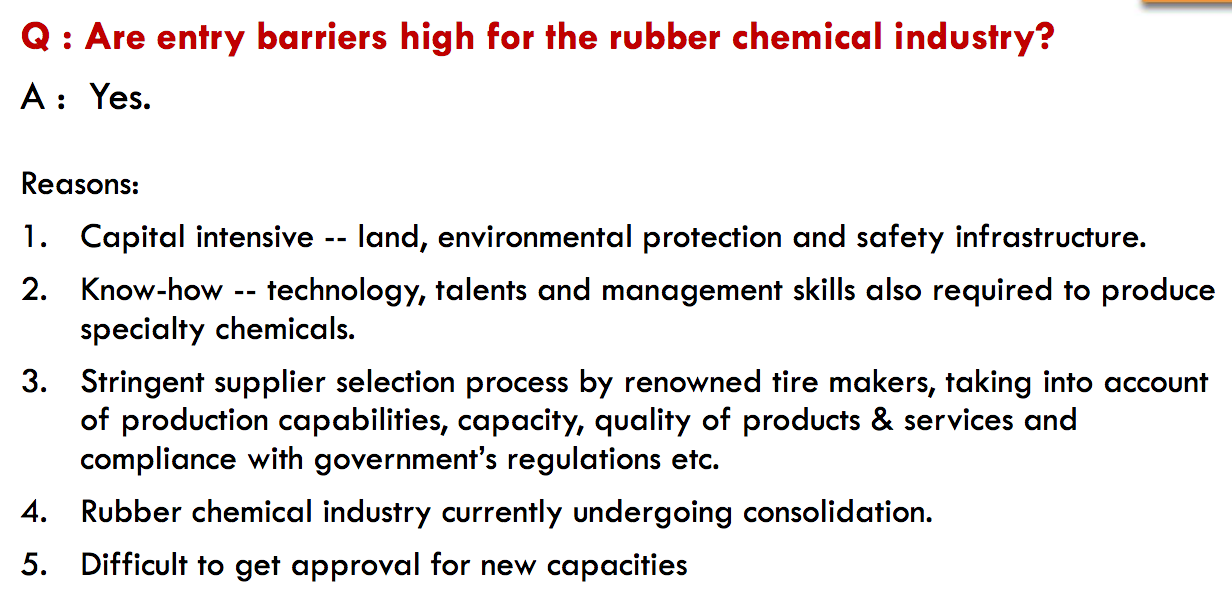

Similar response on above query was there in Nocil’s last conf call as well. Tyre manufacturers take over 1 year to approve any new supplier after extensive testing.

Other than one, all the others are showing good volume growth in imports which means either that anti-dumping duty isn’t high enough to keep them out or that demand is so high that the imports continue to grow. If it’s the latter, Nocil could do well. I also noticed that for the first three products, we are exporting about a third of the quantity imported at similar prices which could mean that domestic demand isn’t so high. I personally think the anti-dumping duty isn’t keeping the imports out because our cost of production is still high.

Management has said this a couple of times, that Chinese competitors continue to undercut the ADD. This is also the justification they give for the cessation of ADD being a non-event.

P. SRINIVASAN C.F.O From concall: (FY18 Earnings Conference Call Transcript )

I think that has been already announced in the Dahej game changer slide in the investor presentation. The current antidumping duties are applicable till July 2019. In this slide it is stated that the contribution increase in FY 2014-15 was largely on account of imposition of Anti-dumping duties which favorably impacted EBIDTA by 4%. So if at all if you are looking at a worst case scenario where the antidumping duty is reduced or suspended or gets removed, you can see a worst case of 4% but internationally from experience we have observed that as and when the antidumping duty gets suspended the CIF prices from the exporting country goes up. Even in some of our inputs, where ADD is in place or modified or revised downwards, the CIF prices gets adjusted suitably. Further considering the expansion plans, on a larger volume base, we are of the view that these impacts will be insignificant.

I recommend everyone to read Pages 23-31 in this which gives a good idea of where Nocil (replace Domestic Industry with Nocil in these pages) stands. I found lot of interesting observations by the DG here.

Also, as an investment, if Nocil is currently at 100% capacity utilisation and it takes time for new capacities to run full steam, in the near term, both the ADD overhang and higher fixed costs of running additional capacities at suboptimal utilisations should adversely hurt margins in the coming quarters. The opportunity looks interesting but I sense a lot near-term headwinds which may not yet be in the price.

I also don’t buy the promoter’s argument that 4% EBITDA margin will be the maximum pain if ADD is removed. Comparing 4% differential (increase) in EBITDA margins from a different year, at different utilisation under different market conditions isn’t the right way to ascertain what the difference will be based on current (future) conditions.

Market share of NOCIL in total Indian demand has increased.

While the Imports from the subject countries have declined during the investigation period, NOCIL has been consistently increasing production, sales and capacity and has increased its market share as a percentage of domestic demand in India. This demonstrates that there is no causal link can be established between the alleged dumping and such injury to domestic industry

The injury in Margins due to imports is only on account of poor management and inefficiencies in the NOCIL production processes. Reference is made to Safeguards case, where it was found that NOCIL had failed to become cost competitive towards imports and that this was due to its high cost of production.

The Report is of 2017 and as per my knowledge , the Anti Dumping Duty was extended even after this report till July 2019. Management is confident of further extension in these Duties. Around 50% of revenue of NOCIL is covered under ADD and the impact of 4% on EBITDA due to ADD seems tough to guess as these duties have been there for very long and company has witnessed high fluctuations in OPM over these years…

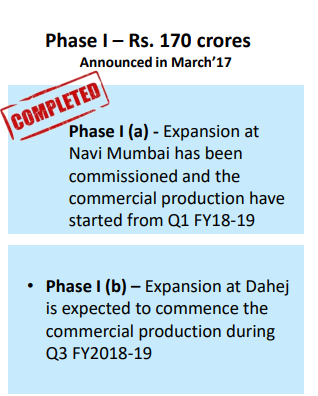

1st Phase of Mumbai Plant got commissioned and reached 100% Capacity Utilization within 3 Months. Dahej Expansion will come by end of this Quarter. They expect an Asset turnover of 2X after these expansions which will be completed by September 2019… Current lower prices of Raw Materials can help it to sustain the margins. Huge expansions by tire manufacturers is coming in next 1-2 Years and can be a good volume play if not the value due to some or the other reasons.

Regarding China , it will be tough for them to dump the products at the earlier prices due to strict environmental norms as well as high labor costs. US has levied 10% additional duty on Chinese rubber chemicals effectively from 24th September 18 and an additional 15% duty will be imposed effectively from 1st January 2019 as told by the management. We may have to confirm whether this is true or not. But this has led to the US companies opening their gates to other suppliers. Nocil existing clients like Yokohama Rubber and Sumitomo rubber are opening up the gates for their US based plants and this opportunity was not available earlier .

If ADD goes away , there is a possibility of China dumping again in Indian Markets but NOCIL would be able to scale up the exports due to new orders from Yokohama and other such players. OCCL and NOCIL management has continuously maintained their stand that the customer takes 18-24 months time before approving the supplier and it will be tough for China to disrupt. China is a leader in specialty Chemicals businesses and we can not undermine their research potential but next 3 Years looks excellent for NOCIL in my view.

Actually MBTS and TDQ were exempted from anti-dumping duty - one is rubber accelerator and another is rubber antioxidant. PX-13 and MOR were extended. Nocil has done admirably since the ruling in terms of topline, bottomline and margins - no question about that. The idea is to figure out what happens when these two are also exempted in July 2019.

The injury margin for PX-13 is 35-45% - That’s how low Solutia in Europe can go and 55-65% for other EU players. That’s a significant undercutting as of last year. (Page 32).

“Exporters/ producers in the respective subject countries have excess capacity of

1,19,500 TPA, 13,500, 6,220 and 58,630 for PX-13, TDQ, MOR and MBTS respectively.” This shows how much capacity is present outside for each. (Page 48) (btw China is not the main concern here but Europe)

The cost of production is way lower outside and the capacity as well is quite high for PX-13 - this is what concerns me if anti-dumping duty is removed, whenever that happens. Imagine having excess capacity at higher costs of production and no anti-dumping duty advantage.

It’s probably a naive reading of the situation by me but when seen in conjunction with the promoter selling, I am left wondering what if I am even remotely right. Whenever promoter cuts down stake, no matter the explanations given in concalls for the concerns raised, the information asymmetry the promoter possessed is only apparent in hindsight.

Management is confident of an extension. Moreover it will be determined by the DGAD about the current impact of dumping and further extension.

While PX-13 is dumped by EU , MOR is about China. .

Regarding calculation of impacts of ADD going away completely, we need to find how much PX-13 and MOR contributes to the sales of the company. May be you should write to the management for better understanding of the situation and exact impact of ADD going away completely.

March 2002 : promoter hold was 33.53%

September 2018: Promoter hold 34%

Between all these years , the promoter holding has been between 28 to 36%. I was too curious to understand these changes over the years as who entered when and exited when and is there any pattern of promoter’s increasing stake during good times or selling during bad times but did not give much attention. If possible , try to analyse this aspect too. Would be very interesting.

Anyway regarding the current selling ,

As per AR 2017 , Mafatlal Group have undergone a business restructuring in which Mr. Hrishikesh A. Mafatlal and Mr. Vishad P. Mafatlal have split their businesses.

NOCIL has come under Mr. Hrishikesh and he has brought his son also on the board. Promoter split businesses in 2016. Navin flourine has 38 Lakh Shares of which 30 Lakh have been sold and rest have come under non promoter category. Mafatlal Ind has plans to sell around 16 Lakh Shares between May 2018 to May 2019 of which around 2.5 Lakh shares have been sold till date. They may or may not sell the 16 Lakh shares as depending on their business needs. Both of these are listed companies and they may have requirement of funds for their business.

There is no selling by Mr. Hrishikesh Mafatlal who now owns the business.

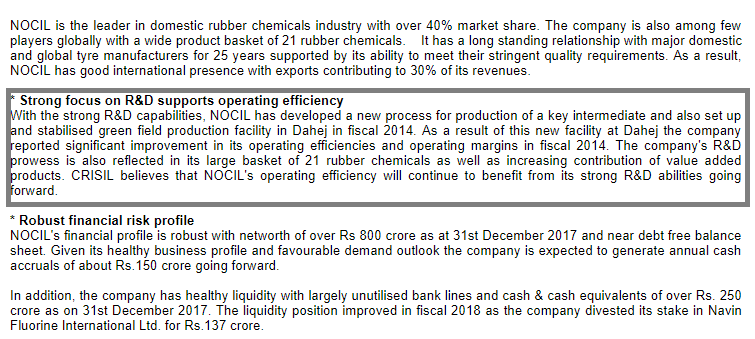

CRISIL Ratings Report highlighting the improvement in Operating Efficiencies due to starting of Dahej Unit as well as strong focus on R&D.

Visible Outcomes of Management Efforts to reduce Cost of Production. Looks like Dahej Unit started in 2014 which is fully automated plant has benefited the Company immensely.

I choose not to give too much importance to what management says. It’s in their best interests to talk up their business. Third-party data sources usually give an unbiased view of what’s happening.

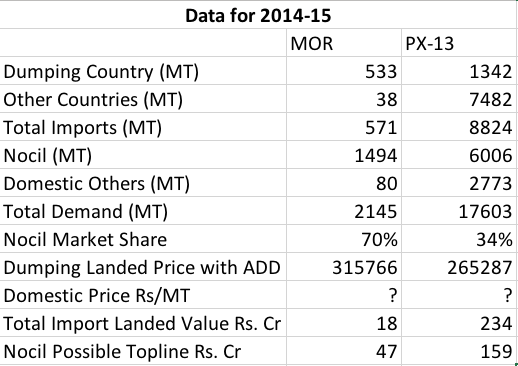

While the management hasn’t been very forthcoming on exact breakup of products (not categories) to topline and the numbers are redacted in the DGAD text, this is the MOR and PX-13 contribution as of FY15. It’s a math problem where enough variables are given to discern the required variables with a reasonable accuracy.

It looks like MOR + PX-13 was about 28% of FY15 topline and MOR vs PX-13 was in the ratio of 23% and 77% back then.

If you see Nocil’s market share in MOR (70%) and the total topline contribution, you will see why MOR/China is not the main problem here at all. MOR isn’t a big contributor to topline and they already had a big enough market share in it.

Now it looks to me like PX-13 is where they have aggressive grown market share thanks to ADD (looking at market share as of FY15) at the cost of importers and other domestic players (unlike MOR, PX-13 had a decent contribution from other domestic players in FY15) and my gut feel is that PX-13 currently makes up nearly 45% of the topline. I see the management has said 50% of the revenues come from products which have ADD. While we might think it might be equal proportion, I think it is not this way and this is why ADD removal in PX-13 could be very harmful for Nocil.

Europe was able to make PX-13 almost 40% cheaper than Nocil in FY15. Let’s assume Nocil’s efficiencies have improved and now the injury margin has narrowed to about 15-20%. This is still a big enough margin for a purchaser to choose imports over domestic when ADD is removed. When looking at Phthalic Anhydride ADD report for Thirumalai Chemicals/IG Petro, I noticed that inputs from other importers of the product (the paint companies like Asian Paints, Berger etc.) was also taken into account. What will stop Ceat/MRF/Apollo et al. to lobby against Nocil, if they can get cheaper tyre chemicals via imports?

Nocil has had tailwinds in terms of growing market, growing market share, growing margins so far because of ADD. If Nocil’s market share in PX-13 has doubled from FY15 to about 70% now, my concern is that, Nocil could not only lose this market share, but will also have problems with gross margins and consequently bottomline.

Disc: I am doing this as a case study to understand how ADD works and how it can impact a business both on the way up and on the way down. My interest here is purely academic. I might be way off or could have made some silly mistakes in my numbers, so please exercise caution and verify the numbers if interested.

Addendum:

Some more data which I found post writing this

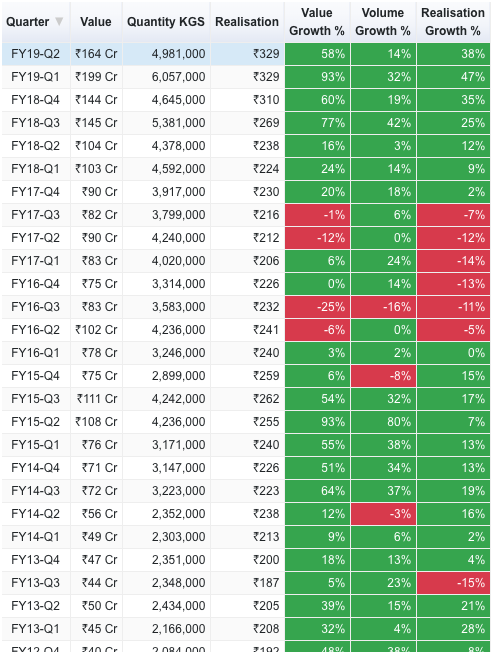

HS Code 38123010 which was the Anti-Oxidants for Rubber HS Code till FY17 has moved like this. Imports have lost a lot of volume since FY15. Remember this was when the market itself must have expanded. The 234 Cr imports in my table from the DGDAD report matches closely with the 255 Cr imports for this HS Code seen here. The realisation has dropped 20% since FY15 which I presume is to match the efficiency improvement Nocil achieved in the interim.

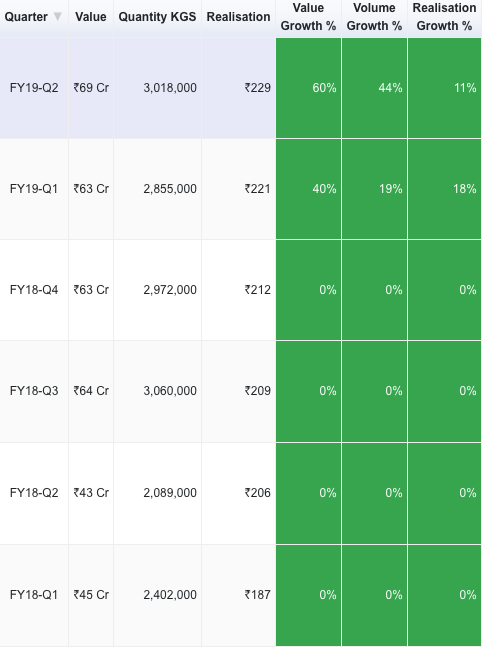

May not directly be comparable as this is for current HS Code (38123910) for Anti-Oxidants for Rubber.

De-growing in an expanding market implies again that PX-13 is currently above 40% of Nocil’s topline.

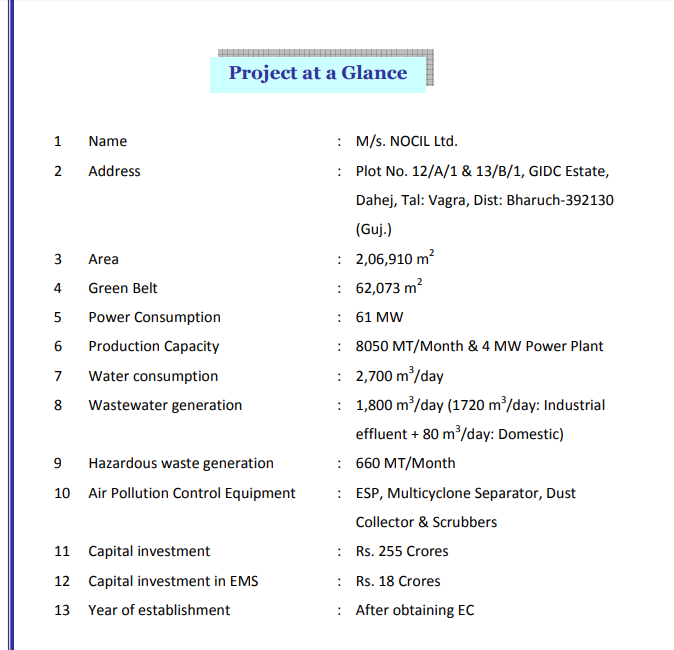

NOCIL has 2 plants : One at Dahej (10000 -15000MT per annum) and the other at Navi Mumbai (40000 MT per annum)

Dahej plant is more focussed towards manufacture intermediates which will then be transferred to its Navi Mumbai plant for converting them into finished products.

Company did a Capex of around 170 Cr recently in Navi Mumbai and some in Dahej . MOR is most probably manufactured here.

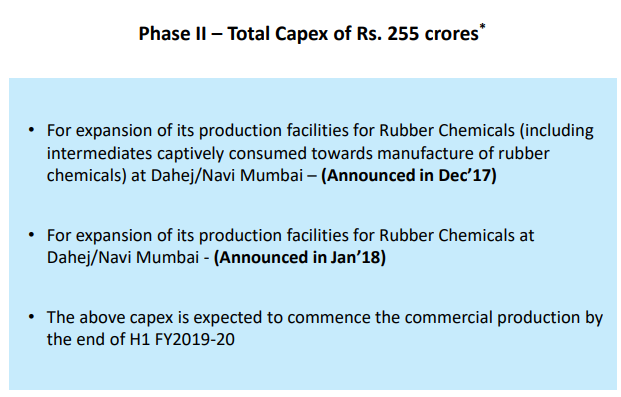

The Navi Mumbai plant has a Capacity of around 42000 MT per annum (3500 MT per Month) where it manufacture finished goods and intermediates. Another Capex of 255 Cr is proposed on this site. After Capex , the Capacity will be expanded to 97320 MT per Annum (8110 MT per Month) for this plant . Majority of Key and Final Products are manufactured here like PX13 , MBT , CBS.

One thing i am unable to understand here is that the Company while filing for Environmental clearance has shown the Dahej Land for Expansion and it showed Capacity of 40000 MT per Year at Dahej Plant while the capacity in my view is at Mumbai. Quite confusing.

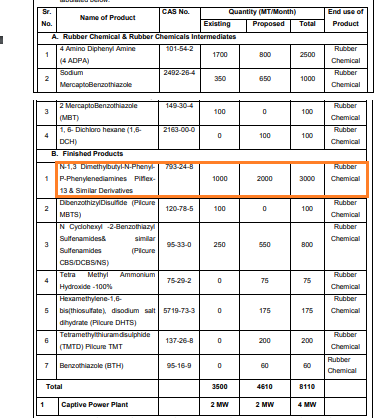

The following Products expansion will be done in this Plant.

Out of the 3500 MT per Month current Capacity , around 1000 MT per Month is for PX-13 , which is around 30% of Capacity of this Plant . No doubt , it is one of the main products of the company. The management is planning to expand the capacity of PX-13 to 3000 MT per Month. It will either result in lower cost of manufacturing due to large production or can backfire if ADD is removed (Provided their cost of production remains still Higher).

It is difficult to guess what is the existing Capacity for MOR is since it is manufactured at the other site. The prices of MOR and PX-13 are almost same.

The rest of the other Products have prices of around 200 p.Kg on an average. The total Capacity of NOCIL is around 50000 MT out of which around 12000 MT is contributed by TX-13 which comes near 24% of total Production (My assumption is that the PX-13 is only manufactured in One plant and has a capacity of 1000 MT per Month with 100% Capacity Utilization).

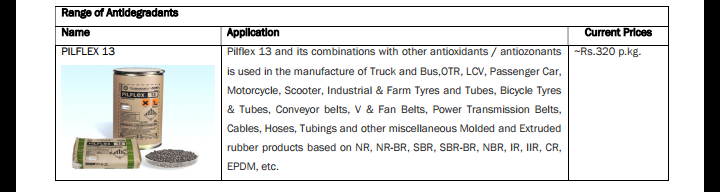

Agree…If we compare with the average prices and Sales of other Products along with the capacity , the impact of PX-13 on Top line should be around 35-40% of Total Sales.

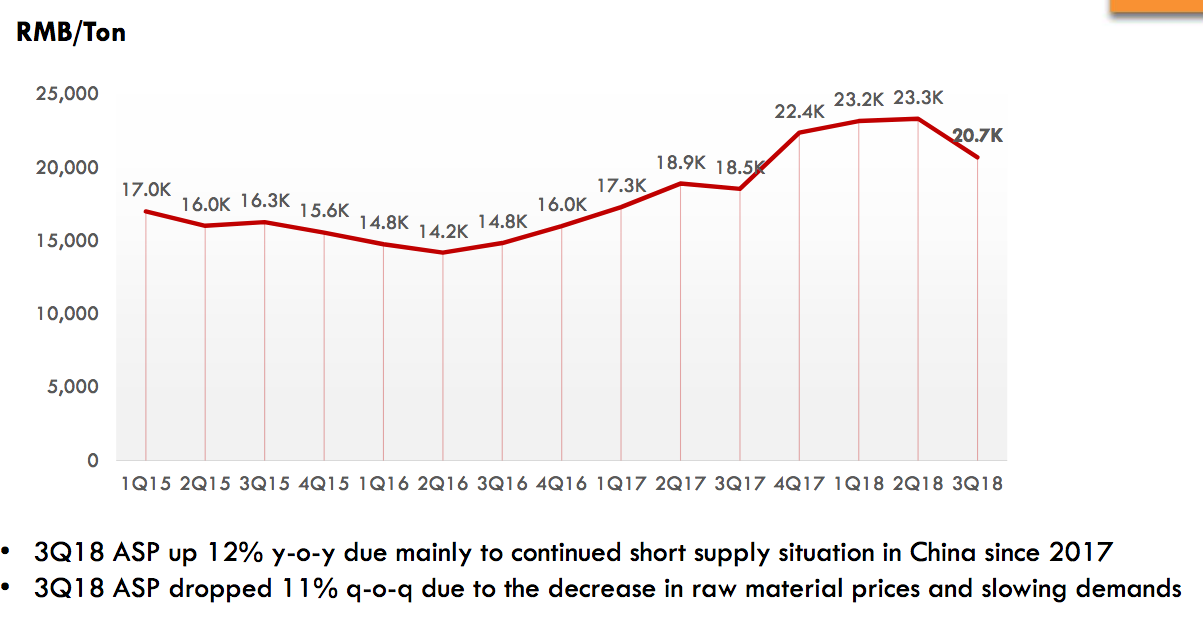

If we compare the MOR Prices , they are around Rs 315 p. Kg for dumped products after ADD (As you posted above) and NOCIL is able to sell it around 320 p. Kg at that time. so yes , Company is able to compete after ADD is in force.

For PX-13 , the Landed prices are around Rs 265 p kg while NOCIL is selling it around Rs 320 p. Kg. Difficult to understand that even after ADD , Nocil selling price was much way higher.

The difference in Data may be due to the fact that you have prices which are for Year 14-15 while prices i got is of 15-16.

The effects of ADD is around 20-30%.

I guess the client stickiness as these tire Manufacturers takes around 18 Months time to approve one’s product So it will be hard to shift suppliers very soon. May be the reason behind no criticism by these tire companies all these years despite ADD being in place from long.

Also Rupee Depreciation may make imports a little expensive and NOCIL Cost cutting measures can make them compete. I am a little Optimistic and biased towards NOCIL.

It is a genuine concern and possibility of it happening can not be denied due to the huge contribution by PX-13 to the Topline.

My Opinions :

The DGAD while revising the ADDs will carefully watch the current impacts of the Dumping. If Domestic Industry is still at disadvantage , i believe the ADDs will surely be extended. If they find that Domestic Industry is now in a much better position , ADDs can be removed but NOCIL will be able to compete with the dumping.

Higher volumes of production may reduce some cost of Production. Proper disposal of By-Products may also help to some extent.

Management has hardly talked about the dumping effect from EU. Lot of dumping of rubber Chemicals story is surrounded around China and Korea. Good that this aspect is brought up by @phreakv6 . Have to understand more from the Management in upcoming Concall.

In Navi Mumbai Part, the first phase of the project has been commissioned and within three months the plant delivered full capacity ans such plant take 12 month to stabilize.

Dahej Plant will be commissioned during the quarter and sample of finish products will be given to customer in Q4 of financial year.

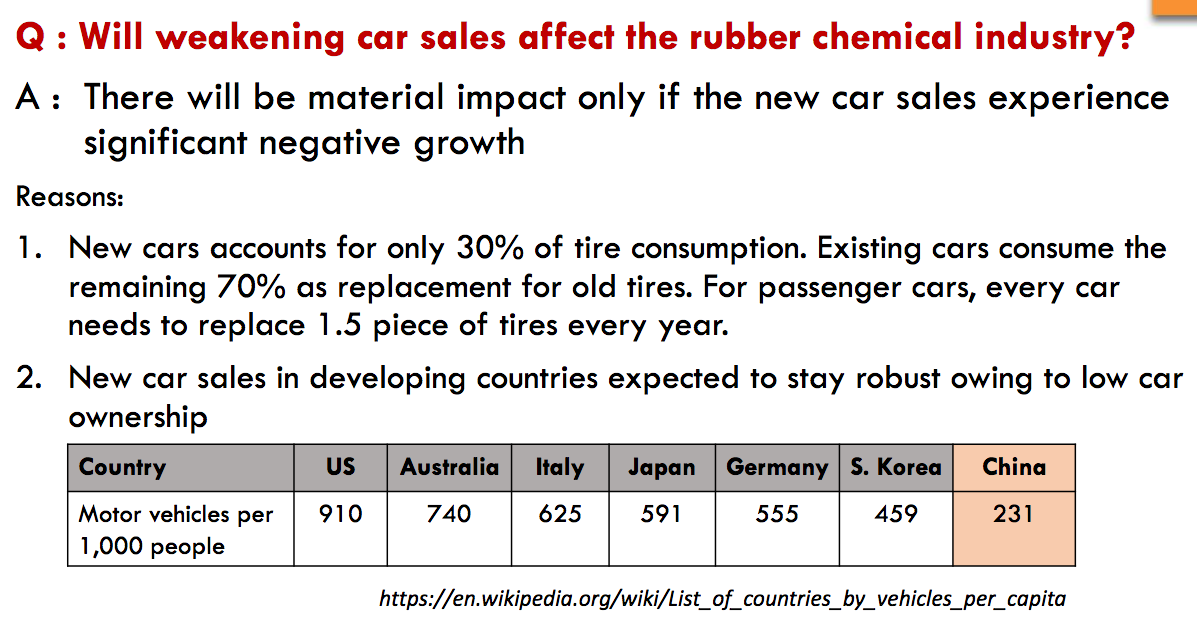

Business is expected to grow about 10 % in volumes during the financial year. Compare to last financial year.

Market Outlook

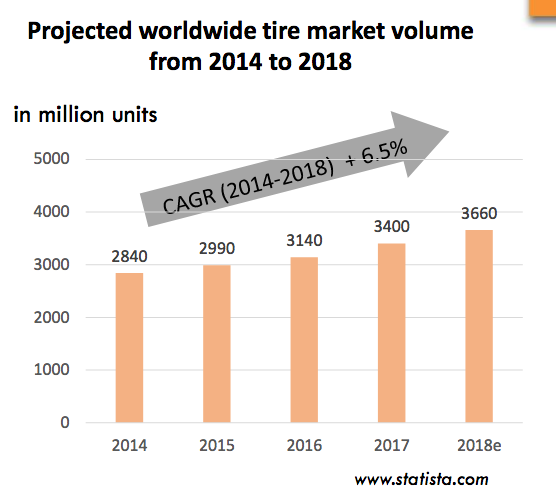

Customers are investing confidently and substantially in growth of their capacities. The global and investments are investing in building up tyre capacities to the extent of Rs.55,000 Cr which should fructify over the next one or two years. This is globally happening across the tyre segments of truck tyres, passenger car tyres, off the road tyres, etc. In India also there are few e major multinational companies, who are also investing and expanding their Indian operations.

Domestic tyre industry will grow between 12-14 %. For next 4-5 years. In line there are major r domestic players announcing their expansion plans over the last 12 to 18 months of about 12,000-15,000 Cr.

Due to recent disruption in supply from China due to pollution issue result in supply disruption to many of the major rubber chemical consumers including the large tyre companies. In this situation company had steady supplies to regular customers both in domestic as well as domestic market at reasonable price levels keeping in mind a long-term view of the business. This has generated a lot of goodwill for the company and it has deepened relationship with customers, which auger well for long term business.

China will be the major suppliers of rubber chemicals to the world but their pricing will increase due to the investments made by the Chinese Players and competitors in pollution control coupled with a strict surveillance so this will reduce the price differential that company was facing earlier.

On 3-4 % growth for rubber consumption globally will generate additional new demand of 40,000 metric tons of rubber chemicals globally per annum. Company is going to invest 425 Cr over three phases. S

Financials

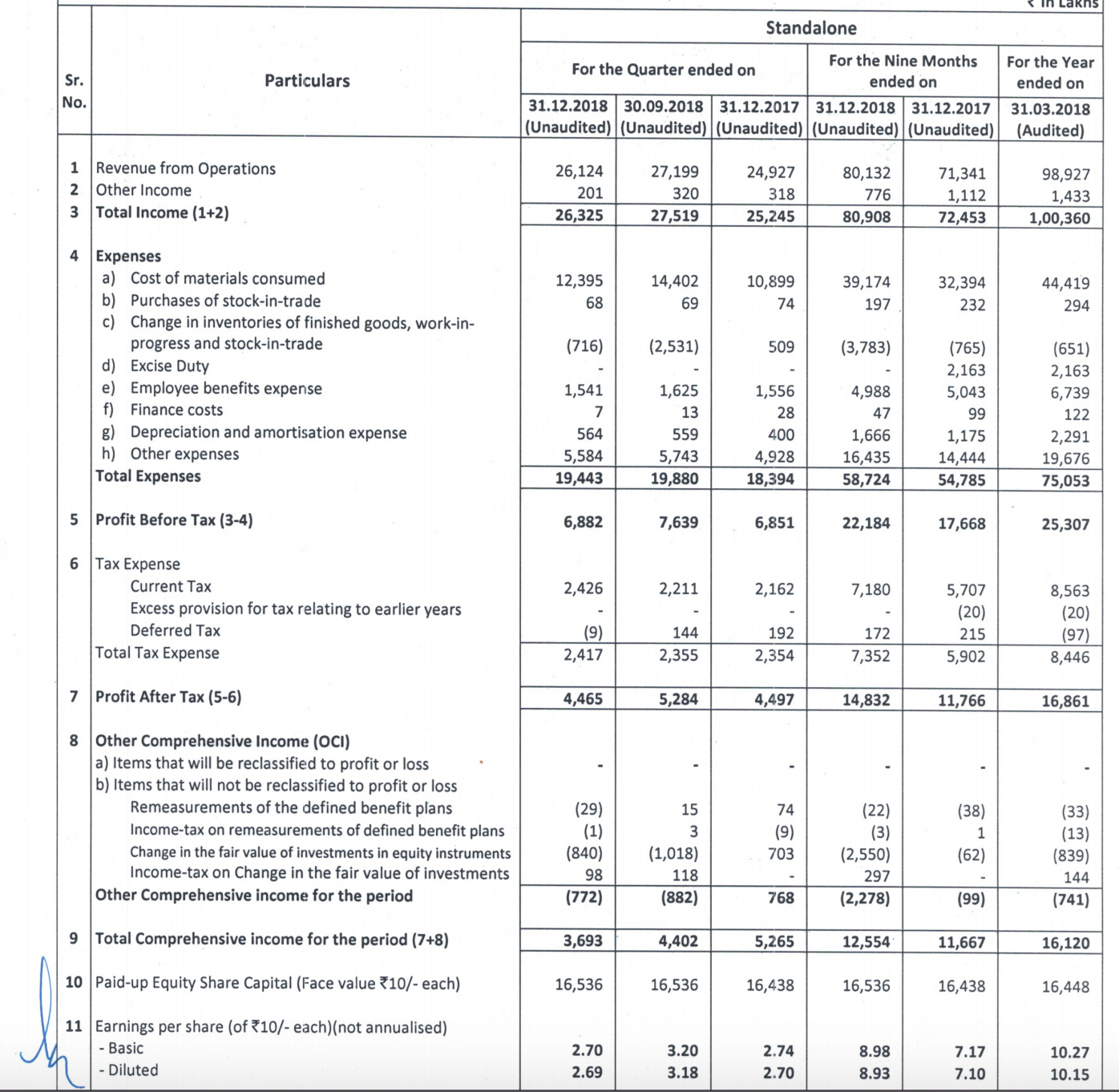

Q2 Results

Revenue grew by 19.5 % to 272 Cr compare to 228 Cr in last year same quarter.

Value addition for the quarter grew by 27.9 % to 153 Cr compare to 119 Cr last year same quarter.

Value addition percentage margins expanded by 368 basis points is 56% in the quarter

EBITDA grew by 46 % to 79 Cr from 54 Cr same quarter last year.

EBITDA margin improved by 528 basis points compare to last year same quarter

PBT grew by 39.1 % to 77 Cr compare to 55 Cr last year same quarter.

PAT stood at 53 Cr compare to 38 Cr last year same quarter.

H1 Results

Revenue grew by 22 % to 540 Cr compare to 443 Cr last year same quarter.

Significant part of revenue is export which have increased from 120 Cr to 155 Cr.

Value addition increase by 26.4 % to 302 Cr from 239 Cr last year H1 FY18.

Value addition percentage margins expanded by 191 basis points.

EBITDA grew by 46 % to 159 Cr compare to 109 Cr H1 FY18.

EBITDA margin improved by 482 basis points compare to last year H1.

PBT grew by 41 % to 153 Cr compare to 109 Cr last year H1.

PAT grew by 43 % to 104 Cr compare to 73 Cr last year H1.

Working capital cycle continuous to be in the region of 120-125 days.

Q&A

Kindly brief on export potential in the world market ? How will company scale up its business ?

There are two issues

It depend on how the trade tensions between US and China pans out.

Currently the duty structure proposed by US is implemented in two phases from September 2018, rubber chemicals were attracting 10%, and from January 2019 it is going to be increased by another 15%.

On world market

35 % of business comes from exports only.

The investments made by company customers like Bridgestone, Michelin, Yokohama rubber company is part of it. Company is already there with approvals and with existing relationships it is very easy for company to participate in these new company which is happening.

The second part of it is the trade war between China and US. China is company major competitor and as of now rubber chemicals had been slapped on an additional 10% import duty by the US authorities effective September 24th. There will be another additional 15% duties coming on rubber chemicals starting January 1st, now which means the China who is a largest exporter of rubber chemicals in the world would find it increasingly difficult to hold their position in the US market. Company existing customers like Sumitomo Rubber , Yokohama Rubber opening the gates for NOCIL to supply to the US-based plants, which opportunities were not there earlier

Out of total 450 Cr of CAPEX from which 900 Cr revenue will be generated how much of it is export ?

It depend on time of availability of raw material but focus will be to maximise domestic market business which has a value addition much better in terms of the duty structure. But company have already earmarked something for exports, The exports percentage of turnover which is about less than 30% in the long run will go up because the global market is much higher than India. India has only 5%-7% of the world market, so 93-95% of the global market. So company have to export which will lead to increase the export percentage.

As the duty structuring favourable to company does that will change post the ADD goes off ?

No company is talking about Indian duty structure which is about 10 % , 7.5 plus other charges is 10% higher. So the value addition per se even if the ADD is not there, in the local market is much higher as compared to exports – because the exports has Nil duty

What will be the impact of ADD going off ?

It will be 4 % on EBITDA margin assuming that duty is in place till July next year and company is in discussion for application of an extension of the same. It should be depend on the merits of the case.

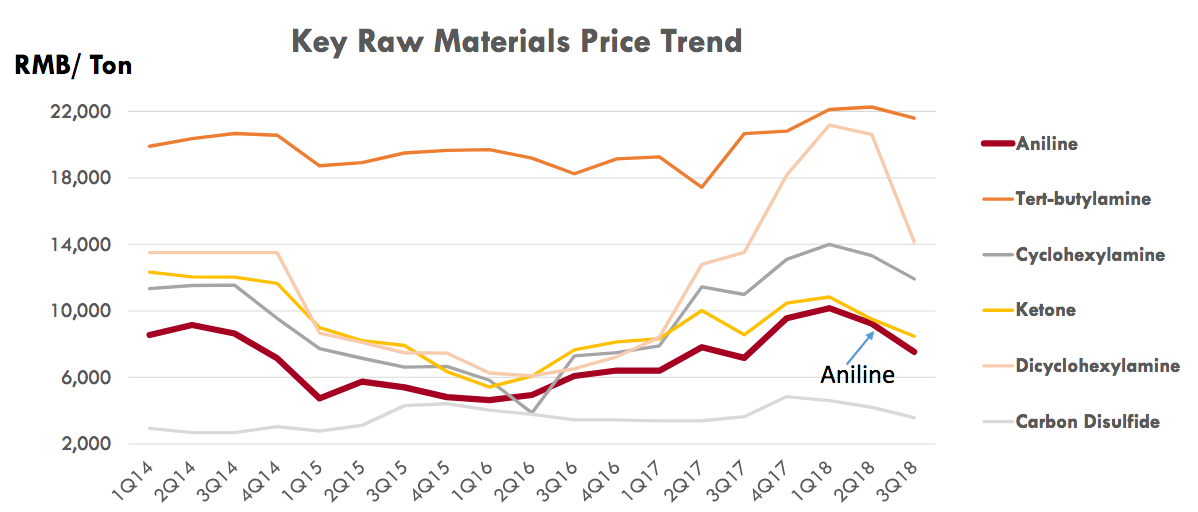

Is there any significant change in terms of basket of raw material availability plus price increase which can impact company margin ?

There is no price increase in the quarter in fact there is softening of raw material prices.

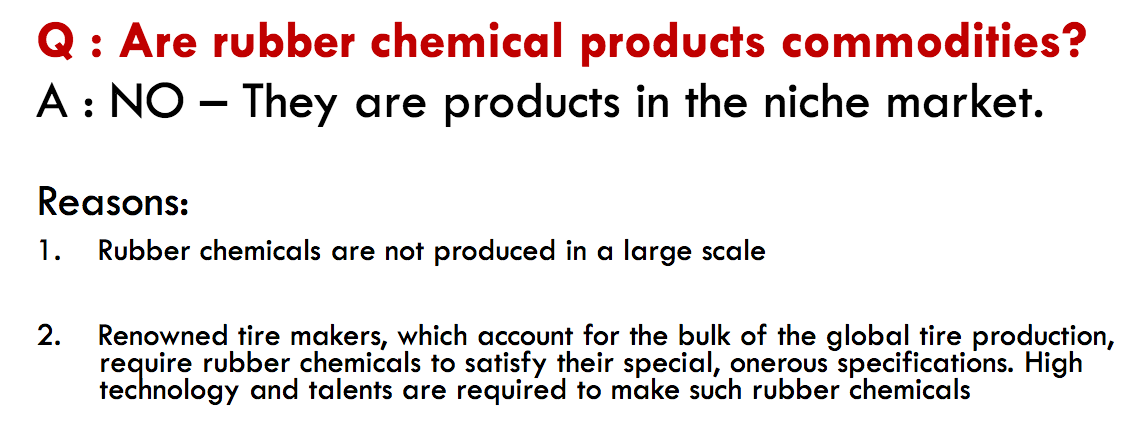

In EBITDA percentage of 30 % how it is difficult for other chemical manufacturer, other countries to establish some more capacity and compete because this looks to be very lucrative business ?

It is lucrative if one see from outward only. But one has to look at the parameters of the business in terms of technology, technology developments, the approvals of the product from the customer , so one has to look at all these parameters.

What led other companies to stop to enter into business ?

Globally about 80 % of this business is was controlled by three large international players. Most of them have now become shut, one has gone out totally, the second one is the mere shadow, they are only in one product in stead of about 15 products that they were in earlier. And the third one is there but have not shown any growth or anything like that because business goes through cycles and the business was not looking good. They lost interest. Maybe they lost patience. But it is very, very unlikely that there would be any capacity additions or any significant capacity additions in the western world or the development world, okay. There have not been any over the last five years or 10 years, any new additions.

For new players the gestation period for this business is rather high, for tyre company approvals, it will not take less than two years and is very difficult to dislodge an existing player. So there is inbuilt kind of deterrents to new players wanting to come into this business.

If there is demand in global market, did company will increase volume in high double digit number ?

Company is not looking at international market because India is a growth market and the first three or four customers all of them have plans individually of about 3,000 or Rs. 4,000 Cr investments over the next two years and on that market company have nothing to do additional , their requirements grow up and which is very natural that the biggest largest, most reliable, one of the oldest suppliers will get a reasonably good chunk out of that business.

Internationally company have about 2.5 decades worth of relationship with the top three, four, five, six companies in the tyre business and company will be intend to take advantages of that with additional capacities.

Company have evaluated the financial feasibility or the project feasibility on an assumption of three years to ramp up 100% utilization. Company endeavour is always to occupy or utilize the capacity much earlier. It depends on how the market pans out, but there are some movements in the market or actions in the market place which can temporarily distort this momentum.

What is the status now of China realigning their capacities and is there a case where these margins sustain through all incrementally from here?

There are two things to look on

Competitors like China Sunshine, Yanggu Huatai, Kemai Chemical, all these companies have invested substantially in their environmental CAPEX or pollution effluent treatment CAPEX with no major incremental additional production aspect. Now for example one of the competitor had to wait for permission from those pollution control authorities for almost a year or year and a half for getting the product on the commercial stream. So company have not t heard any major CAPEX being announced, one may not be surprised because they are currently in the process of rectifying all those noncompliance issues into a compliant zone.

There are some small capacity players who cannot be named individually but aggregating significantly, those capacities are more or less vanished or they are in the process of shutting down.

Does the antidumping duty placed on China by US place an opportunity for company but on the other hand it might also free up some capacities for China, does it have any bearing or any impact incrementally on the margins by any chance?

if a player is operating on the global basis and one market for whatever reasons trade war or other things kind of closes down opportunities in that market they would certainly look at other markets. Company is competing with China from last 15-20 years so company is confident of defending our position against the Chinese players both in the domestic market as well as the international market. The other thing a lot of that aggregation has been taken care, do not forgot that if they have to sell into the India, they are dealing with Rs.74 to a dollar today. Their production cost have gone up. The labour cost in china is also not cheap. So China edge of doing business is largely blunted. There would be an efforts to place larger quantities in to India.

How is the average selling price moving because in this quarter, there might be exchange gains also, because there is softness in the cost side. So kindly give some sense on how the next two quarters company is seeing the average selling price of the rubber chemicals?

To begin with there is softening of some input cost on account of the petrochemicals downside on certain products, amines and solvents. As a result, as a dutiful supplier company have e also passed on those benefits to the customer in the form reduction in prices. More important is company is able to manage the EBITDA percentage.

How much company is selling in US right now and how much china is selling in US and how this will play out in coming time ?

US and the western world accounts for almost 22% of the world market, India is only 5%-7% of the world market. US as a country do not have major produces, so they have to import. Either a producer from EU to supply or from other market including China. Company have a relationship multinational tyre companies, who have plans in US also. More important is to have a relationship. There have been enquiry form few multinational companies to supply to US.

In US if one has to impose antidumping duties or countervailing duties or any such additional duties on a trade partner, there is a two-month period of consultation which has gone through with the industry before the duties come in play. The first tranche of duties came in place on September 24. Two months before that or even more than that, the intentions were pretty clear. Normally it will take 1-1.5 year sustained effort to open up for new location for doing business with company international tyre companies. In the last three month company have at least two major tyre companies figuring in the top seven or top eight global tyre companies opening up the US plans to us for supply which have already started.

How much of revenue come from speciality products and where company would be having fairly high level of pricing power and completely fairly ?

The specialty business is not value added product it includes specialized application as well. It accounts for 25% of the total revenue. And the regular business or the regular products of rubber chemicals which is the traditional one accounts for 75% and typically the volume value also more or less in the same percentage

Does the customers who are looking to increase supplier from India are they coming for long term supplier. Because if China increase the supply then does that customer will go back to China ?

It is very difficult in tyre business to keep shifting and shuffling the supply chain. it is difficult to get into a tyre company as a supplier, will take time one and a half to two years for approvals and to start business. By the same token, it is very difficult for them to throw out a supplier, if the supply chain equations change in favor of somebody else. It does not happen overnight because remember rubber chemicals is only about a few percentage, 3 or 4% of a tyre, but they are very critical to performance. There have been changes in the past where millions of tyres had to be taken back. And those kinds of examples have destroyed large tyre companies, so no one takes that risk. So the new opportunity which company is getting is long term.

Margin in the business is 30 % so it is very high in respect to the fact that they had sent to general chemical segment so in next couple of years competitors will come so does company have plan any diversification ?

Company have opportunities to consolidate position n in the rubber chemical business some more before company get into o the diversification and as far as the margin percentage is concerned or the EBITDA percentage is concerned,

In dahej plant there is a combination of several initiatives, e. One is the technological improvement. Second is the shift in the export parameters from regular products to specialty products, component of the specialty being higher in export business, then there have been some optimization in the utility aspects maybe setting up a in-house turbine, then there is some anti dumping duty. It is a combination of several factors which has enabled company to achieve those parameters.

Between value addition and EBITDA company is able to see the traditional 31% has already come down to 27 % and this will shrink further.

Is there any diversity even at R&D stage as of now or there is anything at the R&D stage also as of now?

There are some products and company is working on it and there are also some samples.

Did company get any benefit of rupee depreciation in the quarter ?

The sales are rupee denominated but the prices are negotiated based on import parity. For a user in India company can buy domestic and can import. The import is going to cost right where the exchange rates comes into play and that is kind of parity that domestic players will seek.

With new capacities coming up and selling more in US and Europe did company have to go for a recognition process of two to two and a half year again or is it already there?

Company have existing relationship and it is just a expansion of new plant and they had already started to buy raw material from company.

When company will ramp up its plant in the export market than the value addition will be about 10 % lower than India ?

Yes

What percentage of company capacity is planning for export from the new capacity ?

Today it is 28-30 % toward export and in long run company will increase it on overall basis. It depends on how market pans out and how many expansion plans are coming of the tyre industry, how many additional volumes are going to get regenerated out of India. As a rule this 30 % export mix will definitely go up.

How will the new 74,000 capacity will ramped up to full utilization given the new American market also opening up.

The project of Navi Mumbai has been commissioned , the technical or the production team has been able to generate a 100% utilization on the plant capability perceptive. On the marketing side company have already placed 50 % of the incremental volumes in the market place, may be in the coming quarters, company will start consolidating further and to ramp that. As far as the Dahej plan is concerned, once the production comes, the samples are approved by customers, then the utilization will start.

On client engagement side , if company is supplying to one client in India and same client put another plant in Europe than how much time company need for approval ?

There are no issues on specifications as they are known and approved . The companies were interested to use company products in Europe plant It was a matter of sorting out what kind of packaging is needed for the European plant because the packaging and the handling systems can be different in India and in Europe.

To what extent is the cost higher of China product compare to company product made in India ?

Labour cost for a chemical industry is 8 % , 7% or so . It is major chunk of the cost.

Production cost in China are not unstable. It is a moving target, it keeps moving very largely depending on energy cost, raw material cost, other cost, fixed cost, environmental cost. Impact of cost depend on the specific rubber chemical because some are more environmentally damaging and some are less damaging, but has a very rough number, the environmental cost could be anywhere between USD 0.30 to USD 0.50 per kg.

Did the negative 8.8 Cr below PBT is toward M2M loses ?

It is a fair valuation method as per the IND-AS accounting standards.

What is the current capacity and on what level of utilisation company is working on ?

Beginning of the year company was about 55,000 tons production capacities and utilization was 97 to 100% depending on the product to product and the demand. Company is planning to expand almost double over the next one year thereabout. So by September 2019 or thereabout company should must double the production capacities.

In which other segment did these chemical can be used and how is the marketing shaping for company ?

In speciality chemical it includes specialized applications where it has specialty there in antioxidants something in accelerators and something in Zinc-based applications also. Each product has its own market. So it includes tyre industry. It includes non-tyre industry, Latex industry etc. Some pharma also is there

Company efforts is to use it in tyre, belting, footwear, condoms, hoses or gloves, these are the industries that company supply.

What kind of inflation company expect in employee expenses ?

Company work on principle of about 10 %.

In the new plant the employee cost will reduce because revenue will be far more than the employee cost.

What is the product pricing difference between company and China product ?

Both have the same quality and they had seen disruption from china from almost a year so they don’t want to depend on China so they are diversifying and it China is charging 3.1 $ for a product than company can charge 3.4 $ and they are happy to give it.

Why promoter has sold its stake ?

In 2016 when there was promoter split there Navin was holding about 38 lakh shares at the time split. They have already sold 30 lakhs, 8 lakhs still there and that has already come under the non promoter category in terms of after the SEBI approval or the stock exchange approval. Insofar as the Mafatlal industries are concerned, their broad approved a total quantum of 16 lakh shares spread over from May 2018 to May 2019 that is 12 months. Out of that they have sold about 2.5 lakhs or 3 lakhs and that is needed for their business growth. It is an independent board. MIL is an independent broad. NOCIL is an independent broad. So these are in the broad, has taken a decision and they are not going to exceed 16 lakhs.

Last quarter the crude price has shot up so did company see the full impact of raw material cost prices or company have long term stock for suppliers ?

In case of raw materials these are benzene derivatives, and company had a softening scenario. So company experienced a fall in raw material prices. beginning July or thereabout and it is still continuing. So as a result, company don’t experienced any major untoward in terms of raw material procurement.

The impact is more depend on the individual demand for the particular chemical and does not diversify follow the trends that crude is showing. So as a result when crude has gone up in the last few months for specific raw material company has see a drop at the moment.

Though nothing new in report that has not been discussed in this thread. Moreover to make the numbers look rosy they took effect of ADD removal at 2 % to EBITDA whereas promoters themselves told its at 4%. There could be few more Guesstimates as I havent gone through the numbers crunching provided by them.

After selling in small bits & pieces throughout August & September, this is the first large lot they have sold, taking the total quantity sold to around 7.5 lac shares out of 16 lac targeted. In fact, I always wondered why the promoters cannot offload the entire quantity in a block deal or two and get done over with it once and for all. Finding institutional buyers for the remaining 8.5 lac shares (costing just Rs.15 crores at CMP) shouldn’t be difficult at all for an otherwise good business like NOCIL. That would remove the overhang on the stock once and for all.

I think if one looks at what happened to Philips Carbon Black and also at reduction in rubber chemical imports (Anti-oxidants, Accelerators) in November along with reduction in Carbon black imports in November, the slowdown in tyre industry becomes quite apparent. In addition to it if you add the overhang of ADD (again, if you extrapolate what’s happening in Tirumalai Chemicals), I think Q3 numbers will be very interesting (from volume & margins perspective) and then onward as the market prices in possibility of ADD removal. This was the crux of my initial observations, now some confirmation seems to be showing up.

got a chance to meet the management recently and they indicated tht further selling by promoter will be via the block deal and tht they will not disturb d market for d same. ON anti dumping being extended they said tht dey will get more clarity on it only by march april