Lol, which commodity has increased price 10%, I’d like to know.

This is called relative valuation (one asset class vs the rest), not intrinsic valuation. And it has its limitations. You have a sound premise (no other asset class providing comparable returns, lots of money flowing into equities, GST reform, more formal economy etc.)…but like Buffett says, you are more likely to lose money with a sound premise than a wrong premise. Armed with a sound premise, risk management takes a backseat, people think 24 P/E is the new normal and start paying high prices.

From a contrarian point of view, I certainly think Real Estate, with its recent reforms (RERA, Demonetisation) could do better. Rentals are on the rise, which could renew interest in real estate investing. Who doesn’t want a buyers’ market?

I also feel Gold, much below its 5 year highs, is a good hedge during these times. Gold is a necessity in India and gold import bill is set to hit 5-year high in 2017.

3 Likes

I agree with you and the gentleman in the video on everything except gold  According to the same gentleman in the video, gold actually does nothing but sit there, it is a non earning asset. That’s what had opened my eyes to the absolute lack of value of gold.

According to the same gentleman in the video, gold actually does nothing but sit there, it is a non earning asset. That’s what had opened my eyes to the absolute lack of value of gold.

Warren Buffett on Gold

1 Like

If you look at the 2 statements above, they are self-contradictory. I agree with the 1st statement, but have a diametrically opposite view on the 2nd statement. If you think a bit longer about it, the USP of gold is its stable value over long periods of time (think centuries or millenia). At a time when Central Banking induced credit cycles are wreaking havoc on economies, gold is rocksteady in it’s value.

On a separate note (and slightly tangential to the main topic), Ray Dalio, CIO, founder and ex-CEO of Bridgewater Capital has written an excellent article on Linkedin titled Central Banks’ Reversals Signal the End of One Era and the Beginning of Another which everyone having even the slightest interest in global macro should read. Excerpt: “our responsibility now is to keep dancing but closer to the exit and with a sharp eye on the tea leaves”. This is eerily reminiscent of what Buffett said in 2000, and some CEOs of too big too fail banks advised in 2007 to “keep playing (musical chairs) till the music is on”.

1 Like

Note that I talk about Gold as a hedge against risk, not a long term investment. Generally (but not always), gold moves in the opposite direction of the dollar and the world economy. Moreover, gold is also known to neutralise the risks of inflation and deflation. It has its use as “portfolio paperweight.”

1 Like

@chintans When I re-read how I phrased my words, you got me

And… I did forget to read Dalio this month. Thank you for sharing and oh boy… his words… “Recognizing that, our responsibility now is to keep dancing but closer to the exit and with a sharp eye on the tea leaves”. They make me smile with happiness in my heart with a cash ready portfolio. I always did envy those guys who had cash in 2000 and 2008. We shall get our day in the sun too…

It’s not a matter of if, it’s just a matter of when.

3 Likes

What is best store for cash in India. Will bond and gilt prices hold their levels in massive draw downs.

Bank account. In a good bank.

One important thing I have learned and with some effort fixed as a mental model: Cash is also a position.

3 Likes

Gilts are the most dangerous in a rising interest scenario. Suppose you buy a 30 year gilt bond with for 100 Rs. @ 6% interest. So maturity value is Rs. 574. On the other hand I did an FD and have Rs. 106 after 1 year. Now if I buy a 29 year gilt bond @ 8.5% interest, the maturity value would be Rs. 1129. Since there is a lot of supply of the paper I am buying and it sets the marginal market value, the market value of your gilt bond becomes 52% of the original. So after 1 year your 100 rs. becomes 106/1.96 ~ Rs 55 (1129/574 = 1.96); mine is worth Rs. 106. If cash is the only option you would consider, try 1-3 year SBI FDs. The shorter the tenure of a debt certificate/bond, the closer it resembles your intuitive understanding of cash.

1 Like

You may have to wait a long time though…the market may not correct immediately, move sideways, or correct only a little. No signs of violent corrections (like 2000 or 2008) anywhere. However, Dividend Yield for Nifty 50 and Nifty 500 are 1.0 and 0.94 respectively…historically, wrong time to buy.

Disclosure: I sold 1/3rd of my equity portfolio and part-prepaid my home loan. Added some Gold, but 2/3rd is still invested in stocks.

2 Likes

Hey @vasuadiga, I like your thinking. And I loved the steps you took. They are superbly awesome. Just asking and sure may be financial considerations; why not pay the home loan in full?

Now I will share something I am thinking about…

But first the disclosure - Basically I have what some might call a crazy mind And thus my questions to myself below.

Here’s a question? How many people would like to be just 1/3 as successful as WB? I for one would be fine with that, So, his CAGR over such a long period of investing have been 20 % odd… So then, today, Indian banks giving 7 odd percent is taking me to 1/3 of WB. Then why use my head too much if I want to avoid in Peter Lynch’s words “In home casino care”. I must disclose I pay no tax on my interest income as a privilege of being an NRI so yeah, I have a better deal. We cannot compare the US bank yield to our yield. They are on different planets so why are our PE’s as high as theirs.

I have even seen a guy asking on this forum on how to achieve 26% CAGR over 10 years… I was like ROTFL big time. He wants to beat WB and Lynch without realizing it.

Now, we have some newly minted millionaires / billionaires who are now already feeling that they have learned something spectacular and special. All they have been investing for a decade or just over it. The fun will be watching it over 3 decades. I have a feeling we will not be able to even recollect most of their names in some years

Here’s the thing… Lets say I take a random figure… 1 Million… keep compounding for 10 years at 26%. I will end up with 10 Million. Then all it takes is once a decade or so drawdown of 50% and they are back at the growth that index investing would have offered without using any brains again.

Now an even more fun scenario; every here sort of knows of the 1929-1930 drop of 91% on the US indices. I want one honest answer on who thinks it can happen again? Nowadays, we are more ready for 10 to 30 with a maximum on 50% drawdowns. Lets say, I was betting on a new high… a high drawdown of 95%. What is the probability? Bhai, I don’t know. So I also keep a percentage invested Hedging Hedging.

The biggest issue is people feel loss of profit if they had stayed invested… I have no such feelings; I feel bigger issue if I actually was to lose money. The percentage I gain is happiness for me because I am not comparing the size of mine to the size of someone else… BTW, I have a decent size

And on the signs of correction; did we have any in the past 1929, 1992, 2000, 2008… actually yes we did… things were going too damn well… hmm… aren’t they going to damn well now?

So then another issue specific to VP… everyone is aware and on some sort of alert level and this is making us think that everyone seems to be aware of it so then maybe it is not the time… All of us need to realize that this is only specific to VP, where we are turning cautious… the real retail is who has not heard of VP is pumping in money like mad… the MF inflows show it. Since we see caution here, we seem to think there is caution everywhere. We have to get this clearly in our head.

Now risk reward; I have made some money, I am content, now if HUL (replace with your favorite stock name) doubles from here on in 12 months, I don’t mind it and happy for those who where in it… I am currently quite happy with 7%.

And to your first point last; I may have to wait for some time; sure, it’s not like I get nothing for it, I get 7% so why not chill.

PS: there is also some stock I am betting on, but not so much on how much I can win, but on now it may not lose me much cash since it is in the money. Stay bearish, and say yes to only a very very little few. Thats my current mantra.

I am actually quite pleased with what I have. So no pressure to get rich quick. I also suspect, you are somewhere in the same no pressure zone.

Have a good evening and please let’s keep the thoughts flowing.

5 Likes

Nice discussion.

I have even seen a guy asking on this forum on how to achieve 26% CAGR

over 10 years… I was like ROTFL big time. He wants to beat WB and

Lynch without realizing it.

Isn’t WB’s genius in having generated the return that he has for his portfolio size of billions. I have heard him say that he would beat the hell out of every index if he had the PF size of a few millions. So, 26% CAGR for 10 years for a portfolio of a retail investor may not be outlandish. Please feel to correct if my understanding is wrong. It will be a great learning before the next crash ![]()

2 Likes

Don’t you have to pay US tax on Indian interest earned?

Yes, you have to pay US tax for Indian/worldwide income if you are a US tax resident. Not just for interest, but for PF interest, long term capital gains and dividends too.

Typical US inflation is 2-3%. If Buffet has made 25% CAGR then he has beat the inflation by 22%. If India’s typical inflation is 8%, then you need 30-31% CAGR to match Buffet. For instance, a guy in Zimbabwe may make 50% CAGR in a 50% inflation - it means nothing.

The inflation and risk free rate needs to be accounted for when calculating P/E, Returns, RoE etc. For example, an RoE of 20% for US company is 17-18% above inflation. 20% RoE for an Indian company is not all that great.

3 Likes

I am not in the US. There are places like Singapore and Dubai where you don’t have to pay tax on foreign income.

@prem_shankar I know I am not WB :). I am grateful if I can hit 12 to 15% and if once in a while I get a good ride above it I am even more grateful.

Please do understand that I am not a proponent of high valuations. I am a pure value investor and absolutely finding difficult to get investment ideas in my value paradigm. Low full tosses are getting increasingly difficult to find.

What I’ve elaborated is what I’m seeing in the market. More and more people are getting into equity. Friends who used to say “Share market is gambling” just a year back are now coming and asking advice about investing in equity. That does make me cautious.

Most of this rally is driven by huge liquidity and due to almost no choice of other investment avenues. We have to decide whether we want to sit on sidelines (which many have been for 2 years now) or participate with our high conviction ideas. I’ve opted for the later. Fully understanding that one can get a good cut in portfolio. But then portfolio has been giving 60% CAGR in last 3 years, so definitely can take a 30% cut.

-Jiten Parmar

5 Likes

This is inspiring and sobering at the same time.

Inspiring to know that value investing works and there are some great examples like yourself on this forum. Thanks for being an inspiration to all of us on this forum.

Sobering to know that the high returns earned by my portfolio in the recent years is due to the process and not because of any special talent / insight that I have.

1 Like

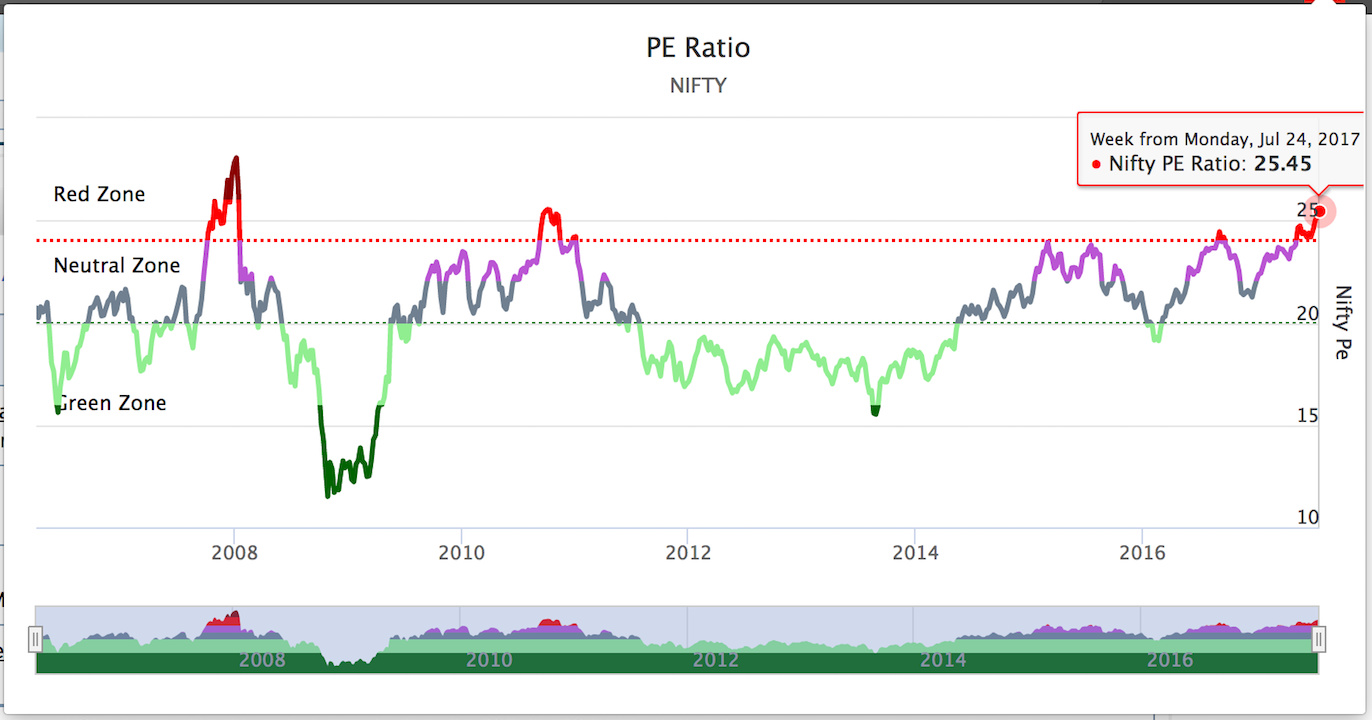

Gentlemen. We have a wonderful visually explanatory module built and shared by @sandeeprawat and I recommend anyone to install it.

This is what it shows today.

Inferences can be drawn. Basically, what I see is that even if we get a very set of good results, the PE ratio might decrease to 23.5 or so if at all as there might be laggards too… but more importantly, how many times have we seen such exuberance over the last 10 years… and what has followed. This very wonderful chart which auto updates would keep anyone sober and also give courage when it is the right time to invest from a pure Mr. Market perspective.

4 Likes