I would have never said anything negative about company. But now my confidence is also shaking. Its better to get out of this stock i guess… What is happening here ??? someone please get the real story. In next concall there is going to be questions blast on promoters.

I think Lasa listing is soon coming and they are making sure that all pledged shares are released and thats why the promoters are selling and releasing the pledges . Will have to wait for the listing to take a call , and moreover the market is much more forward looking than all of us so if infact there was a negative with the promoter selling the stock would have been much down from current levels, which isnt happening 140-170 range it has been around for quite sometime . Market also seems to be waiting for Lasa listing

4 Likes

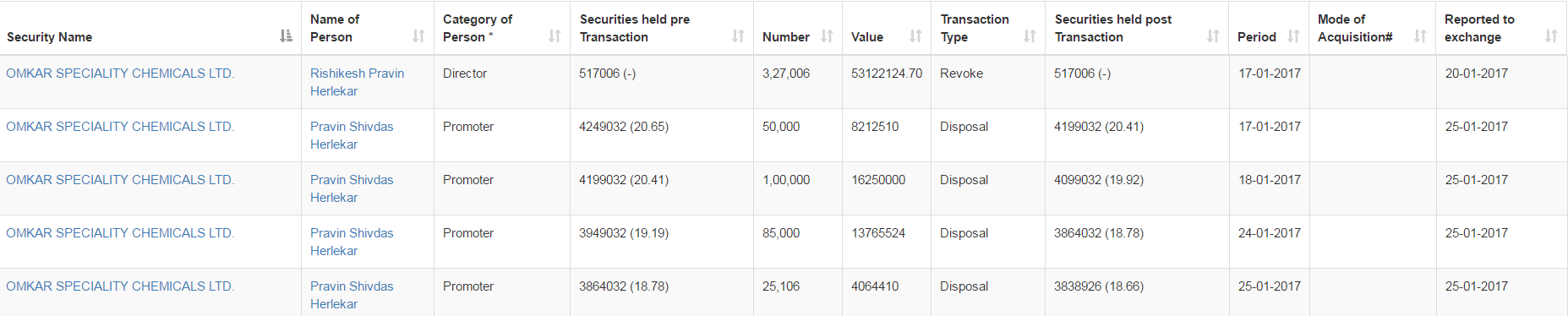

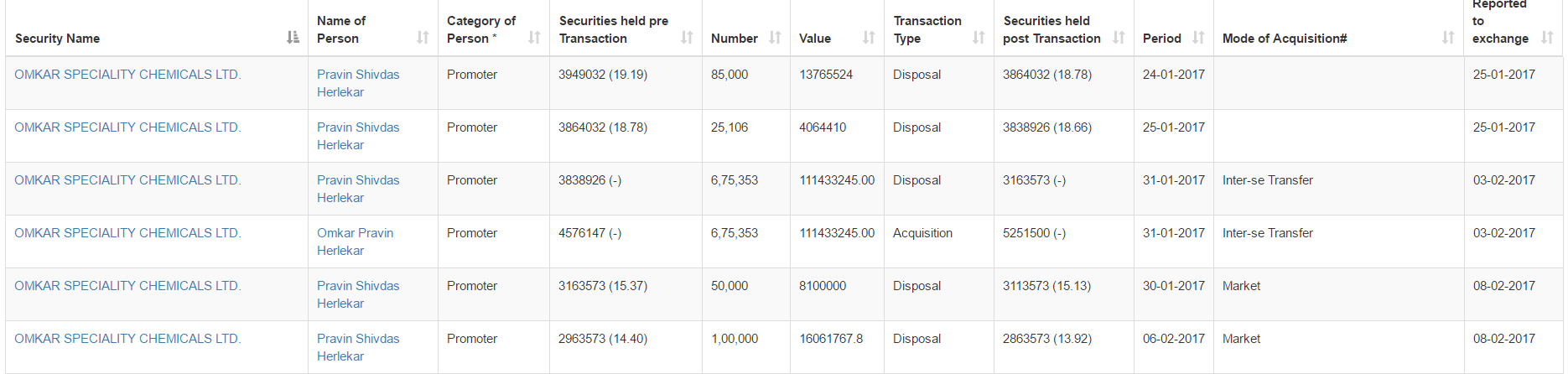

Inter-se Transfer of 675,353 shares from Pravin Herlekar to Omkar Herlekar on 31st Jan 2017. Seems the de-merger process atleast is progressing as per the plan.

I am a very very patient investor but my patience is wearing thin when it comes to this company.

Promoters don’t have basic decency to come out with a simple and transparent statement explaining all their latest moves. Investors send them emails and they come back with some statement or the other highlighting new issues. They have been taking their investors for a ride and have not been able to implement what they had planned be it the timelines or their percentage holding.

How will they run a business which has many more uncertainties and variables? If they could not foresee that they would not have the capital to de-pledge few months back, how will they forecast their business capital needs ? Either they are first degree crooks or completely incompetent in terms of running a business. Either ways I am off this train after the demerger if that happens by this year. If this present trend continues, I doubt market will give any premium to companies run by them. Ambit also had raised some red flags wrt their depreciation policy. I am no accounting expert but we need some forensic accounting and on the ground visit of their factories etc to verify what they have been claiming.

disc - invested

1 Like

I’ve a question. Since unit-5 hasn’t become operational yet, the expanded capacity of unit-6 is being used for growing Lasa’s business. What will happen after the Demerger?

As I went through the filings, I had a feeling of “I was blind, but now I see”

In my opinion, the shareholding changes of the year can be broken down into 2 phases:

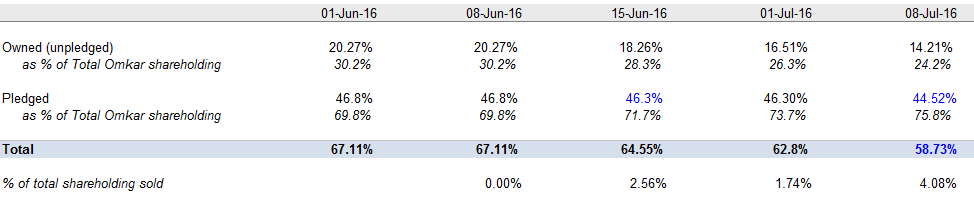

Phase 1: Pledging and sale of shares to fund the working capital of the company.

They basically sold a 10% stake in the company + pledged for working capital reasons. At a market cap of 300cr this roughly translates to the 27cr that they have pumped into the company as loans from the promoter → I believe their story. Would be good to know what caused this WC issue in June / July that they rushed to fund by pledging.

At this point, 76% of their ownership (ie their fortune) is pledged - > big red flag (should have caught it earlier?)

Phase 2: Selling to remove pledge and proceed with de-merger.

i.e they have sold about a 13% stake to remove pledge a pledged share of ~50%. They still have about 26% pledged to go, which means they might still have to sell a 5-6% stake (unless they get their cash back from the company).

Hope this covers some of the issues of the past 6-8 months.

10 Likes

Excellent write up Saran. Yes, if they don’t get the cash back they can always issue shares to themselves to settle it. That way the debt will also go out of the books and they can get some of their shareholding back again. That is they least they deserve for doing so much and risking their own fortune for the greater good.

Perfect…

And yes… looking at heavy volumes some or the other day…

With no price movements…

I believe these selling also has link with Amarnath Securities a brokerage firm… (bought up by Omkar Herleker)

May be these shares which are sold are having regular buyer as Amarnath Securities… because otherwise no price movement with heavy volumes is not justified…

Just a wild guess…

1 Like

The board meeting was supposed to happen at 12pm today, however, I am unable to find the results on BSE/NSE…not sure whether the results are announced yet. Can anyone help

http://www.bseindia.com/stock-share-price/omkar-speciality-chemicals-ltd/omkarchem/533317/

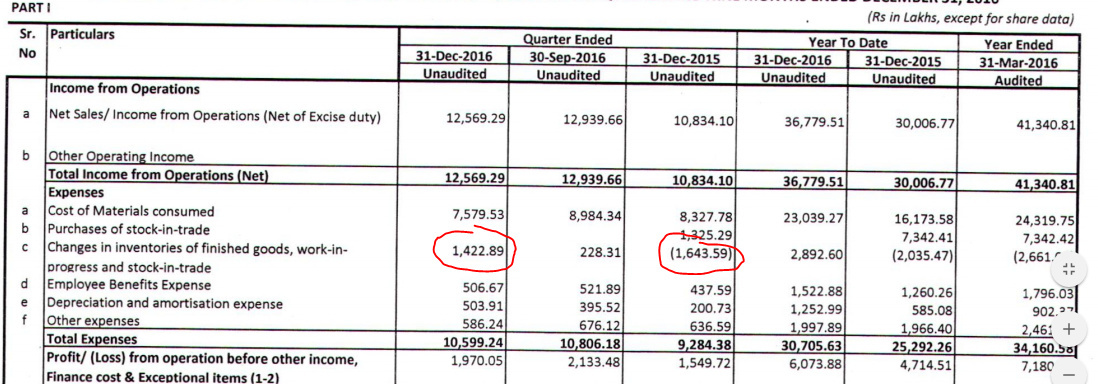

YoY growth of 16% on TL and 12% on BL. Margins have fallen a bit.

10% degrowth on QoQ basis for BL. Edit: Interest paid is also down on QoQ basis.

@investr

If you actually scan it minutely… margins have improved i believe…

Inventory addition to the tune of 14 crore… (If this was not there…margins would have been way better)

I don’t know if i am looking at this correctly or not… but it gives me improvement in operating performance…

Moreover YoY results are superb… so all is well

I think it’s reduction in inventory and not increase

Changes in Inventory is positive… which is increase in inventory (for Q3 FY2017) - 1422.89

The old inventory has been used for this quarter hence its a reduction on balance sheet.

My perception (right or wrong) after going through the results…

- GM of chem biz is down by 2% QoQ.

- EBIDTA margin for Chem biz is also down by 0.84%

- On consolidated basis GM is down by 0.4% and EBIDTA margin is slightly up.

- Looks like larger chemical business not yet turned around.

- It would have been interesting to know receivables level for chemical biz…whether same or down or increased?

- Inventory is increased by 15 Cr. That indicates management believes more orders coming in Q4. Bulk of the raw material is Iodine and that has 30 Day lag period after you place order.

- Looks like Lasa has done better.

Still 12% or so of total company shares remain pledged. I think they are finding it difficult to get loan from the banks. They are trying since Feb 2016 I am told. I am not hopeful on that front now. So not sure if promoters will sell more shares to depledge. I won’t be surprised if they do so. As per my knowledge around 12-14 Cr is still needed. Where will they get that much money from? Expect more surgical strikes whenever price reaches 170 or so  .

.

Really Sad that the promoters do not value their own words. How will investors take their words seriously?

Another Big IF is when Mr. Omkar gets to manage Lasa independently how effectively will he manage this business? I mean maturity and leadership skills. Unknown. I am told he is even more aggressive and Gung-ho than his Babuji! And we also know that they do not have solid CFO to steer these people safely. So still many ifs and buts. And lot of uncertainties in my humble opinion. Let us see how all this pans out. But this stock is not for faint-hearted. Roller coaster ride.

4 Likes

Changes in inventory is something which people dont understand . Lets take an example to clarify how to read changes in inventory once and for all

Opening Stock 100 units * 10 =1000

Production 600 units *10 =6000

Closing Stock 200 *10 =2000

Increase in closing stock for the quarter 100 (200-100) *10 = 1000

My sales are as follows

Opening Stock 100 * 20 = 2000

Out of Production (600-200) *20 =8000

Total Sales = 10000

cost of Materials consumed for the quarter is for the production (600 units * 10 ) =6000

However out of current production of 600 in the quater im selling only 400 units and remaining 100 are from opening stock .

So we have to add the cost of opening stock to P&L 100 10 =1000

And reduce the cost of closing stock to P&L 200210 = -2000

So net ( increase ) / decrease in stock will be = -1000 for the quater

TLDR

Negative means increase in inventory

Positive means decrease in inventory

3 Likes

I think the iodine business which contributes to most of the speciality chem business is operating at lower revenues,because iodine prices are at rock bottom(the latest import data shows iodine at around $18-20).These iodine compounds are commodity products so they cannot set prices.So as iodine prices rise,probably revenues,GM and profits could rise too along with Lasa’s

Omkar Herlekar is indeed aggressive,he had said that EPS for FY 17 will be 25(on a news show) ,we are still Rs9 away.

Full year eps may come to around 21. So this is available at pe of 8. I think it should be valued around 12. Let’s see