Here’s a few things to think about… experienced team members please do contribute with your learnings and experience.

-

Let’s go back in time and read what Prof. Sanjay Bakshi said about the NIFTY PE Ratio: http://fundooprofessor.blogspot.ae/2005/07/reflections-on-indian-stock-market.html

-

Lets see this chart which is available at Craytheon for 3 Year returns (based on the prof’s data) which shows returns based on the current PE multiple in the future (please use the link as I did not want to copy the image without permission) Nifty P/E Ratio, Price/Book Ratio, Dividend Yield Chart

Now, since the above links have one old musing (albeit among the most intelligent) and one technical chart which may not tell us about today, let’s look at some current data.

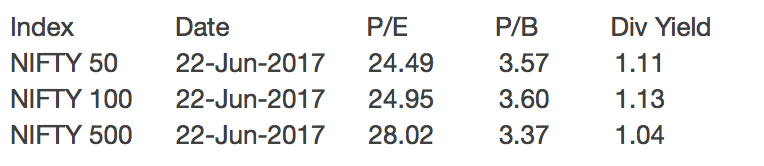

Current PE Ratio’s:

So lets get this clearly… The Nifty 500 is trading at a PE of 28. Which sounds crazy to me at-least.

Ok, for the courageous, here’s the next one…

Small caps indexes with a PE of 100? Hmm… when did we hear that last? Or maybe… “this time it’s different” ![]()

Now to the psychology part…

First a definition of “psychology” from Wikipedia.

Psychology is the science of behavior and mind, embracing all aspects of conscious and unconscious experience as well as thought.

We have been hammered with the below in our minds for behavior…

- We have to be a buy and hold investor… with references to Warren Buffett and the likes.

- Look at the 20-30 year chart… In the long run it works out… this conveniently excludes the logic of investing.

- All big investors are always fully invested… yes for those with a net worth of a billion dollars it might be acceptable to do that… what do changu, mangu, yourself and myself do?

Bigger issue: We convince ourselves of bullshit…

I hold only 10-12 or 15-18 PE (define your range) stocks so this should not affect me… nonsense. when things will happen they will happen everywhere.

–

Now my thoughts and actions…

At these prices can I hold on expecting to find a greater fool? I think the final fools are standing close to the frontier… how far can foolishness go? only a fool with money will advise us.

I became 50% cash at the start of the month, and became 60% cash today. Maybe I am being stupid… I think better stupid that poor.

Do note I am still 40% invested.

What is driving this foolishness…

As the previous person Deepak who posted above… It seems like all bad news is shut out and good news makes rallies. That is true. The huge impending bankruptcy of some major companies as directed recently also barely had an effect.

If I may address the elephant in the room… are we discounting logic in the name of “one person who will change everything?” should we include changing our logical thinking in that?

Stocks can only rise for fundamental reasons… the fundamentals say, don’t be mental.

Now lets see the price multiple of a bellwether stock… Hindustan Lever.

It is a stock that has been known and recognized for a long time and even then it’s multiple has risen from average of lesser than 33 to 52? And everyone is behaving rationally?

I remember peter lynch had mentioned in one of his books that PE should be equal to growth so is it growing at 40 to 50% a year?

In all this we sometimes forget what we learnt when we came in… you make money in stocks when you buy low and sell high… then we forget to sell.

These are my thoughts anyway and I am sharing them with you… would appreciate comments laced with experience.