So lot of individual stocks are still reasonably priced, some are at stretched valuations like HDFC twins, Maruti, Asian paints and HUL. Some are distortions like SBI and airtel.

Issue is with mid caps and small caps trading at 30+ PE(on top of only recent earning growth) rather than HDFC trading at 25. Former has chances of permanent loss of capital as there is temporary spurt in profits as well as PE expansion. Both may vanish together.

I think liquidity will keep this market afloat for a bit longer (Maybe at least till December when we complete 1 year of demonetisation). August saw the biggest FII outflows and still Nifty is marching unperturbed. The divergence in FII flows and Nifty trajectory is very apparent post demonetisation. Ownership has shifted considerably to Indian hands from FII hands in the last few months.

Since Nov 2016 while FII have sold off, DII have bought at the rate of 1 billion USD per month on average with a purchases peaking at 3 billion USD in August!

If the DII inflows continue at this rate FII selling will become inconsequential.

Unlike FII money DII money comes in via MFs SIP which does not quickly disappear.

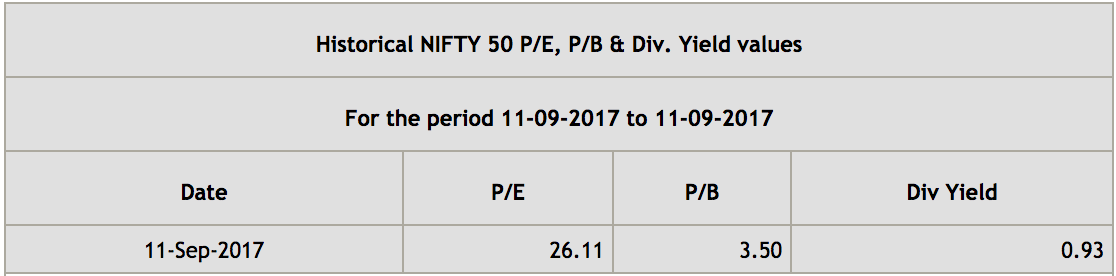

But of course, nothing to worry, there is growth coming, the PE is not high and reforms will take us even higher. The Nifty PE will become 32 X so everyone gets 20% return from here in the next one year, but that is conservative, it could even become 37 X because we all should generally make 35 to 40 % returns. We have 5 trillion coming by 2022 and India is at an inflection point.

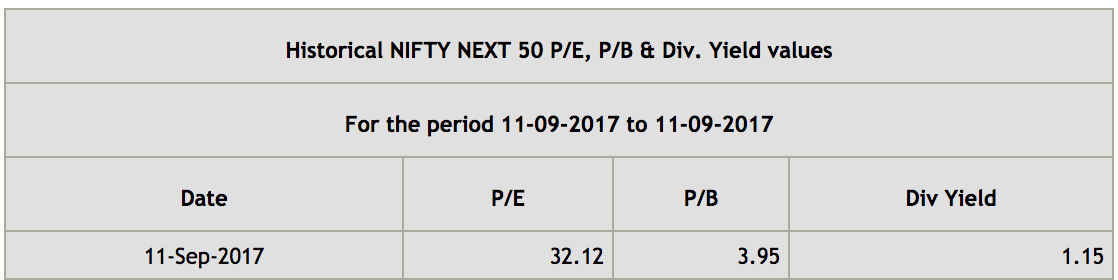

Nifty Next 50 is already 32X. So we should see 40X now. GST is so good, we should trade the indexes at 40-50X. This 32X is the new normal.

Sorry if I am my sarcastic self right now. The last time the Nifty crossed 26X was only in 2008. But this is not the same that was then and is old school, Lets all buy stocks.

FII has become little insignificant anyway. According to couple of fund managers, given the strong inflow in DII, any dips which will form based on FII outflow will be bought out by DII. This seems to be the case.

Looking historically, Indian Markets are costly, valuation are higher. But if we look across asset class, there is not much choice either. Traditionally FD, Gold, RE are the investment avenue for Indians. And at present, stocks are looking better for investors, given low interest rate for FD, gold being stagnant for last three years and kind of stagnancy in RE.

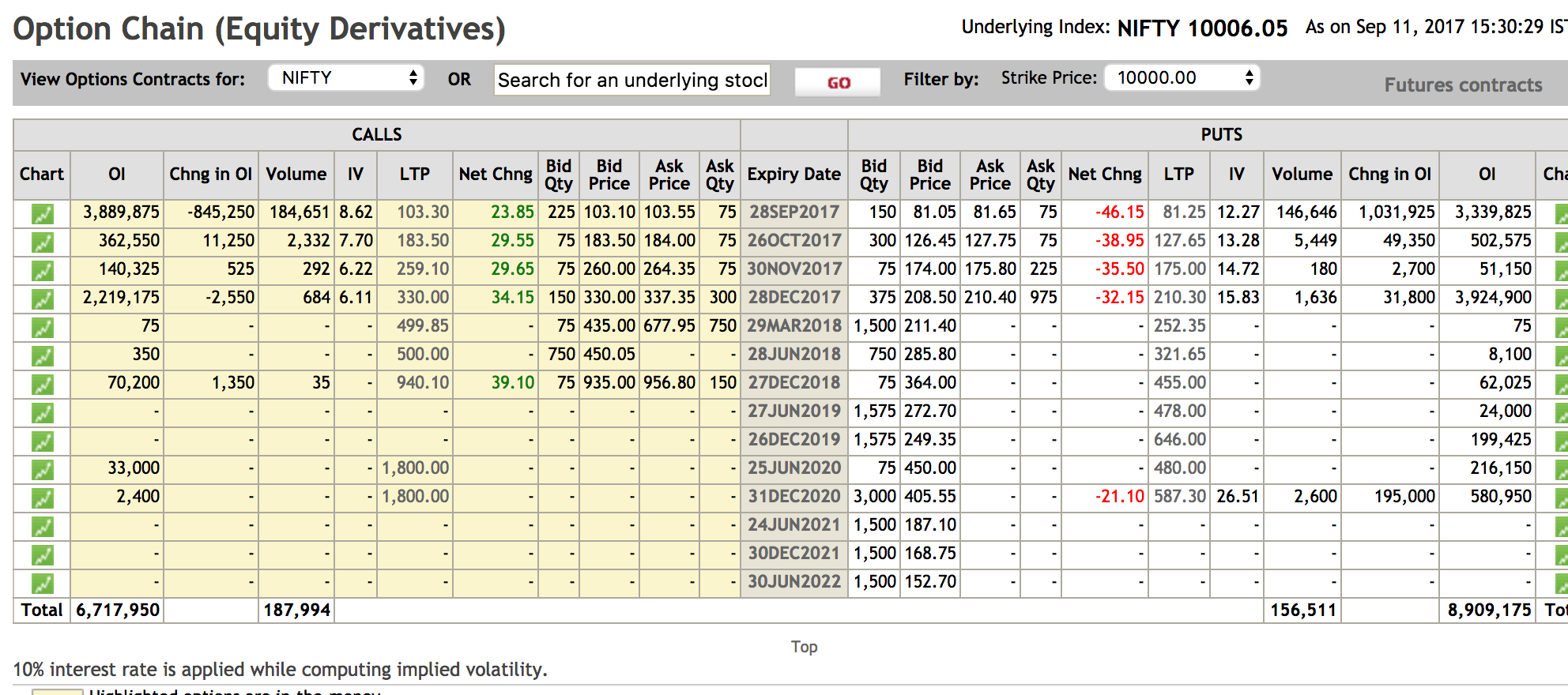

@valuestudent I share your bearish outlook b/c valuation on the markets, while have the same concerns about taxation as @sajijohn. What I have done instead, is to buy long dated NIFTY put options of notional amount ~100% of my portfolio. In my case, these are the December '17 NIFTY 10,000 puts. These cost only ~2.5% of notional to hedge against any decline from these Nifty levels by December '17 end.

Why is this a good hedge?

This works out to be ~8.5% annualized to protect against any declines, while preserving the upside for any bull market euphoria - remember, bull markets die on euphoria - we haven’t seen any of that yet. Yes, valuations level remain high, but that is also partly the result of low interest rates in India and around the world. US 10 year Treasuries trade for 50x P/E! with 0% growth This way, we preserve all the potential upsides, while hedging completely on the downside (might not be complete if you tilt towards small/midcaps which have higher vol, like me but 150% should be a decent hedge). Additionally, they have significant tax saving implication since you do not need to sell of your existing holdings, except to fund the cost of the hedge.

Also, throwing in my hat into the hit and miss world of market timing, I still remain bullish on the markets for the short term. The real driver of this bubble, are the bond markets, driven by up central banks printing money and bidding for assets. As long as the major central banks remain easy and keep printing money - the BoJ is the top 10 largest shareholder in most japaneese corps, while ECB has run out of government securities to buy and is now funding corporates (!!) - this rally will continue. In fact, with treasuries at 50x, I except companies to keep levering up and issuing debt, increasing their EPS thus powering the bull market with earnings expansion and leading the way for multiple expansion.

Did you know? Netflix can now borrow money at sub 4% rates despite being rated near Junk and burning cash? Tesla at sub 6%? As long as companies can get easy money from yeild starved bond markets, they’ll continue buying back and expanding share prices…

Thanks @sarangg. I have been trying to learn more on this to hedge my portfolio but no experience in puts or how they operate. Did learn a bit from Yogesh Sane @Yogesh_s. Hopefully I can figure this out and that seems the only way to hold on to a portfolio right now. Much appreciated.

Yeah I agree, they are especially worried about a market selloff if they ease, so they remain on tenterhooks about ever stopping liquidity. One school of thought about the central bank’s actions, actually is that they will cause hyperinflation, once the massive amount of money they have printed reaches the real economy. In such a situation, cash would fare horribly, as would bonds. Equities should rise in nominal terms, (i.e. share price should increase in rupees), but lose in real terms, with only gold increasing in purchasing power. Its a fools errand to try predict the next crisis though, we’re better off protecting against it (such as by buying gold/hedging)

You are right in your assessment that the Indian markets are trading on the higher side of valuations. But at the same time we should remember that:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” – Peter Lynch

The sole purpose of the market is to give you a real time quote about the companies you are interested in

The other purposes are secondary and except by some exceptional individuals no lasting wealth has been made by timing the market. Market timing has contributed far more to wealth destruction than any other form of investing. Market timers are popular though I give you that. They are in the news and receive the greatest amount of attention and books get written about them and by them but over the long haul they die poor.

A collection of great businesses generating free cash with shareholder friendly management - held for a long period of time through bull and bear phases with extreme amounts of patience still remains the gold standard for lasting wealth creation.

In my opinion, irrespective of market levels, one should do the following if :

holding stocks, if a share seems highly overvalued, even for a fundamentally good company, reduce allocation. It can be increased later when value emerges. Of course, there could be some subjectivity in assessing the valuation.

holding mutual funds - shift allocation from mid-small cap schemes to large cap/balanced funds or debt funds. This shift may be only 10-15% of overall portfolio value.

While it is very hard to time the market, some precautions can reduce capital destruction in case of unforeseen event. On the other-side, there is always a risk of losing some upside.

There’s another way to look at this. Your portfolio is already down 2.5% (plus brokerage) after this trade. You have time only till December '17 to recover that amount, let alone see any upside (after taxes and brokerage). There’s also an underlying assumption that your portfolio moves up or down with NIFTY. What if NIFTY moves only a little, and your portfolio tanks? This isn’t an insurance product for overvalued stocks in your portfolio. I wish you good luck though!

As for “US Treasuries @ 50x P/E with 0% growth”, you should also mention that there’s almost zero risk of downside with that trade. You are assured of 2% return on it. Not much, but safer. Comparatively, equities @ 26x P/E may sound cheaper, but definitely riskier.

Here’s a Warren Buffett quote:

“I would like to say one important thing about risk and reward. Sometimes risk and reward are correlated in a positive fashion. If someone were to say to me, “I have here a six-shooter and I have slipped one cartridge into it. Why don’t you just spin it and pull it once? If you survive, I will give you $1 million.” I would decline — perhaps stating that $1 million is not enough. Then he might offer me $5 million to pull the trigger twice — now that would be a positive correlation between risk and reward!

The exact opposite is true with value investing. If you buy a dollar bill for 60 cents, it’s riskier than if you buy a dollar bill for 40 cents, but the expectation of reward is greater in the latter case. The greater the potential for reward in the value portfolio, the less risk there is.

August has received Rs.21,000 Crore net inflows which is the highest ever. The second highest is a scary comparison from Jan 2008 which stands at Rs.12,717 Crores. Current SIP money is within touching distance of Rs.5000 Crore. These are some insane numbers to contend with.

There are three months in 2017 out of the top 10 highest MF inflow months. Something about that reminds me of Cricket and how the fastest 50s and fastest 100s or even just the number of them being scored have kept getting better over the years with better bats and batting friendly rules and so on. No matter how much a Boycott or Gavaskar whine about bigger bats and mistimed shots going for six, things may just have changed, as with the NIRP regime.

Brokerage should be negligible if you are using a discount broker - under Rs. 200 for 5 lots buy & sell for a Rs. 35 lakh portfolio (literally 1bps). As far as 2.5% goes, it was just an approximation. Recent quotes indicate 1.8%, which works out to be 8.5% annualised. The operating assumption being that my equity portfolio will generate atleast 8.5% a year (i.e. I won’t be down in nominal terms…). Obviously, I have no business attempting to manage my own portfolio if I can’t manage that kind of a return. I realize that the variance of returns means that it will probably be way different than that in a short time period, but just to clarify, this isn’t a short term position, and I intend to roll it over until overvalued market conditions end.

Thus, the only risk remains that NIFTY moves and my portfolio crashes. This is a risk I am fine with, I don’t expect my portfolio to mis-track the NIFTY by over 20-25% (unless there is a structural problem/news in one of my stocks, which a risk that exists regardless of market valuations), which is anyway a level of volatility I am fine with.

Coming to US Treasuries at 50x, I am talking about the 10 year treasury, which yields a hair over 2%. This isn’t risk free - there is huge interest rate risk (duration is ~8 years, so a 1% interest rate move means an 8% loss). Now you might say, oh, well just hold it to maturity. In that case, I don’t think any intelligent investor views stocks as being risky if they just waited for 8 years, obviously the concern in this case is a 1-3 year bear market/crash b/c high valuations.

Not sure what your WB quote means in this context.

Look, no strategy is perfect for everyone. For me, I am trying to hold onto my stocks that I have been holding for a while, for the next 5-8 years. I am, however, scared of overall market levels, (not the valuation of my own stocks), and given the high beta nature of deep-value stocks, I am worried they might crash along with the overall market. This allows me to take a small haircut (8.6% a year), while covering all of my downside. However, I get to hold my portfolio no matter what - if they go up, I participate in the upside, while if they go down, I have additional cash in my portfolio (due to the hedge) that I can use to buy stocks at bargain valuations.

Now if you are confident in your ability to hold through a crushing bear market, like a lot of seasoned investors on this forum (@bheeshma, ayush, donald etc.) because you’ve done it before, you don’t need to handicap your long term returns by sacrificing higher short term volatility.

I have tried doing this in the past and for me it was ( and is) very difficult psychologically to buy things back at lower levels once i have sold them. Either they go up after i have sold and never come back down (very painful) or they go down (or sideways) after i have sold and doubt is sown in ones head which when coupled with other good opportunities that always seem to crop up during that period take your attention (and money) away from what is important ( which is holding on to good businesses) and you are forever trapped in this cycle of timing.

Over time, i have learnt to welcome these fluctuations and formed a view that returns you make are a payment that you have to make for tolerating them.

This way, we preserve all the potential upsides, while hedging completely on the downside (might not be complete if you tilt towards small/midcaps which have higher vol, like me but 150% should be a decent hedge). Additionally, they have significant tax saving implication since you do not need to sell of your existing holdings, except to fund the cost of the hedge.

This way, we preserve all the potential upsides, while hedging completely on the downside (might not be complete if you tilt towards small/midcaps which have higher vol, like me but 150% should be a decent hedge). Additionally, they have significant tax saving implication since you do not need to sell of your existing holdings, except to fund the cost of the hedge.