Please check this… it was told in conference call

This is what I am trying to point out. If they have paid 10 Cr to the lender, they should have got shares worth 25 cr de-pledged whereas their pledging has gone up substantially. Almost 35%. I’m not able to connect the dots.

Are you looking for this?

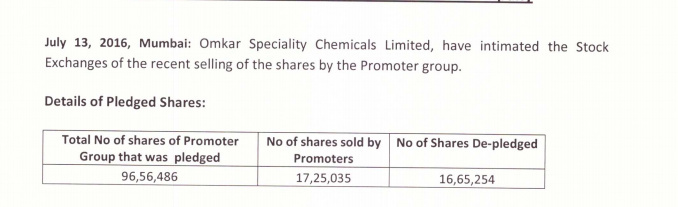

Their June ending filing to BSE is showing pledged shares as 84,14,186 and on 13th July they are sending this letter to exchange informing that their Pledged shares were 96,56,486. Ain’t it a mismatch?

They depledged 16,65,254 shares out of 96,56,486 shares which comes to 79,91,232 .For short term they would have pledged few more shares .If we look at all the disclosures we may get clear picture.

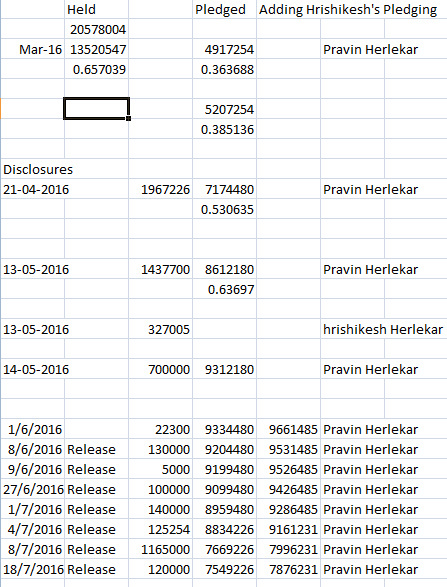

Worked out the disclosures… June pattern seems to be incorrect to me…

For now pledging is around 78L-79L shares…for sure… Cheers

Concall Transcript

1 Like

After reading con call:

-

If you were a bank or a big Investor why would you not get into the company?..I mean they have everything planned. They know what is wrong with the company and they are taking proper steps to fix this. I was really not impressed with the answers regarding why they could not raise money from other options.

-

They are still not sure about the whole de-pledging shares process. Some guy made him confused, when asked about LASA demerge and the pledging level (maybe reliance mutual fund) . He seemed to loose confidence.

-

There was one big positive note. They sold their own stake to bring down the debt level. Its commendable if they are not hiding something.

Please share your views if you read it.

Omkar Speciality Chemicals Ltd. has informed BSE that the rating for their bank facilities has been upgraded from CRISIL BB+/ Stable to BWR BBB for Fund Based Bank Borrowings and from CRISIL A4 + to BWR A3 for Non-fund based facilities.

DSIJ says SELL Omkar. But, all of the reasons cited are known to people on this board. Moreover, they forgot to mention the huge capacity addition which the new plant (soon to be commissioned) will bring.

Still looks like a value-buy to me, if it falls further.

DISC: Invested.

Few Red Flags for me

- Too much visibility of management , Is management too much focus on stock price than running the co ?

- Why director is diverting his attention when so much capacity is coming up & with that money they could have depledged more shares ?

3.When debts are high & high pledging & aggressive management accidents are bound to happen either through acquisition or diversification ? Are we heading for one or will avoid this time ? - Only silver lining is new capacity & spin off.

Vivek.

I have attended last few conf calls and have also asked questions to promoter. I am also invested in this stock so have personal stake in it now. I have been tracking this stock for some time. I thought I give my perspective after the recent call.

-

The pledging had gone to 70% because they took ST WC loan to meet one order. I found out from IR that that particular molecule (i forgot the name) is manufactured in India at this quantity for first time. They were urged by their customer to do trail run. Looking at the strategic importance of this molecule they decided to take a plunge. This is the data I got. We can debate if this is ambitious or fool hardy decision.

-

They sold shares worth 28 Cr and have already paid 10 cr to bring down the pledge. I was already told by the IR that they have decided to release all pledge before demerger. I knew it before the call. In any case they will de-pledge all shares in next 3-4 months. On the other hand all their selling is stopped now.

-

They have 18 or so crores to pay back loans. The promoter said they still need about 10 cr to release rest of the pledge and that they have raised from personal side to do so. The promoters are fairly confident the pledge will go in next 3-4 months.

-

The management arranged this call and answering our queries because we are demanding the answers. They will be happy to focus on their biz if allowed. I, for example, am continuously chasing their IR for answers. I expect the management to have calls and answer my queries. Even if some one thinks they are whiling away their time. I like the fact that management is available to answer the queries.

-

Demerger procedure is handled by competent consultants. I am for sure not going to believe that they do not know about implications of pledging. That might be the reason management had been advised by them to release all pledge soon.

-

After few calls I have developed serious doubts on the competency of their CFO Mr. Aggarwal. The man does not open up at all in calls. Why? Is he that shy even to answer queries on debt etc? Some of their financial decisions can be explained by the lack of good finance expertise within the management. This may impact the company when the company is rapidly growing. In one on one meeting with promoters this needs to be raised.

-

The promoter said they have reached a stage where they can fund WC by internal means and they have paid ST loan taken for WC. They will pay back all LT debt in next 3-4 years. They will use outsourcing for chemical biz to avoid more capex. Lasa has lot of capacity available. So no capex expected for next 2-3 years or so.

-

In the last fortnight the credit rating of Omkar is upgraded by a rating agency. This is positive for stock and comforting for investors. You can find announcement and details on BSE web site.

-

Recently the stock fell to 137.50 and then bounced back next day. I am told the reason is one FII (Driehauss) who was invested in it for some time was also selling and they completed their selling that day. So not only promoters but this FII was also selling in large blocks. Hopefully that kind of selling pressure will now recede. In any case some of us took advantage of these motivated sellers and bought more shares at lower price. Helped bring down average cost.

6 Likes

Ya, I first bought at 218 ,then at 178 and then at 141 but if I consider first purchase at 100% then the second was 50% , and the third 25%. But like management integrity and commitment towards minority share holder. At the same time I also believe that there could be some time before it starts moving and by the way the fiis will again start buying the stock once it crosses 200:blush: such is their behavior

such is their behavior

The percentage was for the quantity I bought

Fund managers add new companies to portfolios

This is an old article dated 30 jun

June quarter results out, very good from all respect. Most importantly interest has come down from 8.2 Cr in Mar to 5.5 Cr in Jun. Think the liquidity problem seems to be improving.

Discl. Small allocation

Did anyone attend yesterday’s conference call? Please update

AGM by Capital Market

New products and new markets will aid in higher growth going forward

The company held its conference call on 17th Aug 2016 and was addressed by Mr. Omkar Herlekar, Whole Time Director

Key Highlights

Of the total sales in June’16 quarter, Iodine constitute around 33% of total sales, Intermediates around 27%, API’s around 35%, Selenium Derivatives and rest from others. Sales from domestic market stood at around 90% while rest is from exports.

Working capital days stood at 111 days in June’16 quarter. Working capital days was at 116 for FY’16 as compared to 145 for FY’15 and 203 in FY’14.

Margins improved on account of better product mix and shift from traditional business to high margin products like intermediates, derivatives and API veterinary segments.

The de- merger process is going on smoothly and will be completed by end of FY’17. The whole idea of de-merger is to unlock the business value of each segment.

Going forward tax rate will remain at around 25%. The company continues to receive R&D benefits.

The credit facility was upgraded by the Rating agencies during the June’16 quarter.

For FY’17, management expects around 15% growth in net sales with better margins.

Promoter holding stands at around 58% and will remain at that level going forward.

Post Chiplun facility, there are no major capex planned by the company for next 2-3 years. The company plans to bring business growth going forward through a leased model of contract manufacturing in specialty chemicals business.

Total debt other than loans from promoters stands at around Rs 210 crore.

Received approval of 5 products and further 6 products are under pipeline for the approvals.

In FY’17, there will be further regulatory approvals of products and newer markets and newer products will be launched which will continue to drive growth going forward.

4 Likes