Current Price Rs. 54.05 per Share (Closing- 03rd May 2016)

Mkt. Cap. Rs. 869.07 Cr.

Book Value Rs. 29.14

PE 11.99x

Price to Book 1.85x

Price to Sales 1.19x

NOCIL Limited is an India-based company, which offers basic organic chemicals. The Company is

engaged in the business of manufacturing and trading of rubber chemicals. The Company offers

products, such as accelerators under the name PILCURE; anti-degradants, such as PILFLEX 13;

antioxidants, under the name PILNOX; pre vulcanization inhibitor, such as PILGARD PVI, and post

vulcanization stabilizer, such as PILCURE DHTS. The Company’s manufacturing facilities include

Navi Mumbai Plant, which is located in Navi Mumbai, Maharashtra, and at Dahej Plant, which is

located in Dahej, Gujarat. The products manufactured by the Company are used by the tire

industry and other rubber processing industries. The Company operates a subsidiary, PIL Chemicals

Limited, which is engaged in processing of rubber chemical products

The Company has successfully managed to improve on both Operating and Net Margins, which is

a good sign. With expected Net Profit growth at CAGR of 13%, the Company could manage the EPS

to touch above 6.00 by the coming three years.

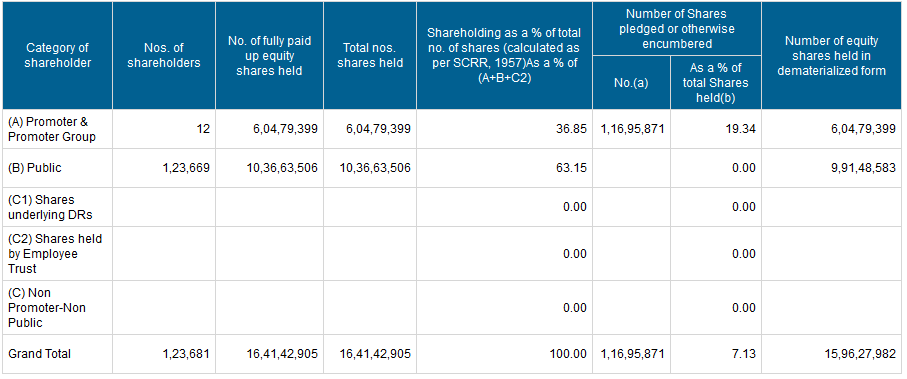

It is good to note that Dolly Khanna were holding 6,19,131 shares as of 31st March 2015. As of 31st March 2016, Dolly has more than tripled her holding to 21,80,801 shares.

Negatives:

China dumping material can hamper the profitability

The OPM have increased but growth in past 2 years have been flat

Thanks for sharing the details. One thing I noticed is: Promoter has pledged 14%+ shares as per screener.in.

It’s a negative thing I would assume. Pledged percentage: 14.11%.

Also, couple of cons are:

The company has delivered a poor growth of 9.57% over past five years.

Company has a low return on equity of 13.36% for last 3 years.

Hi Team,

This is my first stock specific post so please bare with me while I learn what we can and cant write for stocks. I have been tracking Nocil for last 2 years, I have been a silent reader of this blog but thought can contribute on this stock.

Over the last 2 -3 years, Nocils profit has increased due to decrease in raw material cost, including oil and reduction of interest as debts getting paid off.

Nocil also has cross holding in Navin Flourine and Mafatlal Ind , please have a look in the balance sheet in regards to the exact quantity.

Even though profit has increased , Sales haven’t increased which might be due to the fact rubber consumption has not increased. As previously mentioned by someone the company has passed on benefits of low raw material cost by reducing price for select customers.

Worst Case Scenario : Profits stagnate as sales don’t increase due to lack of demand from tyre manufacturer or profits reduce if brent price increase.

Best Case Scenario : Company is able to increase sales if Auto Sector revives and if crude stays at current level then profit increases substantially.

The company has increased dividend over the last 3 years and usually pays around 30% of EPS as dividend. Please note that few Maverick investors have been invested in the stock.

Quarterly Result is due on 27 July.

I do have investments in Nocil. Please feel free to delete the post if I have broken any rules or let me know the feedback. I just thought since I have benefited from the portal can contribute about a stock that I have followed , I am not an expert in fundamental analysis still learning.

Agreed that company has tried to improve the balance sheet. Following improvements have been seen in the balance sheet

I. Reduction in long-term debt.

II. Reduction in short-term debt.

III. Reduction in trade receivable.

IV. Improvement in Cash from operation activity.

But I think the company is facing sectorial headwinds

I. Tyre industry itself is facing huge headwinds due to Chinese dumping. You can read the tyre thread on the forum. Tyre industry being the biggest consumer of Nocil products will cause substantial headwinds for the company in terms of revenue growth.

II. Long term summation from 2006-2016 of net profit = 435cr and net cash flow from operation activities = 383 is showing substantial deviation, which does not reflect good on the management.

III. Promoters are holding 37.61% of company out of which 14.11% is pledged.

OCCL product is unique and has a guarded technology. The entry barriers are high for a new entrant. I’ve written a post on OCCL which may help you understand the OCCL business better.

NOCIL faces challenge from Chinese / Korean competitors. It’s profitability is largely dependent on dumping rules by government. If anti dumping duty is taken off from its products, it will face huge pressure on its margins. NOCIL is a leader in its product suite and is focusing on R&D. Business is facing tailwinds due to govt support.

Both are highly dependent on tire industry which is facing challenges of it’s own.

Disclosure: Invested in OCCL, not invested in NOCIL.

Thanks for the pointers Gaurav. I read the Tyre thread. If the government imposes duty on Chinese imports then this might be a good contrarian call as at the moment tyre companies could be pricing in the bad news. After the import duty domestic tyre sales can increase perhaps. I have read somewhere tractor sales have increased not too sure how much of Nocils rubber chemical is used in the tractor industry.

I am concerned about the point that you raised about cash flows and deviation, is anyone able to attend concall after results and see what managements view is for the year and if they project any sales figure for the year?? We might be able to get a better idea of management perhaps. Appreciate your feedback Gaurav.

Nocil had posted substansial increase in profit for last quarter… promoteres have ambicably split group companies . Risks. Promoters have recently pledged shares with jm finacial

Promoter Pledge have increased from ~0.85 cr shares in June 2016 to ~ 1.72 cr shares in Dec 2016. Does anybody have any idea of the purpose for the same

Company has good margins and has shown significant profit growth in last 2 years because of operating leverage lifting margins at dahej plant…but seems now company cannot grow profits further without sales growth.

And sales growth seems to be low from last 3-4 years and company is already trading at PE of 23 and PB of 4.3.

So from here if company does not sow sales growth…these valuations seem to be fair valuatons

Experts please guide

As per the company website.

“NOCIL today is the Largest Rubber Chemicals Manufacturer in India with the State of the Art Technology for the manufacture of rubber chemicals.”

Currently India is 5th largest PV market and India is expected to become the third largest in the world within the next three-four years.

Indian govt. is supporting Indian tyre industry by putting anti dumping duty on Chinese tires. So I think the company has potential to show good growth in coming quarters/years.

And considering the bull market current valuations are fine if not undervalued.

Umang

I believe PE and PB . are justified & reasonable considering the company’s position in the rubber chemical industry and the ongoing expansion funded from internal accrual.