Better to have money invested in a right stock through long term rather than take a sure loss through inflation and taxes and churning costs.

Interesting perspective Padmaselvan.

One thing which I would like to add is, PE from the current level of 23x falling to 20x (say) doesn’t mean that we are losing money. In your analysis, have you computed the probability based on actual index movement or the PE movement? Say it’s 23x now, after a quarter, say index remains flat but earnings improve drastically, so this will lead to a fall in PE. Basically I think higher index PE implies bullish marker expectations and if underlying earnings do not perform as much it will lead to a downward movement in prices.

Thank you valuestudent. Do you mean the most patient investor?

PE ratio should be viewed in context of interest rates prevailing in the economy. There is a wonderful (inverse) correlation between interest rates and PE ratios. Lower the interest rates higher will be the PE ratios. Interest rates in turn depend on inflation rate and inflation expectations both are trending down since last year’s good monsoon and with expectations of another year of good monsoon, inflation expectations will be curtailed. That means we can expect another year of low interest rates so PE ratios aren’t coming down anytime soon. the fact that markets have rallied despite lackluster earnings reports is an indication that liquidity is at play here and not fundamentals.

Many of the senior citizens I know are investing at least part of their portfolio in equities because their traditional source of income (Bank FDs) is yielding less than 7%. Extrapolate that to millions of fixed income earners around the country (and world) and you can see that money continue to pour into the equity markets. Fact that real estate market is not expected to do well in near future is an added argument.

Current levels of interest are lower than what we have seen in last 10-15 years so current PE should b higher than that we saw in last 10-15 years( except the bubble high levels in 2007-08). the only time interest rate were lower than current levels were the dot com burst period of 2002-2003 but that was mainly because lack of credit from industry due to overcapacity.

the surge of liquidity in the banking system post demonetization was expected to be temporary but it appears that liquidity is here to stay and some of that is spilling over to asset markets especially the ones that can be quickly bought and sold.

12 Likes

HiSivaprakasam. Probability is based on both PE and returns calculated from the index movement. Have tried to capture the return distribution of Sensex (based on index movement) if I invested every time the market trades at 22x-24x PE. I agree that earnings growth recovery from here will normalize the PE value, and it might not look as expensive as it is now.

3 Likes

With successive good monsoons, people would be with ample money and I expected a rise in inflation?

People with ample money will surely boost consumption so demand will rise. A rising demand if not met with rising supply will cause inflation to go up. However, at present economy is operating below capacity so industry can boost supply in response to rising demand so it wont lead to inflation instead it will lead to real growth.

There is a fancy term in economics called output gap which a hypothetical gap between an economy’s capacity to produce and actual production. It is hypothetical as no one can actually measure it but only assert presence of the output gap based on other economic indicators such as industrial output and utilization, credit demand etc.

Current indicators indicate that Indian economy is experiencing an output gap so rising demand will be met by rising supply until the gap closes and only after that inflation will begin to rise. How fast the gap closes is important. As businesses see rising demand well into the future, they build additional capacities so these additional capacities further increase supply thus keeping a lid on inflation. Eventually when anticipated demand does not materialize, capacities remain unused thus giving rise to output gap.

6 Likes

Every Model has its boundaries of working correctly; PE is no exception.

Japan Nikkai long grinding bear market is a case in point.

Market went down along with interest rate.

1 Like

Mahesh Vyas has written a lot about unemployment rate and jobless growth in India. He also predicts that India’s GDP will grow at 6% for the next five years.

I am not sure how demand can increase in such a scenario. I am not bearish about the market (yet), but I am not buying at these levels too.

Nifty valuation as per the famous Buffet Indicator is in a very attractive zone.

I think when we are considering the valuation of index and deciding weather it is expensive or cheap we have to consider the Buffet indicator ie Total market Cap to GDP ratio. the current ration for india is 64 which is below the historic average of 76. The historic high was 158% achived in 2007.https://www.gurufocus.com/global-market-valuation.php?country=IND

The ratio is updated on a daily basis in the mentioned link. So a weigtage for this ratio also should be given when considering the valuation of index.

I think @josephseby one must calculate this indicator using the publicly available raw data on gdp and market cap. I dont think it is at the levels you have pointed out currently.

i have just quoted the figures available in the mentioned link. If anybody can suggest a more reliable source it will be helpfull.

You could access the figures from the SEBI handbook of stats ( with a lag in Sheet 22 in part 1) . Available at this link

Best

Bheeshma

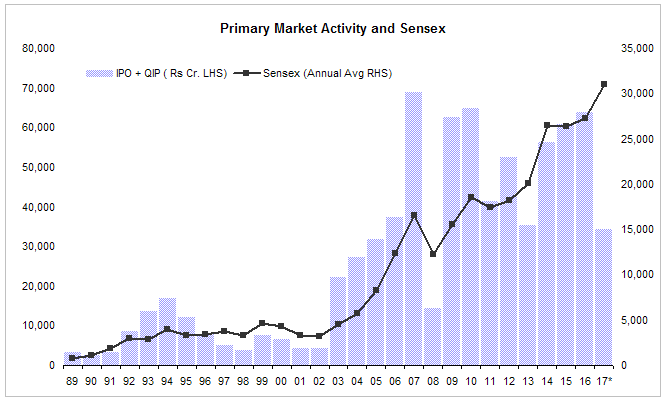

Activity in the primary market (IPO, QIP etc) is a good leading indicator of future returns in the secondary market. In the past, whenever merchant bankers went into overdrive and able to sell IPOs and QIPs in large numbers, markets have given lackluster returns in the next 2-5 years.

There is easy logic behind it. Merchant bankers are always after company promoters to go public and promoters decide to go public when they sense that markets are offering a high value for their shares. That fires up the primary market. IPOs in general are riskier than secondary markets as there is less information available about these companies and lacks a track record. When people earn good returns in secondary market they are not only willing to participate in the primary market but are also willing to buy the shares at whatever price offered which is usually high.

Source: Prime Database, BSE

*2017 activity is until May 30 2017.

Chart above shows that whenever primary activity reached a cyclical high in 1994, 1999, 2007 and 2010, Sensex has given lackluster returns in next 3-5 years. Another interesting observation from the chart is that activity in primary market was clustered around the market-high years and tapered off. This pattern repeated until 2013. Since then, our markets have been trading around fair value zone so primary market activity is seen at a reasonable level without any peaks or throughs.

So far in this cycle, primary activity has not reached a new cyclical high so it is another indicator that markets are not trading in the bubble zone. Having said that, summing all the IPOs and QIPs that are either scheduled or have received SEBI approvals, we may break past records this year. (e.g. recent SBI QIP of 15k Cr is not included in this number). I would begin to worry if the primary activity hits 100k Cr this year.

Details of forthcoming IPOs and QIPs.

8 Likes

RoE now is half of what it was in 2008

One need to look beyond indian borders to understand the reason for the low RoE

Some are predicting rebound of RoE, but I’m skepital of such theory

Blame it on overcapacity, misallocated capital(due to the dangerous experiements by central banks) and graying population.

Absent a war, this will be a new normal

3 Likes

While your logic and analysis is great, maybe you would derive more easily seen conclusions if you would substitute the absolute value of the IPO+QIP with an index which divides the IPO+QIP figure with the overall market capitalization.

4 Likes

Was in a south Mumbai club today morning. Had breakfast a while ago and on the table next to me a elderly gentleman was making an investment with centrum. He was being told about the last 1 year, 3 year and 5 year returns. When the advisor told him to maybe steer clear of small caps right now, the person putting in his money said “I am not interested in dividends. Invest me in growth. That’s where the money is”.

Then I came over to the other side to read a bit. 4 people on the table next to me were discussing stocks and dividend and merits of Marico and Zodiac. They have not discsssed our loss in the match yesterday for even 1 minute. Just a market sentiment indictor as is the nifty PE ratio for those interested.

13 Likes

Sometimes, I just feel that investors are simply discounting all the bad news - global economy, unemployment, stress on banks, sharp rise in rupee and finding solace by being stock specific. The markets worldwide are overheated and rising simply because of excess liquidity (QE). There is hardly any revival in growth. Every country has some kind of monetary policy as QE. The private sector capex is muted. With all these factors, trying to build a long term portfolio is insane. You are bound to lose your money in long term. You may make some profit due to short term bullishness. It doesn’t take anything special to understand this, neither PE, neither ROE. There are only two countries that will trigger the next downturn - US and China. US has exhausted all options to fix there economy, china has grown too fast with excess inventory and no demand. They are trying to dump them with OBOR initiative but its too late. Keep a watch on them!.

10 Likes