Tyre companies on expansion spree,

Company has upcoming capacities, showing excellent YoY growth.

Still stock is in narrow range for last few months. Is there any other trigger that mkt is waiting for?

First Navin Florine and now Mafatlal planning to sell stake

Huge downturn in price, any idea if any news or business fundamental change in it?

Fund Houses invested in the stock

| Fund | Mar-18 | Dec-17 | Sep-17 | Jun-17 | Mar-17 |

|---|---|---|---|---|---|

| L&T Mutual Fund | 3.679 | 2.591 | 1.872 | 1.353 | 0.893 |

| BNP Paribas Mtual Fund | 0.456 | 0.395 | 0.365 | 0.413 | 0.361 |

Despite the excellent financial performance by the company during past 4-5 quarters, only 2 mutual fund houses are invested in it and have increased their holding meaningfully in previous quarter. Mr. Peter Lynch would have been glad to see this

I believe Rs. 150 is quite an attractive level given the growth opportunity and strong financials

Yet to listen to Q4 concall - more notes to follow post listening to concall.

Would really appreciate to hear on - key risk to the business (especially from competition point of view)

Disc - one of key holding in my PF. My views might be biased.

A 30% correction from the highs is very common occurrence, especially after the rally that it has seen. Lot of good stocks stocks have done it in the past few months without any news flow and after good results (e.g. J M Finanacial, Edelweiss).

In fact there is good +ve news flow about the company:

- Govt has extended the anti-dumping duty on rubber chemicals

- Capacity expansion has been planned

- Auto sale are supposed to continue doing good

- Results have been good and consistent

The news of promoter selling 16 lakhs shares over a period of 1 year is a dampener. But then, I dont consider that a negative.

Q4’18 Concall Notes -

- Target expansion plans completion dates -

Phase-1 - Part 1 at Navi Mumbai Q1, Part 2 at Dahej - Q3

Phase-2 - Q1-FY20

Phase-3 - Q2-FY20

- All three phases, estimated capex is Rs.425 Crs. Majority to be funded thru internal accruals

- This expansion is likely to give an asset turnover of 2x.

- Range of about 20 products, 60-65% of total sales from rubber chemical to tyre industry

- Non-tyre industry forms 30-35% of sales catering to 8-9 industries e.g. latex, footwear, conveyer belt etc.

- In recent times, a lot of capex/ expansion plans have been announced by both international & domestic tire companies. Most of these companies existing customers

- Net cash surplus of Rs. 245 Crs.The return on capital employed is 24.5% as compared to 16% last year and return on equity is about 16.3% as against 10.7% last year

- Current capacity is 55,000 tones & operating at 100% utilizaiton

- Pricing is guided thru competions and contracts are on quaterly basis, There is no monopoly pricing

- For FY18 the volume growth was ~ 13% whereas margin expansion is largely on account of value added products and superior product mix

- Raw material prices are linked to Crude prices

- LANXESS India and PMC Rubber are major competitors in India

- China Sunshine, Sinorgchem and Kumho Petrochemicals are competitors overseas - are expected to not be operating at 100% due to environmental reasons in china

- Regarding sustaining all time high margins - Given the current conditions and the current outlook, we do not see much of a challenge as far asthe immediate six months or thereabouts thereafter we will have to see as how it unfolds out of China correction post environmental and basically what is happening there is that there are no new major capacity announcements or expansions announced by competition and given that information we believe we are in the right space to encash this opportunity.

- It takes about 3 yrs. to reach full utilization of the plant from commissioning. Basis current outlook the expanded capacity would take about 3-4 yrs. from now to achive 100% utilization subject to demand

-Management expent healthy double digit volume growth on account of expanded capacity getting commissioned in next 2 yrs. - Antidumping duty is in force till Jul’2019

- Strategy going forward - We are 4.5% or 5% global market share. We would like to increase it to double at least or more than that. We will see as and when the opportunity arises

Company’s cash position is really strong, given the automobile sector going to be in buoyant on account of EV penetration, the market size does not seem to be a problem. Margins might see downside risk but it is more than likely to be offset thru increased volumes.

Disc - Invested - part of core portfolio

If company is really going to perform well future…why promoter sold his shares …why promoter holding decreased…please enlighten me…if i missed some points here…please see share holding pattern…

Hope this helps…

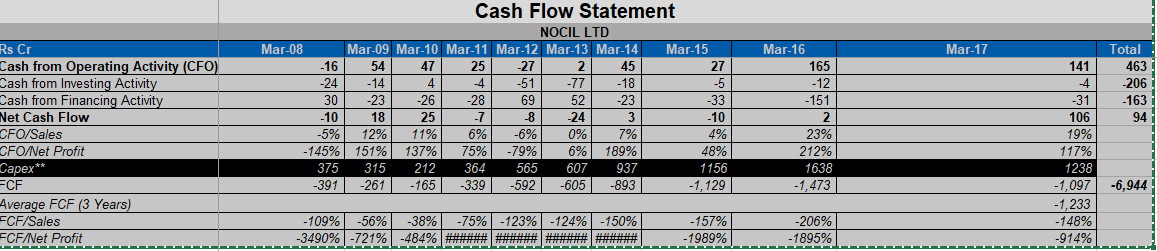

From the above screener screen shot…i think screener is not updating Capex figures correctly?

Is that correct?

Please advise…do i need to see the annaul report to enter these figures?

Please help me

There is note from screener.in on Capex column? Which means…do we need to enter manually from annual reports on this column?

If yes which perticular column from annaul report cash flow statement ( Consilidated or do we need to see stand alone)…

Note from Screener.in is :** Manually enter this number; Convert to Rs Crore if not already done in the Annual Reports; Use “Capital expenditure” number shown under “Cash Flow from Investing Activities” segment of Consolidated Cash Flow Statement available in the Annual Reports

I tried to perform some analysis of NOCIL compared with its China based peers.China Sunsine is the SGX listed and big RC(Rubber Chemical) manufacturer and have more information readily available. Jingshun Sinorgchem is another big RC producer in China and a private company,but does not have much data available in public domain.Sunshine and Sinorgchem are the biggest RC manufacturer.In India both Sunshine and Snorgchem compete with NOCIL.Though there is anti-dumping duty placed on product like PX 13 and MBDS not all product does not have anti-dumping duty .NOCIL currently manufacture 20 odd products and 6 of them have anti-dumping duty placed. Gone through the AR 2017 of Sunsine to understand the Chinese RC industry better and recent stress on Environment initiative of Chinese govt…

-

Chinese RC industry indeed going through tough time many small player has been closed and Sunsine enhancing capability of the plants and making them environment friendly.Mgt expect small player may come back after remediation.There is shortage of supply in 2017 and priced of RC increased by upto 30%

-

Sunsine is expanding capacity ,one plant producing accelerator will come on-stream soon Waiting Govt clearance. Sunshine is much bigger company in-terms of production .Produce RC of 1.7 LT/annum.NOCIL produce 55KT/annum.But Accelerator and anti-oxidant are the main product for both of them.

-

Around 33% of Sunsine produce gets exported outside of China. NOCIL exports 27%-28% of its produce.

4)Two-Third of world top 70 auto Tyre manufacturer is client of Sunsine. Including Apollo Tyres and Ceat.

-

Sunsine margin is bit on lower side(did not find the segment reporting for Sunsine ) compared to NOCIL. Sunsine Pat Margin at CY17 came at 11% while NOCIL at 17% Mar,2018.

-

Clear stress on Sunsine in-terms of Labour cost and Health-Safety compliance.

-

Mgt is optimistic about domestic sales as Chinese auto industry will grow from here on.

-

Volume growth for Sunsine was at 3% in 2017(on large base) NOCIL was at 13% FY18.

-

Sunsine trading at 12 times trailing basis ,NOCIL is at 17 times.

With capacity addition ,Indian auto sector growth ,anti-dumping duty and increasing Capex by tyre companies NOCIL is in good position.

I have invested in NOCIL in recent fall and tracking the company for sometime and waiting for some more slide as small-mid cap on some fall.

PHASE 1 commisioned

Q1FY19 NOCIL:

- Revenues up 24.8% at Rs 268.1 cr vs Rs 214.9 cr

- Net profit up 46.8% at Rs 50.8 cr vs Rs 34.6 cr

- EBITDA up 46.6% at Rs 80.2 cr vs Rs 54.7 cr

- Margins at 29.9% vs 25.5%

Unaudited Financial Results for the quarter ended on 30th June 2018

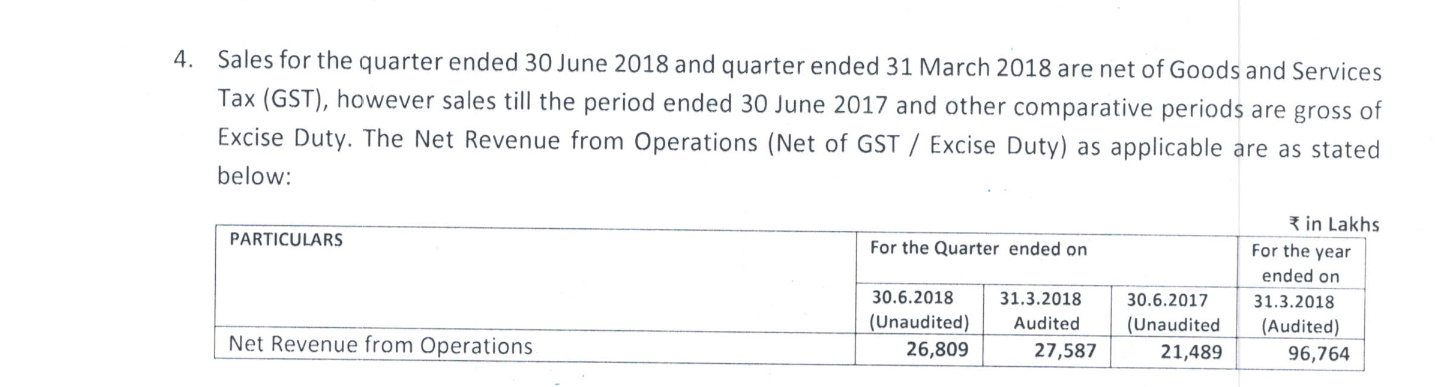

The revenues for June 2017 are 236.5 cr and not 214.9cr.

You need to adjust for excise duty in base year. Please refer to point No 4 in stock exchange filings.

Hi, I had one risk that I could perceive after looking at the five year numbers, sales growth of approximately 50% but receivables grew by approximately 60%, should it be a cause of concern? In fact, receivables for last year ended stood at almost one quarter worth of sales.

I would not worry too much about that. I would worry if the absolute increase in receivables is higher than the absolute increase in sales.

Hai,

What do you meant by receivable…please explain

And could you please explain inside trade

You are right. Receivables have increased from Rs.167 crore as on 31-Mar-17 to Rs.243 crore as on 31-Mar-18, DSO has increased from 82 days to 92 days. Given that the company’s stated policy is 60-days credit to its customers, this does seem to be on the higher side. The Annual Report also reveals that out of these Rs.243 crore, Rs.21 crores are past their due date and a small amount is even overdue for more than 6 months.

I presume the debtors are all credit worthy clients such as large tyre manufacturers (actual write-offs were zero during the year).

So though the numbers are not serious, this is one metric that has surely deteriorated a bit during the year and should be watched.