have moved to a major degree to Pravin, Rishikesh and Anjali Herlekar, that should be the deed of dis-association, but that is just my thinking. It’s the first time I am seeing this play out. I think whatever Omkar was left with is what he was selling. Full clarity day after.

So here is the outcome of today’s meeting

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f4cb3bb7-2469-4778-b69f-db639fced4ea.pdf

1 Like

Ok. Here’s the update. Phew.

Looks good. Also they have bought in an independent director. Will do some research on her antecedents.

Look forward to them showing their integrity to the shareholders; both Omkar in LASA and Pravin & Rishikesh in Omkar.

2 Likes