The new capacity is already operational from 9-Feb-15 and revenue and net profit in q4fy15 is up 17.5% QoQ because of new capacity. The company should have revenue of 810-900cr in FY16.

Agreed - Often, when a well meaning management goes through a couple of crisis - they emerge stronger and more sensible. If nitin voluntarily exited CDR and they have learnt the lessons from the last capex binge, they hopefully have learnt their lessons in ensuring topline.

I am a buyer below Rs. 37-38 if there is a pullback but at the CMP of Rs 45, there is little MOs given the amount of debt.

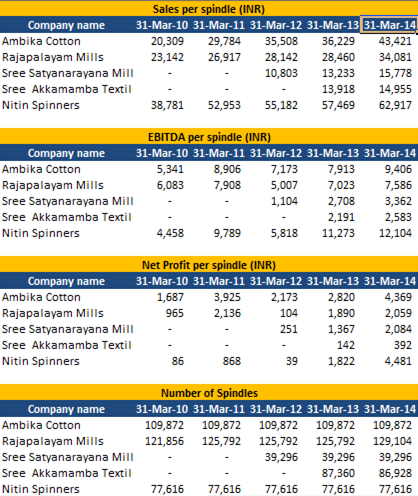

We had put together the table below to compare Ambika Cotton with other players operating in fine count yarn, and also included Nitin Spinners as it threw up interesting insights that need to be better understood. @Aveekmitra said it would be useful to share it with the group here to get your thoughts -

- Nitin revenue per spindle is higher than other players, which is understandable as we are comparing with finer count players where GPSS ~50+ for 80s count, whereas for 30s count (where Nitin operates) is ~200 GPSS (grams per spindle per shift)

- Nitin Spinners’ EBITDA per spindle is significantly higher than Ambika ~30% higher, which is counter to what is expected based on discussions with industry experts, so would love to get your thoughts

Clearly something to deep dive further to understand the high revenues and operating profit per spindle earned by Nitin…

3 Likes

I guess you need to relook into the data of Nitin Spinners once again… I forgot that I did a calculation sometime back where Sales / Spindle came around 39700/- … I converted 1 rotor equal to 7 spindles… It was based on a document I bumped into… I have the PDF file received from a friend. If you want I can mail that to your mail ID. They have around 3000 rotors.

So, you need to account for the Rotors which can produce very high GPSS of coarse count. Secondly, have you reduced, about Rs. 100 Cr of Fabric sales from total sales? How did you arrive at the EBITDA per spindle.

NITIN went out of my attention and so I completely forgot to post it earlier.

Hey guys,

So I bought some shares at 46bucks a pop last week. What I understand from the business and after speaking with management are:-

1- FY16 revenues will be 800cr.

2- 100bps margin expansion should come in.

3- No more capex planned for now.

4- Four days inventory (almost as if the goods are flying off the shelves).

5- They were steadily paying down debt from 2010 (300 odd cr) to 2014 (144crs). But they doubled their capacity this year and took 200cr loan for the same. Hence total debt is again back to 350 odd crores.

6- They plan to repay 30-35cr debt this year.

7- They are already at 95% utilization even after new capex. Which means FY16 could potentially be a BIG YEAR for them.

8- Promoters very well know this and hence they have bought a lot of shares from open market in March.

9- The PE is ridiculously low and the growth runway is huge.

10- I think the company will earn 60cr PAT in FY16 and if we assign a 10x multiple, the mkt cap should be 600cr which is 225cr now. Conservatively, it should see 80-90 levels.

11- Management also said that they will not dilute and also no more capex will happen until next year.

12- Their ROIC is decent at 26% post the massive capex recently. Should keep growing as the company increases profitability.

As long as there isnt a major worldwide recession, I believe Nitin is going to see better days.

Disclosure- Own Nitin Spinners.

Cheers

Neil

Thanks Neil - did you meet management or speak to them ?

Any qualitative stuff you can share with us on teh management - their vision, hunger, lessons learnt from CDR etc.

Hey buddy,

I spoke to them. It was a very general discussion. They were happy to answer our queries on growth plans, outlook, margins, cdr etc.

Few key takeaways

1- They are not going to dilute us. Investor friendly.

2- Repayment of debt will commence this year. Prudence.

3- Management was extremely clear on everything. Clear vision and goals.

Cheers

Neil

1 Like

I wanted to understand about the yarn conversion capacity of a spindle… is there a measure/ benchmark like how much kg of cotton can be spun in one spindle??

My query is as India became a hub of pharma manufacturing thanks to India recognizing process patents way back in 70s n low cost manpower n manfg cost similarly can India become a similar hub of spinning and garment manufacturing for world due to

-

Abundant and cheap RM cotton availability thanks to BT cotton introduction and still huge potential due to low acreage all over India.As such its leads to lower freight and VAT costs as well.

-

Thanks to TUFS setting up of large no of spinning and textiles mills over last 15 odd years

-

Lower manpower and manufacturing cost

-

Its main competitor China moving to higher end products and higher Yuan and labour costs in China.

-

Thanks to pvt sector power generation & APDRP policy large commercial users of more than 1 MW can buy cheaper power from energy exchange leading to lower power costs

-

Bangladesh and Vietnam are more into stitching work thanks to lower labor costs and not into yarn n garment manufacturing

-

Cotton opp size remains huge due to big demand worldwide due to its inherent qualities

If logistics infrarstructure also improves India can be spinning and garment supplier to the world

SO cos like Nitin Spinners and others which are at low PE yet having excellent ROCE of 25% ROE of 29% ,OPM of 18% ,debtor days of only 10-12 days and still available at 4-5 PE be rerated to 10-15 PE?

With local RM availability huge exports,rupee depreciation,govt policy encouragement cant Textiles be the next IT ,Pharma sector in terms of wealth creation due to both EPS & PE increasing?

Views Invited.

Hey Vivek,

Point number 4 is the main reason for my purchase as far as competitive advantage went. Plus the company has just finished capex which has doubled capacity. The numbers are going to look fabulous this year. None of this is in the price I believe as no fund house seems to be tracking this company.

Also, co has guided for 100bps margin expansion.

This looks like a good investment to me. One of the few ‘high growth, low pe’ original ideas in market today.

Hi,

Great discussion. considering the debt structure how is the company insulated from a big -ve event. Any large drop in FX rate, supply slow down can impact them in same manner as 2007.

IMHO sector tailwinds, good mgmt are cases for buying, but debt structure and commodity play limit the allocation.

regards,

PS- not invested. studying.

Hey Saurabh,

Well it is a smallcap and it would be affected just like any other company in the event of a major global recession. The management is very prudent. If you see their debt chart from 2010 to 2014…it reduced by almost 60% (they were consistently paying down debt).

In 2014, they doubled capacity with a mix of internal accruals and debt. Again, they again plan to repay 35cr this year and will keep repaying debt each year. They have specially said no dilution coming.

It is a semi-commodity play but you need to understand the competition scenario and barriers to entry. China is unable to compete. Vietnam and Bangladesh have huge issues of either raw material, labour or electricity hence even they cannot compete.

Indian textile majors are in a sweet spot at the moment.

Thanks Neil. That is helpful.

What i am kind of getting inclined is while textile industry as a whole will be in sweet spot, the individual plays could be difficult for a 10% allocation to any stock idea.

So probably we need to play the industry, have 2-3 stocks…amounting to a certain percentage.

these are my views and i could be completely wrong…

1 Like

MSP raised by 50 Rs per quintal.Is the cotton prices also rising world wide ?Can spinners passon the price rise?

23-JUN-2015 NITINSPIN Nitin Spinners Limited RELIANCE WEALTH MANAGEMENT LIMITED BUY 458964 73.04 -

Nse bulk deal

Hey buddy,

Oh definitely cannot put 10% of your wealth in Nitin spinners. I have 4% exposure to Nitin and 8% to Indocount since early 2014. So over 12% exposure to Textiles at cost. M2M exposure is above 25% thanks to the huge price rise in these 2 stocks specially Indocount which has been an absolute star!

So you are correct…you need to play textiles with 2-3 stocks.

Also, yesterday Reliance Wealth bought some 4.5 lakh shares. The interest is building up in Nitin. Hot money has started to enter.

1 Like

Latest Interview expecting 820 Cr sales with 18% margin !!

1 Like

If you see my post 27 days ago…I had mentioned that the management has guided for 800cr revenue guidance!!

Feeling vindicated…the stock was 45 bucks then.

CHEERS ALL!

2 Likes

As specified few posts back, Would be nice if we understand about the yarn conversion capacity of a spindle… is there a measure/ benchmark like how much kg of cotton can be spun in one spindle??

Sintex is also doing 3.3 lakh spindles and is aiming for 1400 crore revenue. So aiming for sintex as it is into another growing area prefab also .

1 Like

Nitin Q1 results are out

IMHO Work in process type of result…not bad category…Net Profit could have been better (finance cost is the culprit) !!

I think 820 crore topline is in tact with this result…in fact, if they hit the ball out of the park in the remaining quarters, they can slightly exceed it as well. The gap on topline is narrow and not 'Kitexish’

PS - not a buy/sell reco. invested and hence views will be biased

1 Like