Reply to some of the issues:

- The concall transcript has the answer: Pravin replied that he cannot comment on his own performance. I thought it was sincere (willing to give benefit of doubt).

Reply to some of the issues:

Omkar Speciality Chemicals Ltd has informed BSE regarding a Press Release dated August 29, 2016, titled “Grant of Process Patent for development of molecule, 2-HYDROXY-3,5-DIIODOBENZOIC ACID”

Although I fell down laughing when that question on - how you rate on integrity- was asked in the conf call by that individual investor (like they ask in job interview- how do you rate on trustworthiness) …I think individual investors compliment analysts in these calls. They can ask question that analysts may not be able to ask. They can ask tough and some times embarrassing questions to management and are ready to look foolish. And that is their value add. It is one way of telling management, in a no holds barred way, what investors really want from them. Sometimes that kind of candid & blunt communication is good and necessary. After all it is our hard earned money. Isn’t it?

Note- I actually liked the answer given by Praveen to that question. That means he is not great marketing and polished type. I liked that fact. Typically CEOs are very articulate and answer “smartly”.

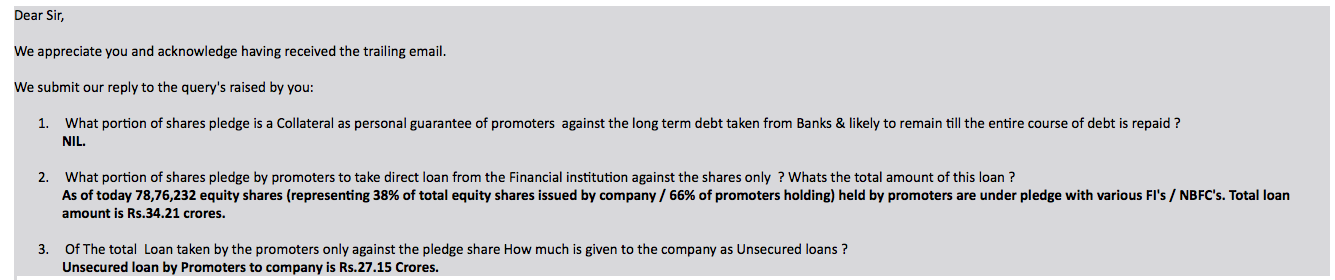

IS there a way to segregate the total pledge done by management on basis of ;

What portion is part of collateral to long term debt & what portion is pledge taken against the money withdrawn ?

Or am I wrong in this & all the pledge is done & money withdrawn by the promoters against that ?

I am not invested in the company but certain things that are preventing me to are listed below. I am not bringing them up to criticize anyone but to understand it a little more

Thoughts?

Navneet

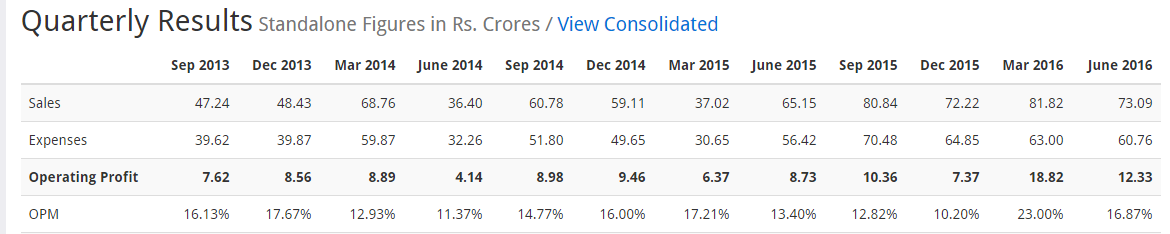

U have to check the consolidated figures as they are only in the chemical business & that would give more appropriate picture .

@hitesh2710 or @anil1820 or @Donald could anyone clarify how to ascertain what portion of pledge by promoter is collateral against long term debt & what portion is direct pledge created & raised money against by promoter .I am seeking guidance on how to do it ?

Sorry to come in on this when question was for seniors. I don’t think there is any way of segregating the 2 purposes you have outlined. Unless the management discloses it. In Omakr’s case the promoters have been repeatedly saying that the loans borrowed against pledged shares have been used solely for supporting company’s operations and working capital requirement.

To add…generally if shares are pledged to banks then it can be reasonably assumed that it is as security. But its likely that they may have specifically borrowed loans from the banks against it. If shares are pledged to nbfc’s then usually it is for taking loan.

For instance in Bodal, the shares had to be pledged as security for their overall borrowings. This again was informed only by the management.

Thank you Vivek for sharing the information with us…

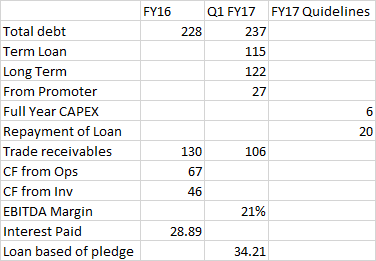

Loan and other details…

.

.

Now we need to watch the debt component closely…

Excellent efforts are being made,wonderful job.

Did you check at what price the warrants were issued vs market price? Just issuing warrants is not blanket shortchanging of the minority shareholders. If ET has it correct, this is what they write:

The stock, which has surged more than 30 per cent in the last four weeks, hit its 52-week high after ET Now broke the story.

The warrants to promoters are likely to be priced at Rs 155-160 per share against the current market price of Rs 144 per share.

Read more at:

I think they made a genuine mistake in expanding at a faster pace and erred in pledging their shares. The lack of financial insights of the promoters play a big part in this - they are technical people. Mr. Omkar may sound aggressive and may have painted a rosy picture earlier in his interviews but his father who started this company from his PF money sounds very modest to me.

Sept-Oct end is when they had promised to de-pledge, so that will be the next trigger

disc - invested in Omkar

Yup ! u r right . That was my initial observation after looking at the AR it got changed .

Disc: Invested.

Can some one help me with the below.

Not able to tally the Short term Loans and Advances & other current assets amount in the cash flow statement with the balance sheet entries

any news on release of pledge or deleveraging which promoters were to do in Sept/Oct

If anyone attended the AGM kindly share .