Rather than go by gut feel, we can do a little better by using probabilities and calculating the expectation. Of course this is not exact but hopefully a better estimate.

Let’s say there’s a 40% chance of Nifty earnings growing at 20% in next 2 years, 25% that earnings grow at only 10%, 25% that earnings don’t grow at all and 10% that earning fall at 10% CAGR.

Further, I assume PE expands 25% in case 1, remains same in case 2, falls 10% in case 3 and falls 25% in case 4.

Expecation thus comes to:

0.4X1.2X1.2X1.25 + 0.25X1.1X1.1X1 + 0.25X1X1X0.9 + 0.01X0.9X0.9X0.75

This comes out to 1.31 which is a CAGR of less than 15% over next 2 years.

Please feel free to tweak these probabilites to whip out any desired result of course.

I think we are looking at Nifty in Isolation and not considering the choices an investor may have. Assuming constant income for most of the population ( at least the ones investing in Stock market), what choices does one have? ( The below refers to domestic retail Investor / Institutional Investor)

Gold - traditional investment choice, and now no longer so thanks to the incessant education that gold barely beats inflation, Can this regain investment favor? Sure, if a certain Korean leader goes over the bend.

Real estate: This remains a recipient of money for primary dwelling purposes and will remain an investment for some people as is the case when Nifty remains at 15 or 25.

Art: I personally never understood this, and I can only think of this as a even more speculative bubble than the Nifty

FD/Bank deposits/Post office /Government : Can be one avenue where some money can be diverted.

Speaking of FIIs, the choices are:

Continue investing, or stay invested in Indian companies which they believe will deliver superior returns as compared to their home companies

Divert some %age of funds from Indian stock markets into their own domestic markets. Last few months the domestic funds have been able to absorb foreign selling, and this is a testimony to the liquidity sloshing around the markets.

The points I describe above are outcome of two factors:

TINA factor - There Is No Alternative ( to stock markets for inflation beating returns, & lack of investment avenues)

Pascal factor. As Blaise Pascal once famously said, all trouble stems from man’s inability to sit still in a room …today it means the inability of the Investor to sit on cash! For a change, this weakness is somehow the strength of the market post PE 25.

So what can prick the balloon? It has to be some unforeseen event, a black swan, which creates so much fear that the monthly SIPs stop and retail investor stops buying equity. If I interpret today’s investor mood in interacting with fellow-investors its not so much greed of making more money, its more of TINA that I see, and the supposed stomach to absorb losses - presumably in range of 10-15-20 %…and not many have seen 60% losses in their investing career!

Some excellent points reinforced by you. I don’t want to repeat them.

Yes very few have seen and managed 50-60% draw down. Unfortunately the current advisory comes mostly from them. Not saying you close your ears, but alert and take every advice as a pinch of salt.

The market’s nightmare is a massive gap down opening. And you can’t do much unless you are hedging using both long and short. But these events need some serious emotional crowd breakdown which can happen on extra ordinary events, that’s why we have 5/6 times in a century. And hedging does not protect you always unless you are engaged always meaning more transactions, more opportunity cost etc.

I guess folks need to be prepared for risk management (to add and build lesser risk free portfolio, maintain losses which are recoverable) and maintain metrics to ensure they are in line. Even if market beats you down still your exposure will make sure you are within risk appetite.

Yes, but let’s not confuse probabilities with possibilities. That 40% drop, even if I give it 10% chance given today’s information can happen. Facts and hence probabilities can change in a jiffie.

This para from John Huber best articulates my own thinking:

One good lesson here is that it’s important to own stocks of companies that can take advantage of crises rather than be at the mercy of them. Even if you are fully invested and all the stocks in your portfolio decline, if you own shares of businesses that can capitalize on the meltdown, the intrinsic value of your portfolio will increase (and stock prices will eventually catch up with that value). Almost every crisis turns out to be an incredible opportunity for those who can think clearly and make rational decisions.

In short, the following helps survive a meltdown -

Don’t leverage for investing in stock market - if you do, you are simply magnifying the impact, the same as the operating leverage does to a company’s financials.

Don’t trade more than invest - this means keep your trading portfolio very small percentage of your investing portfolio. This is merely recognizing that a small trading portfolio is probably necessary for feeling “active” in the stock market and takes care of the emotional need of an investor. If you dont have this emotional need, then don’t trade Its that simple.

Don’t own junk. This is stated with a lot more polish in the statement, dont own for 10 minutes what you dont want to own for 10 years! An MS-Shoes, a Unitech, an Essar Gujarat may all be hottest stock of the moment, but these are the ones that fall the hardest. In fact, this adage is suited to not just speculative stocks, but also the larger investible market - don’t own the hottest stock, unless you bought it with a really high margin of safety, i.e. when the Nifty was at 15 or below! An Asian Paints, a HDFC bank, a Reliance survived the bottoms of 2000, 2008 and will likely survive the bottom of 2018/19/whenever, even if they were to go down 60% from here. But will the Investor make money after it recovers? Likely he will need to wait a long time to recover his capital and then make money, but an investor who invests after a 60% drawdown will make much better return much more quickly. But that means that the investor needs to sit on cash till this meltdown happens, and when it happens, have the courage to invest. Both are MUCH harder than it appears when written here. For those of you who recall the 2000 or 2008 crises, you would remember that not getting laid off was the goal during those times, forget investing

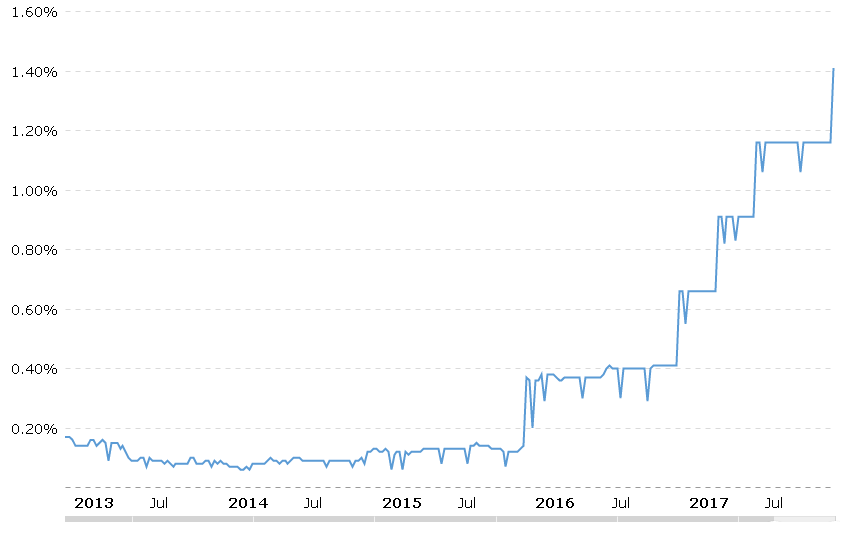

Lows of 2008 made a PE of 11.2 when FED interest rates were around 2%. Current rate is 1.20% and rising. Nonetheless, I think it is the equation of supply and demand that is more important.

No entity borrows money from the banks to invest in the stock markets. At least not retailers. And this rise is fueled by retail investment, which is very sentiment driven, and less logic driven. And Sentiment swings.

FIIs have exited India in throngs because of this: Interest rates are rising.

Low FED interest rates were expected to revive the economy. But that has not exactly happened. World is still in recession. Leaders now believe that interest rate discount is a spent force, and are hence increasing the rates since 2014. This is the main reason for FII to take money out of India/Asia.

Consider this. If the retail sentiment were to swing, and FIIs are already on the way out because of rising interest rates, then who will support the market?

Retail sentiment was a little shaken after the outcome of Gujarat Vidhan Sabha election. On the day, Sensex opened a 900 points lower. Sentiment is nobody’s friend.

Other negative parts -

(1) Oil price going higher & higher - fiscal deficit math of Govt. can disturb. Raw material price to many industries could go up as many raw material price directly proportional to oil price (Paint, Plastics, Solvents, etc.). Hence, negative impact on bottom line of many companies.

(2) Higher interest rate - Higher borrowing cost. Many NBFC/Debt based business could get impacted as their cost of borrowing increase - direct impact on bottom line.

That is not correct way to look at it Fed rate in 2006-07 was between 4-5%. Fed rate was rapidly reduced in 2008 as response to economic conditions. Also, we can not keep hoping for a PE which is produced by an apocalypse like 2008.

If market fell by 50% not sure how many with cash holdings will have courage to deploy.

Not to say that markets are not stretched and will not correct. We need to move with caution but timing the market - not sure.

Just to add, I am a large cap investor with min 5 years horizon so riding the wave works for me. Small caps with so called moats (which are very temporary) will need to be nimble footed and need to have entry and exit strategy.

While we are the discussing the index levels, it’s worthwhile to look at valuations of individual stocks. I believe most people on this forum are stock pickers and that is what really counts.

Having said that, I’m having a hard time finding value in stocks with good fundamentals. Value is only among stocks with weak fundamentals and some of them may turn out to great stories over long term, many other could be value traps. There would be some speculation and luck involved in making money out of these and if there is a general market correction, one can lose a good deal of money.

Exactly my thoughts. Every single midcap I track is at PE 40 or above. We are being told that at current low interest rate environment and all the money flowing in, this is justified. I am not sure if it is. Also given that 2017 has been a very low volatility year, 2018 will not be so. I am also estimating that Modi will go for LS polls in 2018. Hoping to get better entry points in my fav stocks.

Governments like USA’s have borrowed so much that they can’t increase the interest rate beyond a point, even if they want to… Their budgets will go out of control if they increase rates beyond a point…

While interest rates globally are unlikely to rise rapidly, I think it’s the trend which matters and not the actual rates.

Stock market is a discounting machine and as people start seeing rates go up, they are going to extrapolate them into future and sentiment is likely to be impacted.

No no, everyone knows that they can’t go up beyond a point… As the interest burden on government debt will explode… See Japan Govt debt for example… USA is heading in that direction in future… They simply CAN NOT increase rates beyond a point…

Some disagreed when the conversation came to Nifty easily reaching PE 17 and said that a 35% correction (from 10400 to 6700) is a very distant possibility.

On the other hand, some of us seem to consider 6700 to 7000 a strong possibility as it is only a 30 to 35% correction away. This sort of a correction does not need anything apocalyptic to happen, as it has happened several times before, in fact every 5 years or so.

maybe its the new normal nifty PE now and this bull market is quite matured and i dont think we can see 9000 unless there is a big geopolitical issue which can rattle all financial markets…who are we to decide if its expensive or not…let mr.market decide…people waiting on corrections will remain in sidelines and they are bound to buy at higher prices